By David Hargreaves

The Reserve Bank has lightly poured cold water over expectations that interest rates my be hiked as soon as next year by saying that its own 'core' measure sees inflation running at around just 1.4%, while it now views current interest rate levels as less 'stimulatory' than it previously believed.

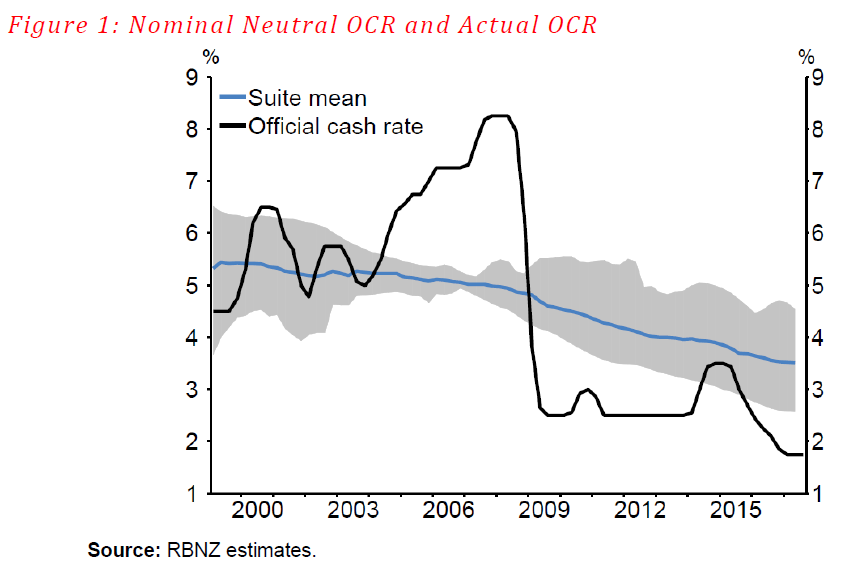

The RBNZ now estimates the 'neutral interest rate', at 3.5%, from above 4% previously. As recently as two years ago, the RBNZ estimated the 'neutral' rate at 4.5%.

Economists saw the comments, made in a speech on Wednesday by RBNZ Assistant Governor and Head of Economics John McDermott, as indicating that the RBNZ would be in no hurry to raise interest rates.

McDermott also made reference to the high level of the New Zealand dollar (currently above US74c) and indicated that the central bank wanted to see it lower.

Essentially, by tweaking down its view of what 'neutral' interest rates are, the bank is saying that monetary conditions in this country are less stimulatory than the RBNZ previously thought - something major commercial bank economists have been suggesting for some time.

Additionally, a 'core' inflation rate of 1.4%, while within the RBNZ's official targeted range of 1%-3% is still below the explicit target of 2%.

Official inflation figures had been outside the RBNZ targets for a long time, but roared back within the range early this year after some sharp rises. However, these rises are being construed as largely one-off in nature.

Last week's official inflation figures were much lower than the RBNZ had been predicting and suggested that during the course of this year the annual inflation figure will fall sharply again.

McDermott said the RBNZ's own 1.4% estimate of 'core' inflation, (which excludes variable impacts such as oil price movements), "has broadly tracked sideways over the past year".

"So while inflation pressures have lifted from the lows seen in early 2015, they still appear to be relatively moderate"

The 'neutral' interest rate is a theoretical, but nevertheless important figure since it guides the RBNZ's view of whether or not current official interest rates are 'stimulatory' or not.

At the moment, based on a 'neutral' interest rate of 3.5%, this means that any Official Cash Rate set above 3.5% would be signalling tighter monetary conditions and a central bank attempting to take heat out of the economy and inflation.

Conversely, an OCR below 3.5% would be seen as stimulatory for the economy and inflation.

Our current OCR - at 1.75% is therefore 'stimulatory' - though not as stimulatory as if the neutral rates was assumed as say 4.5%, the level the RBNZ had it at two years ago.

McDermott indicated that the new 3.5% 'neutral' estimate would now be incorporated into future RBNZ projections.

Westpac senior economist Satish Ranchhod said putting this "relatively moderate inflation picture" painted by the RBNZ together with interest rates settings that aren’t as stimulatory as the central bank had previously expected, "and we’re left with an environment where the RBNZ won’t be in any rush to hike rates".

"We’ve been noting recently that the financial market pricing for RBNZ hikes from around mid-2018 is too soon, and today’s speech reinforces that view," he said.

10 Comments

Doubt we'll see much of a move until 2020.

Does OCR and mortgage rate still move together in the same way in NZ?

No. They never really have.

Research shows floating rates and fixed terms up to 2 years correlate to NZ OCR. 3-5 years rates correlate to US swap rates.

There you Go, ..all the immigration and house price pressure is not making a dent in inflation ... all the good news keeps coming in for the doom and gloomers

this just in: June trade surplus $242 million, boosted by dairy exports

Its party time .. enjoy it while it lasts

Thanks Eco Bird, party time all right all this success, we Win. Now I am going to splash out with my big wages increase.., hang on just checking my increase, back in a moment once I find it..viola $2 bucks ..WIN

3.5%? Either very optimistic or it's taken a long time for RBNZ to adjust their forecast towards reality.

"The RBNZ now estimates the 'neutral interest rate', at 3.5%, from above 4% previously"

Ridiculous, far, far, far too slow to adjust to the real world. I suggest "neutral interest rate" of 2.0%

Sorry I couldn't resist pasting my comment of January 2017 when everyone was saying "higher interest rates are imminent"

"I believe my dog has even odds as the economists do, of calling the interest rates correctly in 2 years time"

At the moment, based on a 'neutral' interest rate of 3.5%, this means that any Official Cash Rate set above 3.5% would be signalling tighter monetary conditions and a central bank attempting to take heat out of the economy and inflation.

Conversely, an OCR below 3.5% would be seen as stimulatory for the economy and inflation.

Our current OCR - at 1.75% is therefore 'stimulatory' - though not as stimulatory as if the neutral rates was assumed as say 4.5%, the level the RBNZ had it at two years ago.

McDermott indicated that the new 3.5% 'neutral' estimate would now be incorporated into future RBNZ projections.

Complete and utter hogwash.

So don’t worry about the federal funds rate, the monetary corridor or actual rate increases across all the money markets, rather we should instead focus all attention on some mythical rate that doesn’t actually exist in anything outside orthodox DSGE models that haven’t assumed the correct monetary position since before the “missing money” of the 1970’s? My response to that is simply that there are times when it takes so very little actual effort on my part to write “they really don’t know what they are doing.” At least in the 1970’s the Fed and economists made great effort to try to bridge that theoretical gap and seriously study the wholesale banking revolution in the context of potential monetary conditions.

Now? “Trust us.”

As it is, we seem to be revisiting Governor Holland’s open suggestion from 1975, with slight revisions for our current circumstances. “A policy of monetary expansion”, such as ZIPR and QE, “might have less predictable effects on expanding credit in the United States and might be rendered less effective if” US and now global banks were stained with misunderstood, if not unknown (to economists), monetary decay by which money markets would be highly attuned. Vice Chair Fischer wants us to believe that his monetary policy views can even define, let alone measure, some “neutral” economy-wide interest rate when the same policy body has taken no interest in money for decades. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.