By Jenée Tibshraeny

Tower has regained its “financial equilibrium” thanks to 88% of its shareholders taking up their rights in a capital raise completed in December.

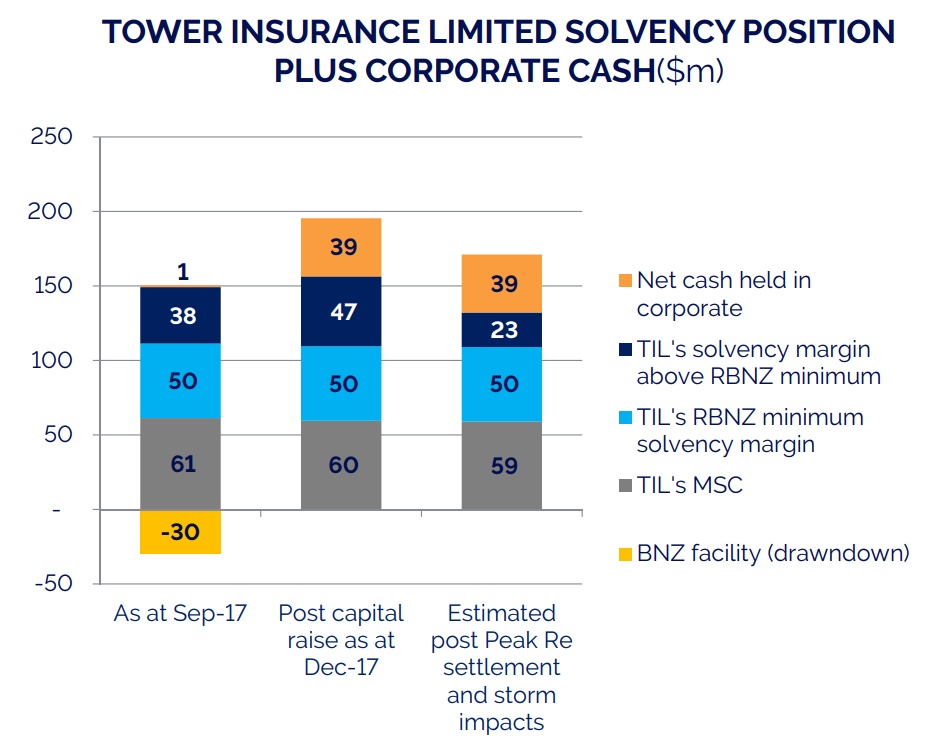

The New Zealand insurer has $62 million of capital above the minimum required by the Reserve Bank (RBNZ) - $39m of which is being held as cash.

This is a vast improvement from its position a year ago, when it only had $5m of capital above this level, so took out a $30m BNZ loan to keep its head more comfortably above water.

Following its capital raise, Tower repaid this loan.

Its rights offer saw it raise nearly $71m of capital. Just over $62m of this came from its shareholders, while Goldman Sachs - the underwriter of the offer - took up the remaining shares.

Speaking at Tower’s annual shareholders’ meeting on Thursday, chief financial officer Jeff Wright said there was a “strong take-up” of shares from existing institutional investors, with a number returning, having previously sold their holdings.

Vero also participated in the capital raise, so maintains its 19.99% stake.

The raise saw Tower exceed the RBNZ’s solvency requirements by $86m.

However this figure has fallen to $62m following the recent storms, and Tower on Wednesday reaching a settlement with Peak Re that will see it receive half of the $44m of reinsurance for the 2011 Canterbury earthquake that it was banking on.

The major risk Tower still faces is over how much it will be reimbursed by the Earthquake Commission (EQC) for Canterbury repairs and rebuilds it paid for on behalf of the agency.

It has accounted to receive $65m, however Wright says this is a modest estimate.

With the court involved, and the issues in dispute complex (largely stemming from different methods being used to calculate liability), Wright believes it will be some years before Tower gets all the money it believes it’s owed.

Looking back

So yes, Tower’s financial position has stabilised.

Yet pressed by someone at the shareholders’ meeting, Tower’s chairman Michael Stiassny admitted it wasn’t prudent for the company to have paid the dividends it did after the Canterbury quakes, up until suspending payments in 2016.

“If we look backwards… you would say, that probably wasn’t the most prudent thing to do,” Stiassny said.

“At the time the dividends were paid out, it is fair to say that Tower’s view - as to the effect of Canterbury earthquake and claims on the balance sheet of Tower - was significantly different than was the case later.”

Tower’s equity fell from $281m at the end of the 2015 financial year, to $224m in 2016, and $216m in 2017.

This is how its dividend payments tracked:

- FY17: $0

- FY16: $27m

- FY15: $29m

- FY14: $24m

- FY13: $27m

- FY12: $19m

The Tower board expects dividend payments to resume at the 2018 full year, “subject to financial performance”.

Stiassny also commented on the issue of the Commerce Commission in July rejecting Vero’s application to get approval to buy Tower.

Challenged on the extent to which Tower - New Zealand’s third largest general insurer - considered the likelihood of the competition watchdog having an issue with allowing the country’s second largest insurer to buy it, he said: “We took legal advice, and we were very comfortable at the time.

“We thought that they would get through.”

Lured by a higher bid from Vero, the Tower board lost the opportunity to sell the company to a rival Canadian buyer, Fairfax Financial Holdings.

Stiassny confirmed the board hasn’t had any further engagements with Fairfax.

Looking forward

Vero is looking to sell its stake in Tower.

There is a possibility its 19.99% blocking stake in the company contravenes competition law. The Commerce Commission is investigating this.

Stiassny alluded to the fact it was unlikely Tower was going to be sold - at least not to Vero or IAG - the country’s largest general insurer.

He didn’t respond directly to a question asking whether it would be difficult for Tower to get a price much higher than the $197m previously put on the table by Fairfax, to reflect the fact nearly $71m had just been injected into the company.

The shareholder who asked this question noted that while more capital had been injected into the company, the underlying business hadn’t really changed.

Tower’s market cap is currently (as at Friday) $246m.

At 73 cents, its share price is the highest it has been since August. Tower’s shares were worth $1.28 each two years’ ago.

2 Comments

Failure to comprehend their potential liability for the Canterbury EQ’s. Persistence in recklessly generous and self serving dividends simultaneously. Insufficient re-insurance, in relative terms, almost as bad as AMI. Guess that explains the punitive, dictatorial, unjust treatment by Tower of a very large number of those EQ claimants.

Big people can make big mistakes and make little people pay for them. New company slogan?

It sounds like Jeff Wright has a high quality crystal ball, given his confidence in not only securing a $65M recovery from EQC, but to also book this recovery now and then further predict it has upside potential. No mention from him that an adverse court decision on these very complex issues could potentially increase Towers liability. Their recent Peak Re experience where they achieved only a portion of the amount they were confident of securing, doesn't provide encouragement over the accuracy of Wrights forecasts. One assumes Towers optimism over the outcome is shared by the rest of the industry, so of interest would be a comparison with the level of provisioning for these EQC 'recoveries' that other insurers have made.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.