By Patrick Watson*

The logic of Donald Trump’s multi-front trade war, if there is any, is increasingly obscure. The tangled mix of policies isn’t accomplishing its stated goals and seems unlikely to ever do so. Meanwhile, it hurts the Americans it should supposedly help.

Regardless, it’s happening, and it has consequences… none of them good.

The president’s latest move to impose escalating tariffs on imports from Mexico is the trade equivalent of “going nuclear.”

Judging by his tweets, Trump thinks it will solve multiple problems: trade, drugs, immigration, and crime. That’s doubtful at best. But as with real nuclear weapons, the blast wave isn’t going to discriminate. It will hit everyone.

If you think the trade war hasn’t affected you yet, brace yourself. You’re about to feel it.

Photo: Nick Youngson/Alpha Stock Images

Tariffs raise prices

A tariff is a form of sales tax on imported goods. The importer has to give the government cash, then recover it by charging more when it resells the goods, accepting lower profit margins, or some combination of both.

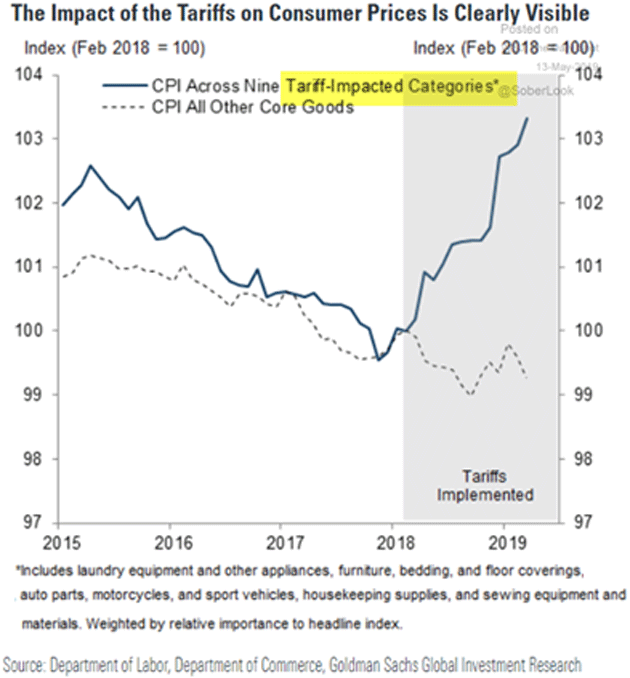

So far, President Trump’s tariffs are showing up as higher inflation. It’s not obvious in the broad inflation measures like the Consumer Price Index because only a few goods have been affected. But in those segments, the impact is clear.

Goldman Sachs recently compared price changes in nine tariff-impacted CPI categories vs. those that weren’t. Since the first tariffs in 2018, an index of those categories rose more than 3%. Meanwhile, all the other core goods categories showed a slight decline.

Chart: The Daily Shot

This impact is about to spread. The president is raising tariffs on almost all Chinese goods and is threatening the same for Mexico.

Again, we won’t necessarily see this in retail prices right away. But if we don’t, it will be only because merchants have stockpiled inventory or decided to absorb the cost out of their profits.

If it’s the latter, it’s still not good. Companies with shrinking profit margins usually try to recover them somehow, like laying off workers or postponing expansion plans.

Consumers will certainly notice if the latest tariff increases persist more than a few months. Top retailers depend on Chinese and Mexican goods. Those prices will probably rise.

That might actually please the Federal Reserve, which has been despondent over its inability to hit its 2% inflation target. At some point, they might raise interest rates to counter the inflation pressure, but I think they’ll let the economy “run hot” for a while first.

This might actually stimulate some activity as people try to avoid tariffs or find substitute goods. But mostly, we will see it as higher prices and lower disposable incomes.

But that will only be the beginning.

Photo: Nick Youngson/Alpha Stock Images

Damage ahead

Remember when politicians actually worried about government debt? I know, it’s been awhile.

We used to think high debt would cause inflation. That hasn’t happened, for reasons John Mauldin explained recently in “Why Debt Won’t Spark Inflation.”

Essentially, debt-fueled fiscal stimulus fades quickly to be replaced by weaker business conditions. Demand falls enough to keep consumer prices and interest rates from rising much, if at all.

Tariffs are similar in some ways. President Trump, at least, thinks he can make companies move production to the US and hire American workers, thereby stimulating growth.

That may happen a little bit, here and there. But it won’t be much.

The business leaders who make those decisions know full well that Trump’s unilateral tariffs may disappear when he leaves office, or maybe sooner if he changes his mind.

Few businesses are going to make major capital investments based on a whim that could change tomorrow. So initially, we will just get the higher prices.

In fairly short order, though, some US manufacturers will reduce output because the imported parts on which they depend are too expensive, thanks to the tariffs, and no alternate sources exist in the US.

Laid-off manufacturing workers will tighten their belts and reduce spending, hitting the retail sector and possibly making some stores close. Those workers will lose their jobs, too.

Then the same will happen in the farm states as Mexico and China shift their once-large grain and meat purchases elsewhere.

By that point, President Trump may see the light and change his mind. But the damage will be done. Business leaders will have seen what can happen. Their willingness to take risks and invest in new capacity will be lower.

Then we may see some highly leveraged companies default on loans that never should have been made in the first place. Lenders will tighten standards and starve even viable companies of financing.

The Fed may try to counteract this with rate cuts or QE. But if we’ve learned anything the last decade, it’s that monetary policy no longer has the same effects it used to.

All this adds up to one thing: recession.

Photo: Pixabay

Last straw

Now, we are overdue for recession even without tariffs. This (historically weak) growth cycle has to end eventually. If tariffs don’t trigger it, something else will.

But tariffs could easily be the last straw. This trade war could make the recession happen sooner, last longer, and cause more pain than it otherwise would.

What aggravates me most are the people saying we have to accept some pain in order to fix the problems with China.

First of all, there is zero reason to think tariffs will solve the problems. So we’ll get more pain but little or no gain.

Second, those who so cavalierly want other Americans to suffer tend to be wealthy, powerful people. They won’t lose their jobs. They have great health insurance and don’t have to worry about foreclosure and bill collectors. Those who actually are suffering will notice.

That being the case, this next recession could easily become more than a recession. People in pain do radical things. And those who caused that pain probably won’t like where it leads.

*Patrick Watson is senior economic analyst at Mauldin Economics. This article is from a regular Mauldin Economics series called Connecting the Dots. It first appeared here and is used by interest.co.nz with permission.

8 Comments

Yep I and many other would agree with you Patrick. Mr Trump is just blundering about not having a clue what he is doing: Article from the Express: Recession WARNING: US manufacturing PLUNGES to lowest level since financial crisis fallout

THE US economy saw manufacturing levels drop to their lowest rate since the fallout from the financial crisis in the latest sign the American economy is losing momentum.

Patrick - you appear well behind the (Energy) eight ball...

https://ourfiniteworld.com/2019/05/22/why-it-sort-of-makes-sense-for-th…

"We used to think high debt would cause inflation. That hasn’t happened, for reasons John Mauldin explained recently in “Why Debt Won’t Spark Inflation. Essentially, debt-fueled fiscal stimulus fades quickly to be replaced by weaker business conditions. Demand falls enough to keep consumer prices and interest rates from rising much, if at all."

You havent noticed Asset Valuations go up ? All that money supply goes somewhere. But it doesnt change the physics of net energy. Demand needs growing net energy. The economy is a game in how to maximise our energy use (ie turn resources into waste)

"Few businesses are going to make major capital investments based on a whim that could change tomorrow. "

Few businesses are investing in ANYTHING.

There is money everywhere and opportunity nowhere (aside from housing population ponzis / retiree pre-death resorts ) Noticed any share buybacks ?.

Interest rates track ever lower as money/debt continues to lose real value and debt is used as income. The next GFC erodes debt and income. Thats a big problem. In the meantime the US is acting in its own interests to devalue other currencies and prop the US$ up. Thats equals a better share of a shrinking energy pie.

You are forgeting that a lot of these companies cant relocate overnight.

Slapping tariffs on China means they immediately become less competitive. For instance a TV from China becomes 25% more expensive than what was the same priced TV from South Korea. Losing the competitiveness means less sales so the producer now needs to discount the price to the importer which comes directly off the profit margin.

Tariffs will hurt China as most of the goods they export are non essentials so they need to remain competitive.

So in reality Chinese firms pay the tariffs via discounting.

Patrick Watson, you should re-write your piece in a way so that a primary school kids can understand it and then email it to D Trump

And to everyone who was taught growth-forever economics.

I had a discussion with an econ Master's student the other day - whatever he'd chosen as papers he'd missed 'reality'.

Fair to say that economic analysis against DJT policy should be taken in the same light as the pre election coronation of Hillary?

"Rumours of my death have been greatly exaggerated"

People have been saying a recession is just around the corner for about 8 years now.

Knowing what to look for, makes it easier. Firstly, the only correct interest-rate going over the peak, is zero. Beyond that, it's got to be negative. If rates continue positive, they're at someone else's cost. Has to be borrowers. What are they doing, globally? Buying existing housing off each other for ever-more debt. Putting ever-more demand on the future, in other words.

Discounting has to cease, then reverse too. The future becomes ever-more important in a reduction scenario - and there is no argument about our depleting regime.

I'm no fan of GDP - but if you note a trend for more debt to be accumulated than GDP increases, you have to ask whether 'growth' is indeed happening? I think they're collectively kicking the can down the road, because they have no other option and they're ideologically hamstrung.

So it is a 'when', not an 'if', and it has to be bigger than the GFC. And it is likely to be when belief in the global RE bubble tanks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.