ANZ Bank New Zealand's annual profit is down 13%, hit by a series of one-off items and higher bad loans.

The country's biggest bank says September year net profit after tax fell $229 million, or 13%, to $1.542 billion from a record $1.771 billion the previous year.

ANZ said its 2016 financial year included charges of $178 million associated with "specified items." Excluding these items its annual cash profit, which fell 9% to $1.53 billion, would've only been down 2% to $1.66 billion.

The specified items were described as an accounting change to the application of the ANZ Group's software capitalisation policy, changes to the methodology for credit valuation adjustments in determining the fair value of derivatives to align with evolving market practice, and restructuring costs. Software capitalisation changes took $37 million off annual cash profit, restructuring (of staff and branches) took $16 million off, and credit impairment charges $70 million.

In its half-year results in May ANZ outlined a $87 million charge associated with an accounting change to the application of the ANZ group's software capitalisation policy. This brings forward the recognition of software expenses resulting in lower amortisation charges in future years.

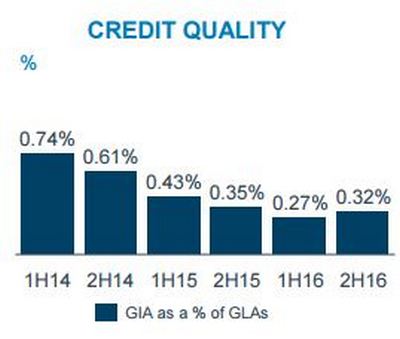

The bank's annual provision for credit impairment jumped $73 million, almost doubling, to $149 million. ANZ attributed the increase to "ongoing normalisation" of provision levels in its lending portfolios, plus lower levels of write backs and recoveries. There were also higher new provisions in ANZ's rural lending. The bank said in its rural loan portfolio gross impaired assets as a percentage of gross loans and acceptances rose to 1.15% from 0.69% a year earlier. Of the bank's $18 billion agri lending portfolio, 67% is dairy lending.

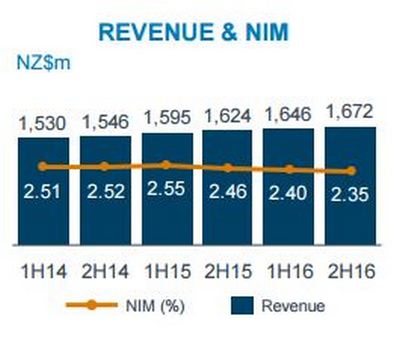

Meanwhile, ANZ's net interest income rose $149 million, or 5%, to $3.029 billion, but its total operating income was down $61 million, or 2%, to $3.824 billion. Operating expenses rose $102 million, or 7%, to $1.58 billion, which was attributed to the software capitalisation charge and restructuring costs. If these items are excluded, ANZ said expenses actually fell 2% reflecting "disciplined" cost management and productivity gains.

ANZ supports RBNZ tightening the screws on property investors

Gross lending rose 5% and customer deposits grew 8%. Nonetheless CEO David Hisco said a challenge for the New Zealand economy at the moment is the slower overall rate of deposit growth than lending growth, noting the banking sector makes up the difference through offshore funding, which is "relatively" more expensive.

"Many New Zealanders see housing, particularly in the current low interest rate environment and in cities like Auckland where there is high demand for accommodation, as the most profitable way to get a return on their money," Hisco said.

"That's why ANZ New Zealand supports the Reserve Bank's tightened restrictions on investor residential lending." (See more from Hisco on this here).

ANZ says its residential mortgage marketshare dropped year-on-year to 31.5% from 31.6%, while its share of household deposits increased to 31.7% from 31.2%.

ANZ's fall in annual profit comes after BNZ last week posted a $125 million, or 12%, fall in its annual profit to $913 million. Westpac reports its annual results on Monday. ASB, which unlike the other three Australian owned banks has a June 30 balance date rather than a September 30 one, reported a $54 million, or 6.3%, rise in annual profit to $913 million in August.

NZ wealth business to be reviewed next year

Meanwhile in Australia, the ANZ Group posted an 18% drop in annual cash profit to A$5.9 billion. CEO Shayne Elliott said the "core" domestic Australian and New Zealand businesses had performed well, but the result reflected the "significant reshaping" of the group to create a simpler, better capitalised and more balanced bank. The group net interest margin fell four basis points to 2.00%, and return on equity dropped to 10.3% from 14%. Total fully franked dividends for the year dropped 12% to A$1.60 per share.

Elliott also said a strategic review of ANZ's wealth business across Australia and New Zealand concluded that ANZ doesn't need to be a manufacturer of life and investment products. The ANZ Group is thus considering selling its life insurance, advice and superannuation and investments businesses in Australia. The New Zealand wealth business will be considered separately in 2017, Elliott added. (Here's a video interview Elliott did with ANZ's BlueNotes website).

Below are some charts covering the ANZ NZ results.

*NIM is net interest margin.

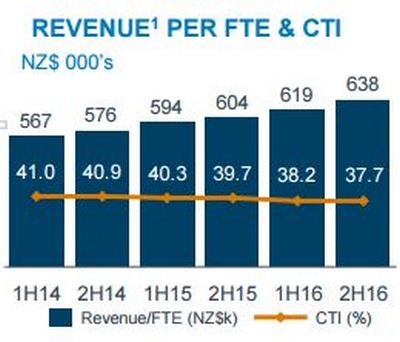

*FTE is full time equivalent employee. CTI is cost-to-income ratio.

*GIA is gross impaired assets. GLAs is gross loans and acceptances.

11 Comments

So ANZ made $1'542 Million profit... it's just that, for once, it's not a record profit (like last year), they still made $1'542'000'000 PROFIT in a world that's in turmoil !

They account for 31% of the market so that's about $1100 profit from each man, woman and child within their market share.

Kiwiimm/Seekae - So what are you suggesting,the corner dairy that only makes $100 profit off everyone in the community is more worthy than a bank that is putting up billions of dollars of capital to fund 30% of all NZ's funding requirements to operate the country ? What do you expect them to make off each man and woman, and if its materially less, do you expect to do so because it won't be them, Kiwibank? Yes I agree, stupid discussion

Disgraceful, the whole system is a joke.

Although lets remember, all these profits and just numbers on a computer and have technically been created out of thin air.. Lets break it down to simple terms. Im a bank. You want $10 from me but i only have $5. I say ok and create $10 on my computer and transfer that into your account with the guarantee that you will pay me back $12. So from my $5 i will then have $12 for doing absolutely nothing. Explain that please. Bring back the gold standard asap.

I would like to reiterate my disdain for the very well paid Hisco by asking, yet again, that the RBNZ to impose stricter lending criteria on the banks. Hisco can of course implement these policies himself. ANZ management is ultimately responsible for the quality of its lending book and will reap the reward for more prudent lending if its predictions are correct. Or is he effectively saying that the banks are managed by a cosy oligopoly in league with the RBNZ and cannot operate without some sort collusion? These comments need to be challenged by media, not just reported verbatim.

ACB, I think we addressed at least some of what you are talking about here - - http://www.interest.co.nz/news/82733/anz-ceo-david-hisco-says-nz-needs-…

Hi Gareth, yes you asked the question in that piece but I thought Hisco's response doesn't stand up to rational analysis i.e. I won't do what is right because my 'competitors' won't and I'll lose market share. How can that approach be in his shareholder's best interests? If Hisco is right about housing and his competitors are wrong then ANZ will be looking to be in a pretty strong position whilst his competitors will be in a very difficult spot. Chasing market share at the expense of lending standards is a sure way to bad debt purgatory. It just reeks of short term thinking and staying with the crowd e.g. if we lose, we all lose together is better than winning alone.

Sorry ACB, Hisco is in the real world. He is saying that not reasonable to expect bank boards to explain to the market why they have less profit and value growth than competitors, because they see some issue round the corner that the market doesn't see, and the deserve share market support on that basis. Both in loan quality, funding term and profits the regulators play a pretty important role, looking round corners and ensuring banks can survive. Give the man some credit for encouraging the regulators to do their role which helps him do his. What the average person can do is put our money where our mouth is - identify the well managed banks, and put our deposits with them and buy their shares. If you happen to right about the outlook, it will reward us handsomely, to do that.

Dave2, sorry your defence of the ANZ is difficult to understand. If all a bank manager has to do is follow what the regulator does then it shows that there isn't much value add for bank shareholders in paying someone many millions per annum. These guys are paid a lot of money to make the strategic calls and take prudent risks. Your last comment about depositors putting their money where their mouth is, seems to contradict your first comment, since if every bank is following the other (or the regulator) then how can you be rewarded for picking the well managed one?

Put it this way, what Hisco is essentially saying is that "I think lending is getting a bit reckless but heh, I am going to keep lending aggressively too, at the expense of my shareholders interests. The reason is because if I put my house in order my competitors will take the market share I don't want (bad debts) away from me." The unspoken part of Hisco's thinking is that his incentive structure is not well aligned with shareholders best interests.

ANZ has become a much for frustrating place to work over the last year since Shayne Elliott became CEO and relentless cost cutting has become order of the day. In my section training and development has been virtually eliminated, and people that leave are not replaced. Bonuses have been slashed. In addition to that the usual share offer of $800-1000 to eligible employees has been scrapped altogether.

As an employee it is exasperating to see them make such massive profits all the while screwing over their employees endlessly. Previously it wasn't too bad but having a bean counter as CEO has basically meant anything that can be taken from employees is.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.