By Roger J Kerr

The U-turn by the RBNZ on monetary policy signals since their statements in late April/early June has been dramatic, however fully justified in my view.

They allowed monetary conditions in the economy to become too tight by refusing to cut the OCR in April and early June when they had the opportunity to do so.

The RBNZ’s defence has always been that they cannot control the value of the NZ dollar and thus they have to accept that overall monetary conditions can move away from where they would ideally want them.

I have provided evidence over recent weeks that the RBNZ’s non-decisions with the OCR in April and June, in particular, was the main driver pushing the Kiwi dollar higher.

The RBNZ’s reluctance to cut the OCR again (up until last week) was all about the housing market and financial stability risk concerns stemming from that.

However, singling out the dairy and manufacturing export sectors last week, the RBNZ have had to concede that these productive sectors are more important to the NZ economy than the loan asset quality/capital adequacy of four Aussie owned banks.

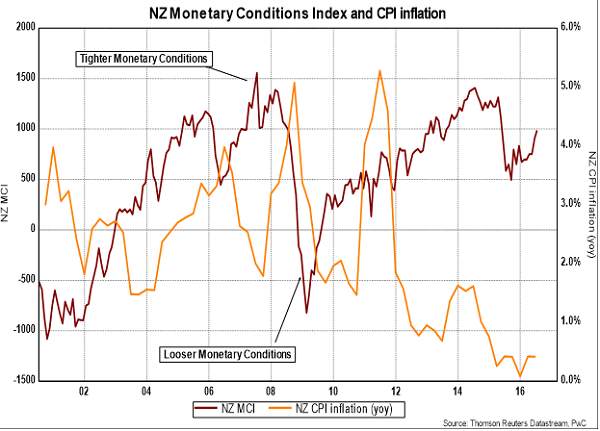

The chart below illustrates why the RBNZ reversed engines on their monetary policy stance last week.

You cannot return inflation to above its 1% minimum if monetary conditions (combination of exchange rate and interest rates) are tight and becoming even tighter.

You promote/allow tighter monetary conditions when inflation is rising too fast and you want to bring it down.

We currently have the opposite requirement!

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.