The Bank for International Settlements (BIS), the central banks' bank, is putting the boot into the struggling cryptocurrency sector and making the case for central banks and central bank money to retain their pre-eminence in an evolving world.

In a chapter entitled The future monetary system in its annual economic report, the Basel, Switzerland-based BIS argues recent events reveal a gulf between a crypto vision of freedom and escaping the oversight of central banks and governments and reality. Reading the chapter, the German word "schadenfreude" springs to mind.

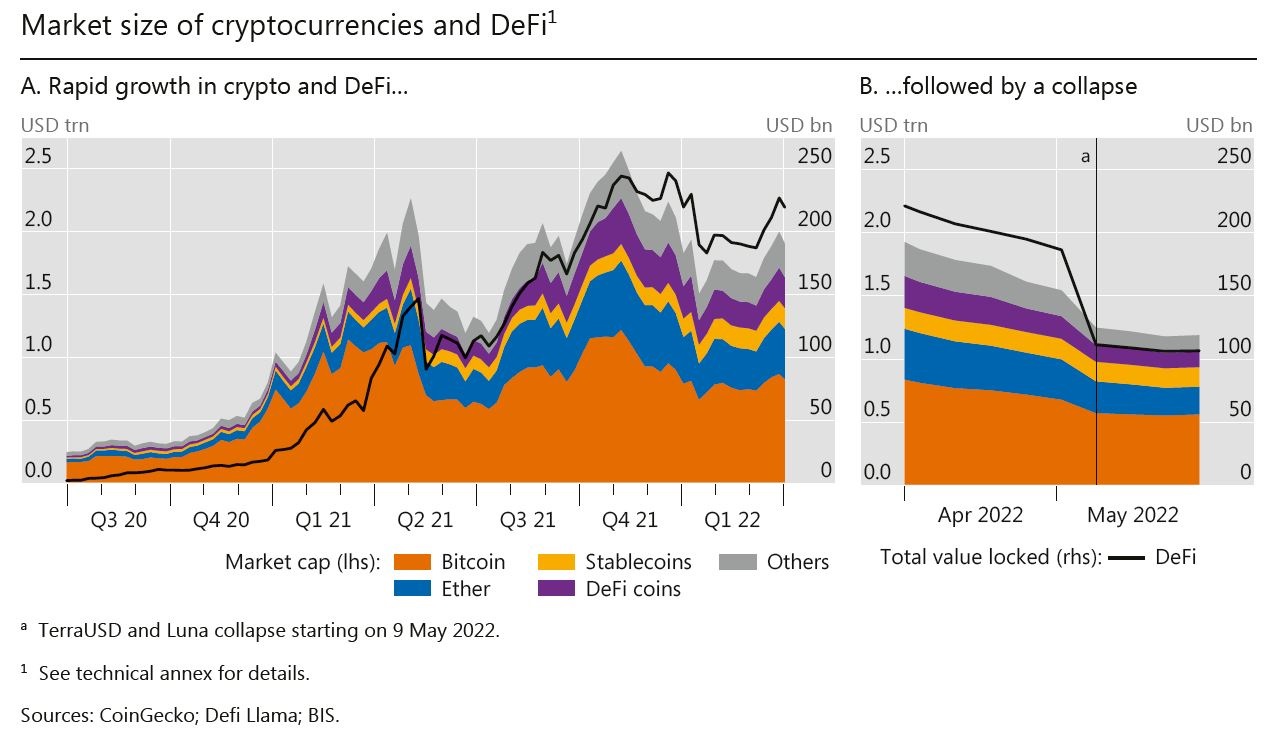

Coindesk reported this week that data from analytics firm Glassnode shows investors exited bitcoin positions worth a record US$7.3 billion over the past few days, amounting to the biggest US dollar denominated losses in the asset’s history. At the time of writing the bitcoin price was at US$19,897, way down from its record high north of US$68,000 last November.

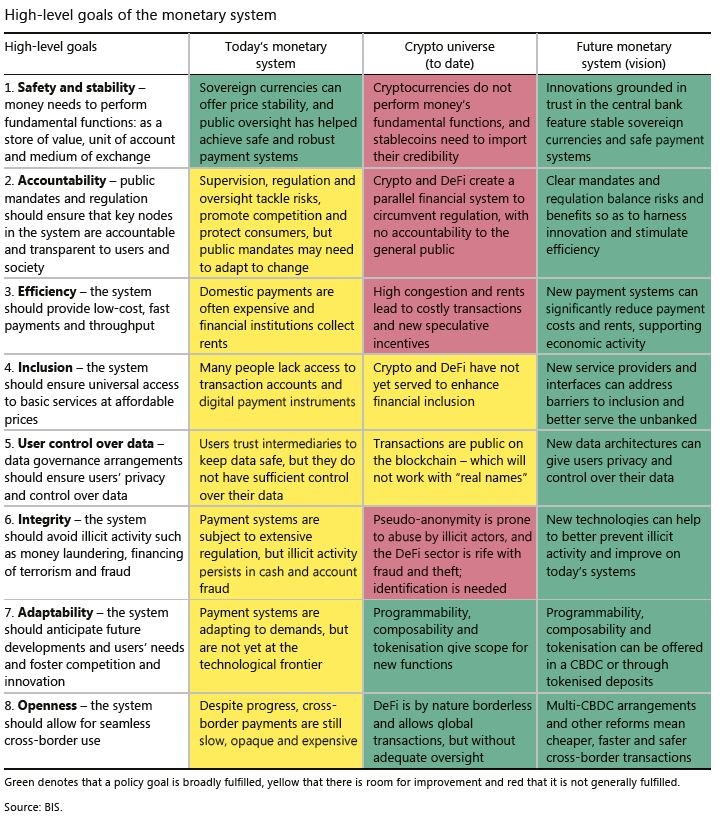

To ensure the safety and stability of the system, BIS argues money needs to fulfil three functions. These are; being a store of value, a unit of account and a medium of exchange. Cryptocurrencies, it argues, don't, and stablecoins need to import their credibility.

"The implosion of the TerraUSD stablecoin and the collapse of its twin coin Luna have underscored the weakness of a system that is sustained by selling coins for speculation. In addition, it is now becoming clear that crypto and DeFi [decentralised finance] have deeper structural limitations that prevent them from achieving the levels of efficiency, stability or integrity required for an adequate monetary system," BIS says.

"In particular, the crypto universe lacks a nominal anchor, which it tries to import, imperfectly, through stablecoins. It is also prone to fragmentation, and its applications cannot scale without compromising security, as shown by their congestion and exorbitant fees. Activity in this parallel system is, instead, sustained by the influx of speculative coin holders."

"Finally, there are serious concerns about the role of unregulated intermediaries in the system. As they are deep-seated, these structural shortcomings are unlikely to be amenable to technical fixes alone. This is because they reflect the inherent limitations of a decentralised system built on permissionless blockchains," says BIS.

Threat receding?

BIS has previously highlighted the threat to central banks from stablecoins and cryptocurrencies. Last September, for example, the head of the BIS Innovation Hub, Benoît Cœuré, urged central banks to crack the whip on the development of central bank digital currencies (CBDCs).

"We should roll up our sleeves and accelerate our work on the nitty-gritty of CBDC design. CBDCs will take years to be rolled out, while stablecoins and cryptoassets are already here. This makes it even more urgent to start," said Cœuré.

Reserve Bank of New Zealand (RBNZ) Director of Money and Cash Ian Woolford recently outlined the RBNZ's thinking on a CBDC in an interview for interest.co.nz's Of Interest Podcast. Among other things he said the RBNZ considering launching a CBDC is in part a defensive move to protect it and NZ's monetary sovereignty from private forms of digital currency and/or big technology firms.

A CBDC is the digital form of a country’s fiat currency. That means an RBNZ issued CBDC, like the physical NZ dollar, would be a liability of the RBNZ, backed essentially by trust in the Government and its institutions. By law the RBNZ is the sole supplier of NZ banknotes and coins, with this being a key raison d'être for the central bank.

According to think tank the Atlantic Council, 10 countries have launched a CBDC, 15 have pilots underway, and dozens of others are exploring the concept of a CBDC.

A tree metaphor

Not surprisingly BIS sees a future monetary system with central banks in the middle. In fact it says the metaphor for the future monetary system is a tree whose solid trunk is the central bank. From this base innovative private sector services can be securely rooted in the trust provided by central bank money, BIS argues.

BIS says fundamental roles of central banks include issuing central bank money to serve as the unit of account in the economy, being the trusted intermediary to debit the account of the ultimate payer and credit the account of the ultimate payee, support the smooth functioning of the payment system by providing sufficient liquidity for settlement, and safeguarding the integrity of the payment system through regulation, supervision and oversight.

BIS very much outlines a case of back to the future, with new capabilities of central bank money and innovative services built on top of them thrown in.

"The future monetary system builds on the tried and trusted division of roles between the central bank – which provides the foundations of the system – and private sector entities [such as financial institutions and fintechs] that conduct the customer-facing activities," says BIS.

BIS argues that new private applications won't be able to run on stablecoins, but they will be able to run via the likes of wholesale and retail CBDCs, and through retail fast payment systems that settle on the central bank balance sheet. It also highlights tokenisation, distributed ledger technology and application programming interfaces, or APIs. Decentralisation, BIS argues, can be achieved without the structural flaws of crypto.

"Because central banks are mandated to serve the public interest, they can design public infrastructures to support the monetary system’s high-level policy goals from the ground up," says BIS.

'Deep structural flaws'

Crypto, meanwhile, has "deep structural flaws" making it unsuitable as the basis for a monetary system that serves society, BIS argues. Stablecoins cop an ongoing serve.

"The prevalence of stablecoins, which attempt to peg their value to the US dollar or other conventional currencies, indicates the pervasive need in the crypto sector to piggyback on the credibility provided by the unit of account issued by the central bank. In this sense, stablecoins are the manifestation of crypto’s search for a nominal anchor. Stablecoins resemble the way that a currency peg is a nominal anchor for the value of a national currency against that of an international currency – but without the institutional arrangements, instruments, commitments and credibility of the central bank operating the peg."

"Providing the unit of account for the economy is the primary role of the central bank. The fact that stablecoins must import the credibility of central bank money is highly revealing of crypto’s structural shortcomings. That stablecoins are often less stable than their issuers claim shows that they are at best an imperfect substitute for sound sovereign currency," says BIS.

"Stablecoins also play a key role in facilitating transactions across the plethora of cryptocurrencies that have mushroomed in recent years. At the latest count there were over 10,000 coins on many different blockchains that competed for the attention of speculative buyers."

Nonetheless BIS acknowledges crypto offers "a glimpse of potentially useful features" that could boost the capabilities of the current monetary system.

"These stem from the capacity to combine transactions and to execute the automatic settlement of bundled transactions in a conditional manner, enabling greater functionality and speed. Thus, one question to consider is how the useful functionalities of crypto can be incorporated in a future monetary system that builds on central bank money."

BIS says that, as issuers of the settlement currency, central banks can support the tokenisation of regulated financial instruments such as retail deposits.

"Tokenised deposits are a digital representation of commercial bank deposits on a distributed ledger technology platform. They would represent a claim on the depositor’s commercial bank, just as a regular deposit does, and be convertible into central bank money, either cash or retail CBDC, at par value," says BIS.

"Depositors would be able to convert their deposits into and out of tokens, and to exchange them for goods, services or other assets. Tokenised deposits would also be protected by deposit insurance but, unlike traditional deposits, they would also be programmable and 'always on' (24/7), thus lending themselves to broader uses in retail payments – eg in autonomous ecosystems."

"This way, they could facilitate tokenisation of other financial assets, such as stocks or bonds. This functionality could allow for fractional ownership of assets and for the ability to exchange these on a 24/7 basis. Crucially, this could be done in a regulated system, with settlements in wholesale CBDC," BIS says.

A public-private partnership

Eyeing its own version of utopia, BIS talks of a public-private partnership to help make the monetary system more adaptable and open across borders, with central banks in the middle.

"A decade hence, users may take real-time, low-cost payments for granted, and payments across borders may be as seamless as the cross-border exchange they support. Consumer choice in financial services should be increased, and innovation will continue to push the frontiers of what is possible."

"In all of this, innovation must start from an understanding of the concrete needs of households and businesses in the real economy – and of the policy demands they put on a monetary system. While decentralised technologies such as distributed ledger technology offer many possibilities, users’ needs should stay at the forefront of private innovation, just as the public interest remains the lodestar for central banks," BIS says.

"In both the design of new infrastructures and in regulation, there is an ongoing need for global cooperation between central banks, and indeed a wide range of new stakeholders."

41 Comments

Watched an interview with a knowledgeable crypto trader.

Key points

Bitcoin will fall, stabilise and rise again, might hit $100,000 (in 2-3 years).

Support level of $30,000, broken recently, and possible next floor is $12,000.

Just now, price was $21,000, last weekend it dipped below $18,000.

And till today, no idea how to buy or sell Bitcoin.

Yes, all that I relate to is Bitcoin, not polkadot , tetra or luna ....and what else.

Tee, you also only refer to Bitcoins speculative aspect (how much is worth) and not of its intrinsic value (or lack thereof), which is this article's point.

Could you also ask him what's the median price of an auckland house in 3 years time, and the Telsa share price?

I have some important investment decisions to make and could do with the advice of some random guy on the internet that can predict the future.

Are knowledgeable Crypto traders just like knowledgeable central bankers? It's all fiat.

This “trust” in central banks that Carstens talks about is being torn to shreds by themselves in real-time. 40% increase in the M2 supply of the USD in the last two years? Who would trust that?

The hardest money will always win, and Bitcoin was engineered to be the hardest ever created. Traders and speculators control the exchange rate narrative in the short term, but savers will control the narrative in the long term.

If you use the words “Bitcoin” and “Crypto”interchangeably, it means you don’t understand either. -Michael Saylor

Crypto/Bitcoin/digital assets is sort of like Libertarianism. Central authorities are a joke? Here's the solution, no oversight at all, everything will just sort itself out.

Maybe if someone came up with a crypto that had a value of "the entire world", and dumped everyone's share directly into their wallets.

Fiat currencies have no value, they all inflate away to zero eventually. The hardest money was the US dollar before 1971, backed by gold and productivity. Once off the gold standard, speculation was the order of the day, fueled lately by zero interest rates and deficit spending.

US dollar hegemony is coming to an end, Putin wants rubles for Russia's oil, Gaddafi wanted gold and Hussein wanted Euro's (oops wrong choice). When all those 'Eurodollars' come flooding back to the US, Rory will be begging to get on the LIV tour.

A CBDC is one centralized ledger for all transactions and balances. Every payment to every other wallet is recorded and can be regulated. It's a different ballpark. If anything, a country with only a CBDC would create strong demand for non CBDC crypto.

Probably no coincidence that PRC is the earliest adopter of this.

this is probably true and in order for central banks and governments to have their control over you (we can all see this coming), then the next thing will be to outlaw all other cryptos.

Just think about it for a moment, its inevitable.

You know... that is technically pretty hard (somebody could say impossible, in a sense)

A new blockchain can be created in hours. By anybody.

Whose willing to risk the jail time?

Authoritarian countries like PRC regulate hard, but crypto still exists there.

US banned private ownership of gold in the past, so it is possible. But there will likely be jurisdictions that allow it as a point of difference or apathy. Then anyone with a cell phone can access it.

Also, probably only G20 size countries could develop their own quality CBDCs. Chains like Algorand and Cardano are already targeting developing countries to co develop their CBDCs. So would be hard for other countries to then ban those chains.

Central bank mafia don't like competition.

Creature of Jekyll Island.

Eschaton,

I tried reading it last year, but had to stop. Griffin may not have invented conspiracy theories but he certainly believed many of them.

Ultimately, without universal confidence in any coin/commodity/asset having modicum of tradeable/bartering value, then it's worthless.

Propaganda. BIS know where they can shove their central control and CBDCs.

A bit rich for Central Banks to be criticising anything. Yesterday I lamented Orr’s “least regrets” as incompetent and this morning Dalio’s Bridgewater notes that Central Banks should:

1. Use their powers to drive the markets and economy like a good driver drives a car—with gentle applications of the gas and brakes to produce steadiness rather than by hitting the gas hard and then hitting the brakes hard, leading to lurches forward and backward.

2. Keep debt assets and liabilities relatively stable and, most importantly, not allow them to get too large to manage well.

Dalio concluded that, by those 2 measures, Central Banks haven’t done well. I agree. And so people in glass houses shouldn’t throw stones.

One of the questions that has never really been answered for me - and that keeps me away from anything crypto as currency - is the enforceability of the contract.

Basically, the State's monopoly on legal force / compulsion (enforcement via courts, taxation, commerce legislation etc.) gives the reserve currency its value and trust.

I simply don't get how any cryptocurrency can hold intrinsic value without it, which keeps the whole proposition firmly speculative.

I guess you're referring to 'legal tender.' Of course, any CBDC may be legal tender. In the case of BTC and other digital assets, it should be noted that the legal process to make BTC legal tender has already started in a number of U.S. states. I would have mentioned El Salvador but that's like feeding trolls.

Japan is probably one of the more advanced countries for legalization of digital assets. There is a bit of confusion as many people thought digi assets were legal tender in Japan, but they're actually not. There's some nuance surrounding the relevant Bill. It's not illegal to use BTC for ex in a transaction and to exchange for goods and services, but the Bank of Japan will not recognize digital assets as money. So there's a huge grey area.

Because of some of the issues surrouding stablecoins as pointed out by the BIS, the BoJ has passed regulation related to who can issue stablecoins in an effort to rpotect onwers. https://www.ft.com/content/7f8130e9-abfa-407b-b04f-2f9f5e47d0df

"I guess you're referring to 'legal tender.'"

Principally yes; the "promise to pay".

Also though, the bundle of rights associated with tender, and what rights the state hold to influence its relative value via monetary / fiscal instruments (including taxation) and the enforceability of contracts and rights associated with holding or transacting that tender.

There's a whole bunch of stuff that Bitcoin and its ilk are essentially silent on (or rather, that legislation is silent on) which make non-RB crypto quite unattractive to be from a risk perspective.

Basically, I don't understand the use case for it that can't be made by existing legal tender.

Principally yes; the "promise to pay".

Fair question. For ex, I contract to mow your lawns for a year in exchange for BTC 0.1. We have a written agreement that states the terms of the contractual obligations. In Japan, you would likely be required to fork up for the service if you didn't want to pay.

Important to note that BTC is not a 'promise to pay' like fiat money issued from a bank as a debt obligation.

Rather than a formal contract (a 'this for that' consideration) I'm really thinking more the implicit contract that comes with tender, so 'enforceability' in a general sense by virtue of being issued by a CB.

i.e notwithstanding forgery, you know a dollar is a dollar and it's generally accepted to be worth something to yourself and your counterparty, and if they rip you off, there's a reasonable expectation that the State will take an interest. I'm not sure that the same 'duty of care' applies to non CB issued currency, whether it's crypto or any other form of token that *some* people decide have value.

i.e notwithstanding forgery, you know a dollar is a dollar and it's generally accepted to be worth something to yourself and your counterparty, and if they rip you off, there's a reasonable expectation that the State will take an interest. I'm not sure that the same 'duty of care' applies to non CB issued currency, whether it's crypto or any other form of token that *some* people decide have value.

Not sure why you would distrust the authenticity of a CBDC. As for "cryptocurrencies", if you're not sure what it is or how it works, there's a simple solution: don't accept it. Furthermore, there may be some future legal obligation for cryptos to be exchanged into CBDCs or authorized stablecoins (essentially a digital representation of fiat) for legal tender. A new Bill re stablecoins is being built around that premise in Japan now.

"Not sure why you would distrust the authenticity of a CBDC."

Sorry, I probably wasn't clear. I would trust CBDC, as much as I trust the value of any other CB issued token.

As per my comment above "There's a whole bunch of stuff that Bitcoin and its ilk are essentially silent on (or rather, that legislation is silent on) which make non-RB crypto quite unattractive to be from a risk perspective."

What I was trying to say is that until there are CBDC's, the state has no implied obligations (not being the issuer or the promissary) to ensure that transaction using crypto are legit or enforceable.

What I was trying to say is that until there are CBDC's, the state has no implied obligations (not being the issuer or the promissary) to ensure that transaction using crypto are legit or enforceable

As I said, depends on whether or not on the jurisdiction. Even paying for goods and services with crypto (barter) is a taxable event in NZ, so it is not illegal to transact in BTC or any other digital asset. Therefore it is 'legit" and 'enforceable.'

"Even paying for goods and services with crypto (barter) is a taxable event in NZ..."

Good point, though whether it's actually taxed is another question.

The State’s power is given and taken away by the people, and the people decide what is money. We can trade and barter, or exchange value in whatever medium we choose. As stated by Gensler and Yellen, bitcoin is a commodity and the real innovation is the Bitcoin timechain. The opportunity to ban or kill it has long passed. It is now like a cyber wildfire that is being fanned by broken money and high to hyperinflation for half of the world’s population. Almost every single other of the 19,000+ “Crypto” tokens are crappy copies and unregistered securities It can take hundreds of hours to learn the difference, and unfortunately many don’t do their DD and get lured into the shitcoin casino for quick gains and speculative dopamine hits. We have monetised things like houses, luxury watches, precious metals, fine art, etc, all of which can be stolen, seized or destroyed. Bitcoin was designed/engineered to de-monetise these inferior forms of money back to their use cases.

When you do understand the innovation of triple-entry accounting, on an immutable ledger, that is decentralised across 15k plus nodes around the globe, all carrying exact and synchronised copies of the ledger, and they all verify the transactions right back to the start of the time chain every 10mins, then counter party-risk and fraud disappears. In addition, due to the sha-256 hashing and proof of work protocol, it is also the most secure computer network on the planet.

Like a phone network or a social network, the value to the users is derived from how many users are on the network. Many mistake this for a ponzi or greater fool scenario, but to many bitcoiners, we don’t care about entry/exit exchange rates (read “price”), we just watch the network grow thereby increasing our “value”.

I don’t think there will be an either/or scenario with bitcoin and existing (or surviving) fiat currencies, but there will be an easier choice as to which ones you hold in your digital wallet and how they can be used. I’d rather exchange some inflating fiat into a deflationary digital hard money, before people realise where the true value is secured.

"The State’s power is given and taken away by the people, and the people decide what is money."

Respectfully, I'd suggest that this opener is demonstrably false, even in a liberal social democracy. If it were true, the State's authority and banks would disappear tomorrow.

However, the rest of your comment makes sense to me, notwithstanding your claim that counterparty risk and fraud "disappears" (again, demonstrably not true).

You're take on equivalence with a phone network is interesting in terms of describing value, but I think you're mixing up the utility value to the consumer (i.e. the ability to transact communications over the network) with the monetary value of the subscribers to the owners of the network (in telco/digital world, ARPU).

Given the ubiquity of network inter-op, the value to the users is not subscribing to any given network as services are essentially relatively homogeneous (electrons are electrons) - it tends to be more about branding and commodity pricing.

Also, a distributed network utilising SHA-256 is not inherently secure in any way. It's how the cryptography is implemented that makes it more or less relatively secure. Trust me on this. It's not a selling point given emerging quantum crypto.

Overall though, I agree it's not really an either/or. I suspect it's more of a case of when CB/RB crypto tender becomes a reality rather than if.

I guess it depends on your belief on why we use the currencies we use. In NZ we accept and use the NZD.

here are three ways of understanding why we use that currency:

1) Because we are compelled to by the government; or

2) Because the community has collectively agreed to use it; or

3) A bit of both.

Traditionally it has been accepted that it is the state's monopoly on violence that upholds the value of the currency and made it widely available. But there are many examples throughout the world and throughout history which counter this - for example, if you go to Vietnam right now, the Dong is the only accepted currency, and the USD is strongly opposed by the government, but you can still easily by anything you want in USD (in fact shopowners prefer that you do). Or look at Nigeria, where alternative currencies are widely accepted and used, despite technically not being tender (and therefore not being enforceable by law).

Personally, I think the reason people use the currency they use is because the community collectively agrees to use it (everyone buys into the collective delusion that the money is worth something to others). Often, the easiest currency to use will be the one the government enforces, and therefore that currency is most likely to be collectively agreed to. But where there are reasons not to use an official government currency, the community may collectively agree to use a different one.

Government enforcement can make a currency more likely to be adopted, but isn't sufficient on its own. On the other hand, community acceptance is sufficient on its own to make a currency viable.

"Personally, I think the reason people use the currency they use is because the community collectively agrees to use it..."

This is really my point, accepting some some elements of that agreement are, realistically, compelled (or simply convenient).

"Government enforcement can make a currency more likely to be adopted, but isn't sufficient on its own. On the other hand, community acceptance is sufficient on its own to make a currency viable."

This is an excellent point. However, as per your example, the counter tends to be *another* official CB currency or a commodity like gold with a higher degree of trust and fungibility / utility, not alternatives like kauri shells or crypto.

for example, if you go to Vietnam right now, the Dong is the only accepted currency, and the USD is strongly opposed by the government,

True. Vietnamese also look to gold as a store of value. It is also one of the fastest adopters of Bitcoin and crypto (which I think is being used for cross-border transfers and payments).

VND is actually on a USD peg. Furthermore, the U.S. accused Vietnam of manipulating its currency. The hypocrisy is quite stark.

https://thediplomat.com/2021/07/vietnam-us-reach-accord-on-alleged-curr…

A CBDC is the digital form of a country’s fiat currency. That means an RBNZ issued CBDC, like the physical NZ dollar, would be a liability of the RBNZ, backed essentially by trust in the Government and its institutions. By law the RBNZ is the sole supplier of NZ banknotes and coins, with this being a key raison d'être for the central bank.

Exactly, and let's leave it at that level ~ $8.987bn. Furthermore, we need the private banking sector ($681.519bn) continuing to independently monetise government debt to collateralise the above mentioned trust in fiat/CBDC money.

Beyond that, creating credit for the private sector and government is not an acceptable function of government exposed to capture by private wannabees seeking influence by funding election campaigns of preferred politicians.

In other words "don't you go stuffing up the system" , it's worked for us bankers, since we came off the gold standard in 1971 .....and we have done extremely well out of it !

Let's cut to the chase .....it's all about profitability and the banks always have and always will do anything to maximize profits .....because that is the No. 1 AIM !

Has anyone ever thought about the transfer of money from one country to another and the fees involved, let alone the "one sided exchange rates".

What about a subsistence farmer in Kenya relying on their son's remittances from say the UK ....if he uses someone like Western Union etc up to 15% of those funds go into an intermediary's pocket !

On this site I notice the "anti crypto" brigade are the ones that have done well out of the current system or others that have done no research at all or just can't be bothered ....then blindly write it off.

People just don't like change ......well, get used to it because it's coming ....one way or another....whether it's CBDC's or Cryptocurrencies or a combination of both.

BIS argues money needs to fulfil three functions. These are; being a store of value, a unit of account and a medium of exchange. Cryptocurrencies, it argues, don't, and stablecoins need to import their credibility.

Bitcoin can and does fulfill these functions. The function that it doesn't fulfill is that it isn't accepted by the government to pay taxes. That's what puts the fiat in fiat... but it has nothing to do with whether a cyrptocurrency fulfills the function of money.

Frankly with high inflation (which is continuously compounding), fiat currencies hardly function as a store of value. Bitcoin or gold fulfill that function better.

There's the volatility question which doesn't really lend BTC being regarded as a somewhat predictable SOV.

Also, there's a considerable efficiency / fungability problem with BTC being a viable unit of exchange.

As soon as the problem of buying a loaf of bread with part of a Bitcoin is resolved that's less of an issue, I guess.

Very true on the tax front though - that'll be a key driver for CB crypto.

As soon as the problem of buying a loaf of bread with part of a Bitcoin is resolved that's less of an issue, I guess.

The solution already exists.

https://www.businesswire.com/news/home/20210605005045/en/Strike-Drives-…

"The solution already exists."

Sort of. Cash doesn't rely on your phone being charged and having an internet connection though.

You would think that as long as a legal contract exists for any transaction there should be enforceability to provide the good(including DC) or service. It shouldn't matter what the item is eg Fiat currency or DC. Governments not wanting to enforce contracts that involve DC show their true intentions regarding their need for financial control and not your freedom from the current financial system.

True, but for a contract to enforceable the consideration needs to be recognised.

Generally, that requires it to be taxable in some form, essentially to cover the enforcement overhead.

The implications for retail banks will be huge. In a country with only a CBDC their importance will diminish greatly. Services will be more like a skin put on top of the base CBDC platform. Barriers to entry will lower and providers will essentially be providing online wallets. Not sure how the mechanics of lending services would work. But defi lending against property NFTs could easily work. And this is already happening in crypto world.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.