By Roger J Kerr

It is well known that the RBNZ place a lot of store on the results and direction of their inflationary expectations survey as a pointer to their monetary policy decisions and settings.

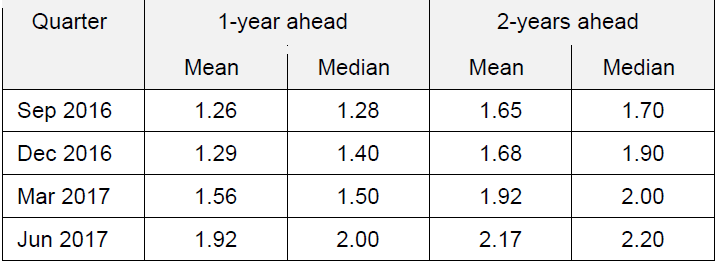

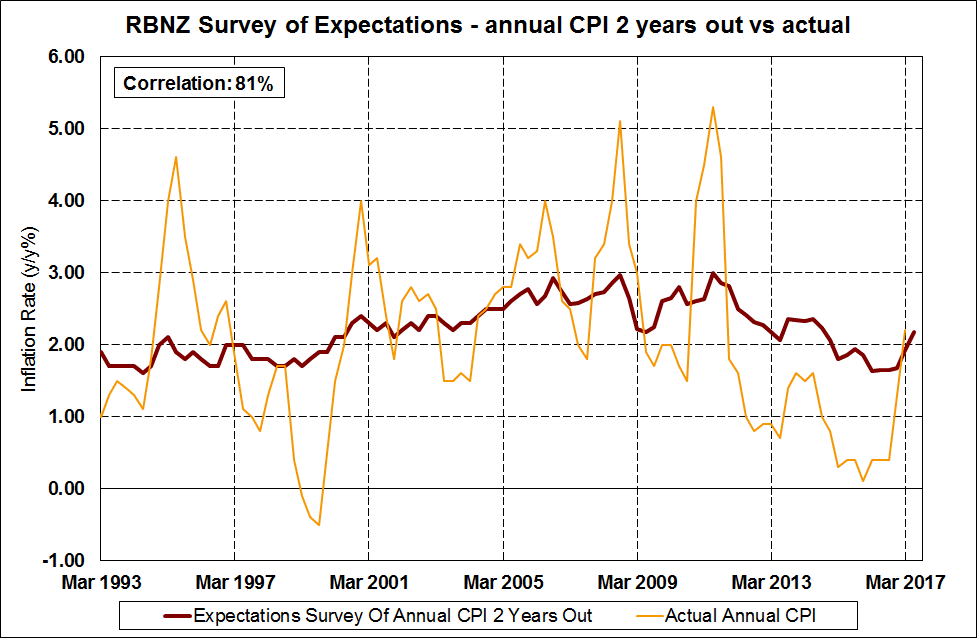

Readers of this column may recall that I have consistently poo-pooed that survey as a reliable indicator of future inflation as the survey respondents always predict that future inflation will be the same as what the actual annual inflation rate is at the time of filling in the survey.

Therefore, the survey’s track-record in predicting future inflation is dismal to say the least.

It is a backward looking consequence, not a forward looking inflation indicator.

The question is then why the RBNZ give it so much credence?

Hopefully Governor Wheeler will address this little issue of survey over-reliance in this Thursday’s Monetary Policy Statement.

The problem with this survey is that there are too many bankers, economists and fund managers (so called “professionals”) in the respondent’s list and not enough business operators who actually set consumer prices in the real economy.

The recent sharp increases in actual inflation to an annual rate of +2.20% has (surprise, surprise!) suddenly increased the survey respondent’s forward view about inflation levels.

Therefore, the RBNZ should be concerned about the jump up in inflationary expectations and adjusting their wording/rhetoric accordingly about the timing and extent of OCR increases to keep annual inflation well below the 3.00% ceiling.

However, do not hold your breath that they will make any changes in Thursday’s statement.

Also, if they think that the increase in food prices in the March quarter is a once-off and will quickly reverse next quarter, they might want to have a chat with a large buyer of fruit and vegetables like My Food Bag who have reported severe shortages and much higher prices continuing through this winter.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

29 Comments

In a basic economic model, inflation would naturally increase as the money supply increases. Indeed we have seen this. Mortgage lending has increased due to historically low interest rates and house price inflation has been the result. I've been lead to believe the Consumer Price Index does not factor in house price inflation - I'd put up a good argument for a house being a 'consumer good'.

The 'Inflationary Expectation' survey is crude and more like crystal ball gazing. It serves to legitimize the domestic economy at the expensive of those who only have access to expensive credit or no credit at all. With us Kiwi's boasting one of the highest personal debt levels and unaffordable housing markets in the OECD ... these respected, yet ball gazing forecasters might find themselves walking on a lot of broken glass.

I'd be more interested in these experts debating stagflation than their prophetic pontifications over what many consider skewed/adulterated inflationary figures. Interested to read what you guys think.

What's your argument that an asset is a consumed good? Many of us would be interested to hear it.

The expectations survey plays an important role. I don't know what your definition of crude is, though..

99% of all surveys could be classified that way. I also don't know why you would think it's true purpose is to legitimize the economy - expectations don't have to be difference positive...

Roger Kerr doesn't see the point in it because he is largely a narrow sighted critic. Perhaps he should survey his contemporaries and see how well their expectations are anchored to real inflation.

I remember reading a working paper a few years ago which detailed inflation expectations among business/industry leaders in New Zealand and by memory there were significant gaps between published inflation and what they believed actual published inflation to be.

Also, who argues that the published figures are wrong?

You diffidently make good points Nymad. I'd argue a house is a consumer good because you consume it by living in it. Housing is a consumptive product. Housing can also be a huge liability, especially when a mortgage is underwater. Not only would the owner have negative equity, they are still responsible for rates, insurance, repairs, etc.

I'd consider a rental property which is making money after expenses to be an asset. However, just because something can be speculated on, does not mean it's an asset. You can speculate on ANYTHING, i.e. a chocolate bar if you think the price of coco is going up. Just because people speculate on houses does not mean they are assets.

Let's not forget, in the 17th century speculators were hung.

Inflationary expectations which dont exist

Correct - there is no inflationary pressures anymore .... only deflation and market manipulation

http://www.zerohedge.com/news/2017-05-06/problem-emerges-central-banks-…

I personally think the time has come that interest.co.nz bans links from zerohedge.com.

It really speaks for how desperate you are to support a rhetoric when you blindly regurgitate a bunch of authors who use the pseudonym "Tyler Durden."

Seriously.

was the article false, misleading or fake news?

If no one is willing to put their name to it, it might as well be regardless of the content.

Do u judge a book by its cover..?? :)

That's not the argument here.

The argument is that zerohedge presents a very specific dommsday-esc rhetoric. No one is willing to put their name to any of the articles. How should reporting ever be taken seriously on that basis?

You'd be okay with interest.co.nz having ghost authors for all their stories?

You'd be fine forming opinions from knowing nothing about the author, their history, or expertise?

Come on.

yes.. zerohedge is kinda "sensationalist"... but I do skim read some of their stuff... and read more carefully if it pushes a button..

Zerohedge is not as bad as the NZ herald, in regards to content..

Quite right, zerohedge is often pure click bait, with the occasional brilliant article written by someone who really knows their stuff. Why would you want to shut down free speech, unless there is incitement to violence?

This isn't an argument of free speech.

No one is putting their name to the dribble that they write, so how could that ever be in question?

Apples with apples, please.

No one is trying to make arguments about financial stability based on the Bachelor's favorite cafe.

So is your point that Central Banks arent injecting massive liquidity?

Or are you officially just a troll?

My point is that why quote people who aren't prepared to stand by their work...

Secondly, tell us exactly why the liquidity is such a doomsday premise.

You do know how monetary policy works, right?

Im guessing it has something to do with water - which is why I try to canvass sites such as this to debate & learn. Unfortunately you seem reluctant to share your knowledge.

The key word, which you use in a post lower down, is "pressure".

The concept of pressure helped me see how the monetary system is interactive. Quantity (or volume) of water (money) alone does not create pressure (asset inflation). A central bank can print money at any time but the effect of that extra volume in the system as a whole depends on many other factors.

There are two broad forces that act on volume to create pressure, one is constriction (controls), the other heat/movement (velocity of money).

It is this interaction that explains why a central bank can (in some circumstances) create volume without inflation.

Consider this https://en.wikipedia.org/wiki/Shakespeare_authorship_question

Perhaps Shakespeare was no different to using Tyler Durden at the time. Should we therefore disregard all of his works and contribution to the English language?

I prefer the zerohedge links so long as people don't believe everything they read and actually think.

ham n eggs

Really..?? I don't really see any deflationary pressures anywhere..???

Central Banks have their fingers on the triggers , in rgards to providing liquidity.

Most of the Western Govts that count are in spending mode.. ( thinking inflation is a dead duck ).

Sure... Another debt crisis will bring in that sucking sound of a credit implosion ( deflationary forces)... but that may be yrs away..??

We are in the midst of the greatest Asset Boom of my lifetime... and apart from corrections( mild recession ...maybe ).... I dont think it will be over for a while yet..???

The deflation mantra has been chanted since the GFC.... but the reality is that we have kinda avoided it...kicked the can.. ( Only Europe has got a taste of it ).

just my view..

The question is why arent we seeing inflationary pressure when the CB's are busing themselves loading up on equities so that the market is in a permanent boom ... is it because actual growth is dead...

Where is there no inflation?

Don't you read the releases...

My view is that this has been happening in the face of private sector "deleveraging" , and also USA and European Banks healing their Balance sheets.. ( as well as they can )..

We are almost 10 yrs on from the GFC...

So.. the new normal becomes an environment of "low growth".

This may be the Wests' version of Japans "zombie" economy...?? BUT... with an inflationary bias... in my view.

Even Europe..even Germany are experiencing Real Estate Booms..

Inflationary pressures manifest in different ways...

eg.. In NZ building cost inflation is running at double digit rates.. http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

I dont see this as a deflationary envirnoment.... Maybe we have to come up with a new term..??? ( like we did with the stagflation 1970s' )

ham n eggs - please name us the countries with deflation

Cost of an average new car 1970 Approx $4000, 1990 approx. 40,000. Today approx 40,000. compare with historical interest rates,

http://www.teara.govt.nz/en/graph/23100/interest-rates-1966-2008

I don't think we will get any real inflation until interest rates rise, and that is unlikely to happen quickly because of global debt.

Ahhh, what's the point?

my point is that there is no inflation, only credit growth. Inflation is too much money chasing too few goods, Not too much credit overproducing goods and chasing too few houses( that's a bubble)

The car analogy and interest rate graph doesn't really show what you want, then.

You would be better off giving details of M1 as opposed to that interest rate graph, if that was your prerogative.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.