Credit bureau Centrix says businesses appetite for debt has started to bounce back, suggesting business confidence may be improving.

With Omicron restrictions easing in late March and April, business debt demand has risen, Centrix Managing Director Keith McLaughlin says in the company's April Credit Indicator.

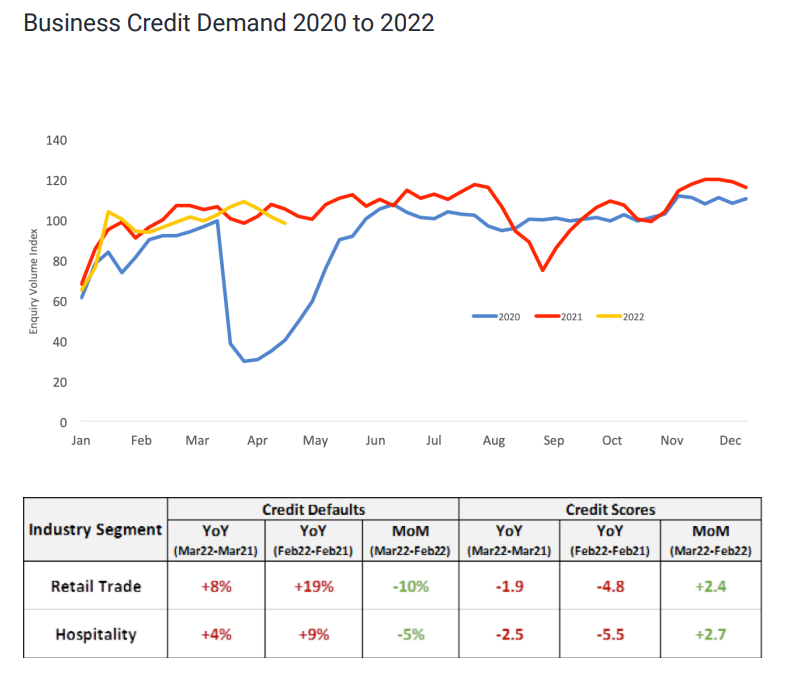

"While business credit demand is down 7% year-on-year in April, the average credit score for new applications is up to 771 – a four-point increase on March 2022. While defaults are still up year-on-year in certain sectors like agriculture, tourism and hospitality, the improvement from last month could be signalling a return in business confidence."

"Coupled with the borders reopening incrementally during the coming months, Aotearoa’s business communities could be looking at an increase in holidaymakers spending locally and a returning international workforce," McLaughlin says.

Reserve Bank sector credit data shows business debt rising this year, with business debt reaching $125.725 billion at the end of March. That's up more than $2.5 billion since December.

Centrix goes on to say that a decrease in credit defaults could indicate signs of recovery across New Zealand, or businesses managing their cashflows and making tough calls before getting into financial distress.

"In particular, the retail and hospitality sectors are showing signs of recovery. While still down year-on-year, both credit defaults and scores have improved from March 2022, reflecting the resilience of these sectors. However, both agriculture and tourism are facing the strongest headwinds as labour shortages, supply chain disruptions and rising costs continue to be a challenge."

The latest ANZ Business Outlook Survey shows business confidence remained very low in April at -42.0. However, a weakening outlook in the residential construction sector offered signs inflationary pressures in the economy may start to weaken, though they remain high for now.

McLaughlin says overall demand for consumer credit is down 6% year-on-year, with average credit scores dropping three points month-on-month. Against this backdrop, loan arrears are increasing across the board, with McLaughlin suggesting people are starting to struggle to make repayments due to rising costs of living.

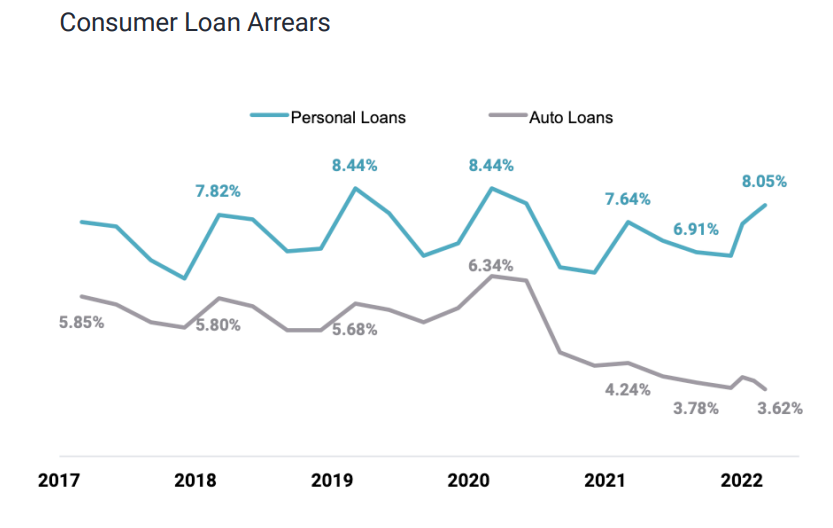

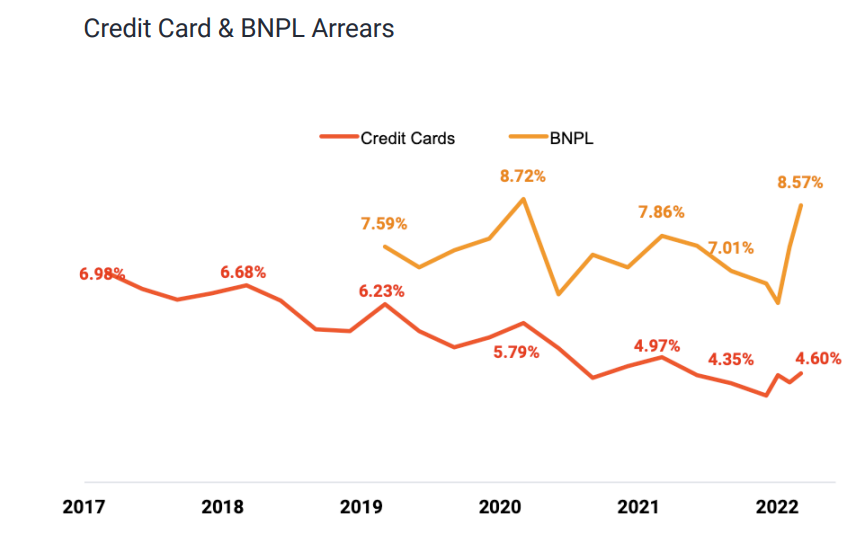

"The number of consumers in arrears is up 5% year-on-year in March 2022, driven primarily by increasing arrears for personal loans, buy now pay later accounts, and telco plans. Missed payments on mortgages and vehicle accounts remain low, as people are focusing their spend in these areas. When money gets tight, people are more likely to prioritise these credit payments over personal loans," McLaughlin says.

Arrears on unsecured personal loans have risen to 9% year-on-year – their highest level since May 2020, he says.

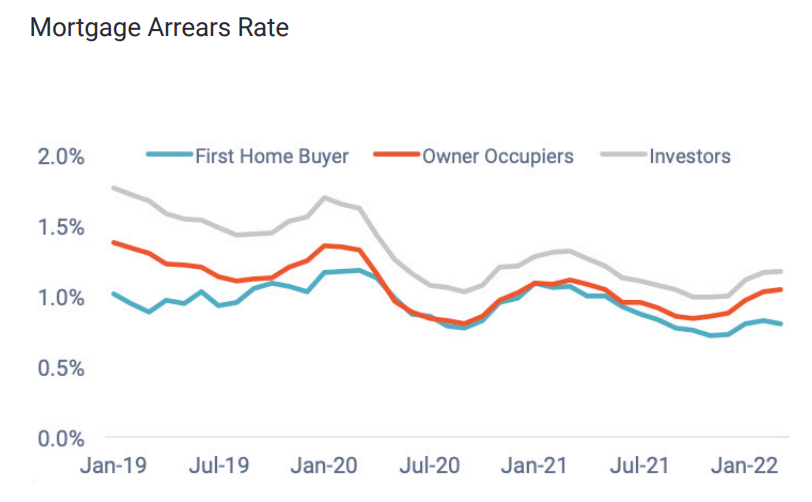

In terms of home loans, McLaughlin says arrears rates for both investors and owner-occupiers have started rising off a low base, an early signal of increasing financial hardship and a potential sign of future trouble.

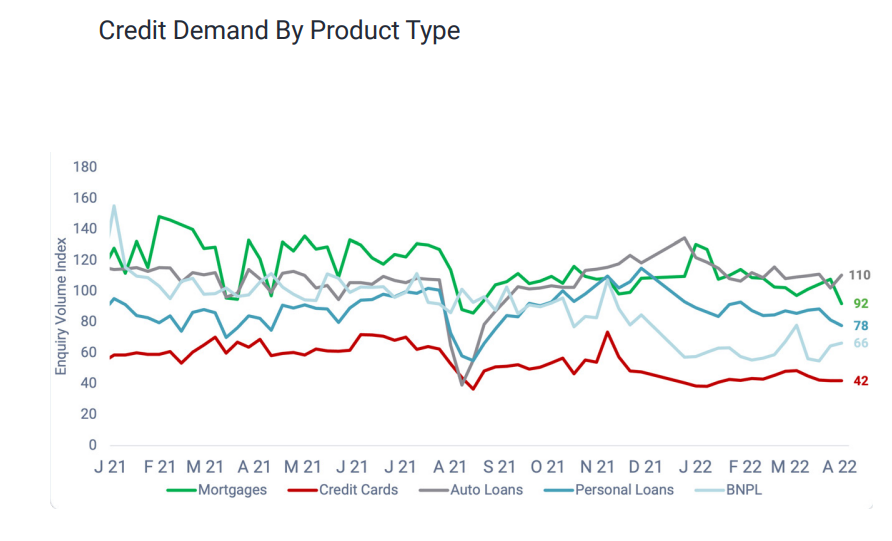

"In alignment with recent CoreLogic data outlining weak property sales, the demand for mortgages has also fallen by 12% year-on-year in March 2022. The value of mortgage lending was also down 30% year-on-year as the market tightens and the lingering impact of the Credit Contracts and Consumer Finance Act changes continues to affect loan conversion rates," says McLaughlin.

"As interest rates continue to climb, the squeeze is likely to be felt by homeowners and investors alike in the coming months."

After dropping to the lowest level since it was launched in 2004 for two consecutive months, the ANZ NZ-Roy Morgan Consumer Confidence Survey lifted 6 points in April to a still very pessimistic 84.4.

8 Comments

It was all about the lockdowns.

Business debt demand rising is good.

In last two years many small to medium businesses were diverting from their core business to housing speculation as were witnessing fast, easy and BIG money that could not even be dreamed in their business and that too without any compliance and regulation. Now that tide is turning ........

Confidence that housing sector ponzi or whatever, one may call is so big that politicians and central bank are trapped and will always be forced to support and promote is falling apart with realization that courtsey central bank and support from government could manipulate to a certain extend and could only delay the inevitable but not avoid - economy cycle.

Bigger the rise - Greater the fall.

I guess you really believe that - SME's jumping on the speculator wagon. I didnt even contemplate that, over the last 2 years we have seen 30+ % increases yoy in sales and profits in my business, every last dollar I could scrape together was poured back into the business to try and keep up with the growth.

I think Centrix are going hard and early, Im predicting, conservatively, that my business will see a 15% drop in sales this year, followed by probably worse than that next year.

As an aside, most small businesses dont have a shit show of raising capital from the bank unless it is secured by a house, or you have millions in stock and absolutely stellar accounts. The biggest issue this country has is a lack of capital, and what there is being largely tied up in unproductive houses, land and other such useless assets.

Wellington commercial construction firm Armstrong Downes announced their shutdown yesterday ... the latest in a long line of small to medium sized construction firms to go bankrupt in recent months .... all around NZ , these companies are burning out , even though their debts may only be in the order $ 500 000 to a $ million or so ...

All is not well in Godzone , very far from it !

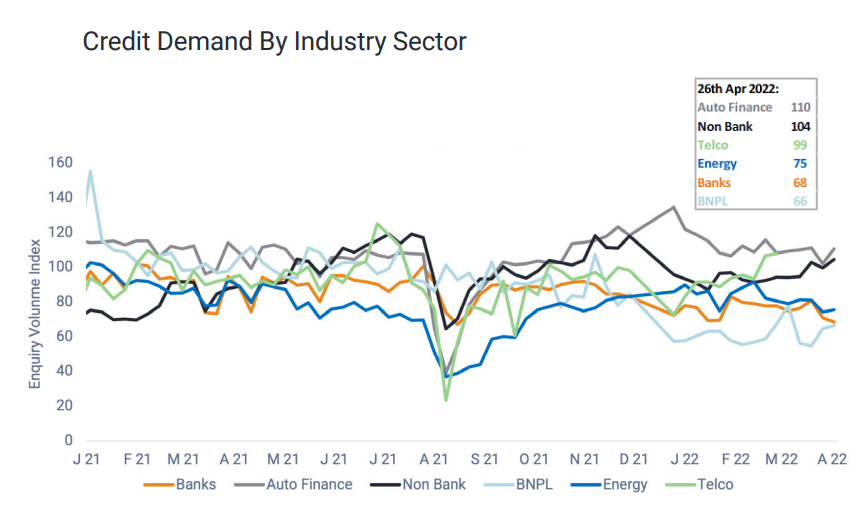

Businesses may also be having to take on more debt to pay for the increasing costs of shipping, products, materials and staffing.

I imagine the increasing debt load is more out of necessity than widespread business expansion. Securing debt against rising residential property values is problematic, so business funding increasingly relies on the internal balance sheet.

Rising debt in Australia

From smh

"Much will depend on how the generation of borrowers who have never experienced a period of interest rate increases react to higher mortgage costs. The risk that higher rates cause an accidental recession is very real."

RBA expected to raise ocr by 0.15% to 0.25%, today.

"At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 35 basis points. It also increased the interest rate on Exchange Settlement balances from zero per cent to 25 basis points."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.