Economists at the country's biggest bank are warning that "a significant economic headwind" could be in the pipeline as the growth in bank deposits slows at a time of strong credit demand.

And they warn that bank lending may be necessarily 'reined in'.

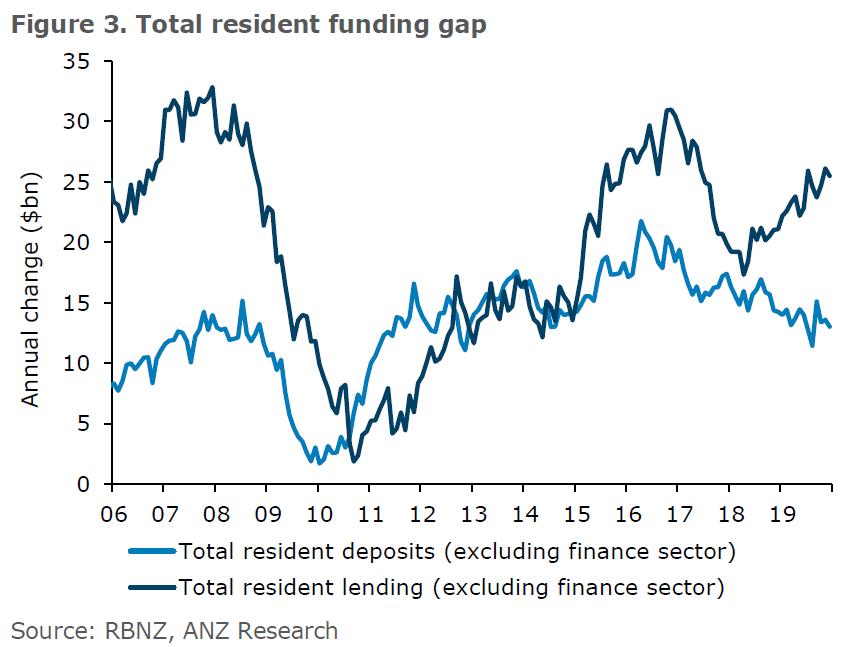

Recent Reserve Bank data showed that household bank deposits grew at the slowest rate last year for nine years, while housing loan growth hit its highest level since mid-2017.

The banks refer to such a divergence between credit demand and deposit growth as a 'funding gap'.

In their Weekly Focus publication, ANZ NZ's economists say the slowdown in deposit growth "matters".

"New Zealand banks need deposits to fund their lending, so the recent widening in the bank 'funding gap' is something we are watching closely.

"In the current environment, generating deposit growth may be difficult – although banks can tap non-deposit funding, this has its limits. Closing the gap is likely to result in a tightening in credit conditions, at least to some degree, at a time when credit demand is strong. A significant economic headwind could be in the pipeline," the economists say.

They say the explanation for the slowdown in deposits is "not as obvious as you might think".

"Overall, we think movement away from foreign ownership of New Zealand housing, the rise of popularity of managed funds and the like in response to lower interest rates, and greater use of cash as a store of value could all be contributing to the recent divergence between credit and deposit growth. However, ascertaining the contributions of these factors is difficult and would require quite a bit more digging."

But they say whatever the reasons for the slowdown in deposits, closing the bank funding gap could be a significant headwind for economic activity going forward, as was seen in 2017 when a similar gap developed.

"It’s possible that banks could tap wholesale funding markets to bridge the gap, but there are limitations to this strategy. That’s not only because of Reserve Bank rules. The ratio of loans to deposits is also a key metric used by investors and in ratings assessments to assess a bank’s liquidity. This means that increased funding via wholesale markets (even at a long duration) can weigh on perceptions of risk and thereby increase funding costs."

It is possible that banks could lift deposit growth to fund the gap, but scope to do this through higher interest rates is limited, the economists say.

"This would also increase funding costs and squeeze margins.

"Alternatively, banks can bridge the gap by rationing lending, either by increasing its price (higher lending rates) or directly reducing its availability.

"Either way, given the extent of the gap, we expect that lending will need to be reined in to some degree."

The economists say the tightening in financial conditions due to the funding gap doesn’t bode well for economic activity, "and indeed it already looks to be putting a dampener on things".

"Survey data of both businesses and banks show that credit has become harder to get. And while not all of this is owing to slowing deposits growth (eg recent changes to bank capital requirements and re-pricing of risk are also factors), there’s little to suggest conditions are about to improve.

"The potential economic implications of closing the funding gap are significant. Both the availability of credit and its cost could become less favourable for households and businesses. In addition to households and businesses facing higher-than-otherwise debt servicing costs, credit could become more difficult to obtain (as banks attempt to align the pace of credit growth with resident deposits)."

The economists say that because banks need to strike a balance between deposits and lending, should the Official Cash Rate go lower, the 'pass-through' to deposit rates (and therefore lending rates) is "likely to diminish".

"But that’s assuming households’ appetite to put their money on deposit in the bank is unchanged. A change in sentiment could make bank deposits, which are at the less risky end of the spectrum, more attractive. And if the Reserve Bank is cutting the OCR, it won’t be because things are going swimmingly."

It’s an unfortunate time for credit availability to be squeezed, the economists say.

"The bulk of current credit growth is because people are wanting to take on debt to buy and build houses, invest in commercial property, expand capacity and the like. But parts of the economy are also being hit by massive disruption in the form of the tragic COVID-19 outbreak. Global shipping routes are seriously disrupted. Farmers can’t send their cull stock to the works because China’s cool chain is congested, and feed in some areas is running very short. Retailers are struggling to get hold of consumer goods to sell. Producers are worried about supply of intermediate goods (building materials, steel, plastics… you name it) and what that might mean down the line. Tourist operators are looking at significant cancellations.

"It is unclear how long these disruptions will last. Let’s hope it’s brief. But many businesses will be needing credit to tide them over. Not a good time for the system to run short."

30 Comments

A number of different smoke signals being sent here

There may be strong demand for credit, but if it is going into house price inflation its not good use of credit.

Banks have clearly ignored the consequences of their excessive lending, which have resulted in high accommodation costs. This extends to unsustainable dairy land prices, that have engaged unsustainable intensification and polluted waterways.

Banks are not good corporate citizens; rather more interested in maximising their profit for overseas shareholders.

It might be a good time for the banks to focus on lending that delivers real growth to the economy, rather than the ponzi scheme they have got going with the housing market.

There is another way the banks could lift their deposits, and that's by increasing the rate of return they offer to depositors. But they wouldn't do that would they, as it would squeeze their margins and profit.

No sympathy here, when they profits represent a return of 15% plus on equity.

"New Zealand banks need deposits to fund their lending, so the recent widening in the bank “funding gap” is something we are watching closely

They do not. From the IMF:

Three structural features of monetary systems form the starting point for this paper. They include (1) a two-layer structure comprising a private sector agent deposit system with commercial banks, parallel to a commercial bank deposit (reserve) system with central banks, with the two being separate and not allowing transfers between the two, that is, reserves cannot be “lent out” to the private sector (Sheard 2013); (2) the fact that money is created upon the creation of bank loans (Werner 2014/16) while repayment implies money destruction, both of which are an accounting reality, and implying that banks would better not be called “intermediaries”; and (3) the fact that the money stock is endogenously and elastically driven by demand and constrained loosely by regulation. The constraints to the provision of new credit include capital regulation, banks’ conditionality on an incremental profit prospect, and, eventually, demand (McLeay et al. 2014)1. Link

Yes, they do need deposits to fund lending growth.

Banks need to maintain lending to deposit ratios, both with RBNZ and, if you'd bother to read the article, with investors (wholesale or otherwise). There is a fundamental misunderstanding of this by some commentors.

It is true that a credit contract creates a matching deposit via money creation nature of lending. But, the bank doesn't keep that - this goes to the seller of course who may or may not bank with a different institution or use funds differently - like managed funds, shares etc, effectively exiting that cash from the system. Banks need to attract and retain deposits to continue to comply with RBNZ and investor needs.

If they didn't would you like to explain to me why they bother attracting deposits at all at a rate significantly above the OCR?

...(2) the fact that money is created upon the creation of bank loans...

In simple terms:

We start with the idea of credit creation, specifically a swap of IOUs between a bank and myself involving a bank loan that is my IOU and a bank deposit that is the bank’s IOU. Nothing could be simpler, and yet the mind rebels, especially the well-trained economist’s mind, because this simple operation increases my purchasing power without decreasing anyone else’s. It seems like alchemy, or anyway a violation of some deep conservation law. Real productive resources are the same as they were before, and the swap doesn’t change that, does it? Spending of the new purchasing power adds another layer of perplexity.

If spending increases but real resources do not, then it seems logical that the increased spending must exhaust itself in higher prices—that is the intuitive appeal of the quantity theory of money. My purchasing power may increase, but everyone else’s decreases because their money balances buy less. From this point of view, the alchemy of banking seems like a kind of theft, something to be deplored in the name of economic science and if possible outlawed in the name of the general good.

A simple concrete example may help to fix ideas. Let us suppose that the swap of IOUs is a mortgage loan, and that I use my new purchasing power to buy your existing house. At the instant of sale, I swap one asset for another, and you swap the other way around, presumably because each of us prefers the asset held by the other. For present purposes, the important point to appreciate is that the alchemy of banking has made this sale possible, by creating new means of payment that you are willing to accept. After the sale, the bank’s new IOU is owed to you instead of to me. In fact, by accepting the bank’s IOU as payment, you are funding the bank’s loan to me, at least temporarily.

But that’s not the end of the story. You were willing to accept new purchasing power as means of payment for your house, and in doing so you wound up funding the bank’s mortgage loan in the first instance. But by no means does that mean that you are willing to fund the loan for its entire term. Indeed, what matters after the moment of payment is not so much your own portfolio preferences as the preferences of the rest of the world to whom you pass along the new purchasing power as you spend it. The question is, when you are no longer funding the loan, who is and in what form? Read more

If they didn't would you like to explain to me why they bother attracting deposits at all at a rate significantly above the OCR?

Time value of money?

Yes, they do need deposits to fund lending growth.

Audaxes is aware of this, but in reality, it's a secondary almost superficial consideration.

ANZ stock pays a 6.8% dividend yield[1]. ANZ term deposits pay up to 2.7% according to this site. Any wonder why saving rates are so low? Everyone's borrowing to invest, because the risk-free rate is barely above inflation.

Bit of irony there. I think ANZ's margin lending rates are close to 6.8% for those willing to "take a punt."

More than 20 years ago, I reached an initial agreement to fund NZ government bond purchases with a local bank - a borrowing rate that made the arrangement cash carry positive was revoked a few days later with many apologies. And that was that.

Another comment with more holes than a fishing net. Were you using the NZGB as collateral? what term were you funding it for? It's very common to fund bonds positively if you use the repo market and the curve is normal, definitely not some arbitrage opportunity snatched from your grasp that's for sure.

None of your business.

I remember a while back you and your cohort were unable to discern a simple interpolated T bill yield accepted at an RBNZ D3 open market operation.

You are the Walter Mitty of Interest.co.nz and I want my prize.

I recall that being done in the 80's. Government Bonds at an attract arbitrage rate were available to Private Individuals up to $250,000 each. The bank could fund the purchases from simple money market operations, and to achieve the Private Individual status lent $250,000 to each staff member, all 300 odd of them, using the purchased bonds as collateral. Many of the staff and management went off in later life to form - Macquarie Bank. (NB: What many staff members didn't realise is that the taxman came a-callin' the next financial year looking for Provisional Tax to cover the additional 'earnings' they had accrued from the previous year!)

The bigger issue is the finance haircut due to credit worthiness. GC+ is what it is - marked to market takes care of the term. In NZ the real tax risk is the discount to par redemption purchase price. Below par purchases are pro-rata accrued annually at Inland Revenue marginal income tax rates as are realised capital gains. Furthermore, tapped, seasoned T Bill purchases are taxed at the original one year issuance term even if the purchase term is less at maturity. One day before maturity bed and breakfast deals with a bank market maker are mandatory. I investigated this issue with IRD, they gulped and said the law was set at a mandatory 33% tax rate for all banks' trading activity and did not take account of individuals and changing the law for the three registered at the NZDM treasury security repository at Computershare was not feasible.

Well its quite simple , the Banks are going to be facing some margin squeeze . If they need deposits , they are going to have to pay better interest rates

The RBNZ is constantly saying we all need to "put our money to work"and now we get complaints people aren't depositing in banks. Make up your mind!

The problem is it's not our money that we're putting to work. We're borrowing it from someone else.

Most people will be taken in by another article like this one mis-representing what banks do. David Hargreaves actually thinks that banks need deposits before they can lend. They don't. The Bank of England (and the German Central Bank and our own Reserve Bank and many others) says this on its website - "In the modern economy, most money takes the form of bank deposits. But how those bank deposits are created is often misunderstood: the principal way is through commercial banks making loans. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks:

• Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.

• In normal times, the central bank does not fix the amount of money in circulation, nor is central bank money

‘multiplied up’ into more loans and deposits."

More can be found here - http://tellmemore.org.nz/

S Creditor,

I think most of us know this already, but are you then implying that banks don't need actual deposits as well? If so, you are, in my view, quite wrong.

Clearly most people don't know it. Just read the next comment. Yes, banks need to attract deposits so that they have something to back up the loans they've already made. (note - the lending comes first and then they seek to attract the deposits). Those deposits they attract however amount to only to a small proportion of the value of the loans they've made - hence the term 'fractional reserve' banking. Of course they know that they will get their share of deposits if they all keep their deposit interest rates round about the same. And of course they are all lending so therefore creating that pool of deposits from which to attract their share. What they don't do (which most people believe and which the article seeks to reinforce) is lend out money people have deposited with them. They are essentially factories that manufacture credit.

You seem to be implying that the bank doesn't need the capital to loan it to a borrower. That it's all just credits and debits against accounts in computers. But surely the bank must have the money to lend? Or do they themselves borrow the money from someone else. Who in turn may have borrowed it also. Where does it end? At what point does this numbers game actually end up with something real?

Correct. I'm not implying that, I'm stating that - and my position is backed up by numerous authorities - Bank of England etc as stated. More of those authorities can be found here - http://tellmemore.org.nz/

Banks do need capital - the Reserve Bank is trying to get them to increase that to around 16% of the value of their loans, but they don't lend capital. They also need deposits, but they don't lend those either. See my answer to the question above. The only thing that's real is the asset you transfer into their ownership as security for the credit they manufacture to 'lend' you.

Well ANZ? don't just sitting there waiting for the fart winds/methane gas from the stocks - do something about it.

Remember the RBNZ advise? - spend, spend, spend, credit, credit, credit, loan, loan, loan - do let us know, which advises that resemble save, save, save - deposit savings are just simply for the looser right? - There's nothing to discuss, NZ Banking & RBNZ already decided one way to beef up NZ economy. So? why start to elaborate a different notes here? - Are you about to change the tact voice now?

All signals points towards bubble and disaster BUT who cares as long as the party is on - for Fed and Reserve Bank along with Government all over the world will do anything and everything to supply cheap and free Booze (Money) for the party to continue :)

Who can say othwise when property / stock market is touching new high and no one knows why, except free and cheap money so party hard atleast for a year as still OCR can be dropped by 1% and than waiting to test negative territory with everoine more eager to throw more money in.....

Logic defies that world hit by Coronavirus but stock market touching new Heights - this itself suggest the market that we are in.............even if world collapse market may be touching new heights....Economy prinicipal to change and have to be rewritten.

Earlier advise was save and spend but now the new mantra is Borrow and Spend so the basic principal has changed and with FOMO and with demontration effect on general public, things are going from bad to worse and this so called party is disaster in making. From here on government to avoid the consequence will have no choice but to throw cheap and free money.

Unless and untill small and medium business grows (unlike asset class only), it will be hard to delay consequences for long.

Right, so clearly you don’t understand bank funding under local legislation

Jeez, didn't see that coming.

The RBNZ should slowly increase the current interest rates, which would result in the following benefits:

- reduce the perverse phenomenon of savers subsidizing parasitic house speculators

- reduce the phenomenon of bank deposit growth disappearing, due to ridiculously low interest rates

- promote saving, at the expense of unsustainable consumption, debt building and housing speculation

- yes, there would be some short term pain, but it is better to have some pain now rather than a catastrophic re-balancing of the economy caused by the bursting of the housing bubble later on

fortunr - the RBNZ won't have to, the banks will do it for them. The banks will be in no position but to raise lending rates, and then deposit rates, for some of the reasons discussed here, and in response to the bank capital changes - expect to start seeing it over the next few months. The bigger risk is that the RBNZ reacts by cutting rates, a counterproductive move but one that wouldn't surprise me since globally we're in a death spiral that the central banks don't seem to know how to extract themselves, and their economies, from.

JK of ANZ already visited CCP no 1 asking about loosening up this China capital control outflow for NZ. So? don't worry, no need to rely on cheaper/less local funds, China is more than happy to lend it.. everywhere in this world, they've build those savings through the past 50 years of cheap labour, fixing it's currency etc. - now those untapped resource is seeking to be loaned easily, the catch is just two: 1) allow to buy land 2) allow people movement. - That's why to some country, such as India, you're unable to spot this activities.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.