By Jenée Tibshraeny

The Reserve Bank (RBNZ) warns insurers’ moves to reduce their exposures to earthquake and flood-prone properties could reduce the value of people’s homes.

Insurers have within the last year upped the ante on risk-based pricing, using more granular data to more accurately charge customers for the risks they pose.

This has seen some premiums sky-rocket, and in the most severe cases left some properties uninsurable.

The Press on Wednesday, for example, reported on a couple struggling to sell their “immaculate” quake-repaired bungalow due to it being uninsurable and banks therefore refusing to lend against it.

While the RBNZ in its previous biannual Financial Stability Report (FSR) released in November said it wasn’t sure whether risk-based pricing reflected “cyclical factors” of the market, or a “structural shift towards higher premiums and more restricted cover”, it appears to have decided the latter is the case.

“It is likely that risk-based pricing will become more widespread in New Zealand over time,” it said in its latest FSR released on Wednesday.

“Owners of particularly high-risk assets should be aware that their insurance costs are likely to rise and the level of cover that they can obtain may become more limited in the future.”

House prices could be hit

The RBNZ noted risk-based pricing transferred the risk from insurers to affected households and businesses, as well as institutions that lend to them.

“This is likely to reduce the value of assets negatively affected by risk-based pricing, and weaken the financial positions of the assets’ owners,” it said.

While the likes of IAG and Tower have refused in the past to clarify with interest.co.nz what portion of their customers would experience premium hikes versus cuts as a result of risk-based pricing, the RBNZ said it expected a small portion to face “materially higher prices”, with very few unable to obtain full cover.

“But the precise impact on the overall availability and price of insurance is uncertain, reflecting limited information on reinsurance costs for New Zealand and insurer strategies,” it said.

“The Reserve Bank is engaging with insurers and reinsurers to better understand the evolving position in more detail.”

Value in pricing people out of high-risk areas

While interest.co.nz understands risk-based pricing to have hit quake-prone properties harder to date than flood-prone properties, Reserve Bank Governor Adrian Orr said in a media conference he saw quake and climate risk on par with each other.

He accepted price signals were necessary to direct investment away from assets vulnerable to the effects of climate change.

“Insurance will evolve, better pricing needs to evolve. People need price signals to make their decisions for a smooth transition [to mitigate against the effects of climate change],” he said.

“On the other side of it as well, we don’t want to see prices rise in some areas and not alter in others.”

Matters made worse by a concentrated market

Asked by interest.co.nz whether the RBNZ was concerned insurers were using risk-based pricing as a money grab, Orr said: “We are right amongst it at the moment, really trying to get our heads around working with the industry, in part for exactly that. Sunlight is a great disinfectant.”

Asked whether there was a point at which the prudential regulator would intervene in the market, he said the RBNZ was trying to strike a balance between ensuring insurers were “transparent” with their pricing, while keeping their books in good shape.

Orr also said he wanted to see more competition in the market.

The RBNZ in its FSR warned: “A rapid and disorderly change in the provision of insurance could also reduce competition and efficiency in the insurance market.

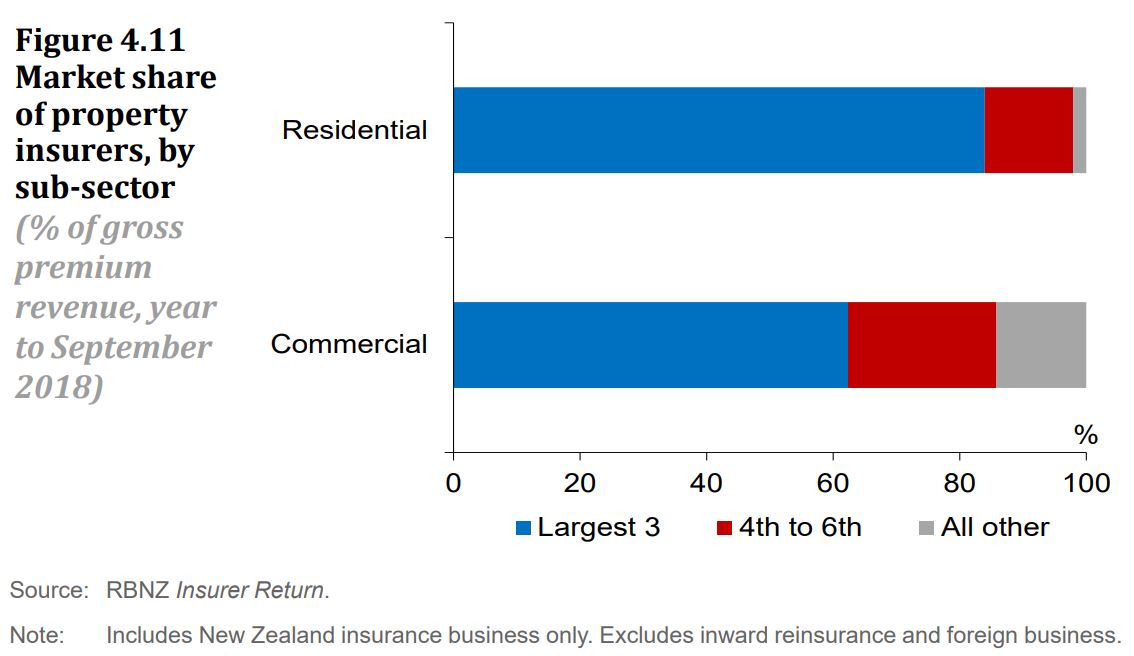

“The impact of risk-based pricing in New Zealand is likely to be amplified by the high concentration of the general insurance sector. High concentration reduces the capacity of other insurers to insure risks affected by risk-based pricing.”

The insurance market is set to become even more concentrated, with Allianz on Tuesday announcing it would stop providing commercial property, motor and liability insurance in New Zealand.

RBNZ working on climate risk disclosure framework

Looking at the bigger picture, the RBNZ warned: “As banks and insurers respond to climate change risks, some risks may ultimately end up with other parties, such as central and local government.

“It is important that these potential market dynamics are understood and managed appropriately.”

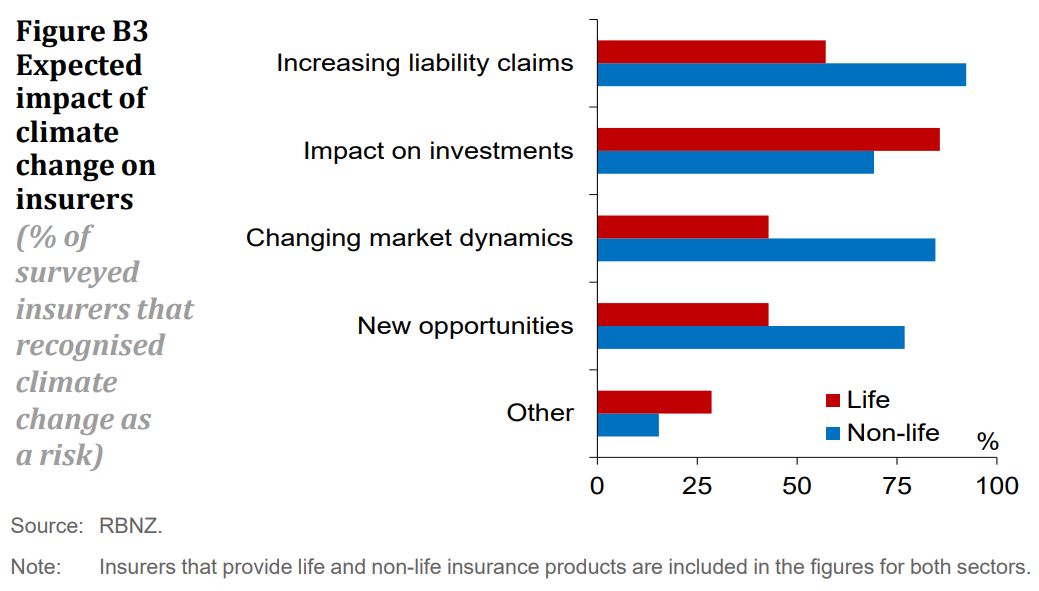

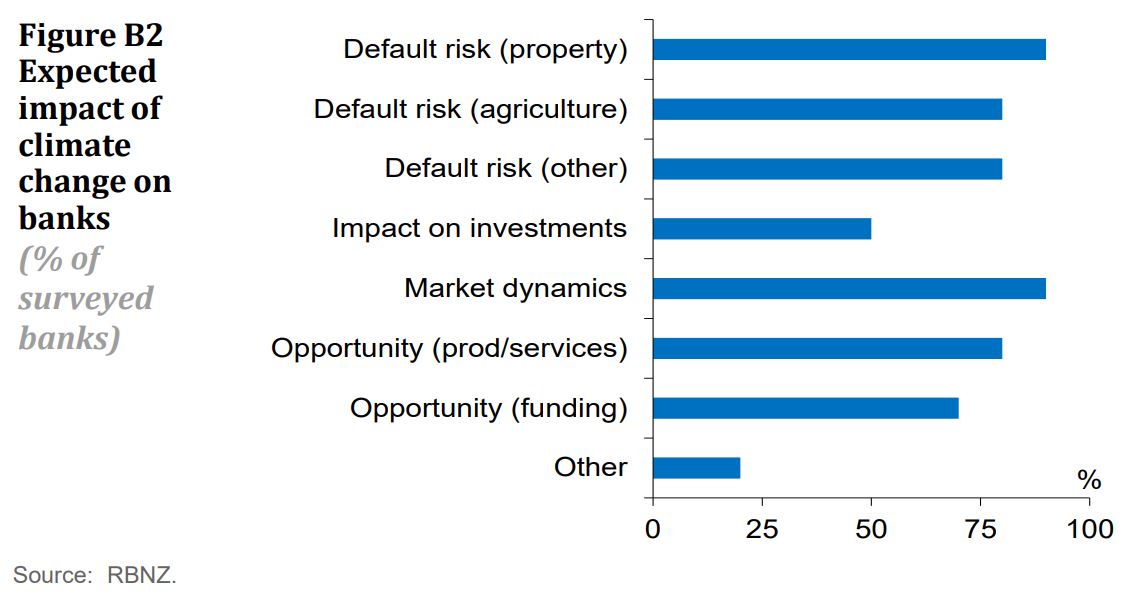

While all the banks and 90% of the general insurers it recently surveyed saw climate change as a risk to their businesses, respondents provided little evidence that these concerns were influencing their day-to-day business decisions.

The RBNZ said it was continuing to engage with banks’ and insurers’ management and boards so they consider all material risks when setting the strategic directions of their businesses.

The RBNZ said institutions’ exposures to climate risks had to be better disclosed in line with international standards.

“The Reserve Bank places significant emphasis on disclosure as part of its regulatory framework, and is committed to working with industry and wider stakeholders to develop an appropriate climate risk disclosure framework for New Zealand.”

For more on how risk-based pricing is affecting apartments, see this story.

And for the latest on how risk-based pricing has pulled Tower back into profitability, see this story.

19 Comments

I am surprised that this is not headline news in the main stream media, maybe it is behind a paywall....

This is bigger then Ben-Hur, no interest rate cut can offset inability to obtain insurance or massively higher premiums....

Quite.

Unfortunately nowhere is safe. Hilly country = earthquake/slip prone. Coastal = flooding/erosion. Both? Sell now if you can.

This will inevitably drive purchasing behaviors, even before insurers/banks enforce it - sure that cottage on the beach might look beautiful today, but within the mortgage period - say 15/20/25 years - it may well be underwater!

The fact that insurers wouldn't insure it and banks wouldn't lend on it will simply mean people can't buy it even if they really really wanted to.

Hmm. Perhaps a new market for submersible housing?

"The fact that insurers wouldn't insure it and banks wouldn't lend on it"

The will become cheap as chips, and as people will use them till the go under water, no one will put money into them, which will mean a derelict looking coast line in the future.

Back to the old corrugated iron bach on the beach front. Yey.

I expect that the insurance industry will be subject to increasing regulation - as, clearly, it's heading in the direction of market failure.

The industry should not forget the basic principle underlying insurance - i.e. "to spread the risk".

I'll be quite happy to see government sock it to mercenary insurance companies.

TTP

Jenee, very interesting. Is there any indication on how many properties will have either increased premiums or be prohibitively expensive to insure ?

could be those insurance companies have been taken out the back of the wood shed and flogged by the reserve banks determination that they can save the world by lowering interest rates. Their return on investments destroyed by low returns while assets have increased four fold.

http://professorfekete.com/articles/AEFHowFedBankruptedInsInd.pdf

So you have a property in say Wellington with a high quake risk and insurers increase premiums by $5000 and now you cant afford insurance without reducing expenditure elsewhere and have to have insurance to maintain a mortgage. Effects - lower discretionary spending= less jobs = less employment = more benefit payments = lower property values= reduced equity to support say business loan and possibly increased interest if loans fall below LV ratio & lower value = lower rateable value next revaluation= higher rates for others and these are just the obvious effects. Can I be sure that Treasury/Govt will factor this into policy as carefully as budget info was secured?

Equals more incentive to pay off the mortgage. Ditch insurance because the govt will bail you out like in Chch if a big general disaster occurs.

Indeed Rumpole, imagine being 66 years old just retired 4k in rates and 5k in insurance living in WGTN, thats a lot of cash out the door, if you have to find 9k per annum you need $276.923 in a 3.25% term deposit, oh yeah you have to pay tax... (and eat.. pay power bills etc) lets call it 300k just for these two out goings.

Pressure to sell up and more to a cheaper to insure location with lower rates will look attractive...

hard to find any council in NZ thats not still paying for past miss adventures.... Huntly is cheap

But who is going to buy your over priced risky old hillside home in WGTN, sitting on several major faults?

Just had look at Trademe Insurance quote for a house policy in Christchurch. Even in suburbs not damaged in the earthquake they are showing annual premium of around $3300 for a $500k cover.

A real (rather than the usual catastrophist) example:

Value insured: $581,300

Insurer: AMI

House area: 185 sq m

Total cost GST inc: $1,452.11

Valid to: June 30 2019

This is for a 27 year old house 200m back from Waimairi Beach, Christchurch........no history of flooding, liquefaction, shark attack or other marine incursions.

Now there might be a premium increase imminent - but it sure ain't gonna double....

Rode through the quake sequences just fine - a verbatim report here....

Waymad. Ground shaking effects and consequent liquefaction varied significantly in the Waimairi beach area, depending on the quality of the land underneath the house. I suspect you’ll be aware of properties not too far from you that fared much worse than the one you cite and those people will be starting to feel the premium pain much more than you. Your example of the comparatively modest premium you are paying highlights the key issue - that insurers now have such detailed geographic information system data that they are able to identify the risk factors at individual property level, not just at suburb or even street level, as was the case until relatively recently. Competitive pressures and brand risk are making them cautious about revealing the very granular level of GIS data they possess and also how they intend to implement risk based pricing but the death by 1000 cuts process is underway. Once Tower jumped out of the blocks with RB pricing none of them could afford to not do the same as otherwise they’d be selected against ( ie increase their % of higher risk properties).

Of course, YMMV. Of the 500+ properties in Waimairi Beach itself, 2 were demolished, both down to garage separating from house, because (quelle surprise) the builders had thoughtfully removed the rebar in said garages, to use on the next house, after inspection but before the pour.

Christchurch has Soils & Foundations maps dating to the early 90's which located precisely the areas of liquefaction, and these proved to be accurate. To be sure, as you point out, back-dune and old swamp areas fared badly - but then again, the S&F maps had nailed this two decades before the quakes. So the notion that 'property-by-property' risk was unquantified until after the quakes, is simply wrong. The S&F maps were broadly accurate, and later assessments had had the Big Data of EQC and private insurance claims to draw upon. The combination is what has led to risk reassessment.

Before the quakes, put simply, the known geotech data had been blithely ignored - by Councils, insurers, owners and Gubmints alike.......

NZ generally needs to accept that anything we build is going to be temporary because of the geological and geographical conditions, and construct and price accordingly.

Temporary on a geological timespan sure.. but in human lifetime spans not so much.

Lockwood houses can take a force 9 earthquake on the Richter scale which is exceptionally strong

This should be the standard along with not building in flood prone areas

Two thoughts.

1.My understanding is the EQC levy is collected on behalf of Govt. by your insurer (need fire insurance as a minimum), ie no insurance no EQC cover. Could you maybe pay the EQC levy direct to Govt. so you are covered for that amount, which is the first amount to get claimed anyway?

2. Are we only talking about not being insured for those flooding and earthquake risks (were they exist), ie could you opt out or have a capped max. for those risk alone, yet still be covered for the likes of fire etc.?

Also there is a difference between not being able to get any insurance, and insurance that is just a lot more expensive. No insurance could mean no ability to use the land/house as security for a loan. Expensive insurance is just your ability to pay, and you could work out the offset needed in purchase price, ie how much lower the capital investment needs to be to offset the increased operational expenditure.

If its a flooding issue then redesign to Queensland or Louisiana style, there is housing already built in New Brighton where house has been raised and ground floor basement underneath in concrete block has been built to withstand flooding. Basement is excluded for cover on insurance policy.

Speaking as someone with many friends in North American Insurance I can say NZ & earthquake risk is top of mind & I know many reinsurers here who won’t touch NZ after ChCh at all

Add in so called extinct volcanoes everywhere in Auckland & Rangitoto overdue to explode & you can see their point of view

Only Aucklanders appear oblivious to risk yet I felt quake jolts

there on 2 occasions over 55 years plus tornadoes since the early 1990s on Nth Shore

Yes it’s not like gods own zone these days

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.