What is the neutral Official Cash Rate (OCR) in 2018 and why does it matter?

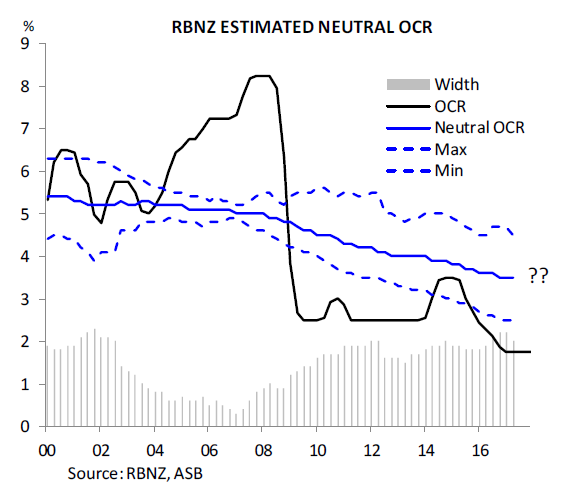

We last heard from the Reserve Bank on this topic more than a year ago, with the central bank giving an estimate of 3.5% amid a range from 2.6% to 4.6%. But some economists are now suggesting the neutral OCR is lower than this.

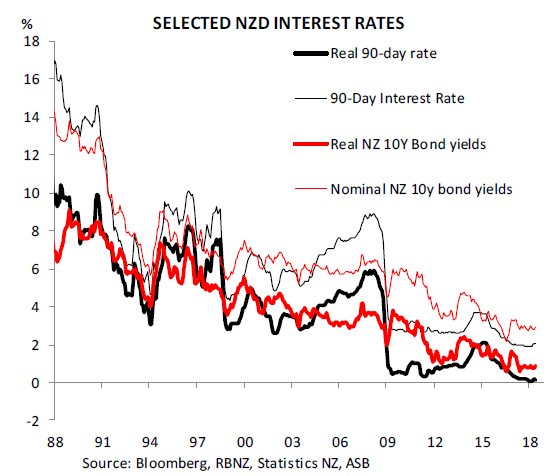

The neutral OCR is the level at which the OCR is neither stimulatory nor contractionary for the economy. Thus it forms a key anchor for the economy. Based on a neutral OCR of 3.5%, the OCR set above 3.5% would signal tighter monetary conditions and a central bank attempting to take heat out of the economy and inflation. Conversely, an OCR below 3.5% is viewed as stimulatory for the economy and inflation. Thus the current record low 1.75% OCR is stimulatory.

As BNZ interest rate strategist Nick Smyth puts it; "In an idealized world, when the OCR is at neutral, growth should be about trend, the output gap zero and inflation stable at target."

ASB's economists estimate the neutral OCR is now just below 3%, compared to around 5% at the start of the decade. This suggests the OCR at 1.75% could be providing less policy stimulus than is assumed by the Reserve Bank. Additionally, the ASB economists say the neutral OCR could potentially fall further with important implications for savers, borrowers, investors and policymakers.

"Our new estimates suggest the neutral OCR is currently in a 2.5% to 3.5% range, and could well head lower from here in the next few years. Structurally lower interest rates will have widespread implications," ASB's economists say.

Below are the implications ASB's economists see for borrowers, investors, savers, hedging risk and policymakers if the neutral OCR falls further.

Borrowers - All else equal, improved serviceability will support asset prices at the margin. This does not mean that asset prices should necessarily be higher than they are at present. The outright level of the asset relative to underlying fundamentals – incomes and income expectations and serviceability – matters. Borrowers also need to be mindful that a low inflation environment means that it will take longer for debt levels to erode in inflation-adjusted terms.

Investors - A lower real interest rate, all else equal, will help facilitate more demand for capital and potentially more substitution (where possible) of labour for capital. More capacity-enhancing investment is a key pre-requisite for prolonging the current economic expansion. Arguably, capacity constraints are currently weighing on the expansion, and our work previously highlighted weak business investment post the GFC as being a primary contributor to the slowdown in NZ trend productivity growth.

Savers - The return to a 5%+ bank deposit rate looks some way off. Low inflation makes saving go that much further and savers should focus on inflation-adjusted returns. Savers seeking higher deposit rates will also need to recognise the potential trade-off between risk and return. There may be the temptation to chase higher yields on offer from less secure investments, but the meltdown in NZ finance companies around the time of the GFC illustrated this is not without some risk.

For hedging risk - A lower neutral rate does not necessarily mean that interest rates will not eventually increase. Indeed our latest forecasts have both the OCR and wholesale interest rates moving up, albeit gradually. There is still value to be had in hedging given that it helps to mitigate risk and can assist in controlling costs.

Policymakers - Structurally lower neutral interest rates suggest that the OCR at current levels is unlikely to be as stimulatory as was historically the case. A lower neutral rate may also mean that the extent of eventual RBNZ tightening needed to contain inflationary pressure will also be milder than past episodes. If the decline in the neutral interest rate is linked to lower potential rates for economic growth then there are broader implications for fiscal settings and wider government policies.

And where do other economists place the neutral OCR?

Kiwibank chief economist Jarrod Kerr says he has long put the neutral OCR at 3%.

"Even as the RBNZ has moved from estimating 4% to 3.5%, there’s a clear leaning towards 3%. We are in a different world, compared to 10 to 20 years ago. That simply means the current OCR setting of 1.75% is accommodative, but not as accommodative as the RBNZ once thought. And that’s evidenced in the lack of inflation," says Kerr.

In a June report BNZ's Smyth suggested the risks around the Reserve Bank's estimate were to the downside.

"If funding spreads remain elevated, it’s not difficult to envisage a 3% neutral OCR or even a neutral rate closer to 2.5% (which, to be fair, is still within the range of neutral estimates from the RBNZ, albeit towards the lower end)," said Smyth.

"Another way of coming to the same conclusion would be to compare the RBNZ’s 2015 estimate of the neutral floating mortgage rate, of 7%, to the current floating mortgage rate of 5.75%. At face value, this gap implies floating mortgage rates are 125bps below this estimate of ‘neutral’, which would translate to a neutral OCR of 3% (i.e. 1.75% + 125 basis points)."

ANZ's economists last year estimated the neutral OCR at 3%.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

12 Comments

"Is the neutral OCR lower than where the RBNZ believes it to be?"

YES

So ASB's owners the Commonwealth Bank of Australia think that the neutral rate of the OCR should be lower than it's ever been throughout the history of NZ interest rates (exception being the last several years of loose policy). Interesting.

YES

Just looking at the last decade of our Great Stagnation, yes. The OCR is a cost and not a % in a way. As an explanation pre-2004 oil was a small % of GDP it was cheap and hence did not impact GDP growth (using the USA or globally as an example). By 2008 it was crippling growth and even turned us into a great recession just like a too high OCR would do.

So my suggestion is the neutral OCR rate is an amalgamation of some other numbers and the OCR is one yet the others get ignored, (directly anyway).

Ergo 2.5% is too high globally if not for NZ might even be <1% as a consequence of these other factors eating into growth.

I think we have or are entering an era where the OCR is ineffective and obsolete as a useful tool beyond it being capable of doing damage to our economy.

I'm not sure about "the last decade of our Great Stagnation", I have 3 businesses and all 3 have expanded remarkably well over the last decade

As BNZ interest rate strategist Nick Smyth puts it; "In an idealized world, when the OCR is at neutral, growth should be about trend, the output gap zero and inflation stable at target."

We're no too far off now at 1.75% then

What an unfortunate name, undermining impressions of one's confidence. He must hold no affection for Nick Smith.

very probably.....though just how low it should be I wonder on.

20 years ago....the OCR didn't even exist! What on earth did we do before that; how did we survive at all without it!

Answer: The RBNZ managed the amount of cash in the system via a regular (weekly) schedule of Treasury Note auctions. The RBNZ had a hands-on approach to The System that has bee abrogated (everywhere!) to the Private Banks in a way that it has never been done before - and look at what a mess they have made of it!

Scrap the OCR; Scrap Inflation Targetting and get back to Liquidity Management, RBNZ. You should run the NZ financial market economy - and you very clearly don't...

End the Fed, I mean... end the RBNZ.

Yet over the many decades such have existed they have managed to improve the stability of our financial system/economy.

as long as you ignore the huge asset bubbles.

https://www.youtube.com/watch?v=EC0G7pY4wRE

and all the inequality

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.