Economists at the country's largest bank see it as unlikely that all of an expected quarter of a percentage point cut in interest rates next week will be passed on to customers.

The Reserve Bank has broadly signposted that it will be cutting the Official Cash Rate on August 11, with the assumption being that this will take the OCR to 2% from the current 2.25% record low.

In their weekly Market Focus publication, ANZ economists say while the OCR is set to be cut again, "we’re also not convinced actual domestic deposit and borrowing rates will move down by the same amount".

"In March, the RBNZ wanted the full pass through from its cut in the OCR into retail interest rates. It might now be hoping financial institutions hold some of the easing back, given the potential for this to just pour more fuel on the property fire. The RBNZ certainly doesn’t need more house price inflation!"

When the Reserve Bank cut the OCR by 25 basis points in March ANZ only passed 10 basis points to floating rate mortgage customers. (Here's the detail of the savings rate cuts banks, including ANZ, made after the March OCR cut).

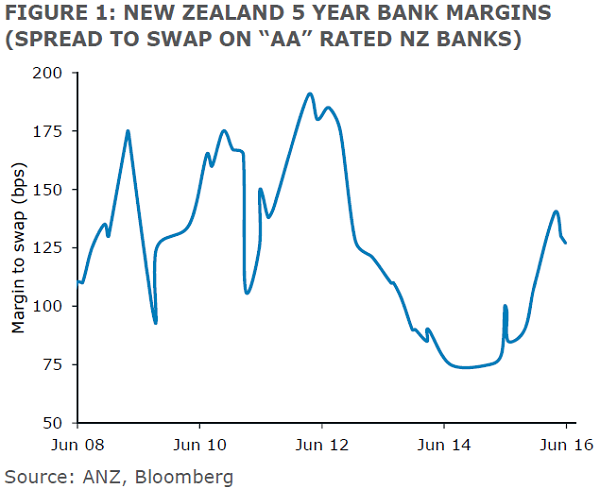

The ANZ economists say offshore funding markets are more expensive than they were in 2015.

"New Zealanders don’t save enough, so offshore markets need to fund the shortfall. Funding costs are therefore trending higher offshore and locally (figure 1)."

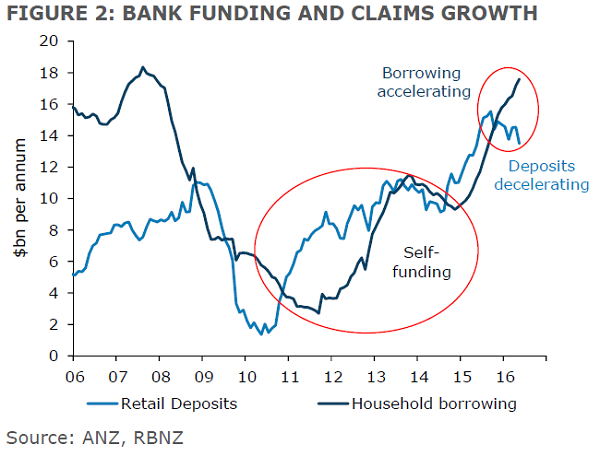

The economists say credit growth continues to outstrip deposit growth.

"For money to go out the door, money also needs to be coming in the door. Banks were basically self-funding post-GFC as deposits grew in line with credit growth (figure 2)," they said.

"That’s changed. There is now more going out (credit), but less coming in (deposits). This gap can be filled by looking offshore (refer point above), but as noted, it’s more expensive and arguably not in New Zealand’s long-term interests to become more dependent on offshore funding markets. Offshore issuance needs to be hedged in the basis swap market (where spreads are widening too). That not only comes at a cost but it chews up capital and credit lines."

ANZ Bank New Zealand CEO David Hisco commented in a recent interview with interest.co.nz's Gareth Vaughan that the bank does try to limit what it borrows offshore.

The ANZ economists say each marginal nudge lower in the OCR puts more pressure on deposits to slow and credit growth to rise.

"There is a limit or a level that if deposit rates fall to, people just won’t want to put money in the bank. Readers simply need to ask themselves how low rates would need to go before they’d revisit what they do with their own cash. It is notable that carded term deposit rates already sit well above the OCR."

Therefore, something has to give, the economists say.

"You can’t logically expect the OCR to fall and for it to be fully passed on to lower deposit rates and borrowing rates in a savings-deficit nation, particularly in one where the central bank is barracking about the increased riskiness of a major component of lending – housing.

"It seems inevitable we are going to see more of a scramble for local deposits in the coming year, unless credit growth collapses (unlikely) or banks simply keep tapping offshore markets. The latter can be done – in practical terms, there is no shortage of cash around – but from a financial stability point of view it doesn’t make sense. What’s more, if you have to pay up to get offshore money why wouldn’t you price more aggressively to attract local deposits?"

Therefore, the ANZ economists say it seems likely the OCR will fall but borrowers won’t get the benefit of the full 25bps.

"There will be angst and complaints. Ironically, not much mention is made of the other side of the equation. Each nudge lower in the OCR penalises savers (depositors), if deposit rates follow."

The economists say deposit rates cannot be taken continuously lower, which means the same for borrowing rates. A wedge between wholesale and retail rates will help the RBNZ as it tackles competing housing and currency tensions.

"That is precisely what the RBNZ needs to see as it tackles competing tensions. The NZD needs a lower OCR and lower wholesale rates, while the housing market clearly does not need lower rates at all (arguably higher ones are required). In response to these tensions, a larger wedge between wholesale and retail rates needs to open up, and we suspect it will."

*This article first appeared in our email for paying subscribers. See here for more details and how to subscribe.

36 Comments

BS baffles most of us .................. the real reason is the Banks will seek to protect their margins with whatever they have at their disposal .

Just like Fonterra with the retail milk price

Its called Capitalism

Anyway ANZ are fibbing , the rates for new deposits will almost certainly fall in line with the OCR , it will just be interesting to see which Bank blinks first

Banks are making losses in dairy now, their goodwill is a secret handshake made by the reserve bank....here you go guys this should cover it........desperate and unsustainable

David Chaston has been saying the opposite about banks funding costs. He thought they had been falling. Did I get it wrong, or did David.

Of course the banks would not be telling porkies.

Floating rates (headline) should be at least 1% lower than they are. Right now.

Why?

The ANZ economists say offshore funding markets are more expensive than they were in 2015.

"New Zealanders don’t save enough, so offshore markets need to fund the shortfall. Funding costs are therefore trending higher offshore and locally (figure 1)."

The economists say credit growth continues to outstrip deposit growth.

For money to go out the door, money also needs to be coming in the door. Banks were basically self-funding post-GFC as deposits grew in line with credit growth (figure 2)," they said.

Absolute rubbish - banks are resorting to off balance sheet hedged foreign funding because the Australian parent banks do not wish to stump up more capital to grow banks assets, via local lending which automatically creates domestic deposits. The graph represents a failure of RBNZ bank funding stats to include money values for foreign funding. View note at bottom of this page.

Let's not forget:

Bank of England: "Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits"

BIS: Deposits are not endowments that precede loan formation; it is loans that create deposits. Borio Page 17 of 38

Stephen, I have read the BOE article and watched the associated video and do not think it says what you think it says.

It's debunking the myth that every dollar lent must be a dollar saved by someone (b/c this would imply no increase in dollar stock). The statement about it creating a deposit refers to a matching deposit (liability) with the central bank, borrowed at cash rates. It still owes the money it lent, but to the central bank, from which it 'borrowed' it.

Add to that the dynamic of core funding ratios and liquidity requirements and the central banks expect that liability with it to be switched with another lender ... eg depositors or wholesale funding. Otherwise, the retail banks would not take retail deposits. It probably over simplifies it to say retail banks invent money..

Think again.

Oh, ok, so under your theory banks just invent money. So why take deposits and pay interest greater than OCR?

"Oh, ok, so under your theory banks just invent money."

Pretty much...Steve Keen has written extensively about this.

Looking forward to your explanation on how this works with core funding ratios and why banks bother to take retail deposits and seek offshore funding. If there's no need to.

Why re-invent the wheel, look up Steve keen on youtube in your own time.

Isn't it just the alchemey of fractional reserve banking.

Bank lends $1 miillion to a house buyer creating a deposit in the borrowers account. Borrower pays to seller creating a deposit in sellers account - highly likely to be another NZ bank. Unless the seller withdraws notes and stuffs them in a mattrees most of the funds will remain in the banking system.

Loan creation creates deposits which remain in the banking system begetting more loan creation via the mysteries of the fractional reserve system.

It's not a completely closed system of course as some funds will leak outside the domestic banking system but it certainly has a little hint of the "ponzi" about it!

All depends on who wants to increase market share,the bank that resists greed looks good

Banks have to make up for any loss due to lvr increase

Banks have to make up for any loss due to lvr increase

@boatman - data has clearly shown the banks have not passed full rate cuts to depositors ... there's still 3.5% TDs out there while people are clamoring for sub 4% loans.

My mothers estate has TD's up to 5.5% which the bank graciously offered to allow us to break - we said no ( most are due around 2019/20 ). I suspect there will be many TD's at higher rates which the banks will still have to manage in with the current mix. Declining interest rates can hurt the banks as well.

"TD's up to 5.5% which the bank graciously offered to allow us to break"

They'll be very keen to break this, nothing too gracious going on there. Did they offer a perk??

@Mr B its academic what the actual rate is , the real interest rate is the margin they earn on deposits , so if they pay a depositor 3% and lend at 4,5% the margin is 50%

If the pay the depositor 3% and lend at 6% their margin is 100%

The sub 4 loans on fixed mortgages are funded through offshore money washing up here from places like Japan where the interest earned is below zero

The banks have extremely complex funding models , with complicated matching calculations , and they make huge amounts of money.

Don't ever feel sorry for the Banks , not ever , they make money no matter what happens

This is nice work if you can get it , and its little wonder that the Aussie banks based here are so profitable , paying record dividends to their parent banks across the ditch

But if you read Mr Hulmes comments, there's no need to take retail deposits because they just invent money.

Bear in mind out of the 150bp margin comes every single operating cost, capital cost, expected losses, as according to GDS's more and more, Banks have most income derived from net income. Who wants to pay fees anymore! Not me.

Its not strictly true that Banks " invent money " they are required to maintain a credit reserve ratio in cash of near cash such as TB's , and their book ( lending book) is rated and weighted by loan type and duration by the Banking regulators to ensure that there is some balance and to ensure they don't collapse

In theory based on what the bank says regarding funding from off shore what would be the situation should I ,for what ever reason,deposit 100k with them and borrow 100k to buy a house.Should I get a reduced rate.

Yes Ngakonui... you would pay a reduced rate. Because you would borrow $100k and then put $100k against the mortgage and pay zero interest. For whatever reason

In this (I hope) hypothetical, the lending rate should be approximated as the marginal cost of financing for the bank.

i.e. no associated risk premium and under perfect competition, no positive profit.

So yes, you would receive a reduced rate.

Remember that your loan from Bank is secured your deposit is unsecured. So if Bank is in strife you may lose your deposit but still have a loan liability.

It appears, from recent statements from ANZ management team (right from top to bottom management), somethings bothering them. Have they lent out too much to too many?

More likely to be concern about how to maintain their bonuses.

So when the RBNZ increases rate, the ANZ et al will increase by what they decreased? ie less than 0.25%? I think not some how

Oil Companies, Banks, take your pick

The Reserve Bank in Australia has dropped there OCR to 1.25% so I doubt any of the Big 4 ozzie banks will be borrowing from the RBNZ, 2.25%??

Well we are run by a bunch of fools. It is time Government took back the reins of the Reserve Bank. How any Charlie can think that lowering the interest rate will stimulate the economy is beyond me. Just think it through. Each time the interest rate is lowered the only people in the counttry who are not indebted are the elderly. Their purchasing power is reduced because their bank deposits pay them less. That withdraws that money from the economy. They buy less. The elderly don't borrow. So the hope is that all the rest of the people will borrow because of the lower interest rate. They don't have any surplus money but by some juggling of their cash flow they may be able to buy on credit. But one day they can't borrow any more and everything will crash. This whole economy is therefore built on borrowing. What in the hell is going on!

the whole world is built on debt at the moment,

NZ is no different, the ones left standing will be the ones with hard assets hence the rush into property

http://www.mckinsey.com/global-themes/employment-and-growth/debt-and-no…

If the whole world is run on debt, I wonder who the hell the world has borrowed from?

it is created, you dont need a dollar to loan a dollar. you can create many with only one depositors dollar

But property will crash too so what happens then?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.