By David Hargreaves

ANZ's economists are warning the Reserve Bank against any early, overly pre-emptive strike against anticipated inflation.

In a preview of December quarter Consumers Price Index figures due to be released by Statistics New Zealand on January 26, ANZ senior economist Philip Borkin says inflation pressures should continue to gradually build over 2017.

ANZ's picking 0.3% inflation for the December quarter, which is above the RBNZ's pick of 0.2%. The ANZ is further picking annual inflation to lift to 1.2%, which would get it back into the RBNZ's targeted level of 1%-3% for the first time since the third quarter of 2014.

"Deflationary influences are certainly still present (NZD, technology, competitive retail environment etc), which will ensure inflation doesn’t run away," Borkin says.

"But these factors are expected to be increasingly usurped by traditional demand-pull forces and the simple mechanics of falls in oil (petrol) prices being replaced by increases.

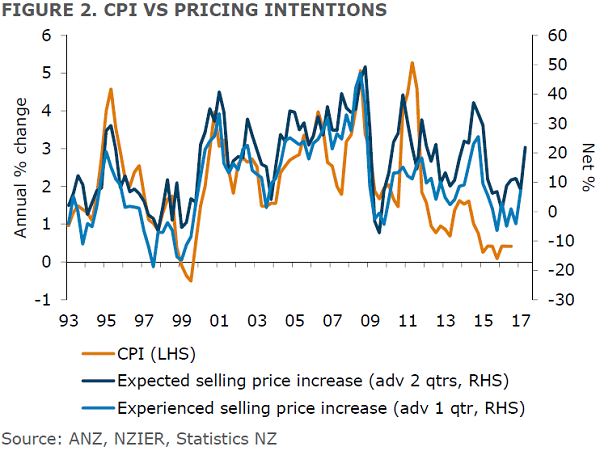

"Inflation has been a missing element of the expansion to date, but evidence is building (rising firm pricing intentions, positive output gap, tighter labour market, stronger global inflation etc) that it is now starting to return. The Q4 inflation figures will be a step in that direction."

But then comes the cautionary note.

"However, that doesn’t necessarily suggest that the [Official Cash Rate] should follow inflation upwards in quick succession," Borkin says.

"Given two false starts to tightening since the financial crisis, the hurdle for lifting the OCR should be high.

"The RBNZ needs (and will likely want) to see the whites of the eyes of inflation before tightening, rather than risking taking another pre-emptive strike that eventually proves unwarranted."

As Borkin says, after dropping the OCR to a then record low of 2.5% in early 2009 in response to the effects of the Global Financial Crisis, the Reserve Bank has twice started tightening cycles that have subsequently needed to be aborted.

In both June and July 2010 it lifted the OCR by quarter of a percentage point, and then reversed this in a single 50 bps drop in March 2011 after the second of the Christchurch earthquakes.

Then there were four 25 bps hikes in the first half of 2014, which began being reversed a year later. The OCR now stands at just 1.75%.

In terms of the expected inflation outcome next week, Borkin says higher petrol prices and base effects largely account for the lift in annual inflation.

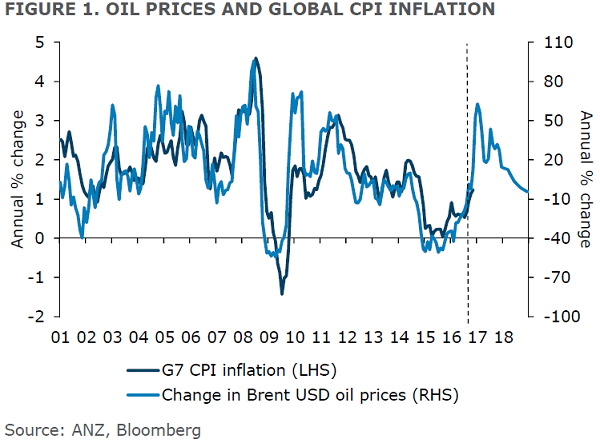

"Retail fuel prices are estimated to have risen by 5% over Q4, in stark contrast to the 7% drop seen in the same quarter a year earlier. This results in a mechanical bounce in annual CPI inflation. New Zealand is not unique in this phenomenon; headline inflation is rising globally as oil prices stabilise after the late 2015/early 2016 falls."

Borkin says that more importantly, there should be further evidence of a turn in the domestic inflation cycle.

"While non-tradable inflation, at an estimated 0.5% q/q (2.3% y/y), is still low historically, it is trending higher and we see risks skewed to a modestly stronger outcome in Q4. Our Monthly Inflation Gauge is hinting at price increases beyond just housing, which is consistent with growing capacity strains across the economy."

Borkin says that tradable inflation should remain soft, however, at -0.1% q/q and ‑0.5% y/y.

"While still negative, this would represent the highest annual tradable inflation since Q2 2014, largely reflecting petrol prices. Outside of petrol, tradable inflation is expected to print at -0.7% q/q (-0.5% y/y)."

26 Comments

Conversely:

"The RBNZ needs (and will likely want) to see the whites of the eyes of inflation deflation before tightening loosening, rather than risking taking another pre-emptive strike that eventually proves unwarranted."

(David Rosenberg, who had the flexibility to correctly switch from bearish to bullish some years back and has switched again! Will he be right again?)

"The economy isn’t that strong, and anyone who thinks one man can reverse, on his own, the structural forces that led to the multi-year disinflation trend — and I’m talking about excessive debt, globalization, aging demographics, and technology — needs to go back to economics school right away."

Agree. The fundamentals haven't changed, the system is still broken.

Other than a blip here and there we shouldn't see much change/recovery.

.

YES YES YES I completely agree with you, I keep saying the same. The world economy has not recovered from the GFC, all that has happened are band aid policies that have not dealt with fundamental problems. I'm so convinced of this that I have fixed several mortgages for 1 year at 4.15% because I don't buy the sustainability of the interest rate rise trend despite everyone saying the rates will keep going up & up

Count me in on this, the GFC has just been deferred, and that can't last.

The new paradigm: the RB OCR follows the banks rather than leads.

When was it never thus.

The RBNZ is one of many factors that determine domestic bank interest rate structures.

Moreover, it is clear that a falling OCR is not positively correlated with narrowly defined rising CPI Inflation indices. Evidence to date certainly demands the RBNZ self imposes a cease and desist order until it can determine what is correlated with a lower official rate other than wealth transfers into rising leveraged asset values funded by risk exposed savers and taxpayers alike.

Just remind me ........... who was it , a year ago, that was remitting spectacular dividends from record profits back to their Australian parent Companies ?

My memory is pretty bad,so can someone remind me who is paying these economists wages.

More warnings from the paid prophets of the ANZ .

Boatman - Their returns are about average amongst the top 100 of companies on the NZX. So I assume that many of those other companies are also paying dividends to their shareholders (who fund those companies that provide those services to the NZ public) as well ? Why are they so special in that regard, or are you just confusing a massive investment capital into NZ by the banks with a large profit number ?

The Aussie banks are so special because they provide the mechanism of house price inflation that drives the NZ economy. The other companies on the NZX are involved in the production, distribution and consumption of goods and services.

Without the constant pressure of cheap money to finance the speculative purchase of glorified chicken shacks the NZD would be low enough for us to earn a good living from trade. As it is we are the subjects of a global, bank driven decline into debt serfdom. Perhaps I go too far, but certainly the banks are key enablers of our seemingly insatiable desire for a self destructive, debt funded lifestyle, both as individuals and as a country.

Is this as good as it ever gets from the Fed?

“The good news is that, while the current expansion is quite old in chronological terms, it is still relatively young in terms of the health of household finances,” Dudley said in a speech to the National Retail Federation.

“Whatever the timing, a return to a reasonable pattern of home equity extraction would be a positive development for retailers, and would provide a boost to economic growth,” Dudley said.

Homeowners may have overlearned the lessons from the housing boom and bust, the New York Fed President said.

Even though home values have risen over 40% since 2012, housing debt has stayed virtually flat, he said.

“The previous behavior of using housing debt to finance other kinds of consumption seems to have completely disappeared,” and people are leaving the wealth generated by rising home prices “locked up” in their homes, he said. Read more

I thought citizens were done with financialisation as a substitute for work related income?

At the peak in 2000, calendar year factory orders were $4.16 trillion. Three years into supposed recovery, factory orders in 2004 were still less than $4 trillion. It wasn’t until the sharp rise in 2005 that the factory sector finally appeared to put what was really a mild recession behind. But manufacturing in the US wasn’t ever the same.

While the US economy was ostensibly in recovery 2002, 2003 and 2004, it was mostly if not all from the “demand” side of the equation. It was during those years where the largest exodus of manufacturing jobs in history was witnessed. Whether or not you believe Ross Perot was correct in his “giant sucking sound” prophecy, there is no doubt that there was some good correlation between the loss of those jobs during those years and what to many was not a recovery; and even in economics, there was a great deal of agreement that economic function during that time was highly unusual.

That is what led policymakers toward embracing the lunacy of the housing bubble in its final stage. In one sense the one led to the other, or at least allowed it to happen. By that I mean the huge buildup in debt was that “demand” side that essentially paid, at the margins, for those goods to be produced overseas. It was the substitution of finance for income; mortgage and consumer debt for the labor lost in manufacturing jobs and production. Read more

Aussie bank returns are certainly not "about average"

Their return on equity is about 18.6% compared to an OECD average of 9.2%

A utility in NZ such as Transpower, which arguably has more business risk than a bank, has a regulated return to equity of no more than about 11% before tax.

A return of 18.6% enables banks to fund credit growth at a high 8% at the same time as providing a gross dividend yield of 7.5%.

A countercyclical buffer on the bank's capital reserve should have been put in place by now to normalise their excessive returns and reduce rampant credit growth.

.

Vested Interest

I wonder when we'll see an article about the new investor premiums that BNZ customers now have to pay. 25bps over and above retail rates. Part of the capital challenges banks now have due to the RBNZ. Have just been released and is disclosed on their rates page. Couple of clients have come to me disgusted when they found the best 2yr rate they could get was 5% despite having very low LVR's.

Good info thanks.

I have just been offered the following rates by ANZ:

Fixed - 1 year | 4.75 | -0.60 % | 4.15

Fixed - 3 years | 5.29| -0.60 % | 4.69

Fixed - 5 years | 5.60 | -0.40 % | 5.20

4.69% for 3 years is a lot better than 5%+ for 2 years

If you got in before yesterday, that would have looked a bit better.

We got 2yr 4.29, 3yr 4.49, floating 5.00 from ANZ a few days ago. Switchers from ASB so maybe extra incentives there.

Yup BNZ just puts this .25 money grab in and doesn't even bother to tell their customers. When mine comes up for renewal will put my portfolio out to bid, short sighted move by BNZ

Was at a Reserve bank breakfast before Christmas and the Governor was asked was the OCR redundant as the banks were not following through with OCR reductions. The Governor talked all around the question and didn't give any significant answer. Obviously there is a problem.

The short answer to the problem is that the banks can't and don't fund off the OCR, its merely a guide from the RBNZ - they fund off what they have to pay local depositors (well over the OCR because the banks are currently having to compete with "you can't lose" rental housing investments that seems to be the only investment that mums & dads understand), and what rate they have to fund the balance offshore at (very much higher than the OCR) - so the correct answer currently is, yes, the OCR for the moment is irrelevant, and the RBNZ knows that better than anybody. Deposit rates need to be higher still to attract funding back, and until that time comes (not this year I suspect) forget the OCR as being relevant to anything.

Previously the banks have been complaining about the 'rising offshore wholesale rates' as their reason to maintain/raise rates. Now, apparently, its a local funding problem.

Perhaps the banks would be best to show more transparency and show customers the entire value chain from the pools/mixes of wholesale funding & local funding, and short term & long term funding so borrowers can see the margins easier.

The short answer to the problem is that the banks can't and don't fund off the OCR, its merely a guide from the RBNZ - they fund off what they have to pay local depositors (well over the OCR because the banks are currently having to compete with "you can't lose" rental housing investments that seems to be the only investment that mums & dads understand), and what rate they have to fund the balance offshore at (very much higher than the OCR)

Cmon - the biggest funding category by far is the O/N segment ($149.569 Billion) and ANZ pays max ~10bps for larger amounts in the online and select adult categories. One month edges up to 65bps

Yup 3,4,5,yrs ago it was a offshore funding problem, but guess what happens when NZ borrowers get record low mortgage rates, NZ savers revolt - now you're going to pay a higher price until they're happy again to fund you through the banks - barring that the banks will limit lending, and reluctantly top up their funding from offshore sources (although limited because of their prudential core funding ratio requirements) which is even more expensive for you - facts are, market conditions change all the time, and you learn about that from reading the likes of market commentators research, and indeed even the banks themselves financial reports.

NZ savers revolt - now you're going to pay a higher price until they're happy again to fund you through the banks

Where did they revolt to?

S7 ~= S6 + S1 (Section A3.3 Total)

Looks ~ balanced to me.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.