By Roger J Kerr

It does not pay to underestimate the dominating role the price of oil plays in our economy.

There is a strong correlation between crude oil prices and whole milk powder commodity prices as Fonterra’s marginal big buyers of dairy products are oil producing nations such as Algeria and Russia.

If the oil price is down these countries are financially weaker and therefore pull back from importing dairy products (and vice versa).

Whole milk powder prices plumbed the lows below US$2,000/MT in 2014 and 2015 when crude oil prices plunged from US$100/barrel to below US$30/barrel.

Whole milk powder prices have recovered (assisted by weather related supply restrictions) to above US$3,000/MT as oil has bounced back up to the US$45 to US$55/barrel range.

Oil and fuel price movements over recent years have also had a major and direct impact on our inflation rate, therefore also impacting short-term interest rate levels.

The collapse of oil prices in 2015 kept our inflation rate very low in 2016. However, when those 2015 price reductions dropped out of the annual inflation numbers in March 2017 the inflation rate jumped up to 2.20%.

The RBNZ cite many other reasons why inflation was so benign in our economy through 2015 and 2016, however the main reason was the collapse of oil prices.

It does not appear that the global oil market is expecting another price collapse to below US$30/barrel over coming years.

Therefore a return to a 1% annual inflation rate in New Zealand over the next 12 months, as the RBNZ are predicting, will require other prices in the economy to reduce.

I struggle to disseminate what goods and services will be going down in price over this time.

Primary industry export prices are very strong and do not seem likely to collapse that would pull domestic foods prices down.

Healthy, free-market competition at all levels in our economy is the largest contributor to low and stable inflation in my opinion. However, in an economy growing at 3% with robust consumer demand it is difficult to see business firms reducing prices and eroding their profit margins.

The balance of risks remains that the RBNZ will eventually be forced to relent in their 2019 timing for the next OCR increase.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

43 Comments

It does not appear that the global oil market is expecting another price collapse to below US$30/barrel over coming years.

Equally, a price rise is hardly baked in. View graphic evidence

{kind=link}

As always, all of this really gets back to the economy, and it has been consistently this way ever since the start of the oil crash once blamed on a “supply glut.” Economic predictions have run so many investors afoul of common sense, where undue over-optimism prevails for no other reason than disbelief. As I wrote back in January:

That’s why…it will be difficult for oil prices to more fully embrace “reflation” in a way that other asset classes have already. Before things can truly go back to normal, something must be done about what happened over the past few years. “Reflation” is mostly about what could happen tomorrow, but oil, in particular, can’t just ignore yesterday.

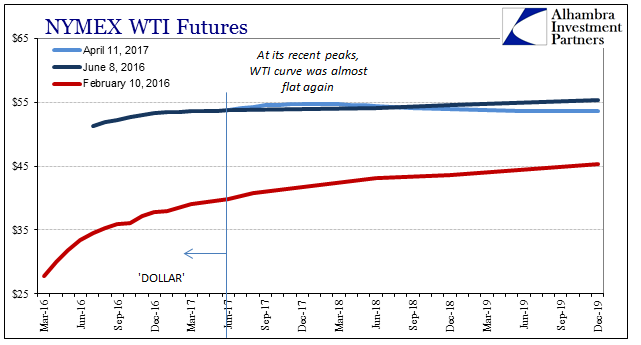

For the most part, it hasn’t. The WTI futures curve, for example, has found an eerie sort of stability pegged at around $55, with mild backwardation in the middle. That suggests, strongly, oil investors don’t expect oil to go much above that level for quite some time. With the familiar “hook” in the front end of the curve, the risks remain still to the downside. Read more

Interesting thing is much of the oil now left needs way more than $55 a barrel to extract and some years. So the thing to watch now is how long the US shale can keep its production up, 3 years? 5years? fascinating really.

Given that they are increasing production, I'd say they are producing and delivering to Cushing for less than the current market price...

so someone is hurting...

Some would disagree. There is a plentiful supply of oil coming into the market from US fracking. The US has the highest level of production since the 70's and are getting close to storage capacity. US oil exports have increased 6-fold since 2006. There are a lot of new, more efficient oil rigs coming online as well. China's demand is lacking. This could see oil sink sub-$30 and even to $20 a barrel. There's technical support around the $47 mark so we'll be keeping an eye on OPEC.

Indeed there is new oil but pretty much only the USA shale. Offsetting some of that gain are old fields historically declining at 2% (ish) and at present prices maybe 4% or even 6%. At the end of the day the oil price is set on supply and demand, even if the supply drops if the demand drops faster we get "over-capacity" Having watched this stuff for a decade now I think there is way to much blind guessing going on and people relying on it. If you are right on such a drop that suggests a NET glut and at that point a lot of pain for those who have invested, gamblers all.

"storage capacity" well its been getting close to for years on and off hard to tell this time if it matters, or not, so many false call on that one.

In response to proposed cuts by OPEC countries the US suppliers have confirmed they will fill the gap in the market. It's what they did with the last cut, and they are confidently saying they will do it again.

If you are betting on a short term bump in price you might get it but the pressure is in the downward direction for mid to long term until wells run dry and production projects run their course.

Define mid and long for me?

As the price is so low the next couple of years seems to indicate conventional fields continuing the decline at 2~6% per annum ( no one is really investing in new fields nor expensive recovery on existing fields with US shale counter-balancing that for now hence 4%+ is probable). However at 4% decline that's 3.6million barrels per day per year that has to be found. So the Q is can US shale double its output again? and the again? big ask by 2020. That is my mid term, ie price will be going up, the Q is can people afford to pay? if not? the dynamics are really interesting.

There is an ugly reality approaching - we are burning through old fields and the cheapest Oil - every barrel is effectively more costly (energy wise) than the previous one.... and a higher Oil price will crash non-existent world growth. Add this to the fact "new discoveries" are less than 10% of current usage each year.

The glut is about cash-flow only ... Something has to give.

https://srsroccoreport.com/future-world-economic-growth-in-big-trouble-…

https://ourfiniteworld.com/2017/05/05/why-we-should-be-concerned-about-…

https://srsroccoreport.com/continental-resources-example-of-what-is-hor…

"Cheap at first then more and more expensive, until the resource is mined out or simply beyond viability to produce. Any fool can see heavy contaminated crude, tar sands, deep offshore, fracked shale and Arctic oil is the obvious signs of decline."

Even out to 2020 the prices are likely to be low. The one thing that really jacked up the prices was heavy investment by retirement funds, most of those idiot fund managers thought the recent high prices were a sign of peak oil. Instead they made everything expensive for everyone.

Ham is right though oil will eventually decline to a much lower level of supply and a rethink of energy consumption will be needed or we will build fusion reactors. The results from current fusion reactor construction is still quite disappointing though so I'm viewing that as very long term and I may be dead before it's a practical replacement.

Development happens in a time of surplus, or an ascending environment. More complexity is not an option in in times of scarcity. If we hit peak oil and the alternatives are not yet in place, then we are screwed.

No sign I can see oil will increase much. Oil prices influence dairy prices in more ways than that oil producers import more. Our competitor dairy farmers rely on crops for stock feed, and grain tracks oil. Oil is low and so dairy will ease in the pretty near future as N hemisphere production kicks on the back of cheap stock feed. Hang onto your hats, dairy farmers and nz will have low inflation.

And the transition to electric is going to be FAST

electric has been round for ages ... so why is it taking so long?

Last week I drove a BMW electric car. The acceleration and quietness was unbelievable. They use the equivalent of 30 cents a liter if petrol is $1.95. You can charge them at a low cost overnight when normally electricity is not being used and is wasted and electricity is charged at a lower cost. The money now going into this technology is huge.

I have also ridden an electric bike, they are amazing. It is incredible how much power can come from a Lithium battery.

I would say that in 5-10 years nearly all new cars sold will be electric.

Oil prices will start to decline when this happens.

A word of warning, as electric supersedes combustion the government will begin to seek to replace the taxes lost from fuel taxes. The first thing, of course, will be road user charges, and I imagine they will increase markedly to take over where fuel taxes left off.

Similar could apply to e cigarettes, though we know it shouldn't

Electric will come in tandem with driverless vehicles. Most won't own a car. Big cities will not allow dangerous self drive vehicles within. From the provinces? Then park on the outskirts and hail an icar. Travel will be so cheap, road user charges will insignificant.

Totally agree but government will still be looking for those taxes provided by fuel taxes from somewhere

....much bigger issue than just fuel tax. The job losses will be staggering. The motor industry verse electric is what the car was to the horse and the digital camera to kodak. Most major traditional car companies will be toast, step in tesla, apple and google etc.

And current govt immgration policy just looks absurd when we see whats coming...we will need less workers, not more.

I think we are fooling ourselves to think otherwise, but those massive job losses will come with way more than just autonomous electric cars, that is for sure. The problem that will arise from it, will be, as you say the likes of a few, huge, multinational corporations owning the technology. With that, they will be able to wield far more power than any little old government can.

We have some major rethinking to do in the future world, not sure how we will be able to break the stranglehold that the likes of Tesla etc will have and the likes of the TPP will make that difficult task even harder

Removing all this demand from the economy crashes the economy.

re superceding combustion ... this is well worth a listen

https://www.peakprosperity.com/podcast/100873/alice-friedemann-when-tru…

itsme,

You would be interested in a report just issued. It's called Rethinking Transportation, the Disruption of transportation and the collapse of the internal-combustion engine and oil industries,published by RethinkX.

It forsees that by 2030, 95% of US passenger miles will be by autonomous electric vehicles owned not by individuals,but by fleets. It predicts that the number of passenger vehicles will fall from 247 million to just 44 million.

On oil,it predicts that peak demand will be 100 million bpd in 2020,dropping to 70 million bpd by 2030. The summary onpages 6-8 are well worth reading.

Sorry the thinking defies $$ & physics - extrapolating from a (costly) BMW to no Oil required isnt possible.

The world isnt short of electricity - its short of cheap energy... the electrical grid relies on fossil fuel infrastructure - not the other way round.

Have you scaled up the amount of rare minerals required to battertise everything? / Have you costed in the cost of the transition infrastructure? / Have you factored in the massive subsidies that have so far failed to deliver anything remotely cost effective? Heres a link on energy subsidies ...

http://energy.utexas.edu/files/2017/03/UT-Austin_FCe_Subsidies_2017.pdf

Theres a reason theres so little uptake, that Telsa bleeds $$ , that it will happen "sometime in the future, when .... "

Its a nice story but is just delusional.

ham n eggs,

As I imagine you know,rare earth metals are not actually that rare. Additionally,Honda has developed a Hybrid engine that does not use either Dysprosium or Terbium. This make it some 10% cheaper to produce and 8% lighter. It does use neodymuim,but it is also found in the US and Australia. You are,in my view underestimating the speed of technological change.

You say that the world is short of cheap energy. What do you consider cheap to be? Is oil cheap or expensive now in your view? Do you really believe that technical issues with solar and wind energy will not be solved? That batteries will not become smaller and more efficient?

How much of the worlds electricity production is non renewable?

exactly - its easy to overlook the fact electricity is NOT actually an energy source. It needs to be created first by a primary energy source.

Linklater - in answer to your questions

- Cheap energy is simply energy that allows the economy to grow - once you account for all the "overhead" already committed in the form of direct costs, Oil co profit so they can reinvest & crucially govt taxation ... this is the part that everyone neglects. If you don't increase our TOTAL NET energy burn (NET = after you remove the energy cost of extraction) you put the squeeze on all those previous promises (ie debt burden already in the system). Net energy pays everyones wages! So energy has become too expensive..

- Do i think solar / wind issue will not be solved?No. The system is by its nature expensive ... due to intermitency, peak load problems, backup, non transportability etc etc ... even if the infrastructure was in place! which its not... it needs a backup fossil fuel system for reliability (you are doubling costs)! And you are really only talking electricity

- Batteries are becoming smaller / more efficient, but we can only work with what we have now ... and the gap is way way too big. Fossil fuels are that efficient.

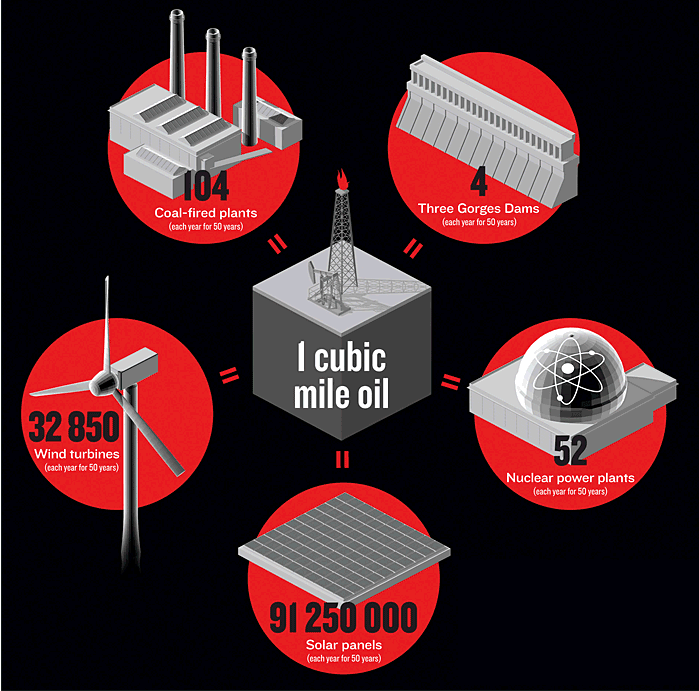

http://energyskeptic.com/wp-content/uploads/2012/08/1-cubic-mile-of-oil…

{kind=link}

I don't think that technological change is a concept H&E has yet grasped.

One only needs to look at the rates of uptake of battery electric and renewable energy over the past 30 years. With the integration of the two, there should be little argument for poor security of supply.

Also, he misunderstands the link between energy usage and economic growth. In recent times this link has been non existent in western countries, and is flattening out in the developing nations.

"One only needs to look at the rates of uptake of battery electric and renewable energy over the past 30 years. "

Yes - Nymad have a look - quite amazing. I wonder how well it would look if we removed the subsidies?

http://www.bp.com/content/dam/bp/images/energy-economics/freesize/prima…

{kind=link}

You mean the subsidies to fossil fuels?

Global renewable energy usage is ~15-20%. Global renewable subsidies are only $80bil compared to $5tril in fossil fuel subsidies.

There's no such thing as a fossil fuel subsidy in energy terms.

You're reading too much Naomi Klein- keep going.

I'm sorry, did you just say that there is no such thing as an economic subsidy to producing usable energy?

No - are you intentionally misreading?

There's no such thing as a subsidy for fossil fuels in ENERGY terms....

The energy surplus provided by fossil fuels effectively backs any subsidisation of so called renewables.

Oh, right.

I forgot economic principles aren't a thing in your understanding of the world.

So, what sudsidises the production of fossil fuels?

what subsidises the production of fossil fuels?

Debt is what gets it out of the ground. If the extraction can't produce enough energy surplus to support the whole system you would soon run into debt problems... which funnily enough! seems to be what we are seeing...

hmm.

So we are subsidising something today that we know we can get for cheaper tomorrow?

Interesting perspective...

"we are subsidising something today that we know we can get for cheaper tomorrow"

Isnt that your point with the progress of renewables ?

The debt isn't a subsidy ... unless of course you now believe the debt added is now effectively a Ponzi only ... in which case we are indeed in big trouble.

I think you need to explain how the economy would work if we took away those pesky fossil fuels & their big subsidies ... you seem to imply we'd be better off

Nymad - this is interesting if you hadnt seen it

http://energyskeptic.com/wp-content/uploads/2012/08/1-cubic-mile-of-oil…

http://energyskeptic.com/tag/cubic-mile-of-oil/

"he misunderstands the link between energy usage and economic growth.."

Nymad - I suggest you do an experiment. Place 10 cows in a paddock. Monitor.

Also place 10 cows in a fenced asphalt car park. Monitor.

Tell me if energy usage comes into play, or if both sets just economically grow together?

Great arbitrary experiment.

Now look at countries. Why is their growth in productivity outpacing their growth in energy consumption?

If your thesis (that strangely no energy economists have picked up on) that the economy is 100% energy and that energy is underpriced was correct, how could this be?

Growth in productivity ... measured by what exactly?

Measured by the same old tired GDP

Another experiment, if old.

Go to a french public toilet and pay the lady to use, she is doing an excellent job keeping them clean.

Voila, going to the toilet contributes to GDP.

Inference ...we should all go to public toilets more and train cows to use toilets... A job for the agricultural economista...

Magnifique...or is that spanish...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.