A sharp drop in intended residential and commercial construction activity is one of the notable features in the latest ANZ Business Outlook Survey.

And businesses generally are sufficiently down in the dumps for ANZ Chief Economist Sharon Zollner to stress that she sees the next official interest rate move as more likely to be down than up.

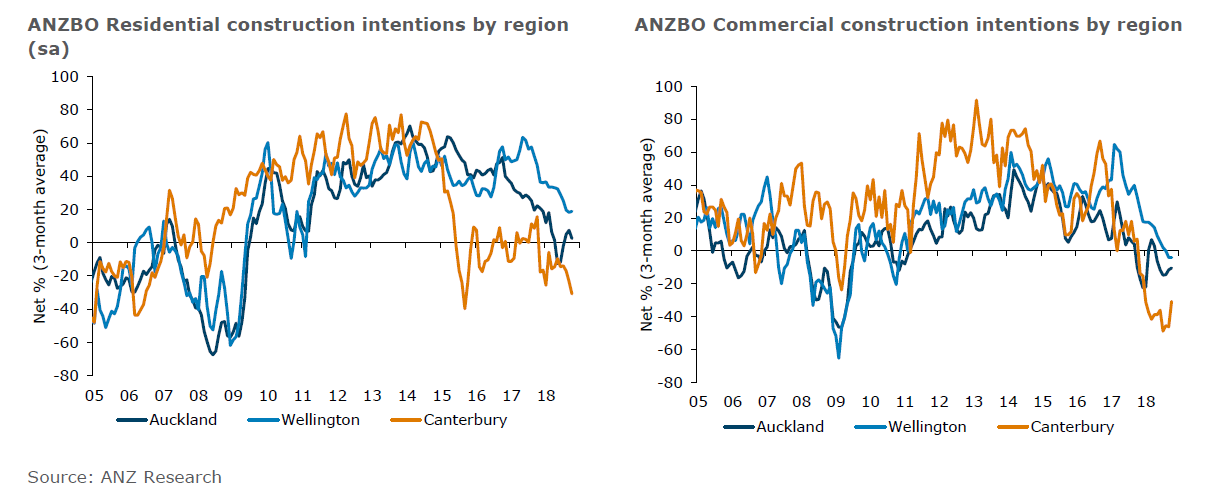

According to the survey residential construction intentions dropped 19 points to a net +5%, while commercial intentions fell 20 points to -24%. Canterbury is the particularly weak on both fronts, while Wellington is the strongest main centre but is trending down.

Elsewhere in the survey, confidence is no longer plummeting, but not showing any particular signs of rising again either.

Another down-in-the-dumps business survey will not be good news for a Government that has been trying to get alongside business and raise confidence levels.

The falls in levels of intended construction activity may ring some alarm bells as the Government seeks to ramp up residential activity through its Kiwibuild programme.

In commenting on the falls in construction intentions, the ANZ economists say while it has become less clear that residential construction intentions lead residential consents, the downward trend certainly doesn’t suggest consent growth is about to take off.

They point out that commercial construction is "lumpy" in any case and no indicator is going to match it closely, "but the ongoing fall in surveyed construction intentions suggests downside risk".

"By region, it’s a similar story for both commercial and residential construction: Canterbury is the most pessimistic (though commercial has bounced somewhat). Construction intentions in Wellington are the strongest but are trending downward, while Auckland intentions seem to have found a floor. (Note the charts are 3-month averages)."

Elsewhere, the survey shows that both headline business confidence and firms’ views of their own activity were steady in October at low levels.

Headline business confidence lifted 1 point to a net 37% of respondents reporting they expect general business conditions to deteriorate in the year ahead.

Firms’ perceptions of their own activity prospects eased 1 point to a net 7% expecting an improvement, a weak level.

“It’s clear that business sentiment is not a tailwind for the economy at present, but we remain optimistic that the boost being provided by a strong labour market, still-high commodity prices, a fiscal boost and now a significantly lower NZD will keep things ticking along,” Zollner said.

Turning to the detail:

·A net 3% of firms are expecting to reduce investment - but that is an improvement from the more than -9% net figure in the last survey.

·Employment intentions remain subdued, up 1 point to a net 0% of firms expecting to lift employment.

·Profit expectations fell 2 points to -15%. Profit expectations in the agriculture sector have dropped sharply in the past two months despite the weaker NZD; this is now the weakest sector at -54% (down 23 points). The services sector remains the least pessimistic about profit, at a net -4%.

·A net 31% of businesses expect it to be tougher to get credit, up 2.

·Firms’ pricing intentions lifted 2 points to +32%, the highest level since early-2014. This likely reflects rising costs such as wages, transport, and imported goods. Inflation expectations lifted 0.1%pts to 2.2%.

·Construction intentions dropped sharply. Residential construction intentions dropped 19 points to +5%, while commercial intentions fell 20 points to -24%. Canterbury is the particularly weak on both fronts, while Wellington is the strongest main centre but is trending down.

“The Reserve Bank argued in the August Monetary Policy Statement that the economy needs to run above-trend in order to get CPI inflation sustainably back to target. We therefore continue to believe that while the impacts of higher wage growth, higher oil prices, and the weaker currency certainly mean there’s no hurry, it remains the case that an eventual OCR cut is more likely than a hike,” Zollner said.

32 Comments

".. an eventual OCR cut is more likely than a hike..". Sharon is probably right. But that will just confirm the deflationary environment that has taken a stranglehold on our and other similar economies. Inflation, if it is the desired outcome, is not created by...dropping prices, and the foundation cost in all goods and services is...the cost of money.

I agree with you that its not a pleasing prospect, although expected, but id note that while the cost of money is the basis for the price of goods, its inverse.

"ANZ Chief Economist says next official interest rate move is more likely to be a cut than a hike"

Nic Johnson, this is contradictory to your prediction of interest rate hikes in 2019. I wonder who is more credible, the Chief Economist of a very large bank, or a conspiratorial keyboard warrior?

I think what Nic Johnson refers to is if the Australian owned banks come under financial trouble in Australia, they may hike interest rates over here to keep afloat. This could happen despite a cut in the OCR.

His prediction was for the OCR. Start rising in 2019 ("to hold up a heavily sold NZ dollar"), then up to 2.5% in 2020 and a whopping 3.5% in 2021.

https://www.interest.co.nz/property/95733/housing-sales-should-be-last-…

It is indeed BLSH

Unlike Sharon, I don't need a lower cash rate to preserve my margins and assist in the creation of more debt to households. ANZ and the other banks however really do need it, because they are approaching the turn in the curve where credit growth slows and households start de-leveraging. If i worked for one of the Aussie banks I'd be screaming for a cut in the cash rate too, but its not going to happen.

Where does your intense distrust of experts come from? It's a common theme in your comments.

BLSH

There's a difference between someone being an expert and someone being an expert with a slightly vested interest or need to influence for personal/company benefit. What else can she do? She can't say in public, 'We really need a cut in the cash rate because our creation of new debt is being hammered by the turn in the housing market, even though we've lowered rates only the existing mortgages are taking us up so that's going to reduce our margins next year unless the RBNZ helps us out' - so instead she makes a self serving prediction as guidance about what the bank would like to happen which is magnified with a prophecy of business doom. It's not her fault, her employer would not let her do anything else. It's not distrust, it's just not being naïve and there is a big difference between the two. Watch the link in my post above and it'll help you to understand why this is happening now.

Isn’t the NZ reserve bank often out of step with others like it ?

We are high they are low & vice versa it is a silly situation

Deflation definitely is the coming financial big wave with ripples already seen in parts of the e Con o my

Just awaiting the big sharemarket crash when overpriced 75K pickup trucks here will be returned to dealers & we can score a bargain Not all bad deflation if you have cash

I see no reason why the Reserve Bank wouldn't be accommodative to the expectations of the merchant banks. And if that doesn't work, we can always bail them out again. Or they can bail in our deposits. Too Big To Fail Right? That banker is just calling it as it is. Keep the sharks well fed and they won't go for your leg. But they have the legislative authority to take your limbs if need be.

..it was not the expert bank economists who picked the gfc now was it?

Rastus

I always read & listen to T Alexander he knows his stuff

Then do the opposite

Worked really well for be

This is very true, we use to have a nick name for him "Mr Back to Front". Nice guy though, gives funny speeches.

Agreed. Everyone has a vested interest. Were lucky enough to get to vote every three years for our vested interest . Most of NZ voted for the property speculation to be stopped, hence the legislation that is arriving at the moment.

The theories that conspiratorial doom and gloomers come up with on this site are hilarious.

BLSH, if you stop and thought for a moment, further rate cuts are a sign of deteriorating economic conditions. It should not be taken for granted that banks will pass it on. It's imperative the current high level of domestic sourced bank deposits remains. These deposits cannot be taken for granted in volatile times. I think your house price recovery in 2021 is looking like an even bigger fantasy than it already was (don't you think?)

Retired Pop

I sure hope you’re right about deteriorating house prices but I fear it will be stubborn Auckland

I’d like a piece of my favourite beach there but alas those lower prices have yet to eventuate

It’s not like I haven’t put in the work writing negative blog posts & predicting house price decline

An honest and reflective comment NL

The chief economist at ANZ is right. RBNZ should absolutely cut interest rates instead of the government looking to solve systemic problems facing businesses.

Cutting interest rates are 100% effective, just look at Europe, Japan, Denmark etc. where a generous QE programme (back-door QE in Denmark) and negative interest rates have delivered enviable economic growth for the better part of a decade. I wonder how much worse could these national economies get if they were to wind up QE and hike interest rates over the next few years.

Japan? Enviable growth? Are...are you sure?

Sense the sarcasm!

More like severely aging population of Japan Italy & especially aging ========CHINA

Japan does have enviable growths...and the biggest of today's was hearing about two large New Zealand entitlement indiviuals from Pollyticks giving them a mere 240000 dollars for a Day Trip.

Must have made Japan's day......but not ours......

Stupidity comes in Big Packages.....balancing Japan's Budget is not our responsibility....we have better use for the money, like Health and other basic needs.....

I am sick of wastrels....in Parliar-ment....who think it is their National skimming scam work to not use a Simple Radio Speaker.........to listen to a simple Rugby Match..for one simple Day.

Fat Chance things will ever change for the better, in this Country... Health Wise and otherwise, when we have Example of this magnitude......Staring us down, so they do not lose Face. Biggest losers in this Country...and we employ em......Unfortunately.

There are other examples of waste....that will fill a rift.....but dang it.....what a pair.

Probably why ANZ makes such a profit...whose credit cards didthey use???.

For the RBNZ to cut rates as its next move wold be a very unorthodox move given we are not exactly in the doldrums just yet and It would reduce the wriggle room in the case of a financial event.

I think they are more likely to sit on the rate and change the LVRs.

I actually think the RBNZs mention of a rates cut is a bluff to push mortgage rate competitiveness between the banks whilst not entirely selling out the NZD. meaning it is easier for those with high debt to get in a better position before the next hike.

But that's just my opinion and I'm no expert either

If the reserve bank were clever they’d keep the OCR right where it is.

Fix government business policy The level of bureaucracy is appalling to have to deal with

NZ has one advantage apart from scenery the world loves ( I have to hear it all the time here )

That is it is such a tiny economy it can turn on a dime to change direction & that’s a big advantage

Has the country got its countrywide fast internet all finished yet ?

Are they trading in French lessons for Python coding yet in NZ High Skools ?

Imagine if every kid in NZ learnt to code

That’s a policy Labour Go Do it

"If the reserve bank were clever they’d keep the OCR right where it is."

https://www.rbnz.govt.nz/news/2018/09/ocr-unchanged-at-1-75-percent

"Has the country got its ohnny Key Policy plank fast internet all finished yet ?"

bwhahahaha. No. At least a year away from being done here in Mt Roskill.

If every kid learnt to code it would make New Zealand an outstanding country that other countries would look up to. The same as when Japan was at their apparent peak at the end of the 80's/early 90's and every blue collar worker knew algebra. Something like that is too inspired for New Zealand politicians to do.

It will interesting to see if we start QE at some point and go negative interest rates.

Like negative interest achieves anything

Look at Japan

You never heard of carry trade ?

They’ll be carrying truckloads of kiwii dollars out of the country if you adopt negative interest my friend

We don't need the private sector to build! Phil's got this under control boys!

I knew this would happen. As soon as the Govt began subsidising developers into the Kiwibuild programme it meant non-Kiwibuild developers would struggle. FHB are now queued up to buy their "cheap" Kiwibuild house, so where is demand going to come from for non-Kiwibuild developments of the same standard but with higher prices? Developers will either need to slash their costs/profits to become cheaper than Kiwibuild homes, or start building for the high end, upgrader market - and if that's not possible, then they will not build at all.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.