By Mark Brown*

- Central banks are focused on bringing down inflation

- The Reserve Bank of New Zealand amongst the earliest to hike rates and now others are moving rapidly

- Sharp interest rate rises are now largely baked into financial markets

- Lowering inflation is the best outcome for businesses and ultimately households

- We think expectations of a cash rate of 4.6% by May 2023, is excessive although markets will continue to monitor inflation closely

Through the course of 2022, inflation across the world has continued to increase, and has been challenging a prior expectation amongst many central banks that this phenomenon would be transitory. The consequences of the Ukraine war, tight labour markets, ongoing supply chain issues and policy-stimulated consumer demand have all operated in sync. Central banks, after a phase of reticence, are concerned that the rise in core measures of inflation could filter through to higher long-term inflation expectations.

Choking off excessive demand now, and normalising monetary conditions, is likely to involve less pain than allowing inflation to rise further.

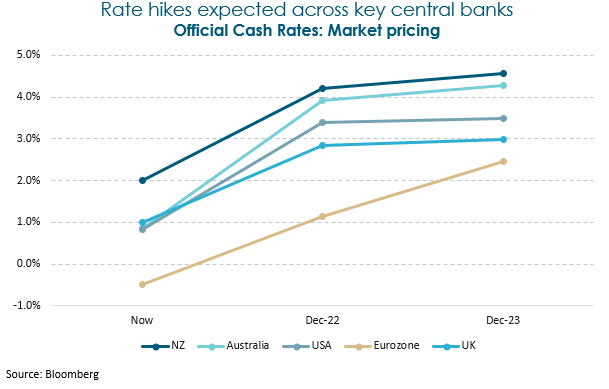

To the credit of the Reserve Bank of New Zealand (RBNZ), they were one of the earlier banks to recognise the danger of rising inflation expectations and started hiking the Official Cash Rate (OCR) last October. They now have the OCR at 2.0%, which is broadly at a level that they consider neutral. However neutral rates may not bring inflation back inside a 1% to 3% target range within an acceptable timeframe. Consequently, in their May Monetary Policy Statement the RBNZ projected that the OCR would need to rise to 3.8% by mid-2023, as they take a ‘resolute’ approach towards managing inflation expectations.

This week the US Federal Reserve hiked the Fed Funds Rate by 0.75% to 1.5% - 1.75% (the Fed sets a range for Fed Funds) as US inflation has continued to rise, with the latest data showing consumer prices rising by 8.6%. The path of US interest rates is a crucial factor influencing longer term global bond markets and as an anchor for equity valuations.

Markets globally are anticipating interest rate hikes across all major economies other than in Japan and China. In New Zealand, the local bond market priced in rate hikes earlier than elsewhere, which might imply more stability in New Zealand as other markets played catch up. However the New Zealand market continues to march interest rate expectations higher and, despite some pull back in recent trading sessions, the OCR is expected to reaching over 4.5% in May 2023. This is nearly 1% above the level the RBNZ projects. We think that the market is pessimistic in this projection.

Already households are feeling the brunt of the higher cost of living and also mortgages being refixed at higher interest rates. Consumer confidence is very weak and the housing market is slowing fairly quickly. In New Zealand and elsewhere, recession fears have grown.

For the Reserve Bank, a slower economy is exactly what is needed to diminish inflation pressure. With the labour market still very tight, the slowdown needs to be more than inconsequential. However no central bank wishes to crush their economy. Indeed, the Reserve Bank’s Policy Target Agreement includes an operational objective of avoiding “unnecessary instability in output, interest rates, and the exchange rate”1. At present, with markets pricing an OCR around 4.5%, that implies term mortgage rates well in excess of 6%. The economic risks seem skewed towards a sharp slowdown in New Zealand, perhaps one that is beyond the RBNZ’s appetite and mandate.

Consequently, we think market pricing has gone too far at present. At present, with inflation credibility at front of mind, the Reserve Bank is probably going to continue to emphasise their determination to subdue inflation pressures and signal rate hikes. However, as the year progresses and more hikes have occurred, we will be in an environment where monetary conditions have become tight and the economy is more clearly slowing. At this stage, communication can change and the Reserve Bank can slow down the hiking path and watch to see whether further hikes will be necessary.

In this scenario, bond markets can become more stable and eventually the valuation link to equity markets may see this first pillar put in place for valuations to stabilise across most asset classes.

With so many rate hikes currently priced in, we would need an even worse inflationary outlook to trigger a meaningful further rise in bond yields.

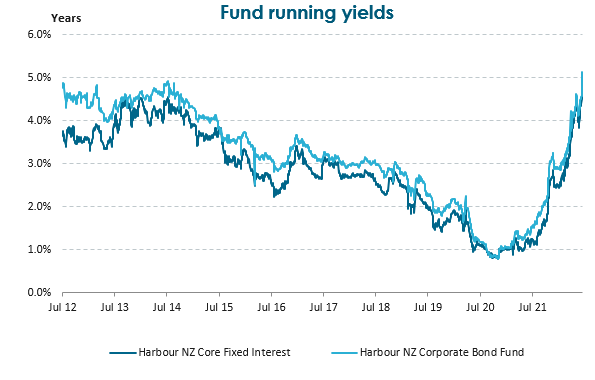

Supporting this argument is that longer term bond yields now reflect an ongoing environment of inflation sitting around the top of the Reserve Bank’s target range. At 4.25%, the New Zealand 10 year Government Stock yield points to continuing tight monetary policy as well as a term premium to compensate investors for some inflation uncertainty (for more, see The end of the “Great Moderation?” published last week). At around 5%, the running yield on Harbour’s New Zealand bond funds is also significantly higher than in recent years.

At some point we anticipate investors will cease looking in the rear vision mirror at one of the worst on record periods for fixed interest returns, and instead look forward. The positive impact of central banks getting serious about inflation is that savers tend to have greater confidence in the real returns they receive across all asset classes.

[1] Reserve Bank of New Zealand (Replacement of Remit for Monetary Policy Committee) Order 2021.

*Mark Brown is Director, Head of Fixed Income at Harbour Asset Management. This article is used with permission and was first published here.

This article does not constitute advice to any person.

66 Comments

Economy cycle has to play out its course - earlier the better.

Central bank with governments blessing went overboard, ignoring data and information that was screaming (as early as December 2020) about the approaching disaster, if rbnz not mend their ways but alas , fire brigade was bought only after the flame were at peak and not to save but to salvage.

This is central bank created situation - poor decision making by people in power that average person is facing today.

I think we’ve all had it too good if we think 7% inflation is a disaster. It may yet become one, but I think they will get inflation under control pretty quickly but it will cause a mild recession.

Actually far from being a disaster, I think high oil prices are exactly what the world needs being a climate emergency and all.

7% inflation, while retail deposit rates hover around 2-3%, is a disaster. Negative real interest rates are symptoms of very unnatural policy intervention that massively skews behaviour so people chase yield in dangerous and irresponsible ways.

Not only that, if we continued to measure inflation the same way we did In the 70’s, we would see current inflation is far closer to previous periods of out-of-control inflation than the official figures suggest

Just triple those numbers and it is what I lived through during the 70's in the UK. It was not a disaster - that would be an earthquake in Christchurch. It was bad but survivable. It left the elderly with savings poorer but not destitute; those with debts sometimes did quite well. A useful move towards equality at the same time as being a redistribution of wealth from the cautious to the feckless.

One advantage of high inflation is it allows bosses to effectively squeeze out poor employees without having the trauma of actually sacking them.

Negative real interest rates are good. The alternative leads to an aristocracy based on inherited wealth not talent.

It was not a disaster back then because real wages were increasing in line with inflation. There’s no indication this has or will happen in this cycle. Plus households are severely indepted compared to the 70s.

You have a point - many households are now and were in the 70s indebted. I don't think many in the UK were as 'severely' indebted as many in NZ today. The number sunk by debt in the next couple of years will be a smallish fraction of NZ households but it will be disaster for them. Repossessed homes, broken relationships, good people driven to emigration.

As the queen asked the UK prime minister after the GFC 2008 -"why didn't anyone predict this?"

How can people believe they will inflation under control with interest rate hikes when the issue is supply shortages? What interest rates hikes will do, is crush our debt-ridden economy.

The solution would be to let the supply driven inflation wave run its course. Monetary policy cannot address supply shortages without risking total collapse.

This is central bank created situation

Pretty hard to determine what situation we'd be facing instead.

"Not an overly mint one either way" is my approximation.

We'll get some inflation relief across the OECD in the last quarter of 2022 and first quarter of 2023. The principal reason for this is that inflation is calculated as a YoY increase and inflation really surged in those quarters of the prior year.

Another thing that will help inflation is rebalancing commodities between countries. Many emerging markets where subsidising fuel and food but ran out of financial headroom to continue to do that, the IMF won't lend without those subsidies being dropped typically. That will reduce overall demand across many developing countries. Finally higher food prices will entice subsistence farmers, who have a higher cost of production, to grow more by using fertilizers and pesticides.

Will Reserve Bank rate hikes help? They're probably a bit late now to help moderate demand. The damage has been done. The best we can hope is that they set rates appropriate to inflation going forwards and don't go off on any more wild goose chases ("transitory inflation").

"Bitcoin has now fallen more than 70pc since November"

Coming to every 'stimulated' asset price near us all.

Probably needs updated to 75pc* since this was published 2 hours ago...

Looks like the markets' canary has fallen off its perch and an angry crowd is about to jump up and down on the remains.

I wonder what will happen with BTC? Another upswing like every other time? Or is this time different, the time where people realise BTC has none of the required characteristics of money and is nothing but a speculative “asset”.

It has some characteristics of money, but none of the same security foundations. It would appear fiat backed by well meaning but incompetent public servants is still waaaaay better than the wild wild west. And there's the rub, to make a crypto people are confident in, you need the exact sort of centrality that most crypto's are trying to liberate their users from.

As I suggested, Bitcoin is the Canary in the proverbial financial/economic coal mine.

If I think that; and perhaps you and others, then so will those well-meaning public servants. And if the Plunge Protection Team doesn't have its fingers in the crypto space, for the very reason of their being, then I'd be surprised.

You can’t have a fixed supply and a stable value. The best case is that the value keeps increasing as people buy in, but that of course is deflation, why would you ever use such a currency to exchange goods. And realistically how many goods can you exchange with Bitcoin? I don’t use American Express because lots of places don’t accept it, and Bitcoin is a world away from being as useable as Amex.

people are worried about 7% yearly inflation with fiat, we’ll Bitcoin has had more than 15% just today!

$17,866 at the moment. Looks like this hedge against fiat currency and money printing is actually the exact opposite. I guess when interest rates go up, people want their money to be safely earning interest in a bank account, why risk it.

I think it could still recover, however there must be a "Panic" point where everyone but the largest holder bail out leaving just a few holding the bags. The panic point will be a psychological barrier, below $10K must be bad. If nothing else it may never recover fully, its been proven to be a very bad investment and protection against what happens with fiat, so what the point.

"Bitcoin has now fallen more than 70pc since November"

Coming to every 'stimulated' asset price near us all.

This is starting to look more like a reality and BTC is the canary in the coalmine. Probably good to pay attention to the housing mkt in NZ.

Step back and just breathe

Orr.

https://i.stuff.co.nz/business/128548000/adrian-orr-to-mps-on-inflation…

I think he’s largely correct although he should have mentioned the exchange rate. While he can’t influence the price of oil, he can influence the strength of the NZD and the price we ultimately pay at the pump.

interesting survey on that page where many more people were concerned about inflation than unemployment, I found that surprising, give me inflation any day. I guess maybe an older audience reading it.

Don't listen to a word that fool Orr says.

Anyone who listened to him 2, or 3, years ago and took on a big mortgage will be regretting it soon if they are not regretting it already.

Orr in August 2019, exhorting borrowers to borrow more, consumers to consume more:

"Orr was firmly of the view that low rates were the new norm ..."

"It’s easily within the realms of possibility that we might have to use negative interest rates,” Orr said."

"Speaking at a press conference, Orr said the MPC members “tossed and turned” but decided it was best to get ahead of the curve - make it much cheaper for households, businesses and the government to “wake up and go and spend” to prevent the economy nose-diving."

He sold an entire generation of borrowers up the river. Lifetime debt slaves. They won't be feeling "least regrets" for listening to that fool Orr. They will regret being fooled and trapped into a lifetime of debt by their own Reserve Bank.

https://www.interest.co.nz/bonds/101089/closer-look-regret-analysis-and…

.. the central bank gods had slain the dragon of inflation ... ... for 2 decades they partied hard in their Valhalla ... rejoicing in their status as conquerors , feted & revered ... immune to the traditional lore of financial wisdom , throwing more logs onto the fire , more & more ... yet that fire remained simmering embers ... this time is different ... the beast is dead ...

Except ... it's not... is it ...

.. the central bank gods had slain the dragon of inflation ... ... for 2 decades they partied hard in their Valhalla ... rejoicing in their status as conquerors , feted & revered ... immune to the traditional lore of financial wisdom , throwing more logs onto the fire , more & more ... yet that fire remained simmering embers ... this time is different ... the beast is dead ...

My new moniker for Adrian Orr is 'father of dragons' due to his spiritual revival based around Maori deities. No disrespect to Maori culture at all. That accusation might be levelled at the RBNZ.

Wow, discussing negative rates in 2019?

Incredible. So morally bereft. We really are fleecing the next generations at every point to keep asset prices high.

{kind=link}

Central banks, after a phase of reticence, are concerned that the rise in core measures of inflation could filter through to higher long-term inflation expectations.

Hmmmm... Stores Have Too Much Stuff. Here’s Where They’re Slashing Prices.

If the agressive Ocr hikes carry on they will not stop inflation, but destroy the economy and worsen the recession that already has begun.

exactly.

... not just Walmart & Macys in the US ... I do believe that our very own Briscoes might be having a sale today , too ...

Hmmmm... Stores Have Too Much Stuff. Here’s Where They’re Slashing Prices.

Yes Audaxes. I've already mentioned that this is also feeding into things like dairy prices across Asia for different reasions. For ex, butter is a discretionary item for Asian shoppers generally, but Fonterra's Anchor brand needs to put prices up. When the price goes up, less is moved from shelf to the shopper basket. Inventories mount. Stock needs to be moved so discounting is happening. My sources have shown me prices increase by 30% at the shelf within weeks, but then return to pre-Covid prices as it backfires miserably.

The online retailer (Overstock) will have a lot of goods to choose from as chains like Walmart and Target try to sell excess merchandise.

https://www.bloomberg.com/news/articles/2022-06-13/inventory-glut-at-wa…

"Controlling inflation is a key pillar to calm financial markets"

Above headline itself confirms that reserve bank goofed up in a Big way with their theory of transitory inflation even though data emerging as early as January 2021 / February 2021 suggested otherwise.

Can argue, what reserve bank did in March 2020 was need of that time but should remember that emergency measures like ventilator is for short term only to control in emergency, the damage as any excess will be more deadly and this is exactly what reserve banks have done :

"Oxygen toxicity is lung damage that happens from breathing in too much extra (supplemental) oxygen. It's also called oxygen poisoning. It can cause coughing and trouble breathing. In severe cases it can even cause death"

Finance $$$$$$$ is oxygen of any economy - unfortunately reserve bank governors being intoxicated by the power that comes with the posistion forgot the basic principal.

Agree, not just in NZ......but the whole Western World has been on the soothing, "it will be alright" ventilator, much too long, fooling ourselves that things were going fine.

Fun while it lasted, the party went on, the can was kicked - until our shoes now wore thin.

The ventilator was ramped up on tripple dose in 2020, overused to death. We have been hooked on some various form of false ventilator since the 2008 GFC.

We need the patient to be set free, painful as it is (in economics or real life) - to establish it own sustaining pulse or otherwise.

Ventilators are known to cause damage to the patient so the analogy is quite a good one. If you have been on a ventilator the recovery is likely to be longer.

(sorry Andrew, my habit of reading comments from bottom to top meant I read yours after writing this. Yes absolutely you are right!)

This sounds good in theory. In realty, raising interest rates will risk a deflationary collapse.

To get the patient back up on his feet, the only way would be to let the inflation wave run through the economy. You cannot print tons of money and issue stimulus and COVID relief to everyone, without also creating inflation.

Was reading Bernard Hickey .....has the median housing price in Auckland fallen by $360000, so 30% to start off isnot far away.

".....Meanwhile, house prices in Aotearoa-NZ fell again, including Auckland City’s median price falling $360,000 or 23% in six months,..."

I wouldn't be surprised if all the gains since the beginning of COVID are snuffed out. COVID should have reduced house prices, we were all braced for that at the time so further losses are not out of the question.

That would probably be the ideal scenario - get rid of all the Covid induced froth (which means only a small percentage will end up underwater), and then stagnate for a decade.

I wouldn't be surprised if all the gains since the beginning of COVID are snuffed out. COVID should have reduced house prices, we were all braced for that at the time so further losses are not out of the question.

House prices should overshoot dramatically in bubble markets like NZ. I'm talking about on the downside as well as the up. The up has just finished.

In monetary theory, for instance, that was the era of Milton Friedman in the 60s and 70s. He thought that when you create more money, it increases consumer prices. Well, I thought that obviously was not how things worked. When banks create money, they don’t lend for people for spending. About 80% of bank loans in America, as in England, are mortgage loans. They lend against property already in place. They also lend for corporate mergers and acquisitions, and by the 1980s for corporate takeovers.

The effect of this lending is to increase asset prices, not consumer prices. You could say that money creation actually lowers consumer prices, because 80% is to increase housing prices. Banks seek to increase their loan market by lending more and more against every kind of real estate, whether it’s residential or commercial property. They keep increasing the proportion of debt to overall real estate price. So by 2008 you could buy property with no money down at all, and take 100% mortgage, sometimes even 102 or 103% so that you would have enough money to pay the closing fees. The government did not limit the amount of money that a bank could lend against income. The proportion of income devoted to mortgage service that was federally guaranteed increased to 43%. Well, that’s a lot more than 25%. That’s 18% of personal income more in 2008 than in the 1960s – simply to pay mortgage interest in order to get a house. So I realised that this was deflationary. The more money you have to spend on mortgage interest to buy a house as land and real estate is financialized, the less you have left to spend on goods and services. This was one of the big problems that was slowing the economy down. Link

For under 30k NZD you can buy a whole Bitcoin and evolve that shrimp into a crab.

What was it that Warren Buffet said?

“fearful when others are greedy, and greedy when others are fearful.”

Not an easy decision though is it?

For the same amount of money you could buy a 10oz bar of gold from Perth Mint and have a REAL, tangible, asset that you can hold in your hand.

I will consider a bitcoin at maybe 3k USD.......but consider it much like a casino bet. 98% crash from its crazy top, seems like a fairly good discount?

BTC Not an actual investment, Not an alternative to cash, Not a store of value. Not just my view- proven by BTCs performance over the last year.

I will consider a bitcoin at maybe 3k USD.......but consider it much like a casino bet. 98% crash from its crazy top, seems like a fairly good discount?

Have the good fortune of previously buying BTC at those prices. Remember it was not so long ago. 2019. Remember, the price is still up 100% in P24M. Could be a long way to fall.

Too many people are trying to get rich through bitcoin rather than actually using it. It doesn't have a proper yield like shares or property or term deposits. Regulation is poor. It's complicated. It's extremely speculative and risky. I just watched this YouTube video about crypto. Well worth a watch as it is short and sensible:

Too many people are trying to get rich through bitcoin rather than actually using it. It doesn't have a proper yield like shares or property or term deposits. Regulation is poor. It's complicated. It's extremely speculative and risky. I just watched this YouTube video about crypto. Well worth a watch as it is short and sensible:

Cheers. An 11-min YT video is probably not going to be offer me much compared to 6 years of my own reading, research, and independent thinking. The current issues with digital assets are more related to leverage. Markets have to clean themselves and these markets do an admirable job of cleansing themselves.

Is BTC speculative and risky based on the past 10 years? Short term, yes. Long term, no. Past performance is no reflection of the future.

That video is more for the curious J.C. although time is dragging on a bit for bitcoin to become stable or at least useful. I guess in your view it was never meant to be stable. The El Salvador thing got people excited but to me it was more of a concern when a country like that embraced it. People need to use bitcoin not just hold onto it as a speculative asset. I have been waiting for bitcoin ATMs in NZ. As it doesn't generate an income and has no substance it is always going to be very risky. To borrow to buy bitcoin would be foolhardy whereas you could fairly sensibly borrow to buy other assets.

BTC is still in its infancy. Should expect the volatility. You don't need ATM machines for BTC.

Bill gates calls BTC/crypto/NFC 'greater fools theory' .. buffet wont touch it - and they is definitely more tech and finance savvy than me.

Dogecoin is suing elon musk for using their currency by inflating it with media releases to meet teslas own ends then dropping in it afterward so it bombed.

The nail in the coffin for digital currency for me was when rbnz started talking about havibg one here (rofl.... about as funny as their recent speech to the reserve banks overseas).

The only difference i see between NZ house market and bitcoin is that there is a tangible thing that keeps people dry and some land associated with an NZ house. So whilst Bitcoin will be worth less than the proverbial Tulip in due courae.. our Nz house prices will drop to what they are really worth vs housing in similar cities internationall y which hopefully will be approx median wage x 3/5 so maybe 200-350k ish in provinces (some extra leeway to account for the housing shortage) and maybe $450k in auckland if we are are lucky. Most houses here are not even particularly well built compared to those in other cities overseas.

I reckon that would be a very positive outcome. Much as i feel for the bank, investors, speculators and government who are loaded up with cheap debt and exposed to fast and large housing price changes - i prefer they all get wiped out and the leaders leave to do their stupid stuff overaeas - i just pray there something left to build a decent long term outlook for the next generation who had no part in this madness.

Ps. Anyone who didnt see out housing market crash to pre covid levels after the pandemic deserves what they get. Anyone that cant see a very high probability of at least another another 5 years worth of gains prior to that getting wiped by the ocr/inflation and increasing liklihood of black swan effects also deserves what happens. As for Bitcoin or money for bailouts... lol.

The nail in the coffin for digital currency for me was when rbnz started talking about havibg one here (rofl.... about as funny as their recent speech to the reserve banks overseas).

Tane Mahuta coin.

Bill gates calls BTC/crypto/NFC 'greater fools theory' .. buffet wont touch it - and they is definitely more tech and finance savvy than me.

Sure. Also, Microsoft and Berkshire Hathaway are great shares to own. Just because of what Bill Gates says shouldn't stop anyone from owning BTC. Do your own research and make your own decisions.

Definitely .. but i think for those that can afford 50% or 100% losses and understand tech, geopolitics and finance in some depth (bitcoins future is complex and largely a lottery). As per the people that bought houses at the end of last year and are currently sitting in ever decreasing value of their now largest investment.

Its just an opinion. As is my opinion house prices will crash to the levels indicated. But opinions based on facts and logic.

Time will tell.

Well there you go. Accept 100% risk as your parameter. If it doesn't work for your risk profile, don't go there. As for BTC futures, if you don't understand the risk, don't get involved.

People judging btc on its performance since November 🤷 the graph is always upwards to the right

But has gone up in general 100% per year since it’s infancy. Amazon had 90% draw downs in the early days. Fiat printing means the currency is constantly being debased

I always love this perspective. Look how "insert high value business with clear path to profit" is like "insert name of latest digital nothing".

You wouldn't want to miss out on the next big thing, would you?

RBNZ is just doing virtue-signaling, last .50 bps increase didn't trickle down to an increase of interest rate by banks, so have zero impact.

If the US goes for .75 raise with the same inflation as NZ (not counting on CPI by NZ stats), then what stops RBNZ to go for Bazooka of .75 or 1% increase, what they are waiting for?

Is managing inflation under their mandate or not?

Are they waiting for this inflation to turn up into hyperinflation because it is not transitory now or they are waiting for NZD to tank .50 against USD?

In 2000 was low 40 cents. I still recall the look of horror when quoting an import price on a small item from US to a customer. By the time we added freight and a margin it was pretty outrageous.

Are you sure ? The lowest I can remember doing quotes for was 0.54 to the NZD.

Reached .40 in April and July 2001.

Quick search and nice graphics shows you. I was surprised it was that low too.

The Flat Footed RBNZ......their boots just get longer and flatter.

They are so far behind the inflation fighting 8-ball, they are not even on the pool table ....... were last seen hiding behind the bar!!

It is impossible to 'manage inflation' after the money-printing frenzy of the last few years. It is simply impossible.

The only choice we now have in our debt-ridden economy is between a soft landing via inflation or a deflationary collapse. Interest rate increases, if aggressive or prolonged, will likely cause a deflationary collapse from which nobody will benefit. In particular, non-asset holders who are hoping for lower entry prices would not benefit from a deflationary collapse. This is because unemployment will be rampant and banks will not lend anymore once a deflationary collapse is on its way, so it becomes nearly impossible to enter the market.

Great comment about a deflationary collapse hurting everyone. Too many people think, "I don't own a house or shares or crypto etc… so I don't care, it won't affect me"

Newshub Nation

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.