Economists at the country's biggest bank ANZ have changed their call and now pick that the widely expected Reserve Bank cut to the Official Cash Rate early next month, taking it down to a record low 1.75%, will be the last one in the current cycle.

Previously ANZ's economists had "pencilled in" another cut early next year, which would have seen the OCR bottoming at 1.5%.

In their latest weekly Market Focus, however, the economists say they now see the OCR stabilising at 1.75%.

"There are certainly still reasons why the RBNZ could get dragged back to the easing table (a global event, ongoing weak tradable inflation through NZD strength, or failure of inflation expectations to lift). But when balanced against strong domestic growth, emerging capacity strains, rising domestic inflation pressures and some signs of a turn in the global inflation cycle, additional OCR cuts have become harder to justify as a central scenario," the economists say.

'More tenuous by the day'

Factors the economist see as making the case for easing "more tenuous by the day" include: Strong domestic demand in the economy, emerging capacity pressures, a tightening labour market, rising domestic inflation pressures (despite the low 'headline' inflation figure), and the fact that the housing market still needs to slow.

Against these factors, reasons that could yet see the RBNZ be "dragged back to the easing table" next year include: the still evident global deflationary forces, the still high New Zealand dollar, lower than ideal inflation expectations in New Zealand, and the current tightening credit conditions.

The ANZ economists say they do expect economic activity growth to moderate in 2017, "but it’s not the sort of moderation to which the RBNZ should respond".

"First, we are talking about a ‘gallop to a canter’ moderation; from 3½-4% [gdp growth] to somewhere closer to 3%. Second, it’ll be partially driven by capacity constraints. The economy cannot continue to grow at a rate above trend for too long. With each passing day, the capacity anecdotes come more to the fore.

"And finally, the impact of a required slowdown in credit growth should not be under-estimated. Credit is being rationed more tightly as late cycle excesses become apparent. That’s a good thing. A failure to rein in credit growth and associated excesses would only up the odds on a starker turn in the economic cycle down the track, which has been New Zealand’s historical experience. In the short term, credit rationing will dampen growth. However, given the momentum in the economy currently and its desirability in a medium-term context, it is not the kind of ‘slowdown’ that monetary policy needs to concern itself about offsetting."

Visible uplift

On inflation, the economists say over the past week or so there has been a visible uplift in the inflation backdrop around the globe.

"US headline inflation is at a 23-month high, China annual PPI inflation has returned to positive territory for the first time since early 2012 (which has some leading indicator properties for inflation in the likes of the G7) and UK PPI input inflation is running north of 7% y/y. In fact, inflation surprise indices are the highest in close to four years for major economies and near the same for emerging markets."

The economists say, therefore, that it is becoming clear that global headline inflation "has based".

"That shouldn’t really be a surprise," they say.

"Due to the stabilisation in energy prices, base effects alone will naturally see headline inflation rates rise further over the coming quarters. There certainly remains uncertainty over whether underlying inflation is going to follow suit in a world where excess capacity exists, but higher headline inflation rates should at least take some pressure off central banks to deliver easier monetary policies, particularly with market-based measures of inflation expectations now rising again too."

'Inflation has passed its lows'

In New Zealand, it is a similar picture, with headline inflation having passed its lows, but like offshore, questions surround whether there will be a sustained lift in core or underlying inflation.

"Certainly our Monthly Inflation Gauge has continued to provide a benign signal outside of housing. And within the Q3 data, most of the Statistics NZ and RBNZ measures of underlying inflation (trimmed mean, weighted median, Sectoral Factor Model etc) were unchanged in the quarter. Additionally, firms’ pricing intentions are historically low."

Against that, however, the economists say that price increases are broadening.

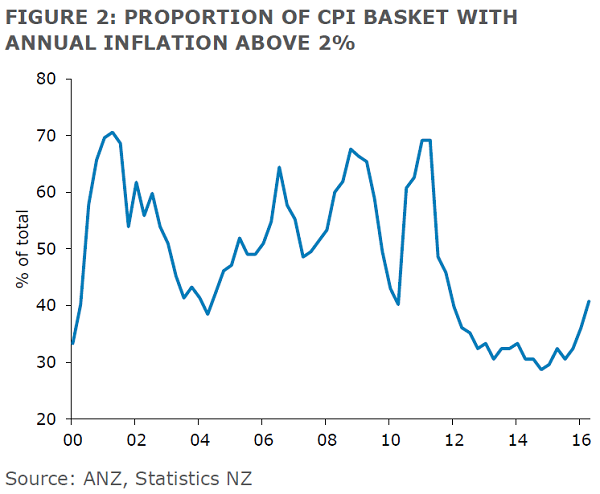

"The proportion of the CPI basket with annual inflation above 2% has risen to 41% – the highest in over four years (see chart). You’d have to think that if the prices of more things are going up, that would influence the formation of peoples’ inflation expectations."

The economists says some temporary influences dampening non-tradable inflation "should normalise" soon. They say central and local government charges (about an 11% weight in the CPI) are currently running at ‑0.5% y/y. This is in part, but not entirely, due to ACC levy reductions. Since 1995 annual government charges inflation has averaged 3.6%.

'Not without risks'

Additionally, excluding ‘uncontrollables’, domestic inflation does look to be responding to the economic cycle. Non-tradable inflation excluding central and local government charges and tobacco – a better gauge of pure domestic inflation pressures – is rising at 2.3% y/y. The economists say that is still low in a historical context, but is the strongest rate in two-and-a-half years and fully consistent with the tightening in capacity pressures evident across the economy.

As well, the prices of labour-intensive services are also rising.

"While services-related inflation in general is low overall (-0.5% y/y), when we just look at the ~15% of CPI components that seem likely to have a particularly heavy labour input (eg restaurant meals, hairdressing, repair services etc), we estimate it is running at 2.6%. This is the highest in two-and-a-half years," the economists say.

"So there are certainly some elements of the inflation picture that are changing. And while low headline inflation and inflation expectations are important to consider, when there is growing evidence that inflation pressures are now responding to the economic cycle – and “traditional” drivers of inflation are starting to gain prominence again – that is important to consider too. Letting some parts of the economy overheat in order to counter the influence of low inflation in other parts is certainly not a strategy without its risks."

9 Comments

The RBNZ should NOT lower the OCR in November because it has no desirable effect:

- It does NOT promote spending (banks are not passing on the cuts)

- It does NOT raise inflation

- It does NOT lower the NZD

But it will be extremely difficult to raise the OCR back to normal levels in the future because of the huge amount of both government and private debt.

CUTTING THE OCR TOO LOW WILL BE SEEN IN THE FUTURE AS A HUGE HISTORICAL MISTAKE

RBNZ: "but, but...but, every other RB is lower and it's obviously working! so.......". Just look at those "rockstar"world economies.

This email I received today from the BNZ needs further explanation. In summary banks lending costs are increasing and they appear to be encouraging more savers with increased deposit rates therefore justifying increased lending rates (regardless of the OCR).

Either way it is clear they wish to maintain their margins and it looks more and more likely that the OCR has little to no effect on private borrowing.

Any views or interpretation of the below would be helpful. Cheers

Below is a brief explanation of these changes and the effect they are having on firstly the Bank’s funding costs, and the flow through to customer interest rates.

· Our cost of funds is a combination of customer deposits [70%], overseas funds, & interbank funding. These contribute in the main, but not solely to where we obtain our funds from. It is also important to understand that Banks are tightly controlled by the Reserve Bank/Government on where it sources its funds and the percentages we can obtain from each. These rules have become even more rigid since the 2007 GFC

· In effect the regulatory requirement to manage our Liquidity Coverage Ratio (LCR) has meant the Bank (and our competitors) has reduced our ability to rely on one month funding — as it does nothing to improve that ratio — and increased it to longer term bank funding (3 months or longer) which has impacted on our COF particularly as we have a lot of 30 day rolling loans.

· Furthermore, given 70% of our cost of funds is domestic deposits, the increased competition in the domestic deposit market is also putting upward pressure on bank funding costs. This is been driven by two factors:

§ Domestic credit growth (more lending in NZ), which means the Banks are required to source more deposit funds to ensure they have adequate capital available to meet Reserve Bank regulations around LCR and;

§ At 3.00% and less deposit rates, deposit customers began to divert funds into other investments (e.g Property, the share market, etc) ,which has meant that the Banks have had to increase the deposit rates being offered, which flows through to the Banks Cost of Funds

· The effect of above was demonstrated in August when we had a drop in the OCR, but not the desired effect of lowering interest rates in the same proportion as that drop. This happened due to deposit rates in the last 2 months’ deposit rates rising by 20-30 points, coupled with a rise in overseas funding costs. As outlined above there are a number of reasons for this occurring but in the main deposit rates got so low that customers started to withdraw funds. Also events like American elections & Brexit have caused uncertainty in off shore markets lifting rates.

· As borrowers’ your total interest rate costs are constructed as a combination of wholesale rates, credit costs and bank funding costs.

· Historically these funding cost increases have flowed through to the borrower post an OCR announcement of a cut, which has meant you as the customer have not seen an increase in rate over the last 12 months, but as mentioned above, not the full effect of the OCR cuts.

· Unfortunately the continued increasing pressure on the Bank’s cost of funds has meant that we are no longer able to absorb this cost and this has been passed on to you the customer in the latest monthly loan rollover.

· There may well be ongoing funding cost pressures driven by the factors above, which will see potential further increases in the cost of funds for the Bank’s and ultimately the interest rate you as a customer have to pay. This is a direct cost, and is not related to an increase in individual customer margins.

· There is some potential savings in looking at fixing for short term periods 1-2 years, with the funding curve negative over this period. This would enable you to lock in a rate, that won’t shift over this period with potential funding cost increases or potential OCR movements.

"Banks have had to increase the deposit rates being offered"

That's funny because BNZ just dropped the rate on my bonus saver account. And why even consider locking into a term deposit at these rates. One might as well stick it under the mattress.

Also, would it be so hard for the bank to notify me of interest rate changes. Sneaky buggers.

Liquidity is suddenly drying up. Early warning indicators from US 'flow of funds' data point to an incipent squeeze, the long-feared capitulation after five successive quarters of declining corporate profits.

"We are seeing a serious deterioration on a monthly basis," said Michael Howell from CrossBorder Capital, specialists in global liquidity. The signals lead the economic cycle by six to nine months.

http://www.telegraph.co.uk/business/2016/10/19/fed-risks-repeating-lehm…

Richard Duncan has been predicting this for over a year as a result of the end of QE. I don't like everything he says, but he looks past the rhetoric to the numbers that matter. He has some liquidity gauge on his site, but you only get that if you subscribe.

Some reasoned arguments in that link. I don't think the increase to 0.5% will have the negative impact that's claimed. The Fed has the same issue as here where the OCR means little. It might push up some costs but if a car loan is 1.99% or 2.24% should not be enough to bring the US economy to it's knees.

The liquidity issue is already forming but I'm not familiar with the driving forces behind that as I don't look at their liquidity data. There is the usual number of people that are overloaded with debt and going bankrupt but most of the population is reducing debts rather than spending.

Only thing for sure is this is the last cut THIS year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.