By Roger J Kerr

There have been too many false starts of long-term interest rates sustaining a new uptrend over the last few years to get too excited about the potential for increases in yields over coming months.

What we do know is that the probability of US Treasury Bonds moving lower in yield is much reduced these days with US short-term interest rate being steadily and surely increased by the Federal Reserve and future US budget deficits likely to increase, rather than decrease going forward.

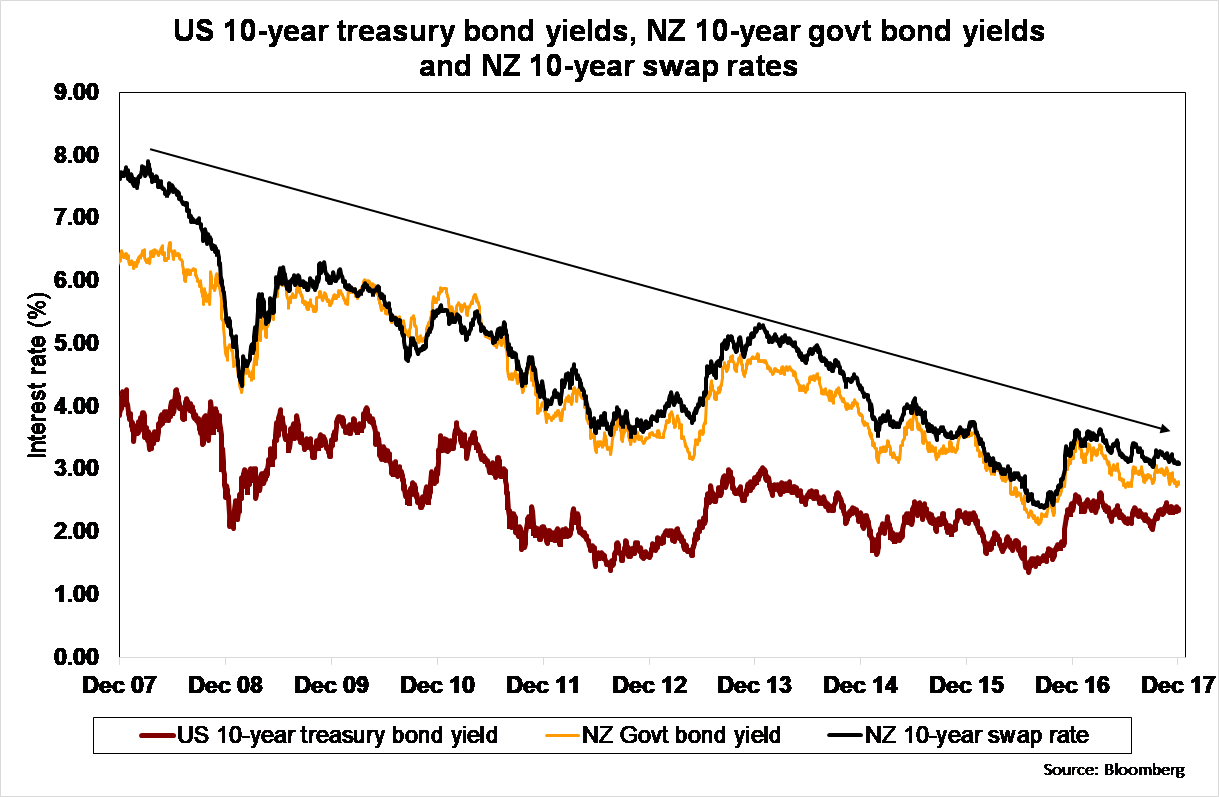

Over recent months the US 10-year Treasury Bond yield has marginally increased, however, it has a major barrier at 2.40%/2.50%.

What is interesting about long-term interest rates is that the margin (or spread) that NZ Government Bonds trade above US Treasury Bonds has continued to decrease.

A year ago the spread or risk premium that NZ Government Bonds price above US Treasury Bonds was 110 basis points.

Today the gap is only 45 basis points (US at 2.37% against NZ at 2.82%).

What is even more surprising is that the gap has closed further since the formation of the new Coalition Government here in mid-October.

The spread compression is totally counter-intuitive to economic and political developments in New Zealand.

The prospect of the new Government having to follow through with large spending increases when tax revenue may be heading the other way leads to internal budget deficits rather than the current surpluses. All adds up to increasing NZ Government debt and thus the NZ risk premium over the US increasing, not decreasing.

Looking ahead, the demand from both local and offshore buyers of NZ bonds must be waning as most report a desire to shorten the duration of the fixed interest portfolios, not extending portfolio duration.

The end result is that there may be two reasons for three to 10 year NZ swap interest rates increasing over the next 12 months, being US long-term rates increasing to 3.00% from the current 2.37% and the NZ:US bond spread also increasing from its current 45 basis points as New Zealand’s risk premium increases in the eyes of global bond investors.

The chart below indicates that NZ long-term interest rates have remained below the downtrend line for many years, however the crunch time as to whether it can continue is rapidly approaching.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

27 Comments

We're definitely at a turning point. Either the Fed rate goes up as stated or things start looking bad and the rate comes down. I'm sure 2018 will be an interesting year.

I can not see any rate increases for the simple fact that the world is awash with debt and it would become to hard to service leading to defaults and right back where we started more QE

Thursday is the Fed funds rate announcement for December. Forex factory is showing a lot of red flag announcements that day.

https://www.forexfactory.com/calendar.php?

The Fed has previously announced they will increase the rate in December. Thursday is a 50:50 on the increase from my perspective.

Well said sharetrader you are spot on

Absolute rubbish. We and Australia are uniquely exposed to higher interest rates due to our ridiculous property bubbles. Some parts of the world, or at least the bits that count (the US), have already been and gone through that same bubble. There is a tightening bias in the US esp and elsewhere and they neither know nor care what is happening down here. 60% of our bank funding is obtained on the international market, we have no choice but to meet the international price for debt. The numbers coming out of the US look good, their interest rates will rise without any regard whatsoever to the impact on us. “It’ll never happen cos it can’t happen” is a cry of desperation from the overleveraged. A 200 bps increase in the cost of finance might give the US a cold shower, it would give Australia and therefore us a full blown banking crisis.

"The numbers coming out of the US look good.."

Does someone actually believe them?

I remain unconvinced that the US want to have that "cold shower" that you talk about. lol

The point being made above was that rates could not rise otherwise otherwise it may be Armageddon. Well, it may be Armageddon for aus and nz, might not be for others. Plainly the US is in a different space. We are now merely a bystander on where international rates go from here.

If the USA is better placed than China to cope with higher interest then?????

Sorry, what’s your point.....?

The NZ government could simply enact their own QE to suppress interest rates. They may even get the added bonus of driving down the NZ dollar, what they have been trying to do for the last decade.

At the start of the GFC, economists stated the shortage of money would push up interest rates ie simply supply and demand, some friends in executive positions in the finance industry stated the same. I can remember my wife who has no degree, but an above share of common sense saying, "that is rubbish, if interest rates go up everyone will be bankrupt and the government won't let that happen, as they wouldn't get voted back in". Time proved my wife's common sense approach correct, note she still has the same opinion, as she says "they have locked it in" , with the it being low interest rates.

The turning point is the massive tax cuts just passed in the US. With this extra stimulation at a time where the US economy is firing leaves the fed with no other option than to raise interest rates faster than it would normally to contain inflation.

Trump policies directly effecting what we pay on our mortgages unfortunately.

I suspect not,

a) How much of the massive tax cuts effect those of the bulk of ppl? ie yes its a massive corporate and rich tax cut. Not so sure, on this "cut" effect as if most ppl have no more money it wont raise rates as the effect will be minor.

Interesting to watch.....I mean,

"The House tax plan does not pay for itself through growth, and more income benefits flow to the top 1 percent than to other groups in its first year, according to the right-of-center Tax Foundation."

So the US will be in even more debt even if the "right wing" think tank's numbers work and frankly they probably wont.

alternative view it will be a mess and make things worse,

https://www.theguardian.com/us-news/2017/dec/10/donald-trump-kansas-fai…

b) Meanwhile, "'The President may be celebrating, but most Americans will rue this day,' says Democratic senator"

Hmm maybe the effect will actually make things worse, I suspect so myself.

Your comments are based on the assumption that the US federal spending/debt juggernaut should be sustained in its current form. Clearly it can't be as 70% of debt repayments are accumulated interest and debt is added every year without any intention of ever repaying it (Obama added $6T during his term alone). The brick wall is not that far off and the impact will be felt widely. A govt that simply keeps consuming a greater and greater proportion of the economy in taxes, regulation and bureaucracy is destined to go the way of Rome. A 20% corporate tax rate in the US is reasonable, and this will spur investment and job creation, not to mention capital flight and investment from dying European and other high-tax economies. While it's trendy to be a Marxist these days (a bit like having a tattoo..) and call for 50%+ tax rates, the reality is that this kind of big govt socialism has always led to economic and social decline. In fact, we are living through this very cycle now, with everyone wanting bigger govt and more handouts. This is simply empowering China and Asia to take over as the next global power houses, and all our PC whingeing and bleating will be just that...

Why will it spur investment? Kansas was an epic failure, tax is paid on profit. Investment is only made if it will increase profit and without money flowing down to their consumers base there is no incentive to expand. This will only accelerate the downward spiral as that lost tax revenue will have to be made up somewhere else.

Tend to agree – and sound reasoning and logic to back it up – wonderful.

However, while” being US long-term rates increasing to 3.00% from the current 2.37%” sounds quite straightforward – its arrival remains constantly problematic.

Without fail this line is faithfully trotted as a standard feature of year end forecasting - and is yet again followed by 12 months of head scratching, bewilderment and sheer frustration by all manner of commentators.

Maybe 2018 will indeed be the year….tax cuts… yes, 2018 will surely be the year….big market jolt….yes, 2018 will be the year!!

Take your point sharetrader but the Fed has hardly rushed at the gate – has hardly maintained a cloak of secrecy– actually an overabundance of foretelling I would suggest.

Even greater dangers lie in wait if “too easy, too long’” once again is permitted to play out (too late already?) – a myriad of bubbles - but please don’t interfere - hmmmm ?

Ask yourself: are Uber, Airbnb, Amazon, upcoming crypto currencies and many more budding online direct services/sales platforms inflationary or deflationary ?

I think the parameters the author keeps using to forcast inflation are out-of-date

Fair point - inflation and its calculation is sometimes a little baffling.

I don’t seem able to catch the “inflation is dead” boat.

Perhaps if I was buying a laptop each week or flying to the Gold Coast every 5 minutes I would be enjoying this period of ultra-low inflation more than otherwise.

An interesting science to be sure – by the time calculators have taken into account one-offs, product substitution and then discounted any other annoying price increases apparently we can comfortably sit back and merrily announce “inflation is virtually non-existent”.

Do this for too long and consumer’s ability to do as their name suggests starts to waiver – and then we have a fun spiral!

Thankfully it appears wages and salaries numbers in various parts of the world are starting to stir to the upside. Productivity can play a part in soaking up these increases but there may well be some degree of follow through in end pricing as well.

Not all doom and gloom – but there are some questions regarding the longer term viability of one or two of your nominated platforms.

Tim Morgan at

https://surplusenergyeconomics.wordpress.com/

gives a good handle on whats happening

right - all those companies are workarounds for shrinking buying power ... the overall pie is decreasing

I'm sorry, I don'treally understand your comment, can you please elaborate hne, thanks

Here's something the foreign press have highlighted that you don't get to see in the Herald.

Recent governments can be so proud.

https://www.ft.com/content/66c16b5e-d8b5-11e7-a039-c64b1c09b482

Nearly 1% of Kiwis are homeless, the next worse are Aust, Canada and Germany at 0.5 or less.

"...where a recent report by Yale University concluded the country (NZ) is suffering the highest rate of homelessness in the developed world with 40,000 people, nearly 1 per cent of the population, living on the streets or in emergency housing or substandard shelters. "

Interest rates on the move up won't improve the data.

Damn that's one hell of an indictment on the past 9 years of economic policy. We voted John Key in three times and all we got was a housing bubble and the highest homelessness rate in the developed world..

Actually the Herald did cover it, briefly, back in August, and challenged the data based on the precise definition of homeless (http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11908336).

Here's the Yale article itself, and it's well worth reading (https://yaleglobal.yale.edu/content/cities-grow-worldwide-so-do-numbers…). New Zealand's data sticks out like a sore thumb among the OECD countries.

Has the man no shame? Roger has been telling us(again),that much higher interest rates are just round the corner,but now he seems to be backtracking(again).

I have come across some poor forecasters in my time,but I can't recall one who is more consistently wrong.

Even a 250 basis point increase in interest rates could trigger problems given the feast of debt we are currently enjoying .

Nah business as usual until WW3 or a Zombie Apocalypse or the USA has another major financial melt down or Donald Trump misses his spay tan appointment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.