*This article was published in our email for paying subscribers. See here for more details and how to subscribe.

10 Comments

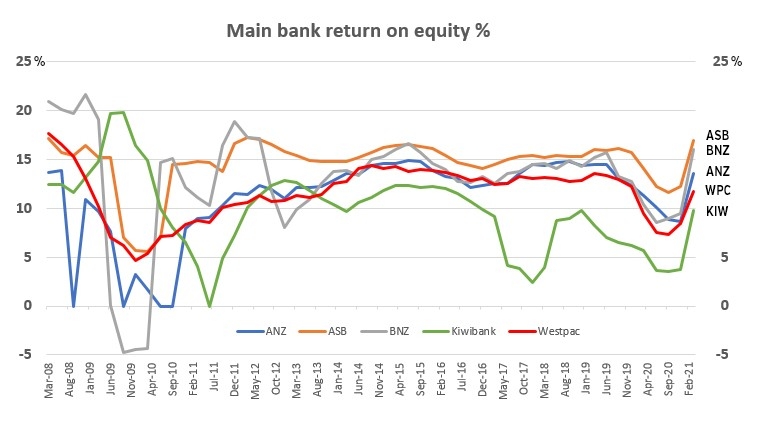

This graph is so depressing. There is a real economy somewhere that nobody talks about anymore - an economy where people innovate and produce things of value and utility - products and service that actually improve people's lives and save people time. Sadly this real economy gets little attention because the world is hooked on the FIRE economy (finance, insurance, real estate). The FIRE economy is fake - it adds no value; it's only purpose is to extract value from the real economy and channel the wealth extracted from people and resources to the few.

Jfoe,

You're right, it is depressing. When the RB announced the Funding For lending programme, I thought-naively- that it would only be available for lending to the productive economy, but I understand that most of the capital taken up by banks has gone to the property market.

As a country, we appear to be sleepwalking towards a cliff edge-are we already over it?

Hmmmm... Say It Ain't So

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%.

Thus around 60% of NZ bank lending is dedicated to residential property purchases for one third of already wealthy households because the RBNZ offers them a RWA capital reduction incentive, to do so.

{kind=link}

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $307,871 million (63.13% of total lending) as of April 2021.

NZ bank depositors face more risk for virtually nil rewards while banks reap obscene profits with virtually no capital risk exposure.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Quote by a famous person....about a hundred years old but stands the test of time:

'It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.'

https://external-preview.redd.it/RgyHCBthx-95yHuiTxnE9MIO6MFjlF9C0lLlz3…

{kind=link}

Amongst a fairly complete list of RB governance failures, this one is the hardest to smell. My gag reflex is full activated on seeing that graph. Banking in NZ is a noncooperative oligopoly -

Typical assumptions for oligopolistic markets.

1. Consumers are price takers.

2. All firms produce homogeneous products.

3. There is no entry into the industry.

4. Firms collectively have market power: they can set price above marginal cost.

5. Each firm sets only its price or output (not other variables such as advertising).

Summary of results on oligopolistic markets.

1. The equilibrium price lies between that of monopoly and perfect competition.

2. Firms maximize profits based on their beliefs about actions of other firms.

3. The firm’s expected profits are maximized when expected marginal revenue equals marginal cost.

4. Marginal revenue for a firm depends on its residual demand curve (market demand minus the

output supplied by other firms)

http://www2.econ.iastate.edu/classes/econ501/Hallam/documents/Oligopopl…

Are they releasing provision too early?

Well doh. It's called the wealth effect.

I'm patiently waiting for my trickle down

lol, that trickle ain't water friend.

The cynic in me thinks: Was the government and RBNZ protecting the banks with most of last years actions by ensuring they can maintain or improve their ROE? Rather than working for the people of NZ, they were working for the banks?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.