This Top 5, the first for 2024, comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing a guest Top 5 yourself, contact gareth.vaughan@interest.co.nz.

https://t.co/OYGkDghuLu pic.twitter.com/3Yid6O7uDB

— Rod Emmerson (@rodemmerson) March 1, 2024

1) The financial market impacts of ANZ NZ's outlier, and ultimately wrong, OCR call.

A month ago speculation was mounting over what the Reserve Bank would do in its first Official Cash Rate (OCR) review of 2024. It was a long three months between the final 2023 review on November 29, a hawkish hold at 5.50%, and this year's first one on February 28. The consensus among observers was that another hold was on the cards.

Then on February 9 economists at the country's biggest bank, ANZ New Zealand, threw a cat amongst the pigeons.

An email from ANZ NZ's Chief Economist Sharon Zollner that hit the interest.co.nz inboxes at 12:53pm that Friday, certainly caught our attention. In it Zollner explained ANZ NZ's economists were now forecasting 25 basis points OCR increases on both February 28, and again at the Reserve Bank's next review on April 10.

This came after ANZ NZ's economists had said as recently as January 18 they expected "a steady sequence" of OCR cuts from August, taking the OCR to 3.5% over 12 months.

Between January 18 and February 9 there had been a hawkish speech from Reserve Bank Chief Economist Paul Conway, resilient labour market data, and the December quarter Consumers Price Index showing inflation at 4.7%, whilst trending down, still above the Reserve Bank's 1% to 3% target.

The ANZ economists' call for OCR hikes gained significant media and financial markets attention in the lead up to February 28. The Reserve Bank, of course, ultimately delivered a dovish hold. Zollner took it on the chin, acknowledging in ANZ's post OCR note; "We got this one totally wrong."

Bloomberg reported on February 27 that 22 of 24 economists it had surveyed predicted an OCR hold, with just ANZ and TD Securities, a Canadian investment bank with no physical presence in NZ, forecasting an increase to 5.75%.

Zollner and her team certainly aren't the first to get an OCR call wrong. In May of last year, for example, Westpac NZ's economists predicted an OCR peak of 6% by August last year. And we won't go into predictions from the real estate sector, those of us in the media or keyboard warriors.

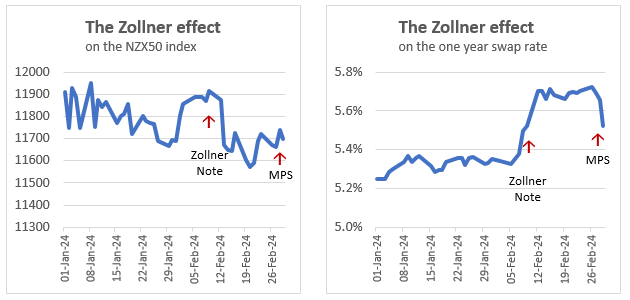

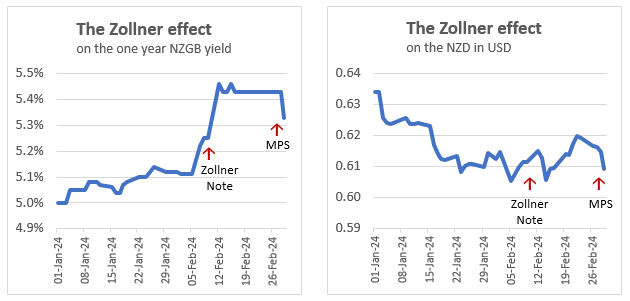

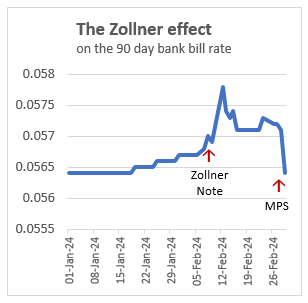

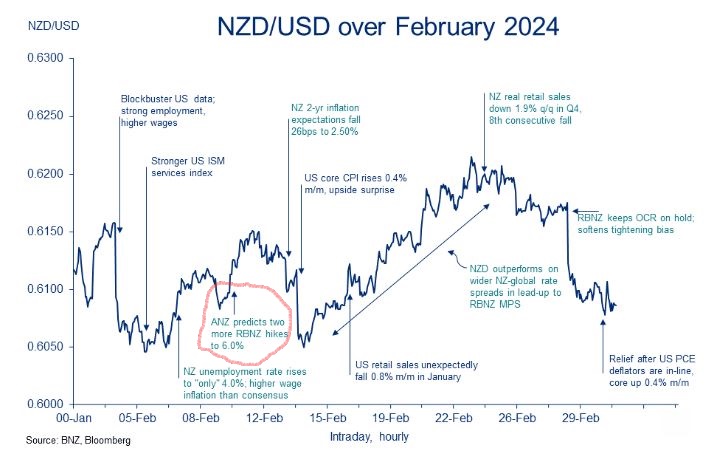

It is interesting, however, to look at the market impact the ANZ/Zollner outlier forecast had. This piqued my interest, so I spoke to a couple of market participants, who will remain anonymous, and asked David Chaston to make some charts.

Here's what market participant 1 said;

Fair to say that the ANZ call did disrupt the market, both interest rates and the NZ dollar. Basically, the call lifted NZ-global rate spreads and was responsible for a period of NZ dollar outperformance. This was during a period of a light global calendar. US CPI, US retail sales were market movers but it is unusual for domestic forces to “take over” from global forces, particularly regards the NZ dollar. Anecdotally, we heard of some business decisions/lending stalling as they awaited the RBNZ’s decision. Thus, the erroneous call was clearly responsible for some market volatility over the past few weeks and likely had some temporary economic impact as well.

And here's market participant 2;

Her change of call to a hike was a factor in pushing the market higher, no question. And that's provable even just by looking at charts of price action in the weeks before and the weeks afterwards. There was a clear spike up on the day that she published her hike forecast. Prior to that there was a little bit of an undercurrent of nervousness about how hawkish the Reserve Bank was building in the markets anyway. The Conway speech was probably the first thing that really got it going.

I also asked Zollner what ANZ observed following the Feb 9 call, in terms of financial markets impact, and feedback from ANZ clients and customers, and what her sense was of how much impact the call for two OCR hikes had.

She said;

What people do with information from our team that is discussed through the media is up to them and we don’t monitor that.

Below are David's charts.

And here's a BNZ chart.

2) How the $30 trillion quantitative easing experiment reshaped our world.

It may have taken the Covid-19 pandemic for NZ's Reserve Bank to embark on quantitative easing (QE) through its Large Scale Asset Purchase programme, but it was a tool used by other central banks for years before that.

In The QE theory of everything, a fascinating article for The New Statesman, Will Dunn traces QE's roots, and makes the case that;

For the past 15 years, every major development in our economy and the cultural superstructure that rests upon it - the explosive growth of social media and Big Tech, the property boom, the gig economy, Elon Musk, cryptocurrencies, fake news, overpriced coffee, Brexit, woke capitalism, Donald Trump and yes, perhaps even Prince Harry and Meghan Markle - can be related to the huge sums of new money that have disrupted every major economy.

Labeling QE "the defining idea of our time," Dunn traces it back to a September 1995 article in the Nihon Keizai Shimbun by Richard Werner, then a young German economist, suggesting a cure for Japan's economic malaise.

In his article, Werner suggested a cure: a new kind of credit creation by the central bank. He called it ryōteki kinyū kanwa, or “quantitative monetary easing”.

In the decades that followed, Werner has watched as different versions of his idea have been applied around the world: in Japan in 2001, then in the US and Europe in 2008, and at a still greater scale in 2020. The total credit created by central banks through quantitative easing, or QE, is now more than $30trn.

I was a young Assistant English Teacher in Japan at the time of Werner's article, on the Japan Exchange and Teaching (JET) Programme. It's fair to say Werner's article passed me by at the time, and Japan's economy seemed pretty good to me!

Dunn's article makes the case that, rather than trickle down, the wealth created by QE stayed where it was, boosting asset prices in shares, bonds, property, art and fine wine, but it wasn't very successful at boosting economic activity.

As QE drove inequality, it polarised politics. Across Europe, America and Britain, swathes of society were not in a position to profit from the wealth boom when it arrived, and were “left behind” – not by globalisation, but by finance. But because it’s hard to get angry at complex central bank policies, the people in these areas got angry at something more familiar: other people.

3) Foxes in charge of the hen house?

In January the Commerce Commission said it had received an application from Payments NZ seeking authorisation to work with others to facilitate a more well-utilised, secure and innovative open banking framework.

Formed in 2010 by the banking industry with the Reserve Bank's support, Payments NZ governs NZ's core payment systems and works with the industry leading open banking and the future direction of payments. Its shareholders are ANZ, ASB, BNZ, Citibank, HSBC, Kiwibank, TSB and Westpac.

Last year Payments NZ announced ANZ, ASB, BNZ and Westpac must be technically and operationally ready to allow their customers to share financial data with third parties via open banking this year, with Kiwibank to follow in 2026. We are well behind other countries, including Australia and the UK on open banking, albeit not everyone believes open banking's the silver bullet to improve banking competition.

The Commerce Commission released a statement of preliminary issues on Payments NZ's application last month, and called for submissions. It's due to make a decision by July 10.

It'd be fair to say there's some opposition.

David Tyrer, Chief Operating Officer at mortgage broker and peer-to-peer lender Squirrel, highlights concerns in a submission posted on LinkedIn.

Broadly speaking, Squirrel agrees that the services Payments NZ has suggested need to be put in place to support a cohesive Open Banking regime. However we strongly differ in our view as to how these services should be governed and driven.

Payments NZ is owned by banks. It would be unconscionable to effectively appoint the banks to have influence over:

a) Who needs to provide services;

b) Who can use the services provisioned under open banking; and

c) When those services need to be available.

To Squirrel’s knowledge, no other jurisdiction globally has supported an industry body owned by the incumbents to make decisions on Open Banking. Allowing Payments NZ to govern open banking could potentially lead to:

- Slower provision of services;

- A reduced number of services being available;

- Third-party users being excluded on grounds that may not be in the best interest of NZ;

- A focus on payment related activities at the expense of thinking about the financial services that can support a more competitive industry and enhanced outcomes for NZ Inc; and

- The continued balance of power resting with the incumbents.

Ultimately Tyrer wants a regulatory solution.

Squirrel believes the Commerce Commission should reject the bid by Payments NZ in favour of a Government-led alternative. The objectives of this organisation should be to move at a speed that’s deemed safe and delivers services beneficial to NZ INC in promoting innovation and competition, ultimately, across industries.

There's more information and other submissions here. Watch this space.

4) Tackling the scourge of surcharging.

This Australian Broadcasting Corporation (ABC) story has detail on just how expensive card surcharging is for Aussie consumers, the likes of which I don't believe we yet have publicly available in New Zealand. A surcharge is an extra fee or charge added to the cost of a good or service, beyond the initially quoted price.

Analysis based on data from the RBA [Reserve Bank of Australia] reveals Australians are losing $960.26 million a year in surcharges when they pay with their cards instead of using cash.

Unlike in the UK and the European Union where card surcharges are banned, retailers in Australia are allowed to recoup their payment costs through surcharging their customers, as long as they are not making a profit out of it.

The previous Labour government passed the Retail Payment System Act in 2022, introducing regulation of merchant service fees charged by card issuing banks to their business customers. The Act also gave the Commerce Commission powers to issue merchant surcharging standards "to ensure surcharges for payment services such as credit cards or contactless payments reflect the actual cost of providing that payment option."

Last August the Commerce Commission said whilst it may regulate payment surcharges charged by merchants to consumers for certain payment services such as credit card or contactless debit card payments, it was;

yet to determine whether regulation in this area is necessary and are currently using an engagement strategy that allows us to learn whilst encouraging payment service providers and merchants to do the right thing by their respective customers.

In Australia, as the ABC article notes, most debit cards are dual-network cards. That means they have a Visa or Mastercard logo on the front and an eftpos logo on the back. This RBA initiative is known as least-cost routing, or LCR. It means payments terminals in businesses will automatically default to the lowest-cost card network to process their debit transactions.

If you insert or swipe your card on the terminal, you can choose the cheaper eftpos network. If you tap your card, the transaction will be automatically routed to the more expensive Mastercard or Visa network.

In theory, it should put downward pressure on payment costs, and the flow-on effect should be smaller surcharges for consumers.

But, so far, only 64 per cent of business terminals are enabled with LCR. The RBA has said the take-up is "disappointingly" slow.

Payment analysts say the hold-up lies with the banks because they make less money out of least-cost routing.

RBA governor Michele Bullock has threatened to mandate LCR by the middle of the year if the industry doesn't meet the target of 80 per cent by then.

Concluding a series of articles on NZ retail payments systems in 2020, I suggested the NZ Government should look closely at Australia's then fledgling least-cost routing system. I hope they are.

5) Living in the most polluted place on earth.

This Bloomberg article, about the Vaal Triangle near the South African city of Johannesburg, encapsulates the challenge between reducing pollution emissions and employing people.

From the highway into Vanderbijlpark, you can see the heavy veil of smoke that cloaks Africa’s biggest steel mill. To the southeast, near the town of Vereeniging, the Lethabo coal power plant, whose name means “happiness,” joylessly belches out ash and toxic sulfur dioxide. Further south, outside a petrochemicals plant in Sasolburg, an adjacent neighborhood regularly reeks of rotten eggs from hydrogen sulfide in the air.

The plants offer steady work for residents at a time when one in three South Africans are unemployed, yet they’re also pumping out harmful emissions at levels so high that Vereeniging is by some measures the most polluted city in the world. The toxins are causing hundreds of premature deaths every year across the Vaal Triangle, and respiratory disease for many of those still breathing. The situation is a stark reminder of the toll the world’s dependency on steel, oil and coal is having on human health – and the difficulty a green transition faces if it costs the livelihood of the workers who depend on old economy jobs.

And it features a familiar story of kicking the can down the road.

The problem has been on the South African government’s radar for decades. In the mid-2000s, it designated the region as the Vaal Triangle Airshed Priority Area, the first zone in which it would make a concerted effort to lower air pollution. Since then the air quality has hardly improved as companies have applied for, and received, exemptions to emission limits and dysfunctional municipalities have stopped collecting waste, forcing residents to burn it. Traffic on the highways crisscrossing the region only adds to the pollution.

However, change may be afoot.

Beyond the government’s new emissions limits next year, there’s growing international pressure for companies across South Africa to clean up their operations. Some of the world’s richest nations are funding a $9.3 billion plan to help South Africa transition away from coal. The Lethabo plant, which is due to start closing down in 2036, may follow the path of older Eskom facilities that are slated for conversion to renewable energy and other activities through the incentive program.

23 Comments

1. Has anyone asked whether ANZ remitted significant NZD to its Australian parent immediately after Zollner spiked the NZD/AUD 0.75cents?

Not just that.

Pretty much every financial transaction, from mortgage re-fixing to current and future hedging arrangements. All need to identified and accumulated to establish whether this was an out-and-out example of market manipulation. I'd even go so far to suggest their email and messaging systems backups should be seized so the chances of any tampering are eliminated.

Zollner is a wolf in sheep's clothing.

[ Cheap insult not necessary. Ed ]

Apt though

Given his flawed approach, he may not be able to afford expensive insults

:)

Oh haha, you're cheap and nasty

What I found most disturbing in the ANZ's OCR hike prediction were the extremely dubious, and almost childlike, reasons given to justify it. Almost as if a CEO had directed the ANZ economists to issue it and suggested the reasons. Much more investigation is required.

ComCom has much work to do.

ComCom has much work to do.

Why bother? we all know the inevitable result.

Argumentum ad odium

Et tu, brute?

We do, because it has nothing to do with them

A recently departed CEO perhaps?

"You might very well think that; I couldn't possibly comment"

On "4. Tackling the scourge of surcharging." ... Many of these costs are either 'one-off change' costs and/or banking networks seeking to recover costs (i.e. making extra profits) from past investments. As well as elements of monopolies doing what monopolies do.

The consumer shouldn't have the burden of checking which is the cheapest method of payment at the time of purchase. The world is complex enough and such approaches simply prey on the ignorant and/or time poor and/or "stressed out and can't be bothered". Further, it encourages the use use of cash which has its own inefficiencies.

Perhaps the threat of nationalizing this nationally important utility - for that is what it is - should be used to force the players to stop gouging both the merchants and the consumers?

Nothing to do with Jessica Mutch McKay becoming ANZs head of corporate responsibility and govt liaison?Its dodgy af.

boosting asset prices in shares, bonds, property, art and fine wine, but it wasn't very successful at boosting economic activity.

the QE seems believe money can be created out of thin air and no price to pay. but when you hold that newly printed paper into a real store, exchange that into real goods and services, are they getting paid or not? is there a price to pay somewhere by somebody or not?

the QE seems believe money can be created out of thin air and no price to pay.

QE is not money printing though. Using the case of Japan, even though they've been on a massive QE program forever and a day, Japanese people and firms have not been lining up at banks to spend like drunken sailors. There's a difference between base and broad money.

Over the past 20 years on a per capita basis and adjusting for population changes, the annualized rates of broad money supply increase per capita:

- United States: 6.2%

- Euro Area: 5.5%

- Japan: 2.9%

Labeling QE "the defining idea of our time," Dunn traces it back to a September 1995 article in the Nihon Keizai Shimbun by Richard Werner, then a young German economist, suggesting a cure for Japan's economic malaise.

- The mighty Audaxes has often quoted and linked to Werner. His Quantity Theory of Money should be read and understood.

- Japanese translation of Werner's 'Princes of the Yen' has been widely read by Japanese. He is respected in Japan - that's a lofty achievement for a foreigner. He also speaks Japanese well enough to be interviewed in TV. Smart cookie indeed.

- Werner was invited into the WEF many years in a role similar to Cindy and Trudeau - young global leader. Big difference here is that Werner is not shallow and empty. He questioned and criticized an ECB bigwig and fell out of favor very quickly. WEF ignored him and never invited him back.

QE does not create any new money or assets, only government deficits or new bank lending can do that. QE only exchanges one asset for another.

Economist Silvana Tenreyro of the Bank Of England explains this here, https://www.bankofengland.co.uk/-/media/boe/files/speech/2023/april/qua…

Economist Paul Sheard of Standard And Poor's also states the same here, https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

Nice try - interesting speech, but wrong.

The problem is that they're trying to paper over the difference between required (by the temporary System they/we set up) economic 'growth', and the (physically-inevitable) tailing-off of real growth. It was a can-kick; an attempt to keep the show on the road, by people with a vested interest in the show retaining perceived credibility.

What it did, was to legitimize more debt per time, which continued the illusion of 'growth' - unsurprisingly resulting in more that $1 in debt for every $1 of GDP - itself a far-from-adequate measure anyway. As such, it has widened the already-irreconcilable gap between 'proxy-held expectation', and 'potentially consumable'. In terms of time, it was printing money, or was intended to have the same effect.

They all should have done first-year physics - heck, even 6th Form would have done.

Actually, Audaxes just put up a very appropriate link:

https://www.nakedcapitalism.com/2016/03/michael-hudson-on-debt-deflatio…

'This decline was offset by the Federal Reserve and the European Central Bank trying to re-inflate the Bubble Economy by Quantitative Easing – providing reserves to the banks in exchange for their portfolio of mortgages and other loans. Otherwise, the banks would have had to sell these loans in “the market” at falling prices.'

'Economics is taught like English literature. Teachers explain the principle of “suspension of disbelief.” Readers of novels are supposed to accept the author’s characters and setting. In economics, students are told to accept just-pretend parallel universe assumptions, and then treat economic theory as a purely logical exercise, without any reference to the world.'

'Economic theory, like history, is written by the winners. In today’s world that means the financial sector. They depict banks as playing a productive role, as if loans are made to help borrowers earn the money to pay interest and still keep something for themselves. The pretense is that banks finance industrial capital formation, not asset stripping.

What else would you expect banks to promote? The classical distinction between productive and unproductive (that is, extractive) loans is not taught. The result has been to turn mainstream economics as a public-relations advertisement for the status quo, which meanwhile becomes more and more inequitable and polarizes the economy.'

Touche...

The financial sector today is decoupled from industrialization. Its main interface with industry is to provide credit to corporate raiders

Like our very own Graeme Hart, who profited massively from the sale of state assets 40 years ago (Government Printing Office) and recently helped bankroll the election of the Nat/Act. coalition. What public assets are left? Auckland Airport shares are about to be sold. Our remaining state-owned hydro-electricity assets are bound to be worth a pretty penny.

New book 'Silent Coup: How Corporations Overthrew Democracy' by journalists Claire Provost and Matt Kennard, goes further in describing the international structures and laws (ISDS) that cut off at the knees any attempt at economic reform.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.