By the Westpac NZ economists*

A recovery in global dairy prices has provided welcome relief for the beleaguered dairy sector, with cash flows for most farmers headed firmly back into the black this season. While other parts of the agricultural sector have been performing better in recent times, insipid global growth and rising supply are expected to keep the prices of most commodities contained. And with the NZ dollar lingering higher, and competition heating up in many key markets, exporters will need to keep working smarter to stay competitive.

The dairy sector has found itself on firmer ground over the past few months, courtesy of a 50% lift in global dairy prices. This recovery in prices (back to mid-2014 levels) reflects supply and demand moving into better balance, although sentiment and prices look to have run a bit ahead of fundamentals. While this makes prices vulnerable to some retracement as we move into 2017, a more balanced market should see prices remain well clear of this year’s lows. For New Zealand’s farm gate milk price, the timing of the price moves is critical. With higher prices coinciding with peak production, we’re now forecasting a farm gate milk price of $5.80/kgMS this season. And we see further improvement ahead, with a $6.10/kgMS milk price pencilled in for 2017/18.

While a higher payout this season will see a return to positive cash flow for most farmers, we’re not expecting farmers to rush out and spend. After two seasons of negative cash flow that required most farmers to take on additional debt to carry them through, the focus will now be now on getting balance sheets back in order. But nonetheless, the outlook is certainly more optimistic than we expected three months ago.

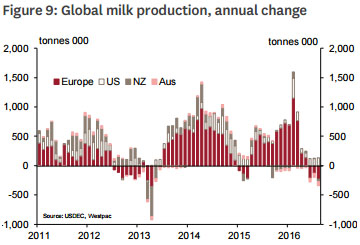

Clear signs around the middle of this year that global milk supply was moderating (after the previous year’s surge higher) has been the key factor lifting prices. Notably, European milk production in July and August was running 1.4% below 2015 levels, with payments by the European Commission to reduce production providing farmers further incentive to scale back supply. Australian production has also fallen sharply, as farmers grapple with low returns and wet weather. But bucking the trend has been US milk production, on track to grow 2% this year.

New Zealand milk production has also been tracking lower, off the back of a smaller national herd and a swing back to a predominately pasture-based regime. But it was news of a soggy spring sharply lowering production in some regions that really caught the attention of dairy markets, and gave prices a second wind. While Fonterra is forecasting a 7% decline in its milk collections this season, we are not as pessimistic about nationwide supply. If anything, the sharp lift in prices helps limit downside in supply, as it encourages farmers to raise production by adjusting feed regimes. Moving into next year, we expect broader production dynamics to weigh on dairy prices. Barring a significantly dry summer, New Zealand production should be less dire than many fear, while the pace of decline in European production is likely to ease.

Demand has also chipped in to support higher dairy prices. Improving demand has been dominated by China, with imports of whole milk powder in the year to date up 20%, while demand in the rest of Asia has remained sluggish. We see a more gradual pace of demand growth ahead, as global growth remains subdued, and as previous low prices gave buyers ample opportunity to stock up. Meanwhile, the unexpected US election result has created additional uncertainty about the outlook for global demand and commodity prices.

A brighter hue

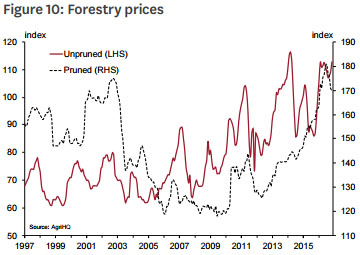

It’s been a bumper year for the forestry sector, buoyed by solid domestic and export demand. Strength in domestic demand isn’t surprising given the boom in construction. But a surge in exports this year has been surprising, with record volumes of logs and timber shipped in the September quarter, while prices have hovered around record highs.

An acceleration in demand from China, which takes the lion’s share of New Zealand’s log exports, has driven the shift in momentum this year. After treading water through 2015, real estate construction has picked up, as rapid house price growth has broadened across cities. Developments in other key export markets have also been positive. In Korea, a solid pipeline of construction has seen log demand recover, while demand from India continues to trend higher.

With the large standing of early-1990s plantings ready to be harvested, New Zealand is well placed to capitalise on high prices. But other exporters are also eyeing up opportunities. Russia was exporting record volumes of lumber to China through the middle of this year, as producers benefit from the weak ruble and improving productivity. And with the US and Canada struggling to renegotiate a lapsed trade agreement for softwood lumber, more Canadian supply might end up on the Chinese market.

Heading into next year, prices are likely to feel the pinch from both directions. At the same time as large suppliers look poised to increase supply, demand growth may falter as Chinese construction continues to be buffeted by several headwinds – not least, a lingering oversupply of new homes in some areas.

Mixed bag

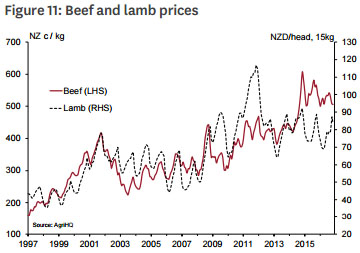

Beef and lamb farmers have seen diverging fortunes in recent years. Beef farmers have benefitted from exceptionally high prices since mid-2014, as global supply has been constrained by herd rebuilding in the US and Australia following severe droughts. But with herd rebuilding in the US now well advanced, US beef production and exports are set to rise this year and next. Global production is expected to rise 1% in 2017. This would be the largest rise since 2013, and should eventually be reflected in lower prices.

But even with global prices remaining favourable, life might become more difficult for New Zealand beef farmers, as a reduction in trade barriers increases competition in key markets. China has announced the removal of a 13-year ban on some US beef products, and the US has also eased import restrictions, with the first fresh beef exports shipped from Brazil recently.

Meanwhile, the sun hasn’t been shining so brightly on lamb farmers. Prices have been oscillating around an average level for the past few years, as relatively tight supplies of lamb from New Zealand and Australia have been countered by subdued demand in key European markets. The fall in oil prices has also hampered demand from the Middle East, and exports to China have been very disappointing, down 17% in the year to September.

Prices are expected to track broadly sideways over the next year as supply remains tight, although the Brexit vote has clouded the demand outlook. In the near term, the sharply weaker pound makes British lamb much more competitive in the UK and other European markets, which will weigh on NZ dollar returns. And over the medium term, access to the UK market is uncertain, with British sheep farmers likely to push for tighter restrictions on New Zealand lamb.

While the meat sector faces numerous challenges in growing export returns (not least, the downtrend in sheep and beef numbers over time), our recent Industry Insights report highlighted several opportunities for the sector.¹ The prospect of chilled meat exports to China presents a significant opportunity, although there are a number of hoops to jump through first. Another opportunity is to create a coherent New Zealand “brand” internationally that would help “tell the story” of New Zealand products, in order to shape preferences and attract a premium price in the way that other sectors have.

¹ http://www.westpac.co.nz/assets/Business/Economic-Updates/2016/

| Sector | Trend | Current level1 | Next 6 months |

| Forestry | Prices have held up surprisingly well, but we don't expect this to persist as international supply responds and Chinese demand moderates. | high |

|

| Wool | Synthetic substitutes to remain attractive while oil prices remain low. | average |

|

| Dairy | Modest retracement expected in coming months after big lift in prices since mid-year. | average |

|

| Lamb | Uncertainty over demand in key markets to continue to weigh on prices. | below average |

|

| Beef | Prices to be underpinned by relatively tight supply in the near term, but downside risk further out. | above average |

|

| Horticulture | Benefitting from strong demand and productivity improvements. Further improvement expected heading into next year. | above average |

|

1. NZD prices adjusted for inflation, deviation from 10 year average.

This article was prepared by the full Westpac New Zealand economics team. Michael Gordon is the acting chief economist at Westpac New Zealand. This is the third chapter of their recent publication "November 2016 Economic Overview", and is here with permission. The first chapter is here. and the second chapter here. The next two chapters will be re-posted here, in turn.

9 Comments

The EU have begun to liquidate their stockpile of powder so future lifts could be difficult.

The problem is others are getting bloody good at getting cheap feed and Russia has a huge wheat crop and quality is down so lots more cheap animal feed.

The UK can import feed cheap from Argentina. I don't see an easy way forward for us but I am forever hopeful, well since the 80's anyway but no great light yet, still just the train in a tunnel. Eventually it will all be about the debt. Australia is worried about the size of farmers debt, which is not that much higher than ours when their exports are 5x as much and there are a lot more farmers in Aust..

https://theconversation.com/farmers-are-in-debt-and-more-debt-wont-help…

http://www.world-grain.com/articles/news_home/World_Grain_News/2016/11/…{D297F282-29C1-495F-BCB2-53A7902E3D2F}

http://www.world-grain.com/news/news%20home/LexisNexisArticle.aspx?arti…

Aussies have managed to increase food exports by $11B/annum since 2012, while iron ore did the opposite, so some of that farm debt was put to good use.

Beef prices have been at record highs and Aussie is the third biggest exporter in the world behind Brazil and India.

http://beef2live.com/story-world-beef-exports-ranking-countries-0-106903

Total annual beef production value is only $14B so that $11B increase has a lot more to it than high beef prices.

So wheres it coming from? Wheat prices are low, their dairy exports are not huge.

“The growth in the value of Australia's agricultural production was largely driven by an increase in the gross value of livestock disposals and products,” said Lauren Binns, Director of Rural Environment and Agriculture Statistics at the ABS.

http://www.abs.gov.au/ausstats/abs@.nsf/lookup/7503.0Media%20Release120…

http://www.abc.net.au/news/2016-03-01/abares-outlook-2016/7209506?pfmre…

Different time frames 16-17 vs. 12-15. 2017 value expected to pass $60B from your link. That is impressive growth from 2012. Hence my original point some of that debt has been put to good use not just inflating land prices.

Living in chains

Big, well-funded companies will be chosen to act as models for outbound investment, including companies in the Ministry of agriculture's industrialized leading enterprise program (virtually all major agribusiness companies), and enterprises affiliated with the state farm system (like Bright Foods, Beidahuang, and Jiusan). The plan encourages Chinese enterprises to establish agricultural production, processing, storage and transportation bases outside the country’s borders to create global agricultural industry chains.

http://dimsums.blogspot.com.au/2016/11/china-prepares-for-outbound-ag.h…

All is well is dairyland. I heard that cows down South are being quoted at $2000-2400/cow, 2yr olds $1500-1700, and 1yr olds $1000. When asked if the buyer thought these prices were high, the young man looking to buy his first herd said, 'no, there's a shortage of dairy cows'. I wonder which bank is funding him.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.