By Roger J Kerr

Understandably, there will an intense focus on the RBNZ’s inflation forecasts for 2016 and 2017 in this week’s Monetary Policy Statement.

The benign inflation environment we have experienced over recent years is about to abruptly change as oil price swings and the NZ dollar currency depreciation shunt annual inflation sharply higher.

Anecdotal evidence from our diverse client base across corporate New Zealand suggests that significant price increases are already under way.

Whether this price setting behaviour is higher than RBNZ expectations holds the key to how actual inflation tracks against RBNZ forecasts over the next 12 months.

If the NZ economy was weak most companies would not get away with significant price increases for their products/services as they would fear a loss of sales and market share.

Outside reduced spending from dairy farmers and the businesses who serve the dairy industry, the NZ economy could not currently be described as weak.

Construction and tourism sectors are very strong, new vehicle registrations are at record highs, services are very robust, retail spending is boosted by rising house values/record low mortgage interest rates and manufacturing exporters are buoyed by the much lower exchange rate value.

A small minority of manufacturers selling into the mining and oil/gas industries around the world however are experiencing reduced demand as customer spending and investment levels are slashed due to tumbling commodity and energy prices.

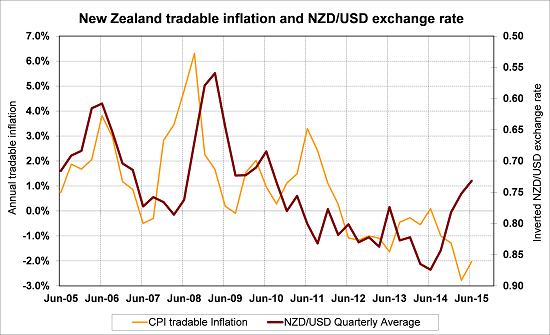

The historical correlation between the NZD/USD exchange rate and tradeable inflation has always been very close.

The 28% depreciation in the NZD/USD rate from 0.8800 to 0.6300 over the last 12 months reliably points to annual tradable inflation increasing from -2.00% to well above +1.00% over coming months.

As the chart below depicts, the quarterly average for the NZD/USD exchange rate (red line) will continue to fall to below 0.7000, potentially suggesting even higher tradable inflation to +2.00%.

On the assumption that non-tradable inflation (domestic prices not impacted by the exchange rate) remains stable at its current +2.0% level, the overall annual CPI inflation rate looks set to increase sharply from +0.4% to over 2.00% over the next nine to 12 months.

To subscribe to our daily Currency Rate Sheet email, enter your email address here.

Daily swap rates

Select chart tabs

Roger J Kerr is a partner at PwC. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

47 Comments

Cripes, imposing the current NZD/USD rate on the above graph for the September guarter forecasts a ~4% tradable inflation rate. Will the RBNZ just look through this higher component CPI horizon as irrelevant and cut the OCR with impunity?

So as that 4% takes yet more money out of ppls pockets the RB will raise the OCR? and take out even more $s, bound to end well.

LVR's at 90% on steeply rising Auckland property prices deterred very few. I guess the total interest bill is the same if not higher than when the OCR was 8%. Speculators can only be cured of their obsession with penalty interest rate levels.

You mean by borrowing money overseas and sending the interest to Singapore / Hong Kong / Japan instead of a New Zealand Financial institution?

Which New Zealand financial institution might you be referring to.

TSB, SBS, The cooperative bank, etc, etc. You know the ones that employ New Zealanders instead of being wholly based overseas and look only at your ability to supply equity in their local currency ?

Disclaimer: I have not personally moved my mortgage overseas yet because i believe that there is still significant downside risk for the NZ Dollar. If the Dollar drops below US 0.55 then I will in all likelihood switch to a Singaporean dollar mortgage at circa 2.5% pa. At this time I believe that the NZD will have upside potential from the aforementioned level and that even if the NZD does drop further I will have roughly 2% worth of buffer ( the difference between NZ rates and SGD interest rates)

Oh, and their share of the market is? And I believe they enjoy the same OBR funding backstops as the rest.

The OBR backstop is irrelevant to borrowers who are considering foreign mortgages instead of your proposed 8% penalty interest rates?

It is irrelevant to borrowers who are considering foreign mortgages instead of our current 4.35% "penalty" mortgage rates.

Is it easy to switch your mortgage to an overseas bank? Lloyds used to to offer expat mortgages with currency switching for foreigners in S'pore, Japan, and HK but you couldn't be a resident of the country you were from.

HSBC offers foreign currency mortgages if you can offer sufficient security in that currency or prove income in that currency.

OK, but it seems like you think you can get mortgage funding from an offshore bank. I don't think you can. For ex, if if you swanned into Tokyo Mitsubishi looking for a mortgage on NZ property, I think they'd look at you odd.

Maybe, but if I walked into OCBC in Singapore and asked for an overseas property loan ( http://www.ocbc.com/personal-banking/Loans/overseas-property-loan.html ) I think that they would require evidence that I could pay it even if the NZD tanked and then they would give it to me.

Alternatively liquidate an asset here, buy one where you are looking to get your loan and use the rental income from that property to secure a mortgage in that currency for that property. You will also be able to leverage any equity that you put in upfront to use as part of a mortgage for a property here secured on the property there. ( this part is theoretical )

And they would require that you live and work in S'pore. Like I said, this nothing new and you are req'd to top up your loan if the exchange rate works against you. People got burnt badly which is why many banks stopped these loans. They were targeting expats on strong salaries.

http://www.simonconn.com/the-dangers-of-foreign-currency-mortgages/

And no, Tokyo Mitsubishi would not likely give you a mortgage for NZ property. If they did, you'd likely need a Japanese guarantor. As a non-resident of Japan, you'd be lucky to open a savings account.

The ONLY thing relevant for borrowers with foreign currency based loans is the potential for currency fluctuations! Maybe just ask the polish government why they banned swiss currency loans in their country...

http://www.bloomberg.com/news/articles/2015-01-15/polish-banks-zloty-sl…

Bingo - I knew of a NZ based outright CHF mortgage debtor at 3% a few years back - The rest is history - liquidated. Hedging the foreign debt through the forward FX market kills the interest rate advantage. Unless, like our banks, currency swaps are employed on the domestic debtors behalf. - but this a market only open to wholesale accredited players.

dp

Can you please explain how ppl / businesses with no more money pay for more expensive things?

impunity? as in someone criticise them as doing wrong? What is the state of inflation in the tradeables right now? -1%? So in effect the tradables will see a 5%? increase in their costs but without a monopolistic market cannot pass any or most of that on to consumers as consumers have no more money.

impunity? as in someone criticise them as doing wrong?

Yes.

New Zealand central bank Governor Graeme Wheeler needs to get inflation back to target and some observers think he has “plenty of room” to cut interest rates, Finance Minister Bill English said.

“He’s been out of the zone for years now, below the midpoint for quite a long time,” English said in an interview late Thursday, referring to Wheeler’s 2 percent inflation goal. “He’s meant to be following the Policy Targets Agreement, that’s the bit I look at, and one day somebody will start asking the minister of finance questions about whether he’s actually following the agreement or not.” Read more

Can you please explain how ppl / businesses with no more money pay for more expensive things?

Same way I do with lower returns on my term deposit investments

You still have not answered the Q.

Even if your income is fixed at say 10,000 per month if the cost of your debt (think mortgage of about 1,000,000) drops because of lower interest rates (from say 5% or 50,000 per year to 4% or 40,000 per year) then the money that would otherwise have gone towards interest ($10,000 in this example) can be spent elsewhere.

This is a different argument the Q still remains un-answered. As I said if you have $100 how can you spend more? your reply is oh I have $110. That may well work for you as an individual but it doesnt work when many ppl only have $100.

Why is this a valid comment/question? well it explains the symptom of no inflation for the last 7 years in occam razor terms.

(

Your argument supports the contention that lowering the OCR gives a debtor more money to spend, all else being equal), I do not disagree with you.

otherwise in an increasing inflation scenario the argument is as we see inflation the RB will put up interest rates thus your debt "saving" is actually not, it is declining as it costs more to service your debt, not less. This is a double whammy.

Answer is simple Steven.... in Aggregate "NZ" borrows.... we have played this "game" of growth for 40 yrs or more..

We have not learnt anyy lessons from the GFC....and so.. we will keep doing what we do until we have our own GFC..

Govt borrowing....and private sector borrowing.... AND... that credit growth goes around...and around...and we call it "growth"...

Your solution of lower interest rates.... simply encourages "more".... credit growth...

ps.

well it explains the symptom of no inflation for the last 7 years in occam razor terms.

Can u elaborate on this...??? how so..??

Now that RJK has predicted higher inflation we can all rest assured that it ain't gonna happen :) My personal analysis of the correlation between forecasts and actuality on this site indicate that Kimberly Martin is usually correct about as often as Roger Kerr is wrong :)

Yep Roger has been making inflation predictions for the last 7 years.

I hear that even a stopped clock is right twice a day. Maybe in a few years ...

and he has been wrong for 7 years. What has changed to make him right that we will finally see some inflation? is doing anything about it a safe undertaking?

no he isnt and no it would not be.

Annual CPI inflation looks set to increase sharply from +0.4% to over 2% over the next nine to twelve months.

Assuming this does come to pass, and given the exchange rate already assumes 0.5% cuts in the OCR, then the RBNZ would finally be meeting their target. Yet the change appears to be represented as a bad thing.

ppls wallets are in NZD. So if imports get more expensive that clearly signals ppl will be buying less of something. No one has as yet answered how you get inflation overall when many if not most ppl have no more money. If imports do get more expensive and ppl buy less that signals deflation somewhere in the economy and even job losses.

If suppliers' willingness or ability to supply goods and services at a certain price point diminishes, then you can still have inflation overall even with no more money in peoples' hands.

huh? if their ability to charge more "diminishes" or is zero then they have to absorb those increased costs, ergo there is no overall inflation across the NZ economy.

If they have an ability to charge more aka Councils and rates then someone somewhere else loses the ability to charge what they are charging today ergo there is no overall inflation across the NZ economy.

The inflation comes from money that would have been paid back to The RBNZ via interest not having to be paid to it. There is a NET increase in available money when interest rates drop because the rate at which the RBNZ "reclaims / destroys" money is reduced.

This is a different argument, in fact the opposite which I agree with. ie with no inflation or dis-inflation lowering the ratee means a lower payback and hence more spare money. My point is the opposite.

The idea is that imports get more expensive but exports get cheaper. So jobs are lost in import dependent businesses and gained in export ones. Government jobs, central or local are largely immune to this process which is somehow supposed to be good for the rest of us.

There is something deeply messed up with the thinking of the Central Planners at the RBNZ and Treasury, they are intelligent and well meaning but largely clueless about how things really work. The RBNZ is essentially a copy of the US system, hardly a recommendation, as its main purpose is to protect the bank's management from their own stupidity.

"Outside reduced spending from dairy farmers and the businesses who serve the dairy industry, the NZ economy could not currently be described as weak."

Really? Then please explain why NZ business confidence is currently approaching GFC levels?

If the NZ economy was weak most companies would not get away with significant price increases for their products/services as they would fear a loss of sales and market share.

Roger, this only applies potentially to those companies that source their key raw material locally. And if you had the knowledge how the big construction players really think, then you wouldn't make that statement. There are also always some factors at play such as Graham Hart prepping a big float and buying market share for NZ Timber group. Once that is over, prices for basics such as timber or plywood will shoot up. Stuff that is not made locally is going up at the rate of 10+ % already... (and that is only because the overseas supply chains offer a discount of 10-12% to keep stock flowing). No large corporate will run at a loss for too long, almost everyone relies heavily on imports and every larger player knows pretty well what the others are doing!

I guess the RBNZ has to choose which is worse - an economy in recession or a little bit of inflation. To me a little bit of inflation (e.g. 4% or 5%) actually seems like a good thing at the moment with everyone loaded up on debt. I can't see us having any more than 5% inflation no matter how low the OCR went - people just don't have the money to pay inflated prices.

the RBNZ needs to ignore the debt position and focus on inflation and the economy, put it down if needed or raise if needed

if those that loaded themselves up with debt fall over so be it, from dead wood new shoots will grow

Can you please explain how ppl / businesses with no more money pay for more expensive things?

Even if your income is fixed at say 10,000 per month if the cost of your debt (think mortgage of about 1,000,000) drops because of lower interest rates (from say 5% or 50,000 per year to 4% or 40,000 per year) then the money that would otherwise have gone towards interest ($10,000 in this example) can be spent elsewhere.

I have already replied and this is not answering the Q, in fact your comment seems to support it.

In that case the remaining obvious answer is debt.

only 41% of the population own houses and of that less have mortages , its the majority that you need to be spending on consumer goods to keep the economy going so for them less inflation is more important

That 2013 Census data is complicated by "family trusts" - in addition there are an awful lot of people who don't 'own' and don't pay any rent. Presumably because the property is tied up in a 'family trust'.

Corks Roger. Your model of the economy is not working at the minute - evidence your calls on inflation and exchange rates in recent months. Past cycles would suggest the exchange rate will continue to fall. I would suggest that the PPI shows there are low inflationary pressures and corporates would be very courageous to hike prices and margins. I would also note that the transmission from exchange rate rises and falls to prices is muted as many corporates see through the medium term fluctuations.

There has been no meaningful raise in wages for many years for majority barring some top elites , if imports get more expensive then there is less disposable money , would that lead to overall Inflation? I doubt it unless there was increase in wages as well.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.