Here are the key things you need to know before you leave work today (or if you work from home, before you shutdown your laptop).

MORTGAGE RATE CHANGES

Only the Police Credit Union raised rates today. All current mortgage rates are here. And note, you can compare mortgage offers with our new calculator that takes into account other costs and cashback incentives, here.

TERM DEPOSIT/SAVINGS RATE CHANGES

ANZ has changed its Serious Saver account by cutting its standard rate by -35 bps and increasing its bonus rate by +40 bps. That will get then you a potential 1.55% bonus saver rate. The Police Credit Union raised TD rates too. All updated term deposit rates less than 1 year are here, for 1-5 years, they are here.

UP IN FEBRUARY, BEFORE THE NEW UNCERTAINTY

There are signs of recovery in the residential construction sector in the latest (February) building consent numbers. They were up +11.7% from the same month a year ago. But retirement village unit numbers are still in the doldrums.

UNCERTAINTY BEFORE MARCH

In the commercial (non-res) sector, the annual volume of private sector consents slipped to a new 12-year low, while the corresponding figure for public sector consents reached a two-year high. (H/T Infometrics)

DEAD LAST

Each year CPA Australia survey small businesses across the Asia-Pacific region to benchmark performance on growth, technology, innovation and hiring. Their 2025-26 survey is out and the New Zealand results are sobering. For the second year running, NZ small businesses have ranked last out of 11 markets for growth.

TRACKING OUR FUEL SITUATION

MBIE is tracking the days of cover we have for some key fuels stocks. We will track that and update regularly here.

|

Stock, days cover

|

Number of ships | Petrol | Diesel | Jet fuel |

| In-country | 29.3 | 21.6 | 22.1 | |

| On water within EEZ (up to 2 days away) | 6 | 4.3 | 8.4 | 11.4 |

| On water outside EEZ (up to 3 weeks away) | 10 | 25.1 | 22.2 | 12.6 |

| Total NZ stock, March 29, 2029 | 58.7 | 52.2 | 46.2 | |

|

previously reported

|

Petrol | Diesel | Jet fuel | |

| In-country | 27.9 | 21.7 | 25.3 | |

| On water within EEZ (up to 2 days away) | 5 | 12.5 | 6.1 | 2.0 |

| On water outside EEZ (up to 3 weeks away) | 10 | 18.9 | 26.7 | 23.1 |

| Total NZ stock, March 25, 2026 | 59.3 | 54.5 | 50.4 | |

|

previously reported

|

Petrol | Diesel | Jet fuel | |

| In-country | 24.5 | 18.1 | 20.1 | |

| On water within EEZ (up to 2 days away) | 19.8 | 15.8 | 11.7 | |

| On water outside EEZ (up to 3 weeks away) | 4.3 | 12.5 | 21.6 | |

| Total NZ stock, March 22, 2026 | 48.7 | 46.4 | 53.4 |

DONE OUR QUIZ YET? NO? DO IT NOW

Our quiz has been updated for this week's edition. You can do it here. And a new one will be added every Monday.

MOMENTUM LOSS

Realestate.co.nz says the housing market lost momentum in March. The number of homes for sale hit an 11-year high in March even though new listings were flat.

NZX50 TURNS DOWN

As at 3pm, the overall NZX50 index is down -0.3% so far today. It is heading for a -0.5% weekly fall, and down -4.2% from six months ago. From a year ago it is still up a net +4.5%. Market heavyweight F&P Healthcare is down -0.9% so far today. Gentrack, Freightways, Serko and Air NZ lead today's gains, while a2 Milk, Infratil, Meridian and Tourism Holdings headline the declines.

FILLED UP

There is a lot of cash money out there looking for a risk-free home. Managers of the very large $850 mln LGFA bond issue have confirmed maximum uptake, and the yield will be 4.936% pa. They got offers in excess of $2.8 bln ! There is another $450 mln NZGB tender tomorrow, and normally they don't get the level of demand we saw for the LGFA one. But you never know. Local governments and Nicola Willis can raise the funds needed today easily. They just need the future you to pay it back

ARE YOU A BANKING & FINANCE PROFESSIONAL?

You may wish to consider subscribing to our specialist daily newsletter. Details here.

STRONGER MILK FLOWS

Fonterra reports that their New Zealand milk collections for February were 143.2 million kgMS, +7.1% above February last season. Season-to-date collections are 1,218.3 million kgMS, +3.1% above last season. Meanwhile in Australia, they say milk collections there for February were 8.4 million kgMS, +3.4% above February last season. Season-to-date collections are 78.4 million kgMS, also +3.4% above last season.

WATER QUALITY POOR & NOT GETTING BETTER

Probably related to the previous item, StatsNZ says our river and lake water quality remains poor. Phosphorus levels showed improving trends but Escherichia coli (E. coli) trends worsened at many river sites, while overall lake health remained poor. (You can be sure Federated Farmers will ignore this update and resist any measures to improve things.)

QUALITY QUESTIONS HERE TOO

It is not only water quality we should be concerned about. If you are interested in who is behind some of our biggest commercial media brands, you should check this out.

A SUDDEN TURN SOUTH

In Australia, the main business trade association said their Industry Index fell 19.9 points in March to -23.6, the steepest monthly decline since the initial pandemic phase of early 2020. Industrial activity, employment, new orders and sales indicators all fell markedly in response to the emerging energy crisis. Uncertainty was the main factor, with 30% reporting volatility in fuel prices, freight and/or supply arrangements because of the energy crisis. More than a quarter (26%) of businesses said rising costs were a major pressure – in fuel, freight, raw materials, resins, plastics and packaging.

BIG UPSWING

There was a surge in residential consents issued in Australia in February, with 19,022 issued. That is the most for any month since mid-2021. Of note is the rise in Victoria where over 6000 consents were issued. That compares to NSW's 4332 and Queensland's 3890 in February. It is notable that states with relatively lower new-build consenting are those with higher rises in house prices.

'NOT AFFECTING US'

Interestingly, the Bank of Japan's Tankan survey of businesses there for Q1-2026 shows little negative impact from the current geopolitical situation. Those forms surveyed remain quite upbeat.

SWAP RATES DROP

Wholesale swap rates are likely to be sharply lower today on global trend as markets bet on the chances of Trump cutting & running. Keep an eye on our chart below which will record the final positions closer to 5pm. The 90 day bank bill rate was unchanged at 2.54% on Tuesday. Today, the Australian 10 year bond yield is down -8 bps at 4.93%. The China 10 year bond rate is unchanged at 1.81%. The Japanese 10 year bond is down -1 bp at 2.34% today. The NZ Government 10 year bond rate is now at 4.66, down -12 bps from this time yesterday. The RBNZ data is now 'prior day' with the Tuesday rate down -5 bps at 4.73%. The UST 10yr yield is down -3 bps from this time yesterday at 4.30%.

EQUITIES ALL RISE, EXCEPT IN NZ

The local equity market has fallen -0.4% in Wednesday trade so far. But the ASX200 is up +1.6% in afternoon trade. Tokyo has opened on Wednesday up +3.8% in its opening trade. Hong Kong is up +1.9% and Shanghai is up +1.1%. Singapore is up +1.6%. Wall Street ended its Tuesday trade on a strong note with the S&P500 up +2.9% on the rumors Trump is about to chicken out in his Persian Gulf foray.

OIL UP, MOSTLY IN THE US

American oil prices have risen +US$1.50 with the WTI benchmark now at just on US$103/bbl, while the international Brent price is up +US$1 at US$106/bbl. This differential is skinny, back to pandemic levels.

CARBON MARKET QUIET

There have been a few smaller transactions so far today on the secondary market, and the price is holding at $41.50/NZU. See our daily chart tracker of the NZU price for carbon, courtesy of emsTradepoint.

GOLD RISES AGAIN

In early Asian trade, gold has risen another +US$83/oz and now up at US$4693/oz. Silver is up +US$2.50 at just under US$75/oz.

NZD HANGING IN THERE, WEAKER AGAINST THE AUD

The Kiwi dollar is little-changed from this time yesterday against the USD, up +10 bps at just on 57.4 USc. Against the Aussie we are down -40 bps at 83.0 AUc. Against the euro we are down -25 bps at 49.7 euro cents. This all means the TWI-5 is still just over 61.2 and little-changed from yesterday..

BITCOIN HOLDS

The bitcoin price is now at US$67,730 and down -0.4% from this morning's open. Volatility has remained modest at +/- just under 2.0%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

34 Comments

The Limits to the Energy Transition

Acknowledgement to PDK posting the link this morning.

Managing the transition as noted on the white paper is the obvious sensible, rational action. Options identified to aid the transition are also sensible and rational.

But the potential societal upheaval required to manage transition is the greatest challenge, in my opinion.

Policy settings in NZ continue to drive rural population decline and urban drift. Whereas rural drift is a more logical outcome of the transition. That would mean a massive hit to residential property values in major urban centres. I cannot see that being enabled within current political dynamics.

The following article in Stuff this morning sharpened focus on societal implications for transition.

This illustrates changes in expectations of society over the last 50 years. Essentially a much more common expectation now, is that when I have a self defined urgent need, I'm entitled to immediate resolution of that need and an external agent is responsible to deliver that within the time frame I define as acceptable. Personally, I thought it was a pretty stupid article for Stuf to publish but that is beside the point.

Along with expectations is the elevation of comparison with others, that at one level is a natural human condition. But becomes dangerous when it fails to recognise prevailing conditions in the local situation. In the ambulance case, I would challenge anyone to identify where such an outcome would not have occurred in any other country. Triage assessment is, ultimately, inherently subjective, and ambulance services are a limited resource. Thus, leading to a prioritisation process informed by other objective data built over time, but only able to apply limited or no objective data about the current enquiry.

The expectations permeate thoroughly through society. And they cannot be sustained in and following the transition.

Comparisons feed expectations.

Amongst the most unpalatable outcomes of the transition I can visualise is in health care. The resources necessary to maintain or extend current expectations will not exist. That portends the human biological species will contend with the same overpopulation challenges all other biological organism function within – population collapse to a new level sustainable by available resources.

Not a pretty situation.

Woke energy policy working it's magic.

https://www.farmersweekly.co.nz/news/kaitaia-timber-mills-may-close-wit…

Tell the truth, Profile.

There's nothing woke there - that was is a case of 'the markets' (the mantra chanted by your tribe) in operation, and with no accounting for societal good. I'll re-phrase that - a track record of not only disregarding societal good, but commandeering it to profit therefrom.

I did note your need to deflect the LouB post, though. Predictable.

Yes, let us bask in the societal good of shutting down a woke ETS compliant hydro powered sawmill and replaced with a Chinese coal powered sawmill. The societal good of coal sourced methanol and aluminium coming our way soon.

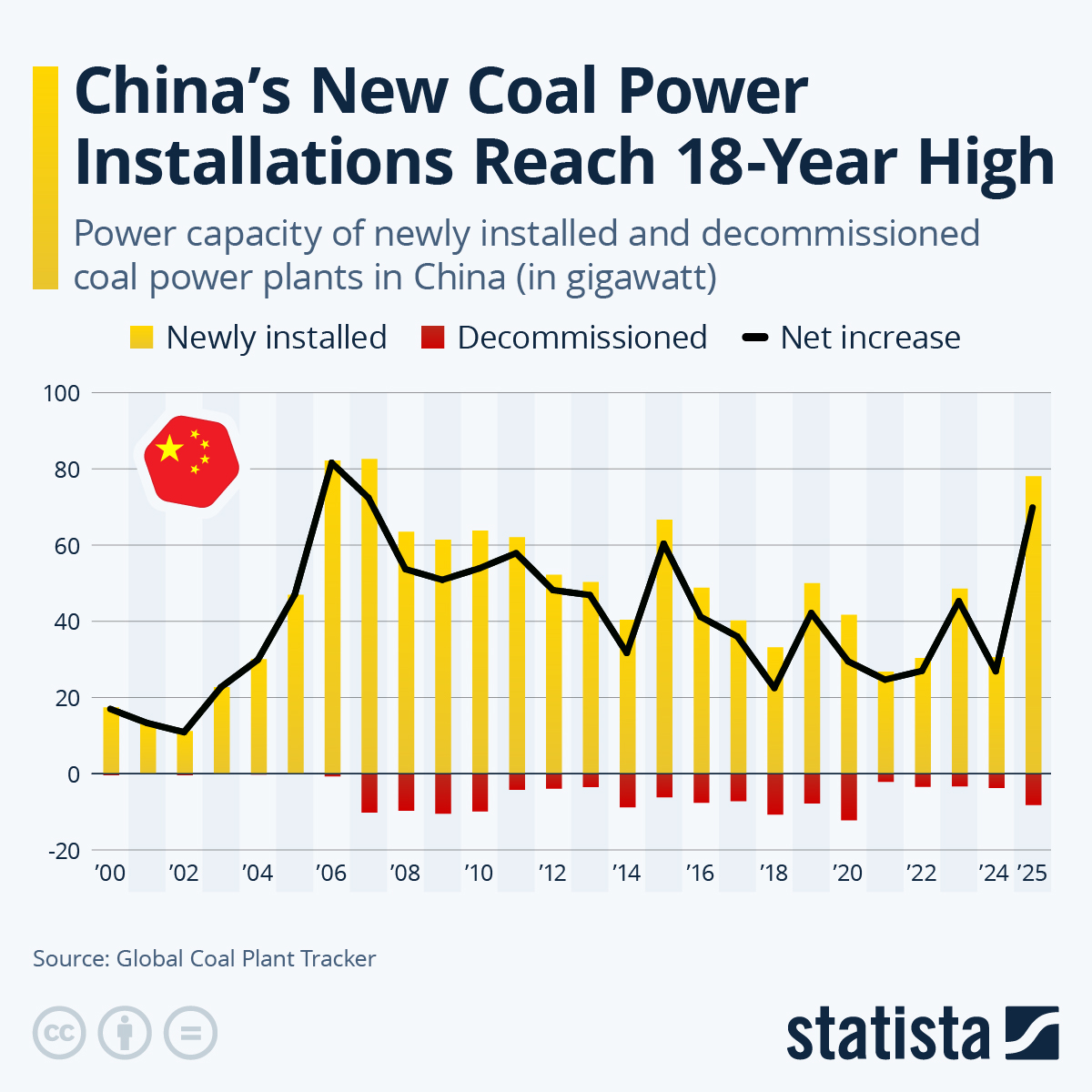

https://cdn.statcdn.com/Infographic/images/normal/36007.jpeg

{kind=link}

Nah Profile. It's the old non woke working its thing.

In early Asian trade, gold has risen another +US$83/oz and now up at US$4693/oz. Silver is up +US$2.50 at just under US$75/oz.

Silver has been looking strong near term - up 7% past 5 days and still up 95% in past 12 months.

Gold miners as well (via proxy GDX) - up 10% in past 5 days and 82% past 12 months.

It's only the past 1 month when you hear "glad I didn't buy that crap" at the BBQs. People only started taking notice at the top.

Markets are so fickle. Do they think the Iranians are going to stop the war if Trump heads back with his military to the USA with his tail between his legs? The Iranians need to make this as painful as possible to the West to act as a deterrent for future attacks. Israel aren't going to stop the bombing. The strait will remain under Iranian control.

Weak Iran has run rings around Trump and the powerful USA.

They are fighting a war that works for what they have and does not follow the USA rules. Asymmetric. Classic.

ie: Hormuz. Shelling the USA bases in the Arab States. (who is going to want host those bases in the future. Dispersed Iranian command and supplies. (Meanwhile Israel is running out of protection supplies) Trump is getting the blame for the energy crisis, after Greenland and now this, it will be a problem for the USA for the next 50 years.

After the Iranians escaped USA control in 1979? the USA would have done best to just get over it. And especially stayed in the nuclear control agreement that Trump ditched in his first term. Two big mistakes.

Except there was nothing to stop Iran from being non compliant with the agreement. Just look at it now, what would anyone do about if they did transgress. Neighbouring Arabic nations can’t or won’t even intervene to prevent Iran from choking off their major sea supply route. Iran has through its structure and disciplines proven to itself that it is virtually untouchable and they will be able to fall back on Chinese and Russian assistance to rebuild.

Canada getting very serious about propping up their Ponzi. Mark Carney has not announced a brand‑new set of incentives over the past week - he is rolling out a joint federal–Ontario package that layers on top of Ontario’s tax break and municipal fee cuts.

Today, the Prime Minister, Mark Carney, alongside the Premier of Ontario, Doug Ford, announced a new partnership between Canada and Ontario to build more affordable homes, infrastructure, and transit. This partnership will reduce taxes and fees for a home in Ontario by up to $200,000.

The federal government and Ontario will cost-match a total of $8.8 billion over 10 years, focused on housing-enabling infrastructure projects. This funding will support the reduction of municipal development charges by up to 50%. These reductions will be in place for three years and target municipalities covering 80% of the province’s population.

Tax relief for homebuyers: Building on the elimination of the GST for first-time homebuyers last year, through this partnership, the full 13% of the HST will be removed for new homes in Ontario valued up to $1 million, saving buyers up to $130,000 on the purchase of their home.

https://www.pm.gc.ca/en/news/news-releases/2026/03/30/prime-minister-ca…

For a moment there i thought you said that Mark Carney rolled a joint....

I was just going to post the same thing.... maybe he has a prescription...

With all of the riparian planting and fencing off of streams duck populations have blown out - animals that carry a higher load of E. coli than cows and defecate directly in to the water.

Riparian planting would help phosphorus load and decrease of 59 percent on monitored river sites between 2005 and 2024 demonstrates this. Create stream side duck habitat and get increased E. coli.

But hey, let's have needless crack at fed farmers.

"Southern farmers struggling with an explosion in the mallard duck population can seek approval for a cull or to disperse the birds, says Fish & Game New Zealand."

https://www.farmersweekly.co.nz/news/fish-game-outlines-farmers-duck-op…

https://www.stats.govt.nz/news/mixed-trends-in-river-and-lake-water-qua…

Don’t holiday down there, Trev. Not in season at least.

The point is that it is BS.

As is usual from that source, hereabouts.

The reality is that farming has become too intensive. That required some sort of mitigation - riparian planting was seen as the least-bad option. But it still tells us they're over-using the land - and I'll tell you their way of farming is totally dependent on the resource we're fighting over, globally.

But as with all spin, a narrow window is chosen - cherry-picked - in this case a cost to farmers re ducks. As always, the big picture is ignored.

"But it still tells us they're over-using the land "

Overusing/misusing...Canterbury a fine example.

Mmm, so the effluent amount produced from 100 dairy cows is about the same as about 2500 ducks. Don't know if I've every seen a flock that size. That'd be some easy picking from the maemae. Got a machine gun in there?

100 cows?

There are nearly 700,000 cattle in Southland.

Was that stat cherry-picked too?

No, was just doing it with an easy multiple. But average herd is around 450. So there would have to be a nearby flock of ducks around 11,250 in number to produce that amount of BS :)

we should kill them and make peking duck.... pancakes spring onions who doesnt like that

The problem with that reckon is the ducks produce an order of magnitude higher E. coli per day so for your 450 cows you would only need 77 ducks to produce the same amount of E. coli. Those ducks are defecating directly in to the water, whereas the cows are fenced off with a riparian strip. Perhaps that explains when P is down 58% but E. coli is up. Riparian planting is a two edged sword - trout out, ducks and deer in.

"Each duck produces 1.17 x 1010E. coli bacteria per day compared to a dairy cow, which produces roughly 2.01 x 109 E. coli per day."

https://www.nzherald.co.nz/the-country/news/drone-controversy-highlight…

It'll never fly, Profile.

Your problem is not an uncommon one; you start by assuming a narrative - yours - is the best, and the thing to save/champion.

The problem comes when it was based on BS - which not just yours, but the narrative of the whole first world, in the big picture, is.

Just remember, the ducks and deer and cows were introduced by?

Us. Just, some of us have said 'mea culpa' and have gotten on with making things better.

That time PDK learned Pukeko produce copious amounts E. coli while trying to push his narrative.

"two sites were responsible for most of the breaches.

These were urban areas in New Plymouth frequented by resident wild birds, the committee was told.

A third site, Waimoku Stream at Oakura Beach, where samples are taken every three years, also showed high levels of the bacteria.

All three sites showed an increasing trend of pollution from birds over 24 years of sample testing, the committee heard."

https://www.stuff.co.nz/environment/300287156/ducks-and-seagulls-habitu…

Not just ducks, Canadian geese (plague proportions South Island high country) and swans (Wairau lagoon, Marlborough) apparently over 3,000 there. I frequent the former and saw first hand the latter, last weekend. And they're bigger than a duck. Also, most of the time live on the water, unlike livestock.

If you provide breeding /feeding environments for pasture feeding fowl what would you expect to happen?

More on the Allbirds collapse. WSJ suggests in reality nobody gives a rats about woke things like sustainability. But in reality, this factor comes way down the batting order behind factors like style, price and comfort.

I agree. Particularly in tough times, people are not going to shell out for emotional gratification. People say they care about sustainability, but you have to accept that there's a fair amount of virtue signaling going on.

https://www.wsj.com/business/retail/allbirds-the-tech-bro-favorite-once…

More on Allbirds

1. New tech didn't change unit economics, you still had to get stuff to people.

2. Just because a VC bloke in San Ffrancisco thinks a $2000 bike is cheap, doesn't mean anyone in the normal world wants to spend much, all these brands were aimed at wealthy people that didn't exist in the numbers expected.

3. Flawed exit expectations, none of these brands wanted to IPO, they all wanted to grow fast and big enough to irritate a massive company into buying them, which was always risky.

4. They forgot to try to build a mass market brand. The main learning from this is even absolutely bananas profound technology like the internet, doesn't change many fundamental laws of the world, like shipping, returns, advertising costs, human nature. And more that that, what goes up fast, can come down fast, Allbirds had one mad successful shoe but fashion is almost always a fad, unless you do everything right, and for that you need category experts, not software thinkers.

Their 2025-26 survey is out and the New Zealand results are sobering. For the second year running, NZ small businesses have ranked last out of 11 markets for growth.

Is this the true barometer for the state of our economy?

many NZ small business sell to the housing market... enough said

Good observation.

Treasury Wine Estates in Aussie looks to be in trouble. Crazy how they ended up with these issues.

A controversial $1.3 billion acquisition of a luxury vineyard at the top of a mountain between Los Angeles and the Napa Valley in California is threatening to upend Australian winemaking giant Treasury Wine Estates.

Shares in the ASX-listed winemaker behind the iconic Penfolds Grange, Wolf Blass, Lindeman’s, and Wynns brands have sunk 63 per cent over the past year, as hedge funds lift bets its $1.9 billion debt pile spells more trouble ahead.

https://thenightly.com.au/business/treasury-wines-faces-elevated-risk-o…

I am hearing wine industry in NZ F ed until 2028, too much grapes not enough people buying, due to health and other option, like green shoots.

Boomers cutting back (anecdotal), and no sustained demand in the following generations. Still.....that grange is a stunning drop.

Look on the shelves in your Supermarket, the bottom ones, where the cheap stuff is (as retirees can't reach it). It's mostly Australian crap and when people are struggling, they'll buy the cheap stuff. Also, every dog has its day: houses, gold, silver, wine, oil, etc. Some have more than one 'day'. Dairy is having its day right now, long may it last, but it won't last forever...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.