Term Deposit interest rates are very low. And they may go even lower.

So, what alternatives are there?

A year ago we posed that question, and since then term deposits returns have fallen relentlessly, shoved lower by monetary policy.

But as returns have evaporated, savers' attractions to them have increased. Amounts on deposit have risen regardless.

That is not to say savers are happy about the situation, but the point remains, they are a key focus of savers all the same.

In the past week, a deputy governor of the RBNZ has voiced what others have suggested; if you are not happy with the returns, looks for alternatives. Put your money elsewhere.

There are many options. But we still seem reluctant to shift to any of them.

The reluctance is understandable, especially for savers who are at or near the end of their income earning careers. The fear of the risk of loss far outweighs the prospect of additional gain. There are few oppotunities for these savers to oversome mistakes or unfortunate events. Liquidity risk weighs heavier too.

Some savers are seeking out higher returns and prepared to accept elevated risks.

But if you are a term deposit saver, you and your fellow savers have shown little enthusiasm for alternatives.

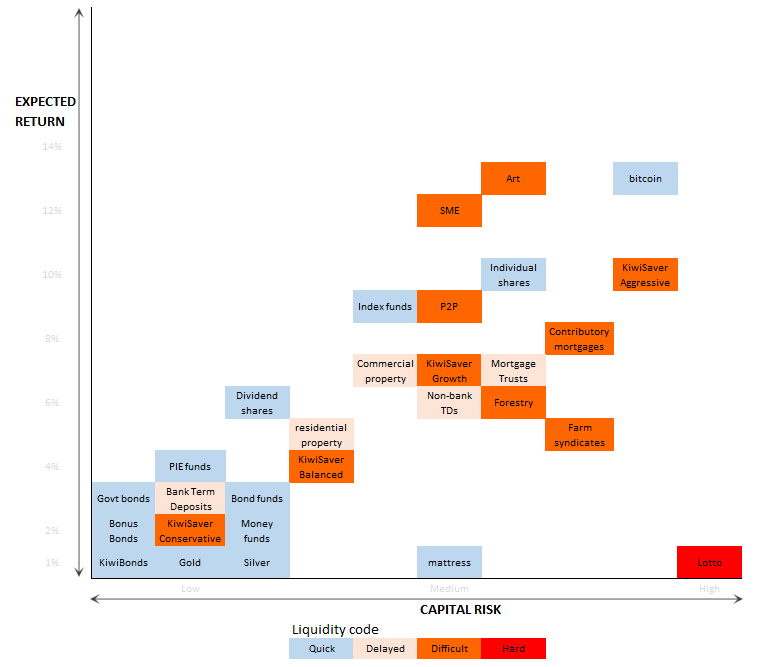

I want to suggest a framework for thinking about alternatives.

For increased returns you need to face up to the risk to your capital sum, and the liquidity risks of many alternatives. Investments that don't have functioning markets make it problematic to get your money back either before the stated maturity date (commercial property funds are one example), or perhaps ever (and investments in SMEs are examples here). They can offer good returns when things go to plan, but if unrelated 'events' intervene, you can be stuck with poor to no options.

So we need a framework to think about options. The only reliable advice is to use a professional who understands you personal objectives, and risk tolerance. This article is not investment advice and does not replace it.

But when you do talk to a professional, you need to have done some homework so that what you agree with them has some considered input from you.

What follows is a template that might start you off. The positioning of the alternatives will need to be moved around until you are happy, and appear realistic and reasonable to you. It's a starting point only, one that should help you get your own thoughts together.

Don't use this template as a recommendation or even a best-practice suggestion. It is only a starting point for you to develop a matrix foir your own personal situation. We strongly recommend to work with a qualified professional.

One of the key words in that template above is the word "expected". The only way to assess future returns is by making judgements about what to expect, and as we all know, in the short term at least, expectations can be buffeted by the unexpected. You need an intermediate or long term focus to be able to look past the fear of the unexpected. You need patience.

The key points to become clear about, are your tolerances to:

- risk of capital loss

- liquidity risk

High-risk takers usually talk up the advantages of leverage, but remember, leverage cuts both ways ... no matter how many people try to tell you "you can't lose with property". Gamblers in CFDs talk the same game.

Options in New Zealand are skewed compared to options available in other larger countries principally because we don't have deep capital markets, or in fact many functioning markets at all, that price and clear many of the options that are available. But some markets are developing and it is worth seeking them out.

One final point. Most of the categories above deserve finer splits. As you hone your analysis in favoured areas, your next task is to delve deeper into specific alternatives and specific options.

53 Comments

And just how many truly professional advisers are out there? Most who don that mantle are anything but; they take commission on products and must immediately be ruled out. They are pure salespeople and should be seen as such.

Only those who charge fees on an hourly rate can be considered professionals and as in all professions, their actual skills will range from very high to poor.

The article made one really good point. Before talking to anyone, people need to do some hard thinking themselves and as I found out in my long career as a consultant in the UK, most don't bother to do that.

Well put.

And as a corollary, I'll just repeat my view that the era of ever-lower interest rates is nearly at an end. Not because 'they' don't want lower ones, but because even they can see that (1) they don't work as expected - people save more the lower rates go for all of the abovementioned reasons and (2) they finally see that 'more of the same' isn't going to change that.

So. What we might face is the exact opposite. "Inflation" spurring interest rate rises. MAKE people divest their savings by threatening the loss of purchasing power. Many will remember that and react far 'better' than squeezing their returns.

Will that work? I doubt it in the longer term ( it will have dramatic effects on other segments of the economy) but when you're out of options that have repeatedly failed and are in a hole as big at the one 'we' have collectively dug for ourselves what else is there?

Quite good of high lighting CAPITAL RISK for different investments. If it’s long term then kiwi saver balanced and growth is a good investment.

No, it can't be, and neither can very much else.

They are all bets on the future, and that boils down to betting on ever-more resources and energy being available in the future.

How many times has it got to be said? And how many times will commentators ignore it?

Interest-rates had tredned to zero and below, BEFORE the virus. Debt was collectively unserviceable BEFORE the virus. And any 'investment' had to be averagely able to bid for less real stuff in the future, a truth BEFORE the virus.

And I'm betting there's not one 'advisor' who knows this. They were all trained to believe the world was flat. Otherwise known as being taught economics, present form.

Just a thought if all depositor take their deposit away as advised by RBNZ Governor will the banks not have some problem in terms of liquidity needed to offer loan.

Also now, is other investments not more risky than before specially for someone who has not invested before and depended only on fixed deposit as wanted no risk - Basically now RBNZ wants everyone to go out and take big risk as RBNZ has runout of ideas/tools

OR

Maybe RBNZ can see that some banks may default in futire if it continues, the way it is now and is warning depositor to take their money out of bank.

LOL - RBNZ engineering a bank run?

Nice piece David. Lotto cracked me up. I almost never buy lotto for that reason.

Art is worth thinking about. I have some Japanese pieces, not high value, but at least mid value, that have more than doubled in value over the past 10 years.

And it has personal satisfaction factor.

Cars are another investment option as can be seen by the hauls that get taken away by the police at gang bust raids.

Unfortunately its a rare car that increases in value over time though. And they have holding costs: a garage which could be rented out to some poor sole.

Cars are just like gold, it appears that when fear abounds, nobody wants to buy anything. If you sold shares at the beginning of the latest downturn you probably didn't buy gold with that cash. That's a two step process and one which as far as I know has not been shown to be valid with cash still holding its value as the prime transactional mechanism in the short term.

I suspect that gold would only really really be of value if there was a complete international meltdown which this Wuhan thing is not even close to being.

Lotto has an expected value that is negative.

Perhaps... only just perhaps ;-)... City doesn't make any money of people holding cash.

Things are going "nuts"

https://youtu.be/macsrQQeVO8

"But ... you need to have done some homework so that what you agree with them has some considered input from you."

Yes definitely. I have always been one for being hands on and self managing. This has usually worked out a lot more successfully than simply handing stuff over to others to whom you're just a number. In a couple of instances letting others do the job that I could do was a spectacular failure

I like the concept of the article, but that chart comparing risk needs a major overhaul!

I’m a little speechless to see Bitcoin & “Aggressive Kiwisaver” (ie Mostly shares) as the same level of Capital Risk, and Then “Art” several degrees “safer” - and then Gold as one of the safest! (Go look at a gold price chart and look at the massive swings up and down).

I think the positions of Bonus Bonds and Kiwi Bonds should be swapped around. In the current environment, I don't think anything has a lower expected return than Bonus Bonds. They're nothing but a cash cow for ANZ.

My mother had a couple of thousand in Bonus Bonds when she passed away. I didn't have any paper work so I presented my written authority to carry out her affairs and asked if she had any still.

No was the answer.

I later found some paper work and cashed them in.

Moral of the story, never trust the ANZ.

In the past week, a deputy governor of the RBNZ has voiced what others have suggested; if you are not happy with the returns, looks for alternatives. Put your money elsewhere.

He should have recommended spending not investing.

If there is slack in the economy, then new spending most immediately draws down inventories, triggering new orders and new production, so mobilizing previously underutilized capacity, both capital and labor. In this counter intuition, my purchasing power increases and the consequence is that aggregate income increases. From this point of view, the alchemy of banking seems like a kind of widow’s cruse, something to be treasured by economic science and if possible exploited in the name of the general good. Link-page 3 of 27

On residential houses!

Tony’s opinion $$!!!??

Surprise!!!! Most respond to buy shares.

https://i.stuff.co.nz/life-style/homed/300027516/spending-plans-drop--e…

His surveys are almost worthless, as they represent a very narrow segment of the population, one that is wealthy and property-obsessed.

His surveys are almost worthless, as they represent a very narrow segment of the population, one that is wealthy and property-obsessed.

His surveys represent his readership. Just like Granny Hearld's polls or surveys represent their readership. If TA bases any claim as anything different than representing his readership, then he's nothing more than a fraud. If I ran a poll across the Northland Rugby Union Supporters club about their favorite team, I'm sure Taniwha would rank high or Auckland relatively low.

I used a financial advisor who represented Zurich Financial Services. These companies are notorious for targeting expats across Asia with tax-free pension plans. It's the same old schtick and basically any old monkey can do what they do. Anyway, I naively signed up for a plan many years ago. The allocation was not the worst but I later added China equities. The salespeople do their best to lock you in or terms that maximize their commissions. If the investor pulls out at any time, they can lose up to 50% in penalty fees, etc.

Anyway, my advisor was identified by the Japan FSA as operating illegally, which I came across through an article written by a legal colleague. I sensed the opportunity and took the info to Zurich based in Hong Kong and argued that I had been sold to by an unlicensed advisor and Zurich needs to take responsibility. They seemed desperate that I didn't blow it open and asked me what I want. I asked to be released from my plan with no penalties. Even then, Zurich tried to charge penalties when the final investment sum was calculated. When challenged, they were quick to rectify. Fortunately for Zurich, those were 'boom times' and there were plenty of other foreigner prey to target.

Well done.

You definitely would not have got your money out in a downturn.

So you are a bit lucky too.

But me personally, I would never have signed up for this sort of thing in the first place. I am not trying to blow my horn. I will have missed out on making money from all sorts of schemes. But countering that, I have not lost money either. eg My Kiwisaver is at its peak again: I didn't change funds or add any money into it after the Wuhan stuck. It shows that conservative/cash has merits for those who are happy with just plodding along.

"If the investor pulls out at any time, they can lose up to 50% in penalty fees, etc."

Was it an investment linked assurance scheme (ILAS) product? There are a lot of investment products with high commissions embedded. There were ILAS sold in Hong Kong where most of the first 3 years of installments paid in were commission to the salesperson / financial advisor, so if they redeemed within a short period, there was a large cost for the investor.

Exactly. They would also ask you about the plan term: 10 years, 15 years, 25 years without telling you that if you went for 25 years and pulled out after 10 years, then you would pay penalties for the remaining 15 years. So any potential investor would logically choose 10 years and then keep paying into the plan after maturity without the risk of penalites. Most of these plans are run by companies like Zurich and Skandia. Even though they're 'tax free' (based in tax havens), the fees are quite exorbitant.

The Japan FSA cracked down on a lot of IFAs because they were operating without the approporiate licenses, even though they were registered businesses in Japan.

The same IFAs were also pushing property funds like LM Investment based on the Gold Coast ('you can't go wrong with bricks and mortar') run by Kiwi Peter Drake. Even though LMI was OK'd by ASIC, this was was a monumental disaster.

https://www.goldcoastbulletin.com.au/news/gold-coast/bankrupt-businessm…

'you can't go wrong with bricks and mortar'

Yes, that phrase is commonly used by sales people of real estate related assets.

Was this the fund?

https://www.scmp.com/magazines/post-magazine/article/1558078/when-inves…

If seems that the fund had a higher yield (than bank interest rates) to attract investors. This is where investors potentially get caught out in their search for yield. Seen it happen many times.

The fund was involved in making loans to property developers. - that is inherently risky, akin to the finance companies in NZ where many depositors lost their money.

"Launched in 2001, this fund, one of more than half a dozen operated by LM Investment Management, lent money to Australian property developers and paid out fixed returns slightly above prevailing interest rates, making it popular with clients nearing retirement."

"While common practice is for fund managers to diversify their holdings, the accounts show that a hefty 60 per cent of the Managed Performance Fund was tied up in one asset, a HK$1.4 billion mortgage on Maddison Estate. This was a Queensland-based site where Drake planned to build a residential compound. LM promoted Maddison Estate as having a future value of HK$6.8 billion. KordaMentha valued the still undeveloped site at HK$145 million to HK$163 million. According to KordaMentha, loans made by the fund to real-estate projects are still under investigation."

The reach for yield can make retirees move their money into investment products with high risks. Always know the risks of the investment products and look beyond the yield. Here is one such example:

https://www.google.com/amp/s/www.wsj.com/amp/articles/bankrupt-in-just-…

CAVEAT EMPTOR

Excellent article David. Though I'd have to admit that I'd be more inclined to invest in Art market then I would Bitcoin (Or the other 2000+ cryptocurrencies) out there.

I'd also put investing in cryptocurrencies on the extreme high risk level more so then the art market because they have to deal far more with every day global tech and political changes, not to mention that one of the major players China is about to introduce its own state government controlled cryptocurrency.

And we can all see how emboldened China has become even in the last few months and we know that they will force their citizens to move away from the likes of Bitcoin to their state controlled cryptocurrency.

That could leave Bitcoin high and dry with a rather server user share market loss in the next year or so.

Independent article: China says state cryptocurrency set to rival bitcoin is 'close' to launch.

https://www.independent.co.uk/life-style/gadgets-and-tech/news/china-cr…

The Economist: China aims to launch the world’s first official digital currency. https://www.economist.com/finance-and-economics/2020/04/23/china-aims-t…

I'd also put investing in cryptocurrencies on the extreme high risk level more so then the art market because they have to deal far more with every day global tech and political changes, not to mention that one of the major players China is about to introduce its own state government controlled cryptocurrency.

You don't understand Bitcoin then. The CCP or any other govt could create a cryptocurrency. But it's not Bitcoin. It's a centralized crypto that follows the whims of a govt or central bank. For example, they could increase the supply at any time, threreby removing one of the key features of Bitcoin: scarcity.

You cannot "force" someone who owns Bitcoin to hand it over to the state, particularly if it's in cold storage. And let's say the CCP and the U.S. govt made Bitcoin illegal. So what? You might have countries such as Japan and Cyrpus as jurisdictions where it is not illegal.

Any knowledgeable Bitcoin owner should not be afraid of state-owned cryptos or even Libra.

Correct. Any government controlled crypto currency will never have more value than their fiat currency.

If not pegged to their fiat, it may even have less value.

JC you obviously don't understand the CPP then. Haven't you been watching whats been happening in the the news with Hong Kong etc.. It's not about markets it's about control of their people.

JC you obviously don't understand the CPP then. Haven't you been watching whats been happening in the the news with Hong Kong etc.. It's not about markets it's about control of their people.

Nothing to do with a CCP-backed cryptocurrency or Bitcoin. The CCP cannot "replace" Bitcoin. Furthermore, even its ownership were made illegal, that would more likely increase its value.

JC Obviously you haven't read the articles that I attached in my original comment. It's not a case of the CCP replacing Bitcoin, it's just a case of the main investor user base for Bitcoin and Bitcoin mining is in China. Did you know that China cryptocurrency exchanges were said to account for 90% of global bitcoin trading. So with the CCP adding their own cryptocurrency this will massively impact other crypto currencies including Bitcoin. But go on, keep reassuring yourself that everything will be OK, even when common sense dictates otherwise.

JC Obviously you haven't read the articles that I attached in my original comment. It's not a case of the CCP replacing Bitcoin, it's just a case of the main investor user base for Bitcoin and Bitcoin mining is in China. Did you know that China cryptocurrency exchanges were said to account for 90% of global bitcoin trading. So with the CCP adding their own cryptocurrency this will massively impact other crypto currencies including Bitcoin. But go on, keep reassuring yourself that everything will be OK, even when common sense dictates otherwise.

Nonsense. A state-owned cryptocurrency has nothing to do with Bitcoin. They're completely different things. The CCP cannot close down Bitcoin outside their jursidiction. Period. Secondly, if the CCP confiscated Bitcoin ownership, it's irrelevant. BTC will exist regardless.

JC The only one spouting "Nonsense" Is you! You're missing the point completely and rambling on incoherently saying that the CCP is trying to replace Bitcoin when I've already explained several times to you that is not the case. It's just that the Chinese government cryptocurrency will naturally have a large part of that investor base since most of Bitcoins investor base is largely Chinese. Anyone can see that Bitcoin will exist but will be missing a large part of their previous investor base which means its value will drop over time.

Huh? The properties of a digital yuan and Bitcoin are completely different; specifically, a currency on a decentralized ledger that is scarce and cannot be controlled by central banks. That is why Bitcoin has grown into its own asset class. It doesn't make sense for a Chinese owner of Bitcoin to sell Bitcoin and buy yuan (assuming they own Bitcoin for its properties). Even as a speculative instrument, it doesn't make sense.

I agree J.C., and would like to add that knowledge of cryptocurrencies in NZ especially, is hampering any development of the essential understanding of digitization that is essential in the coming economy.

The chinese digital yuan is already being tested in 4 major cities in china.

The chinese are well ahead of nearly everyone with not just the implementation of a central bank digital currency, but fully understanding it's global applications. The usd may be at 60% use as a global reserve currency, yet this is a shrinking %. The usd relies on legacy systems, ie SWIFT, which is expensive and slow. A digital yuan has the advantage of all digital assets, in that it is borderless, and highly cost effective.

Link it's use with over 100 countries that are already part of the belt and road initiative, and you can start to see the potential.

That the digital yuan is a rival to bitcoin, or libra etc, is almost beside the point, when considered in trading terms, a digital yuan simply makes it easier for nations to trade with china, and cost effective too. China is every countries largest trading partner, which one of them wouldn't want to reduce the fx costs and time involved in the trade?

The advent of such a currency brings more urgency to the relevance of bitcoin and other decentralised digital currencies, as these are important to individual trading across the entire planet. Bitcoin is an effective way of being independent of national central bank currencies. Neither is exclusive, yet it is time for the public to seek an understanding of digital currencies and assets, regardless of how our legacy financial system denegrates them. Bitcoin and other decentralised digital currencies are a vote for freedom, the digital yuan is simply used to purchase something originating in China.

Should the nz public remain in the dark about the digital phenomenon that is happening, nz itself will remain in the dark, or more correctly, in the past.

A digital yuan is not a rival to Bitcoin. Never has been. Never will be. Bitcoin is not used in trading and even in few transactions. A digital yuan could be valuable in a real economy sense in that it can be used with WePay and ecommerce. To me, it's quite totalitarian.

Can't teach an old dog new tricks JC. It surprises me how many folks on interest haven't taken the time to look into Bitcoin. Anyone with an understanding that markets are confidence based only needs to take a look at bitcoins cap ($179.70B), holders (now 100M+), and hashes (security) to see Bitcoin is established and here to stay. It's been hundreds of years since a generation had the opportunity crypto is presenting. As for which ones will replace currency, too early to pick. But as a long term value store Bitcoin has won the race. And as a smart contract solution etherium is established. If you're not taking Bitcoin seriously right now, you'll live to regret it.

The expected returns above for asset classes (except bank deposits, long term government bonds) are based on long term historical returns continuing into the future?

This may not be the case.

David, I love this piece. Um, mattresses as medium risk was a bit questionable :)

The first thing I'd add is the template is 'for average times', but we aren't that. Right now hyper share valuations in US must extend share funds out to much higher risk 'at this point in time', globally, before prices correct back to fundamentals (which are shocking)?

Also I think central bank stimulunacy has been a paradigm change in a broken investment world. With interest rates near or below zero, bond/treasuries are in my mind every bit the risk of shares right now. Indeed we've had forced on us a world of all risk for non-commensurate returns. Awful time to be retiring.

It is indeed. I half expected to be made redundant by now and become one of the ‘early retirement’ types. I’m sure it will happen, but when is anyone’s guess.

Right now, I look like one of those ‘Preppers’ and a bit foolish. We took cash out of the Bank, took a 0.9% after tax haircut on TD returns to move into KiwiBonds, bought Gold coins (6% buy sell margin) and a Rolex I don’t intend to wear (10% buy sell margin), but so far the ‘smart money’ seems to have moved direct to property which an agent friend say is ‘pumping’ as evidenced by his sales in the last two weeks. Time to admit I have no friggin clue where this is going. My wife is looking at 2brm brick and tile properties near by. She might be the smart one in the family at this rate, albeit it is fun looking at the coins and I might need to check the cash balance as I suspect it’s disappearing $50 at a time ;)

Actually it's a great time to be retiring.

The generation who got the best run ever and who are handing those who follow, a stuffed planet, an overcrowded planet, a de-stocked planet and a pile of worthless digits.

They live the peak. I wouldn't complain, if I were you. All you lack is relativity.

I personally would place bank term deposits in the medium risk sector of the chart. The longer the term, the higher the risk. All we need is another lock-down and our banks will be put under considerable stress (this was the message of a senior level banker published here on interest.co.nz very recently). Term deposits are high up the list when it comes to what a bank has license to freeze. The OBR is not a myth, it is a reality; see RBNZ webpage https://www.rbnz.govt.nz/regulation-and-supervision/banks/open-bank-res…

There is no alternative. Now everyone is compelled to become investment savvy. Those that are nearing retirement have something they need for the future, yet they have to weigh up risks. Thanks to the rbnz, there is no alternative that allows a solid return, while people go and enjoy their retirement.

The actions of the rbnz can hardly instill confidence in the monetary system. A third of nz gdp comes from financial services. So investment advisers are a dime a dozen. Nz economy has been hollowed out. Stocks and property, work in the finance industry. An unhealthy economy is unlikely to get better by forcing everyone and all money into the investment vehicles that helped exasperate the sham we find ourselves in.

Instead of asking why our financial elite got us in this situation, we are now expected to weigh risks, presumably so that the elite remove any sense of liability for any losses incurred.

True alternatives should be seen as anything outside the fiat system.

That's the only way of voting no confidence to the financial masters.

This is a "boots on the ground" reality piece.

My aged (96-year-old) mother has going on $250,000 in her 'big bank' of which about $215,000 is on term deposit which matures end of this July. In the past, her term has been 1 year and then renewed at the going rate for another year. These rates have been gradually diminishing incrementally over the past years but I predict that by the end of July they will only be around 1.5% for a one year term. So, at this July maturity I'm going to recommend that she puts at least $200,000 in Kiwibonds for a 6-month term at the current rate of .5% (if it remains at that rate come July, or even a lower rate would be ok.)

Kiwibonds are currently rated at AA+, while the 'big banks' rating is AA-, so this will give her a window of security until we see how the land lies after the 6 month Kiwibond matures. The loss of the extra bank interest forgone (effectively around 1%) is negligible in the overall scheme of things and she would prefer to leave the principal intact to her legatees than have a few extra dollars with the extra risk, remembering that these are extraordinary times. I consider the OBR a completely unknown process as to how it would play out in practice, but I would hazard a guess that it would take months if not years to completely resolve itself.

My gut feeling would be that property may be the best long term investment as long as your leverage allows you to be happy with a lower rental income. I think that those who have to charge usurious rents will come unstuck. I have lately noticed an increase on the usual number of 'for rent' signs going up in the southern inner city suburbs.

Notice that precious metals don't even make the chart. Been a bit rocky for gold in past month, but should not be ignored.

Gold has performed pretty well pre-GFC up to now.

https://snbchf.com/2020/03/obyrne-global-supply-gold-silver-coins-bars-…

Gold and silver are both on the chart.

The lack of investment options in NZ is tragic, all those years of John Key prophecising that we would become the Switzerland of the South Pacific...all we got was the Panama Papers!

Just wondering why managed funds are held in trust while term deposits aren’t.

Is it a cost issue or something to do with the way they’re structured?

And if they could be restructured to be held in trust would that negate the need for a deposit guarantee scheme?

Be a Borrower and not a Saver, for the next 2 years. Spend and boost the economy. Take one for the Team.

Thought it might be a good ideal to revisit this..

https://www.interest.co.nz/personal-finance/100327/jen%C3%A9e-tibshraen…

Great article thanks David, gets me thinking. How about another asset class. Those at home expenses, ie energy, fuel gas, insulation, better temperature control. I'm thinking that in a low return environment you may get really good returns from insulating or solar, thermal curtains, electric car, etc etc.

Of course you get the comfort as well as the return.

A note on payback. A payback of 10 years is a simple return of 10% (no compounding calculated).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.