By Roger J Kerr

It is instructive for future US dollar foreign exchange rate movements that retail sales, manufacturing and industrial production data on the US economy were all weaker than expected last week - but the US dollar was not sold lower on this negative news.

In fact, the American currency made gains to below $1.1200 against the Euro.

To be fair, US inflation data for August was somewhat higher than expected with annual core CPI now running at +2.3%; encouraging news for US dollar bulls who say the Federal Reserve should be increasing their interest rates sooner rather than later.

Despite the forward pricing for a Fed hike this Thursday falling to almost zero, the US dollar has not weakened.

On the contrary, the USD has strengthened on the back of the higher prospect of US interest rate increases in December after the elections.

The long awaited strengthening of the US dollar this year may finally be arriving in the last quarter.

Assuming that Fed Chair Janet Yellen delivers positive rhetoric for a December hike in the post meeting press conference this Thursday, the forward guidance signals should be sufficient to push the US dollar to below $1.1000 against the Euro. Lower oil prices, risk-off mode in global sharemarkets and potential for a weaker Yen on Bank of Japan monetary policy changes later in the week all point to US dollar gains as well.

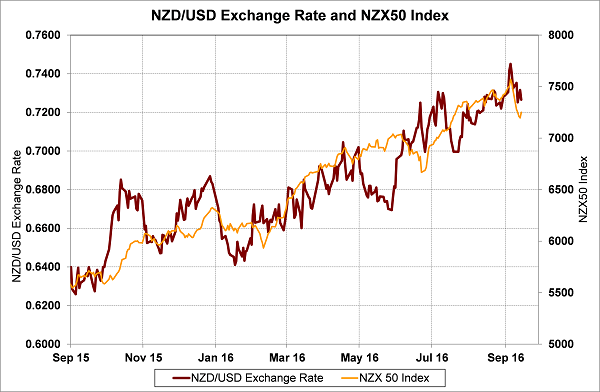

The New Zealand dollar commences this week trading nearer to the bottom end of the 0.7200 to 0.7480 range it has been in since mid-August.

Continuing USD gains on global forex markets should pressure the NZD/USD rate lower in the short-term.

NZ GDP growth data for the June quarter released last week was expected to be another positive for the Kiwi dollar. However, the 0.90% increase was at the bottom-end of market expectations and the NZ dollar lost ground rather than being turbo-boosted up to 0.7500 as some had been anticipating.

In many respects the strength of the NZ dollar is fully justified with strong growth above 3.00% and inflation less than 1.00%, thus the economic metrics are very positive.

However, there is major hitch with the higher currency value maintaining inflation below the required 1% to 3% band for two years now and the tradable part of inflation (imported consumer goods) being below 0% since 2012.

The Policy Targets Agreement (“PTA”) between the RBNZ and the Minister of Finance mentions that annual inflation may be outside the target band “temporarily” provided the RBNZ outline the measures they are taking to address the breach.

There is no question that the RBNZ themselves are interpreting “temporary” very liberally nowadays - as two years’ of breach in their eyes is nothing when looking at 20 and 30 year economic timeframes and cycles.

I am not so sure the Minister of Finance and the Board of the RBNZ would interpret the PTA as being that flexible and at some point the Governor needs to be accountable for allowing inflation to be so low for so long.

The RBNZ have had ample opportunity to be more aggressive with interest rate cuts this year to push the NZ dollar lower to get inflation up and have not taken them (despite my rants!) In adopting the slow and measured approach over the last six months they have compounded the problem on themselves.

What is also hard to understand is why the RBNZ now think they can only cut the OCR on full Monetary Policy Statement dates where they provide a full economic review/outlook and not on the OCR review dates in between. Why even have the OCR review dates if changes are never going to occur on these occasions?

The dairy GDT auction this week will be another small increase in commodity prices and thus be mildly positive for the Kiwi dollar. However, I expect the stronger US dollar ahead and after the Fed’s statement on Thursday morning and thus a NZD/USD rate moving below 0.7200. The RBNZ OCR review later on Thursday morning at 9am is looking like a non-event with predictable words from Governor Wheeler.

Looks like offshore portfolio investors in the NZ sharemarket have been selling out of late and taking their sizeable profits this year from both the equities capital gains and NZD gains against the USD.

Ahead of US interest rate increases in December and NZ interest rate decreases in November, the time has come to bank those profits before they are eroded away.

The herd is starting to push the Kiwi dollar exit gate and the strainer post holding the gate may not be strong enough!

Daily exchange rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

1 Comments

Its crazy, with almost zero interest rates , we are stumbling around unmapped territory, and we don't know where we are or where we are going

With QE there has to be some kind of endgame because we cannot have one of the 4 factors of production , in this case money, having zero value .

If the Fed increases rates , there should be a stock-market rout , and all asset prices that have been inflated with cheap money, should deflate .

I say should , but we know we are in unmapped territory , so who knows where things are going to end up

Its not leaving a good feeling for a happily -ever -after story .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.