In a move that may pre-empt a downgrade of its AA credit ratings on New Zealand's big four banks, Standard & Poor's (S&P) has downgraded its Banking Industry Country Risk Assessment (BICRA) on New Zealand to group 3 from group 2, placing major local banks in the same group as Italy, the United States, Britain and South Korea.

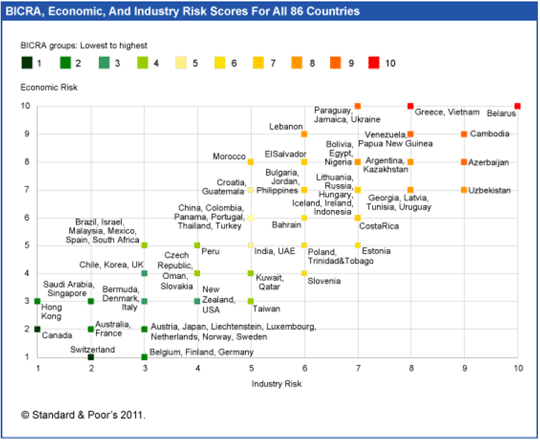

S&P says its BICRA methodology evaluates and compares global banking systems using economic risk and industry risk factors.

A BICRA is scored on a scale from 1 to 10, ranging from the lowest-risk banking systems (group 1) to the highest-risk (group 10).

The move comes as S&P completes a long running review of its ratings methodology, which it has been anticipated could see New Zealand's ANZ, ASB, BNZ and Westpac have their credit ratings downgraded a notch to AA-, potentially increasing their funding costs.

Any rating change is likely to be announced later this month or in December. See more on this here.

"Our economic risk score of '3' for New Zealand reflects our view of the country's 'economic resilience' and 'economic imbalances' as being 'low risk,' and our view of 'credit risk in the economy' as being of 'intermediate risk,' as our criteria define those terms," S&P said.

"We consider that New Zealand's open, flexible, and well-developed economy, and its relatively high income levels, partly offset the weaknesses associated with its dependence on agricultural commodity exports."

"We believe the economy has favorable prospects for sustained growth given there remains strong demand for agricultural exports. In our view, the New Zealand economy's overall resilience reflects decades of structural reforms and wages restraint. In the recent years there has been some private-sector deleveraging, and an orderly wind-down in the real estate prices, factors that in our view should limit the risk of a sharp correction," the credit rating agency added.

"Nevertheless, we believe that the external imbalances, evidenced in persistent current account deficits and high external debt, could affect the economy. In our view, credit risks in the New Zealand economy are reflected in a high level of private sector debt, at about 150% of GDP, and the concentration of lending to the agricultural sector, including the dairy sector."

S&P goes on to say, however, that it considers these risks are partly offset by conservative lending and underwriting standards, a legal framework that supports creditors, and a strong track record of a low level of nonperforming assets and credit losses compared with elsewhere over the past several years.

Recently both S&P and rival Fitch Ratings downgraded New Zealand's sovereign credit rating to AA from AA+.

Meanwhile, S&P has assigned New Zealand an industry risk score of 4, with the possible ratings also ranging from 1 to 10.

S&P says the industry risk is determined by the quality and effectiveness of bank regulation and the track record of authorities in reducing vulnerability to financial crises, the competitive environment of a country's banking industry including the industry's risk appetite, structure and performance, and possible distortions in the market. It also covers the range and stability of funding options available to banks, including the role of the central bank and government.

"This (NZ) score takes into account our view of New Zealand's 'institutional framework' and 'competitive dynamics' as being 'low risk,' and our view of New Zealand's 'systemwide funding' as 'high risk.' We consider that regulation is conservative compared with international standards, and that the regulators monitor banks closely and frequently," said S&P.

It said the regulator - the Reserve Bank - has a "reasonable track record" of identifying problems early and taking corrective actions, evidenced in very few instances where support has been required. Furthermore, the New Zealand banking industry is supported by "restrained risk appetite."

"In our opinion, the sector has generally been able to prudently price for the risks taken, and has generally not shown tendencies to chase aggressive returns," said S&P.

"Additionally, we note: the absence of the use of innovative, complex, and risky products; very limited high-risk lending; and prudent compensation practices. We consider that there are minimal market distortions due to government intervention or competition from the nonbanking sector."

Nonetheless, the high dependence on net offshore borrowings, which S&P estimates fund about 42% of domestic customer loans, and limited support from core customer deposits, which fund only about 44% of domestic customer loans, weaken New Zealand's banking system.

"We consider that these weaknesses are partly offset by potential funding support from the Australian parents of the major banks and the government and regulator. We regard the government and regulator as responsive and flexible to the changing needs of the banking industry."

"We classify the New Zealand government as being 'supportive' of the banking system, reflecting our expectation that the government is likely to organize or facilitate market-led solution to support systemically important financial institutions should it be needed." S&P added.

See more on S&P's changes in our earlier story here.

(Update adds S&P chart and detail on industry risk scores).

17 Comments

"ratings methodology" ....that'll be throwing the dice with the other hand...right...err left!

isn't this the ratings agency with a record of branding CDOs as AAA when the crap was FFF

They set and kept Poor Standards!

Great News S&P timing could not be better....i gues you didn't like John Boy's little crack about less chance of a downgrade with National so decided to go the BIC route on it.....ha ha ha ha ha ha ha...!

Well whaddaya say now the Billy Bob........

On the ratings side of it............you had to get it right sometime.!!

... but we're still a notch above North Korea ! .... I think that's just cause for celebration , don't you ?

Kazakhstan has risen to BBB+ , recently . .. Oh , how Borat has enriched that sweet country . If only Bernard Hickey would don a mankini , and raise the profile of NZ , similarly .

Kim Jong il has lunacy for an excuse GBH......we used to have geography....!

Can't wait for the currency boys Mickey and the team to get the spin going on it....should be a laugh......

When is the next milk powder auction...?

What's the bet smile and wave will appoint goofy, our first ambassador to North Korea! Phil will love that...a chance to see what socialism can become.

Gummy,

You first with the mankini

Me in a mankini would be cruel and unusual punishment for many, many people, not least of whom would be me, then you, and then everyone else....

cheers

Bernard

For the uninitiated ctnz a fantastic watch...the circulation of it to the masses becoming the priority.

It's funny you know because when I had a theory about bringing down the horse my choice of first target was Coca cola...! hilarious but true.

Watching that guy move around .. must have ADHD .. reminded me of Greta Van Susteren the legal commentator on Fox News .. the only thing that moves is her mouth http://www.youtube.com/watch?v=es9IWh6DKhg

Reptilians....

"According to British writer David Icke, 5 to 12-foot (1.5 - 3.7 m) tall, blood-drinking, shape-shifting reptilian humanoids from the Alpha Draconis star system, now hiding in underground bases, are the force behind a worldwide conspiracy directed at humanity"

Maybe so... :)

"We classify the New Zealand government as being 'supportive' of the banking system, reflecting our expectation that the government is likely to organize or facilitate market-led solution to support systemically important financial institutions should it be needed." S&P added.

And from the RBNZ's 'Open Bank Resolution' policy document:

"Whilst there are differences between different classes of

unsecured creditors, they all have the same legal claim on

the bank. Each has freely invested in a private institution and

has enjoyed a return on that investment whilst accepting

the risks associated with the investment. Under the OBR,

it is expected that all unsecured creditors would be treated

equally with the same proportion of claims remaining frozen

for all depositors and creditors. The only difference in

treatment will be the speed with which each class of investor

is able to access the unfrozen portion of their claim."

Why on earth would a retail depositor support this regime?

Retail depositors are captured in a low to negative real return financial vortex dominated by increasingly incapacitated and incompetent regulators. Forward regulatory guidance is changed on a whim to favour those with the least to lose.

The systems in place favour the few (covered bond holders?) at a cost to be borne by the majority be it through taxation or capital lost. When was it ever not so?

"We classify the New Zealand government as being 'supportive' of the banking system, reflecting our expectation that the government is likely to organize or facilitate market-led solution to support systemically important financial institutions should it be needed." S&P added.

Translation- we regard the Goverment as yes men to banking interests.

@ Christov & ctnz

We are captured by our banks to the extent they monetise the issuance of government promises to pay.

The mantra of foreigners selling their currency to lend to us is the biggest fallacy ever perpetrated

Foreigners (offshore investment banks) raise credit lines @ NZ domestic banks to settle their purchases of NZ Government debt issues. Hence the local Austalian four finance all our national borrowings.

All we ever do is borrow foreigner's credit ratings, thus we debase our currency locally.

And those ratings are increasingly suspect hence I see an explosion of asset backed borrowings (covered bonds) dominating proceedings, whereby euro/dollar investors demand access to the banks' assets. Not that this reduces the creation of NZD. The cross currency basis swap mechanism to get foreign currency borrowings turned into NZD demands more be created.

"We are captured by our banks to the extent they monetise the issuance of government promises to pay."

Yes of course, because government debt provides them with a risk free safe haven. The last thing a bank wants is for an OECD country's government to pay back all their national debt. Not when under the Basel Accord, they don't have to back OECD government debt with any bank capital at all. The Euro crisis is largely a ploy by British and U.S. financial interests to destroy Europe's economy in order to force them to implement drastic political and economic reforms so that they can acquire publicly owned infrastructure assets at firesale prices. Just like they did in the wake of similar economic catastrophes throughout the Third World in the 1980s in the wake of Paul Volckers interest rate shocks.

http://www.euromoney.com/Article/2459161/Privatization-The-road-to-wiping-out-the-US-deficit.html

"My theme this evening is somewhat different. I still want to argue that when governments introduce reform is a dangerous moment.... So I want to examine what we have learned about the way economic policy reform can most successfully be implemented. I want to look at what we mean by economic policy reform: I would argue that successful economic reform is much more wide-ranging than we realized until relatively recently...Crises force significant policy reforms on a government. Hence my reference to a dangerous moment. In a crisis, there is little enough time to act, let alone think. The exact nature of the crisis will determine what reforms are needed and in what order."

http://www.imf.org/external/np/speeches/2004/091004.htm"The cross currency basis swap mechanism to get foreign currency borrowings turned into NZD demands more be created. " "

Stephen... Can u tell me where I can learn more about how this works..????

Is it that the Reserve Bank simply steps in to provide liquidity...????

What is the relationship between the Supply and Demand dynamic of our floating exchange rate.... and the creation of NZD so that the foreign currency can be changed into NZD..???

I can't find much info out there... about how this happens ...and how it shows in the Reserve Bank Balance sheet...

Also... your comments on the OBR are eye opening !!!!!! I never quite realized how one sided our Reserve bank is...

Cheers Roelof

@Anarkist

Yes of course, because government debt provides them with a risk free safe haven

I think the the 'risk -free' 'ring of confidence' that previously embellished sovereign debt has been broken.

Banks have taken hideous losses, in the last few days alone, on their European sovereign debt portfolios.

My contention is that governments will find it increasingly difficult to finance their citizens transfer payments with the issuance of paper which traditionally implied negative pledge status.

The introduction of the New Zealand Local Government Funding Agency, http://www.chapmantripp.com/publications/Pages/Local-Govt-Funding-Agency.aspx states the followinguuuuuuustate implies clearly that some councils may have to pledge assets to secure loans:

Clause 9 applies only if the Funding Agency is also a council-controlled trading organisation. This clause overrides sections 62 and 63 of the Local Government Act 2002 and authorises local authorities to give guarantees, indemnities, or securities to the Funding Agency and to lend money or provide other financial accommodation to the Funding Agency on more favourable terms than those that would normally apply.

This just the beginning of the introduction of asset transfer mechanisms that will de-nude us of our infrastructure.

The contention that the UK and US will be the beneficiaries is unlikely as printing money as they do makes them just as vulnerable, as their respective currencies de-base.

I have no sympathy at all for bank losses, because a) they were self-inflicted and b) they weren't truly hair-cuts, because if I'm reading the news about the European parliaments plan for dealing with the Euro crisis correctly, every dollar the banks lost they received back in bailouts from the EFSF. And besides a good portion of the debt liabilities European governments assumed were to bailout the banks due to their reckless lending behaviour. "For the past two centuries, the tables have progressively turned. The state has instead become the last-resort financier of the banks. As with the state, banks’ needs have typically been greatest at times of financial crisis. And like the state, last-resort financing has not always been repaid in full and on time. The Great Depression marked a regime-shift in state support to the banking system. The credit crisis of the past two years may well mark another." http://www.bis.org/review/r091111e.pdf "The contention that the UK and US will be the beneficiaries is unlikely as printing money as they do makes them just as vulnerable, as their respective currencies de-base." Nah, because the "money" printing only creates extra reserves on bank balance sheets, but with modern monetary mechanics reserve balances aren't the limitation. Willingness of banks to lend is. When economic activity is contracting like it is, hyperinflation is practically impossible. Unless the people lose total confidance in the monetary system, which means that we would have far more critical things to worry about than mere cost of living.

Excuse cut and paste and edit errors

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.