Here are the key things you need to know before you leave work today.

MORTGAGE RATE CHANGES

ASB has lowered most of its fixed mortgage rates, except its hot one year rate which it raised to 4.45%. The reductions for longer terms were all -10 bps. More details here. Sovereign made identical changes.

DEPOSIT RATE CHANGES

We mis-reported yesterday's NZCU Baywide term deposit changes. It was their 18 month rate that rose to 4.15%, and not their 12 month rate as we originally reported.

OF RICE AND TULIPS

Yesterday we [breathlessly] reported that the bitcoin price had touched US$14,100 before falling back. That is old news. Today it rose over US$17,000 but is now at US$16,857 and that is NZ$24,500. Most people have heard of the rice and chessboard fable. Perhaps bitcoin's growth is going down those lines? From January 1, 2015 the bitcoin price started at US$314 and then doubled in 529 days. Then it doubled in 322 days. It doubled again in 44 days, then slowed down to double yet again in 121 days reaching US$5,440 on October 12. It then doubled in 50 days to US$10,860 by December 1, 2017. Seven days later it is up another +70%. Maybe the next doubling will be by Tuesday?

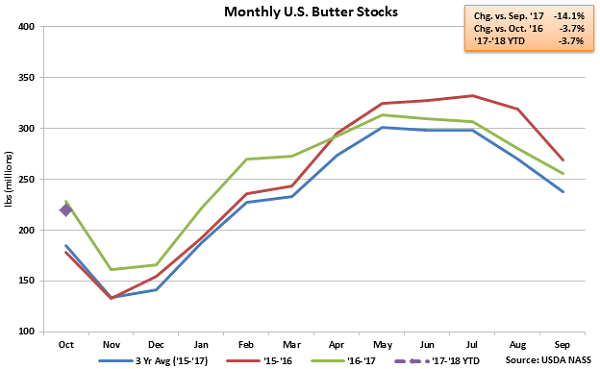

ARBITRAGERS MIA

They may be standing in queues in Paris waiting for more butter supplies to arrive, but butter prices on this side of the world are falling, and quite sharply. Today's USDA review of Oceania pricing reflects a substantial fall, down -22% in nine weeks in USD terms, down -18% in NZD terms. Cheddar cheese is falling too, although not as fast. Commodity SMP and WMP are holding however.

PUSHING AN UPSIDE

Higher sales volumes for chemicals and plastics producers helped lift manufacturing in the September 2017 quarter, Stats NZ reported today. Overall sales volumes rose +8.6% from the same quarter in 2016 although the pace of this gain is less than the +9.4% in the June quarter. This is one of the components for the Q3 GDP result which analysts are expecting a +2.6% outcome, but today's component might give it a lift.

WHERE FAMILIES GATHER

New Zealand is projected to have over 2.2 mln households in 2038, 500,000 more than now, according to a new official update. The medium projections show the country will have more households in every region, city, and in most districts. One interesting view in this data shows Auckland as the 'family' capital of New Zealand. This city has a larger proportion of families than any other, and while that is currently just over 75% of all households, in 20 years time that ratio is expected to only fall to just under 75%. The level is lower everywhere else, and falling much faster. (On the West Coast, families only make up about 62% of households; the NZ average excluding Auckland is 69%.)

INCOMES UNDER-REPORTED

New Zealand's average household incomes were reported lower than they actually are in an error made by Stats NZ. They fixed that error today. Average household income from all sources is actually $107,759 per year, and the median from all sources is $86,392 pa. These numbers are +$5,962 or +6.0% more as at June 2017 than were originally reported. This update means that 'only' 7.4% of people who own houses spend more than 40% of their incomes on housing, and 18.3% of renters do that. (However, those that spend 40% or more of their income on housing generate 100% of the discussion.) Even more interestingly, ten years ago those two numbers were 7.9% and 18.2%. So in fact, housing cost pressure on households has not increased in the last decade.

DEAL ENDS

NZCU Baywide has ended its personal loan 'special'. That 8.9% promotional rate has now reverted to 9.9%.

WHOLESALE RATES UP & DOWN

Swap rates rose +1 bp today for all terms 2 years to 10 years. The 90 day bank bill rate slipped to 1.89% and that is an all-time low.

NZ DOLLAR SLIPS

The NZ dollar is lower at 68.3 USc. On the cross rates we are unchanged at 91 AUc and 58 euro cents. The TWI-5 is now at 71.4. If you normally check the bitcoin price here, look up to para #3 today.

You can now see an animation of this chart. Click on it, or click here.

Daily exchange rates

Select chart tabs

14 Comments

I might have missed it but I have not seen any comment on why NAB had to pump another $1.1bn into BNZ yesterday via an equity raise. Any ideas?

Caught out using Westpacs capital models?

So in fact, housing cost pressure on households has not increased in the last decade.

That is a spurious claim if you ask me. Housing cost pressures have probably not increased for those who owned houses in 2007 (as an aggregate anyway). For those people in 2017, who are buying houses "for the first time", the pressure would have increased immensely, despite the rise in incomes over the same time period.

While interest rates are low, housing cost pressure remains low. The biggest hurdle for FHB purchasing is the size of the deposit.

While interest rates are low, housing cost pressure remains low. The biggest hurdle for FHB purchasing is the size of the deposit.

Depends how you define housing costs. Debt servicing is just a component. The primary components are the deposit and debt to be repaid. Low interest rates are a nudge for people to borrow and to borrow as much as possible, therefore low interest rates can drive housing costs.

I know interest rate prediction is hard right now but you can’t look at debt costs based on record low interest rates.

If the French just rolled over and ate any old butter , stopped selling it at a profit to Germans, shelves would be full.

https://secure.attenbabler.com/wordpress/wp-content/uploads/2017/11/Mon…

{kind=link}

Our 21 Century tulip bulb bubble is something called Bitcoin .

The youngsters in our office ( all graduate professionals mind you ) tell me this is the next big thing , a currency that is freely traded everywhere .

But , here is my issue with it ...........even if it is NOT a Ponzi scheme , as long as bitcoin remains this volatile, it's useless as a currency.

Quite useless , and it will crash

It is volatile. It crashes all the time. Back to where it was a few weeks ago.

I expect the price to stabilize over time.

a looong time... actually replace the word long with this clip https://www.youtube.com/watch?v=SkgTxQm9DWM and you will see the scale of long we may be looking at.

"freely traded everywhere" I think they need to look up the definition of 'freely traded' and everywhere. Unfortunately with Bitcoin there is a lot more ticket clipping than credit cards, (and a lot more issues with making payments especially for micro transactions or even just transfers). Once they have the severe transaction time and energy cost issues ironed out and the extremely high volatility then there may be a sweet spot. But even the edge development (even the lightning developers) are talking on a scale for years for that to happen if at all, (it is likely not all currencies will survive, I am looking at you kitties). Meanwhile Bitcoin futures trading are opening up, low/no fee sale in December, payment guarantees available. Why not treat the speculative asset as it is if you have the money to burn. Most governments will be incredibly slow at updating laws, offering regulation, consumer protections and tracking so the party may last for a while yet for speculators. Betting for or against it with the high volatility can offer good gains or steep losses either way. Many of the youngsters in your office would likely have spent that much on concert tickets, new devices or games so gambling with the cash is probably just as fruitful if not more for them anyway. It is a good lesson for the future (after all it is not like there is compulsory financial education in schools so where else would they have to learn).

That NIWA chart!!

Difference in El Nino and La Nina? The worlds hot water & wetter weather sloshing back to meet us every few years then moving away again. So things are heating up and become much dryer now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.