By Gareth Vaughan

Kiwibank CEO Paul Brock says interest rates are already low and the Reserve Bank doesn't need to cut the Official Cash Rate (OCR) "right now."

Brock was responding to a question in a media briefing on Kiwibank's half-year financial results about whether New Zealand needed lower interest rates.

"I think we've got low interest rates," Brock said. "My view would be not right now, but that's in the wisdom of the Reserve Bank as to all the stats they're seeing."

The OCR is currently at a record low of 2.50%. The next OCR review is on March 10 and some economists believe the Reserve Bank should cut the OCR further due to almost non existent inflation.

Brock estimated offshore wholesale bank funding costs were up about a third year-on-year, but said Kiwibank wasn't significantly affected by this given it's predominantly funded through domestic retail deposits. The bank said it's using deposits to fund about 80% of its home loans.

Kiwibank's December quarter cost of funds was 3.5%. And Kiwibank's Core Funding Ratio at December 31 was 86.1% versus the Reserve Bank mandated minimum of 75%. The industry wide figure at December 31 was 85.8%.

Brock also suggested the Reserve Bank shouldn't cut the OCR to offset rising funding costs for Kiwibank's four Australian owned rivals.

"I would've thought that given the profitability of the other big banks, it shouldn't be an issue for the Reserve Bank. It's really a supply and demand equation about how much they want to grow in the New Zealand economy versus how much they want to grow in the Australian economy," said Brock.

He added, however, that competition among banks for deposits had been strong over the past six months with "a lot of fight." Kiwibank's deposit rates are "very competitive," Brock added. Bank deposits weren't leaving en masse to other forms of investment, which was sometimes seen in a low interest rate environment.

"I guess that goes a little bit to the confidence of investors given where the economy's at."

See all carded bank deposit rates here. And here's our recent story comparing deposit rates across the banks.

Meanwhile, Brock reiterated that Kiwibank has no plans to enter the rural banking market.

"At this stage it's not appropriate for Kiwibank to be entering the rural market. It's not to say a New Zealand bank over time at some point might go in. But if we look at the cycle they're in, the stage we're at as a bank, we've got enough on our plate. We're not rushing into the rural market at this point," said Brock.

Half-year profit flat at last year's record high

Kiwibank's net profit after tax for the six months to December 31, 2015 was $71 million, unchanged from the equivalent period of the previous year equally its record high for interim profit.

Net interest income rose $10 million, or 6%, to $189 million. However, total operating revenue was up just $5 million, or 2%, to $245 million as net fee and other income fell. The bank's operating expenses climbed $13 million, or 10%, to $146 million. Kiwibank's impairment allowance dropped $3 million to $6 million.

Expenses rose as Kiwibank pushes on with a multi-year upgrade of its core banking system, which Brock has said will cost "more than" $100 million. The bank's currently working through phase 2 of the project, which includes migrating savings and transaction accounts to the new SAP system. Brock says phase 3 is still to follow, which will include moving across lending systems and customer records.

Phase 1 was completed last August, bringing across inwards and outwards payments to the new system.

Asked whether the project was on budget, Brock said it was "broadly in line."

"I think at the end of the day it's a multi-year programme, they're pretty complex, they always seem to take longer and be more complex than what you expected. So how you establish budgets around these things is an ongoing process, but we're broadly in line with what we've expected for the first phase. The second phase is costing a little bit more and we're in that at the moment. It's a very complex phase," said Brock.

He said he wasn't sure how long phase 3 would take.

"(But) I'd expect as we get towards the end of 2017 we should be getting close to finishing. But I don't have an exact date on that at this point."

Lending & deposits growth 5%

Across its half-year Kiwibank grew gross lending - home loans, business banking and credit cards - by 5% to $16.35 billion. Customer deposits were also up 5% to $14.43 billion.

Meanwhile Brock said Kiwi Group Holdings, the NZ Post subsidiary that includes Kiwibank, Kiwi Insurance and Kiwi Wealth, is on track to top last year's annual profit of $127 million after tax. He acknowledged, however, that the second half-year was likely to be tougher than the first-half, although the economy had been "surprisingly resilient."

"We are seeing the economy slowing a little in the second half. One of the things we will see with interest rates being a bit lower, that might make the second half a little more challenging. However, we've got good growth from the first half on track so the NIM (net interest margin), provided it holds, we should be okay for the full-year compared to last year," said Brock.

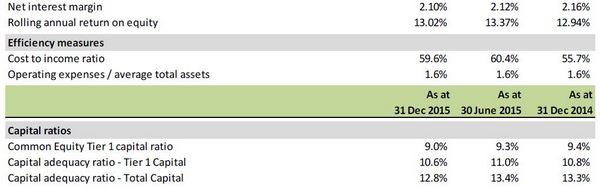

The bank's net interest margin fell six basis points to 2.10% in the December half from 2.16% in the equivalent half of the previous year. It was also down two basis points from Kiwibank's June 2015 year figure of 2.12%. The bank's cost-to-income ratio rose to 59.6% from 55.7%.

Kiwibank paid $24 million in dividends to NZ Post during its half-year, equivalent to 34% of net profit after tax. Kiwibank has no specific dividend policy, but Brock said there was a "strong dividend track going forward."

Kiwibank profitability measures

20 Comments

Chief executive Paul Brock said because the bank largely funded itself with deposits from customers it was seeing little impact from higher offshore borrowing costs, however he believed the cost of borrowing for its rivals was up around one third on a year ago "maybe a little higher in some terms".

With higher funding costs hitting rivals who borrowed offshore to fund new loans here, Kiwibank was sitting pretty.

"While we're more domestically funded, it will give us an advantage. It really depends on the amount of cash floating around the economy. Right now there seems to be a fair amount floating around."

Higher funding costs could add weight to calls for the Reserve Bank to lower interest rates to boost banking margins to a bid to stimulate new lending. Read more

Why are savers expected to subsidise debtors, including banks - since when has being a bank depositor equated with acts of charity? It is obvious from Brock's comment foreign wholesale banks perceive that lending to our banks represents a higher risk and demand a higher rate of return. Why doesn't the regulator demand the same?

Exactly, I may be reading between the lines here, but I believe Paul Brock is really highlighting how dependent KB is on depositors to grow, thus as the OCR is likely to get lower and lower to the point where these new depositors may dry up or withdrawal on mass. This seems to be his real underlying concern.

I would just like to say to Paul that just because the RBNZ drop the OCR you need not be mandated to drop your banks savings/TD's, and PIE's interest rates also! How about actually encouraging savers rather than making them the subsidy for your exposed loan portfolio?

Stephen has made two points, the second being that borrowing overseas is more costly than using depositors funds, which means the overseas lenders see a higher risk here. Are they reacting to the diary collapse or waiting for something else to occur, like housing bubbles bursting?

Why are savers expected to subsidise debtors, including banks - since when has being a bank depositor equated with acts of charity?

A good point. When the nation is overindebted, it would seem.

The question I cannot get my head around is this. In 2000, household debt in little old New Zealand was $60 billion, by 2008 it was $160 billion, now it is $210 billion. In order to make it possible for kiwis to make their interest payments, the interest rate has been modulated downwards by the RBNZ. The economists and politicians think that as long as debt doesn't grow faster than GDP then all is well and we have a sustainable system. Is this so?

http://www.interest.co.nz/charts/credit/housing-credit and click on the $ Amount tab.

I have a nasty feeling that the comfortable view of the RBNZ, the banks, economists and political and bureucratic classes may be false. I guess I'm saying that modulating the interest rate to offset the trebling of principal outstanding can only work for a time, before a major redistribution of asset ownership follows.

My understanding is that credit availability drives house prices; rising credit gives rising house prices, this gives rising collateral, which leads to rising credit, and the cycle repeats. So banks' willingness to lend is the primary driver.

As you have so painstakingly pointed out (many thanks for that, by the way), the banks' ability to lend ever increasing amounts over the last few years has been based on a wholesale (mainly Eurodollar, possibly Asian dollar) funding explosion.

The result is a massive increase in principal outstanding against kiwi houses, from $60 billion to $210 billion. Can this go on for ever, or is it self regulating at some point?

Well a) if you dont like being in a charity, go elsewhere.

What!!! - create a bank run.

You might need one of these..

http://www.jamesbull.y9.co.nz/safes-locksmiths.html?gclid=CJXnn-PXjMsCF…

Yes I might.

Buy shares in safe manufacturers

Safes Sell Out In Japan, 1,000 Franc Note Demand Soars As NIRP Triggers Cash Hoarding

http://www.zerohedge.com/news/2016-02-22/safes-sell-out-japan-1000-fran…

You're right about the shares !!

We might see adverts like the hoarders guide to the bureaucracy!

for the truely paranoid,

https://www.google.co.nz/search?q=tactical+gun+safe&biw=1793&bih=878&tb…

So free market rules, and economics 101 - suppyy/demand, as he says " fair amount floating around." so all this "investor" money looking for somewhere to give a return, but too few businesses are borrowing.

Bank claims are rising much faster (2x plus) than nominal GDP. Let's not forget these claims/assets are created by the banks themselves, hence the deposits arising from them. Mr Brock is being economical with the truth to defend the indefensible requirement to pay the risk adjusted return depositors are entitled to. The foreign wholesale lenders have demanded one third more to compensate for risk and got it.

Never forget, from the Bank of England - "Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits" … "In normal times, the central bank does not fix the amount of money in circulation, nor is central bank money 'multiplied up' into more loans and deposits."

Supply and demand, want a better return? take your money and invest is elsewhere.

so instead of say 3% they got 4%? whop dee doo doo.

What is interesting is the table that indicates their latest Cost to Income ratio is 59.6%. does this mean their profit margin is 40.4%? Or what are they not telling us? Great business, banking!

At very low rates, percentages-of-percentages are a confusing thought trap. Best to look at the NIM (net interest margin). That is 2.1%, and falling. That compares with the sector here.

OK David, but Interest income is only a part of the total picture. For example that table indicates that while the banks earned $2.3 billion in interest they also reported $864 million in other income. Also forgive me for being a little cynical but only 2.1%? Mind you, on the sums they are talking about, it is still a lot of money.

At least table doesn't report the degree of imbalance that 90 Secs at 9 am reports HSBC has.

Kiwibank obviously does not have many dairy farms on its loan register.

With the NZD heading north towards 0.70 come March 10 the RBNZ will not only have to reduce the OCR, it will now have to over-deliver and reduce it by 0.50 for the reduction to have any useful effect.

The RBNZ has painted itself into a corner.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.