Okay, so a quick question to start: What last happened in New Zealand 2491 days ago?

A chocolate fish is in the mail for anyone who correctly identified that it was the last time interest rates officially went up in this country.

Yep, that's right, on July 24, 2014, the Reserve Bank hiked the Official Cash Rate from 3.25% to 3.5% in what was the last of four quick-fire hikes that year as our central bank mistakenly pulled the trigger and fired at inflationary phantoms. But the hikes were all subsequently reversed of course, and then some.

While the RBNZ's currently some way from conceding that interest rates are going to have to rise again (and we'll get another reading on this at the next Monetary Policy Statement release on May 26), others in the marketplace are increasingly of the view that rates are going to have to rise.

Significantly, economists at the country's biggest bank, and biggest mortgage lender, ANZ, have this week changed their call and now expect interest rate rises from August of next year. They've likely taken their cue from the ANZ's own business surveys that are showing cost pressures going off the scale.

Our central bank, like others around the world (and notably in the US) is so far attempting to 'look through' the current wave of price pressures, which are in large part stemming from Covid-induced supply chain disruptions.

But there's an increasing view out there that these pressures will be pervasive and persistent enough to ultimately require central bank responses; so, interest rate rises.

As indicated in the lead in to this article, any rise in interest rates - which will lead to higher mortgage rates - is going to be, to say the least, a novelty.

A shock to the wallet

There will be substantial numbers of mortgage holders in this country who have never experienced an increase in their monthly mortgage payments (unless it is through some reorganisation they've done themselves). It could be a shock.

As the RBNZ highlighted in its recent Financial Stability Report, new mortgages taken out for house purchases in the past two years represent approximately 30% of the current stock of mortgage lending. "Newer borrowers will generally be more vulnerable than earlier borrowers, as they have repaid less principal, generally experienced smaller equity gains, and may have had their serviceability assessed at lower interest rates."

With interest rates so low, mortgages have been able to get much bigger, while the serviceability factor has actually continued to improve. But if we now hit the reverse button and start seeing increases in mortgage rates, a rise from such low levels is going to be keenly felt.

This is at a time when significant numbers of people, particularly first home buyers, are buying houses at increasingly stretched debt to income ratios.

At the moment the OCR is at just 0.25%. ANZ's economists are suggesting a series of hikes starting from August next year that would see the OCR at 1.25% by the end of 2023. Well, that's not the end of the world is it?

But let's just have a quick little crunch on the interest.co.nz mortgage calculator.

Based on the RBNZ's mortgage figures for March (latest available), the average-sized new mortgage nationwide was $335,000.

If we were to assume a mortgage of that size, with 30-year term, and current rate of 2.25%, the monthly payments would be $1281 a month.

Onwards and upwards

Okay, if we were then to assume that any 100 basis point increase in the OCR gets fully passed on to mortgage rates, that would see the rate on our mortgage rise to 3.25%.

It doesn't sound much, just a 1% rise right? Wrong. It's about a 14% rise in terms of monthly payments. Our monthly payments would rise by $177, to $1458.

Look, that should be well manageable enough, but will still be noticeable. Also, if we look at the whole term of the mortgage, the amount we would pay in interest an fees across the whole term would rise by $63,720 (a just over 50% increase) from $126,160 to $189,880.

That's an 'average' mortgage.

Let's try something a bit more bracing.

The RBNZ's latest debt to income ratio figures for March showed that about two thirds of Auckland first home buyers in that month were on DTIs of over five - and that their mortgages worked out on average to be $752,000 each.

Using the same formula as in the above example on our calculator, these FHBs would be currently paying $2874 a month. At 3.25% they would be paying $3273 a month (works out at an extra $92 each week). The interest and fees paid across the term of the loan would rise (again over 50%) by some $143,640 - from $282,640, to $426,280. Oh, and yes they would still have to pay the original $752,000 back as well.

So, not insignificant.

It could be worse

And that's a small rise in interest rates. What if inflation really proves more pervasive than even bank economists are starting to believe?

Given that central banks, including our RBNZ, are currently 'looking through' the inflation and want to wait and see that it is of a more lasting duration than has proved to be in recent years, they are all likely to wait too long before hitting the rate rise pedal. That means when they are forced into action, well they may have to squeeze the pedal harder than anybody currently thinks.

If we go back to the $752,000 mortgage example, a rise in rate to 4.25% would see monthly payments rise to $3699 a month. An increase to 5.25% would hike the payments to $4153 a month. That's $1279 a month more (44.5% more) than would be being paid currently.

Unlikely? Perhaps. But impossible? No. Remember we are talking massive mortgages with 30 year terms. And a lot can happen in 30 years.

Historic mortgage rate figures from the RBNZ show that six years ago (and beyond the memory of many now-mortgage holders) the one-year fixed mortgage rate was about 5.5%.

But the average-sized mortgage then was about $206,000.

Low interest rates have been a honey trap. They've lured us in to ever increasing piles of debt.

We've got to keep fingers and toes crossed that inflation doesn't take off. Because if rates really start going up, it will be bee stings all round.

110 Comments

IF persistent high inflation does eventuate then Orr will be forced to act and up the OCR. If he doesn't all the conspiracy theorists may have a point. However, with the current CPI the OCR is appropriate and all the whinging is sour grapes.

I'm just trying figure out who the conspiracy theorists are that you are referring to? (and what is their point of view?)

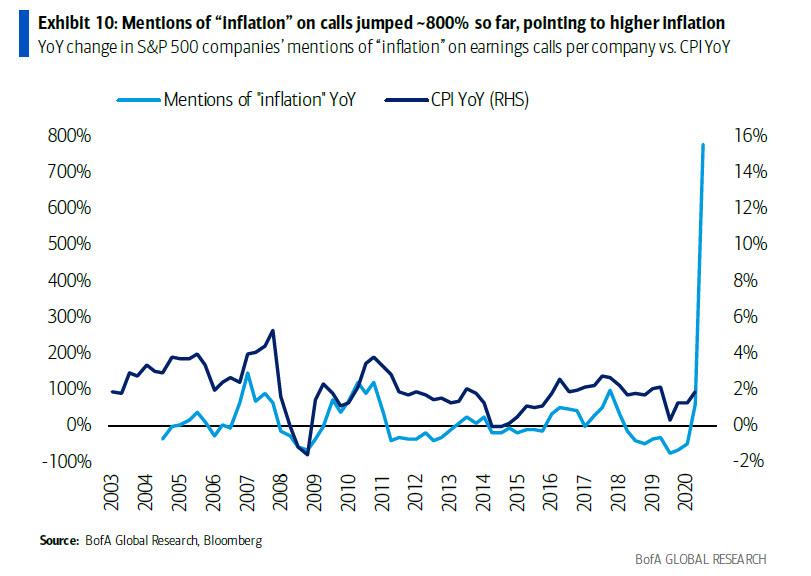

Is it charts like this?

https://cms.zerohedge.com/s3/files/inline-images/mentions%20inflation_0…

{kind=link}

The conspiracy theorists are anyone who hasn't made over $200k tax free capital gains this year and who thinks this is not fair or justified.

Those that think "REAL" CPI is running at 15% and not 1.5% and therefore OCR should be at 20% with their TD rates at around 21%.

This is the only chart that matters:

https://www.stats.govt.nz/indicators/consumers-price-index-cpi?gclid=Cj…

Those that think "REAL" CPI is running at 15% and not 1.5% and therefore OCR should be at 20% with their TD rates at around 21%.

The 'real CPI'. What a joke. The conspiracy theorists are those who think the CPI as an inflation measure is a crock and the real measure of inflation is related to money supply expansion + increase in the price level. I'm one of the conspiracy theorists.

So what is your calculation for the inflation figure for March 2021?

RBNZ 1.5% v JC ?%

I don't know because I have more important things to do than building an index for no monetary compensation. What I do know is that is that the value of labor and purchasing power is being eroded primarily through expansion of the money supply. That is the 'real inflation', not a construct that underestimates this destruction through an aggregate price level.

Lyn Alden recently wrote an 'Ultimate Guide to Inflation', which is very useful if you want to understand more about what inflation really is. The graph showing US broad money vs the CPI should give you an idea as to how much understated the true inflation rate is.

I paid $18 for a Big Mac combo plus a Qtr Pounder today. No silverware, no Piano quietly playing the corner, no Maître D just a self serve checkout, boxed bread and meat. Maybe there is something to this inflation thing.

About 10 years ago, I would buy a morning coffee at McDs for about 120 yen in Japan before heading up to my office. Damn it was cheap. Here's another thing. The coffee was really good for 120 yen.

Paid $6 for a scone in Tauranga. Coffees now regularly $5. Auckland rates rise 5% next year. Southern Cross goes up every year regardless of any claims. Fuel edging up.

Did I mention house prices and rents?

Min wage increase has fuelled it.

What's in the basket? Airfares and toilet paper?

Restaurant meals and cafe food and beverage prices are rapidly rising. Won't take much of an increase from here for people to start to freak out.

Inflation is going nuts. I purchase electronic parts from one company and it used to be freight free if you ordered online, now overnight the freight is suddenly $10.

Minimum wage increases are fuelling house price growth?

Min wage increase has fuelled it.

Almost necessary in a non-deflationary environment. Japan has dealt with 20 years of a deflationary environment because they have huge consumer demand that compensates for lower profit margin. The Anglosphere cannot survive without perpetual asset bubbles.

Big TV's that are rare purchases.

I'm finding the same here in Canterbury. Our Council has just advised us that our rates and water charges are going up shortly. Petrol is up, insurance is up, groceries, you name it. As a retiree, who used to be able to count on a little interest from term deposits to 'help out', I'm now finding even going out for coffee these days is a luxury.

Ah but now it only costs 100円

Apart from property in Tokyo and luxury items and services, Japan is damn cheap.

In 2020 at USD$4.89 Big Macs in NZ cost USD$0.38c more than in 2015 (USD$4.49)

https://www.statista.com/statistics/274326/big-mac-index-global-prices-….

Heavy G, these are the year on year broad money increases.

This is a good place to start

Aug 2020 354,806 11.9

Sep 2020 355,780 11.1

Oct 2020 359,598 11.8

Nov 2020 360,384 11.1

Dec 2020 365,780 12.2

Jan 2021 359,421 11.3

Feb 2021 361,166 10.6

Mar 2021 365,809 8.2

For Milton Friedman, inflation was never a cost-push or exchange rate increase effect, but a national phenomenon produced by monetary policy. As a conclusion, Friedman said that inflation was always produced by high public spending and a growth in money supply.

Which is true. The quantity therory of money is sacrosanct. MxV = PxQ. To argue against it is to argue against 2+2 = 4. It is mathematically impossible for NZ to claim an inflation rate of 2% over the last 20 years when the broad money supply has been increasing at 8.3%. The CPI is a fugazi.

Simple explanation as to why money growth is not directly related to inflation.

https://www.forbes.com/sites/johntharvey/2011/05/14/money-growth-does-n…

Some observations from New Plymouth

Rates to go up 12% this year.

Electricity: Fixed rate up 4%, kWh rate up 7.5%

Petrol has gone from 1.99 to 2.14 over the last 8 weeks alone.

Insurance: House and Contents down -7.8% (increased cover)

Groceries: Although the interest tracking shows minimal change, our local is definitely showing an increase. Sales have all but dried up, and shrinkflation is common amongst fruit/veg charged at piece rates. i.e. Brocolli, Cauliflower, Cabbage, Pumpkin, Melons (water and Rock)

- Mince up 5.8%

- Sausages up 14.1%

- Cheapest bread up 30%. Luxury bread hasn't been on sale since pre covid.

- Cheese up 8%

- Butter down -9%

- Milk stable

- Bananas stable

- Potatos up 20%

The most noticable thing however is the lack of stock. MSM seem to be accross Pet Food and Nappies, but a lot of other things are becoming harder to source (mostly range based - e.g.. where there were 7 options now there 3)

If we said that was a CPI basket, then average inflation is running at 7% (all things weighted equally and excluding fuel because I can't be bothered annualising)

Annecdotally we are noticing that RRP are remaining the stable across consumer goods. We don't make regular enough purchases of the same thing to quantify.

But Shrinkflation and Quality degredation are very much a thing, and sales are few and far between on common items.

I ignored housing because I am mortgage free. But for transparency sake ours is up 19.8% over the year. So if we factor that in, average inflation is 8%.

It only matters now, we are talking about CPI in future.

Conspiracy theorist - a person intensely disliked by bank and big pharma shareholders

The real question - is the current CPI measure fit for purpose?

fit for the governments purpose... to inflate the debt away

My fingers and toes are crossed for inflation and the higher interest rates that go with it. Let’s see this whole thing crash to the ground sooner rather than later.

The last year has shown us expect the unexpected so ruaway inflation and interest rate rises will not suprise me one bit.

It is time for common sense to return to markets and that includes stopping interest rate cuts to protect the over leveraged and face up to the fact sometimes you have to winners and losers which my help the people at the bottom to have a brighter future.

He. He. He.

Jack Nicholson laugh.

You want people to lose their homes?

How do you do the ethical maths between some losing their homes and others being able to afford homes with more reasonable prices? How do you account for the whole country becoming more competitive as our living costs reduce with lower house prices? How do you account for the savers and retirees being able to support a better quality of life from their term deposits?

There's two sides to the equation, by focusing only on one you are displaying a bias.

They still hide behind others plight because it benefits them. Everyone can see them for what they are. Everyone knows....

History suggests high inflation erodes everyones standard of living, its not just about housing

They do. They reek of envy. You have the 2 classes of DGM. The elderly who cashed out of property, are sitting on a $1m cash and want TD rates to be 20% so they can live the rest of their days off the interest.

Then you have the wannabe DGMers who squirreled away $50k by living in their parent's basement for the last 40 years as others got on with buying a house and starting a family. They pray for 22% mortgage rates to crush home owners and crash house prices to around $100k. That way they could pick up a cheap mortgagee sale and possible swoop in for a ready made family assuming there are a lot of marriage break ups as well. Vultures be vultures.

There may a little of both around. There's also people like me, who own a house or two but aren't 100% piled into a single asset class and don't depend on house price inflation to fund their lifestyles. I'd be financially better off if house prices doubled, but I would much prefer to live in a world where they fell 10-20% in the short term, and then flatlined while wages catch up. Larger falls than that would I suspect be net-good for society, but there would be collateral damage to the relatively innocent.

Not everyone is always arguing in their own self-interest.

Then you have the wannabe DGMers who squirreled away $50k by living in their parent's basement for the last 40 years as others got on with buying a house and starting a family

If they had taken that 50K and allocated say $40 to Bitcoin every month over the past 9 years, the ROI would be approx 61,000%.

'They reek of envy.'

I don't envy anyone. Well done to all the investment geniuses who trotted along to an auction and outbidded everyone else. What fantastic financial skill!

I don't begrudge them a cent of their winnings.

Conversely, if they suddenly become 'losers' because the market starts tanking, I don't think they should get (yet another) bail-out. I'm sick of people wanting to have a double helping of chocolate cake, and then eat it to.

@Te Kooti

How do you "lose" a home? Are these homeowners called MCK Hotels?

Sorry, NOT Sorry - sounds like you're spouting a bunch of hogwash. If you don't pay rent, you get evicted. If you don't pay a mortgage, you get evicted/mortgagee-sale. Seem like you want to live for free.

Personal responsibility is what's required.

I didn't spout anything Zack, homeowners are the winners, not the people here praying for higher rates which will not eventuate to any meaningful extent. The salient point here is that I hate to see anyone evicted and would not be seen advocating for others misfortune.

Who are you to say that higher rates "will not eventuate to any meaningful extent"? And if you truly believe that substantially higher rates won't eventuate, why do you even bother to have a crack at those who want this endless credit expansion to be dialled down? All people want is a return to stability and some equilibrium in the eternal struggle between borrowers & savers. We aren't after anything unreasonable. To say that we cannot ever get back to some sort of normality because people may 'lose their homes' - that's just holding the whole machinery of the system to ransom.

US debt has hit $28 trillion. Unless you believe NZ will go out on it's own, its pretty clear that raising rates is simply not possible.

The Fed has boxed itself (and thus us) into a corner. Inflation, but no ability to fight it with hikes.

What you think might happen if they try?

True however if we end up with serious inflation which is clearly possible all bets are off particularly if the credibility of the Fed and Co is severely damaged which would be the case. That said the central banks will not give up easily and will resort to everything imaginable to hold the line with interest rates. A critical part of the equation would be wide spread strong rises in inflationary expectations then you have a very serious problem.

Both the Fed and ECB are already on record saying they will not respond to short term inflation spikes as inflation has been below target for so long. Clearly there is going to be an inflation spike, but there was going to be one anyway as we move to net zero carbon. If we get meaningful wage rises I may change my opinion, but until we get through the Covid supply chain disruption and stimulus we won't have a clear picture.

Exactly right.

The FED doesn’t have much room to move at all. There will not be any great rate increases that the vultures with $50k worth of life savings on here are hoping for.

These are also the same self appointed moralistic guardians of “equality” praying for the market to tank. Massive hypocrites.

I imagine most will sell and just downsize so may have to change homes but won't be homeless (which I feel is the extreme you tried to convey). On the flip side with the current environment we actually already have homeless families because they can't afford to buy or rent. If you don't want house prices to change then you're already happy for people losing shelter.

Question, are "their" homes actually theirs? Maybe you should read the mortgage agreement more carefully...

But that's what the government is saying non-stop. It's THEIR house, it's THEIR house. If I put a down payment on something, whatever it may be, and then I find I can't pay for it then it gets reposessed. And what is unfair about that? We have people racing along to auctions, recklessly outbidding everyone else to pay some crazy price, and then apparently we all have to ensure that they never get into negative equity and moreover never lose THEIR house. It's a ludicrous situation. If you buy something you better be darn sure you can pay it off, otherwise you've obtained it by fraud and deception.

Maybe you should read the certificate of title more carefully

If some lose homes so be it.

It teaches a lesson not to over leverage otherwise imagine the mess we will be in if no one is allowed to fail.

It’s this bleeding heart mentality where someone taking a risk and losing is not allowed anymore, victim mentality, ‘social darwinism’ et al. Social darwinism is the good looking bloke getting the attractive girl, the person with better genes not getting cancer, the person with better social skills and fully working synapses getting the promotion i.e. you cannot make life pain free and ‘fair’ for all uniformly - to attempt it is to reject the basic tenets of human society and life on this planet.

If you read the literature available on the RBNZ website they state that changes in interest rates take 9-18 months to have an affect on inflation.

If they aren't raising rates now, its going to be too late. Your labour and savings have already been earmarked to be sacrificed to save the sacred real estate cow.

Inflation doesn't only hurt people who have savings, it also hurts those real estate cows. All costs of living go up, you don't think banks will increase margin on the mortgages that they lend out to pay for their costs?

Always worth reminding ourselves after reading an article like this that the RBNZ doesn't set mortgage rates, markets do. Mortgage rates can and do move independently of the OCR.

Kiwis seem to keep forgetting that we don't own any of the major 4 banks. If interest rate rises are deemed necessary by the banks then interest rates are going to move up. The is no direct link between the OCR and interest rates. The OCR is just a "Recommendation". Orr is going to get caught with his pants down.

Just a recommendation however FLP has provided cheap money at that rate.

the inflation pressure will be temporary. It's caused by the flush of support funds to individuals during covid, esp. in US.

Debt around the world is still high and there's no significant changes of the economic structure, can't see the upside pressure sustainable.

All these showcased what UBI can do: deflate asset price and inflate CPI.

Which assets have deflated in price exactly?

Good luck with that! With massive QE happening all over around the world, lets see where this gonna lead to.

"can't see the upside pressure sustainable..."

Correct

Wages wont keep up with costs ... too much deflationary pressure with any price rise

So UBI in any form it is

https://www.reuters.com/world/us/households-including-most-us-children-…

but UBI wont solve anything ... just a can kick

the pie is destined to be far smaller

"People don’ t understand that the economy runs on energy (of the right type, and cheap enough) rather than on money. Debt can be a temporary bridge to allow new investment, but if the debt doesn’t pay back with interest, the system tends to collapse."

"Taking a longer view, the level of the dollar was able to float a whole lot higher, after oil prices fell in 2014. This was also when US QE ended, for a while. This is based on the 10-year or 25-year chart found here:

https://tradingeconomics.com/united-states/currency

If we look back to the 1997 to 2002 period, the US dollar was also able to be very high during that period, which was when oil prices were very low.

Oil prices are now being pumped up. This has been enabled by the falling dollar, as the US adds more debt. The Euro is now at 1.22 relative to the US$. WTI oil prices is at $66, and Brent seems to be about $69. Can Brent really go above $70? We don’t know. At some point, high oil prices and high prices of other commodities pull the whole system down."

Inflation is temporary is a farce and is an attempt to convince market that reserve bank knows what they are doing and in control of the situation, reality is otherwise.

Also still in panademic but if emergency is over, should reserve bank be not taking off the from the acceletor and drive as normally as possible.

To be fair, lots of people said the same kind of thing after the GFC, in the UK and US at least. All the money printing and government deficits, surely inflation is coming? Turns out there were a couple of brief spikes to ~5% then it settled down again.

I wouldn't ignore the risk of high inflation, but it's definitely not guaranteed.

And what were they saying in Ireland?

Probably much the same. Inflation wasn't involved in the Ireland housing crash.

Yet many property investors / FHB still don't want believe what serious inflation can do to their lives. They still believe Government and RBNZ are siding with house owners. Maybe for now. But once it starts affecting the financial stability and economy, they will not hesitate to throw you under the bus.

I think everyone is under the (false?) illusion that the government will bail them out if shit hits the fan. It's certainly the message that has been sent since the GFC internationally ("too big to fail") - maybe they'll bail out FHB's or introduce more mortgage holidays etc...

I don't think its false, the government will bail you out. They have already done it so no idea why you think it will not happen again. The people know it and thats why they are into the next house purchase boots and all. The very reason we are in this mess to start with is the verbal signaling from this government and the actions of the RBNZ crashing the OCR to record lows.

To what extent? If someone has leveraged themselves into 10 properties and gets into trouble, should they be bailed out with a clean credit record just like the mid-20 year old First Home Buyer who saved a $100k deposit and unfortunately bought their first home at the peak of a bubble?

Maybe the Government could roll out State Advances mortgages through Kiwibank of 3% for First Home Buyers who purchased in the last 5 years, fixed for 30 years, as an apology.

.. it is not about "should" - it is about "would" / "will".

Wellington elites and scumlords are on the top deck, single dwelling owners in the middle and the normal workers and people on beneficiary are in steerage. The top deck have been provided gold plated life boats ladened with the ships treasures and have been cast to safety with Orr manning the lifeboats. The middle deck dwellers where thrown life rings. 50/50 chance of survival for them. The steerage dwellers might as well have been strapped to there beds, theres only one outcome for them....... but why? Why is 2021 NZ no different to UK 14th April 1912? Who voted in Mr Orr? How did he get his job? How does he get to decide who sinks or swims?

They don't even have the abilities to bail out savers when banks bankrupt, do you think they can bailout million dollar houses owners? Bailouts need money, it was doable back then cause we still had our high OCR, by dropping OCR, can provide extra simulation to economy. Now? How are we going to do that when it's almost 0% already? How much inflation are we going to do that after RBNZ printing out more money to help the bailouts?

Except housing *is* our economy. Houses and to lesser extent cows. That's it.

I believe the RB will go full Japan and buy every Gov't bond on offer to keep rates down if necessary. I'd like to be proven wrong, but I think there's strong political incentive to do 'whatever it takes' to stop a property rout.

Agree and will know next wednesday.

I have a business unrelated to housing. I am considering moving it to another country because my staff are finding it too difficult to house themselves in NZ. That cant be good for the economy.

I feel like we are going to read versions of this article for at least 2 years

I am of the view they won't put them up...because they know the debt becomes unpayable and they want to inflate it away.

(But do they have that level of control i.e will the markets just push them up regardless)?

So I guess with no rate rise, hunker down for inflation.

Anyone?

But what happens if they do nothing and inflation continues to rise dangerously? At what point (in your view) are they forced to take action?

CPI measured at 8% for the next few years, 10%, 15%, 20%?

When do they go, right unless we step in and raise rates, we're in trouble here and the trouble of doing nothing, is worse that the trouble of doing something.

As they can’t raise rates they have a problem. An option may be to restrict credit. Control inflation via lack of credit.

Who knows eh.

History seems to be on the side of dying fiat currencies being printed to parabolic, rather than sovereigns deciding to bite the bullet and allow deleveraging. So I think on balance you are right - rates will stay low, and money supply continues to explode (bailouts all round), propelling the can down the road until we have forced deleveraging as currencies collapse.

I'm planting more nut trees this year - nuts will be worth a buck each, even without chocolate coating.

What I don't understand is why the RB is so hell-bent on always moving by 25 points at a time. They could easily adjust things by 10 or 15.

Governments around the world are pumping stimulus into the economy. Which is causing people to buy more S#!T. In the places where they make the majority of the S#!T it is getting harder and more expensive to manufacture due to Covid and other factors. So they want to charge more for their S#!T. The people actually making the S#!T want to be paid more as well. There is also limited capacity in the supply chain to ship S#!T. So the S#!T shippers have been able to increase their rates 4-5X from last year. Very soon the S#!T buyers will see the price of S#!T rising fast. That will mean they will want to buy more S#!T because they know the price of S#!T will be even higher in the future. Also they will start demanding more money for the S#!T they do (or can't be bothered doing in some cases). You wont be able to "look through" that S#!T. It will be thicker than an RB economist.

The RBNZ gov decreeing current cost push pressures to be temporary, has me worried. In our businesses we are seeing an ongoing tsunami of significant price increases in imported components. Metals and plastics especially. Orr is effectively predicting a reversal of the commodity cycle upswing and also that the current labour cost increase pressures will magically abate just as the migration flood is finally brought under a semblance of control. Time for him to take another peek over the top of Adrians wall I suggest.

Lowering interest rates and higher house prices have really become a self-reinforcing cycle over the last three decades. The more debt we have the lower interest rates we need. In many ways I hope inflation does pick up over the long term but, aside from demand shock caused by excess monetary and fiscal stimulus, I just don't see wages or productivity rising to support inflation over the long term. It seems more likely trends will persist to me.

It's actually very difficult to gauge where Western economies are with LSAP, FLP and stimulus measures still in place.

Arnt all the Mortgages stress tested at 6% anyway, so no problem right?

The test rate assumes all the consumers other spending remains at current levels. A 5 or 6% mortgage rate alone may be sustainable but if all other spending rises due to inflation all bets are off. Banks just have to hope wage growth is higher than inflation growth in reality, stagflation would be really painful.

Surplus just needs to be greater than 0 at 6%. Personally I don't think I'd be comfortable with a surplus of $0.

So far as I can tell, the bank also doesn't mind if meeting your repayments involves you only eating instant noodles.

Retail banks do but other lenders not so much. That's probably a small percentage of lending anyway.

Dear Interest.co

If rates do rise, the fantastic intellectuals behind NZ media will pump out the doom and gloom of how tough it is going to be on mortgage holders. Perhaps you could make a special note to buck the trend and to pay attention to some facts:

- Every single mortgage taker has serviceability tested by their bank at higher rates e.g. 7%, not the current 3%. Unless the media insists on telling them they are victims, they could knuckle down and meet the challenge.

- Mortgage holders have the opportunity currently to lock in a 5 year fixed term at a very good rate (Does someone have the numbers to demonstrate what this will save if a significant rise does appear in the next couple of years?)

- Every* FHB jumping on the ladder shut their eyes and said "we have to take the risk" when they put in an offer far beyond what their gut instinct says. And every one of them is matched by someone who missed out on a purchases because "its too much, not worth the risk".

- Some people took our their mortgage (or upgraded mortgage) more than 2 years ago (shocking isn't it), and since then their mortgage payments have... decreased. Or stayed steady. There has been inflation, there has been wage raises (especially in the jobs where property owners are realistically found). It is possible that these people increased repayments or savings such that their capacity to pay higher interest rates is ready and waiting to be used.

- The average kiwi does not give a flying f*** about property investors, at least those who aren't "in it for the long haul"

Looking forward to the never ending saga of interest.co.nz property-article comments over the years to come :-)

Simon - in the calculations of 7% interest rates, does that assume that they've applied the fact that inflation would be high (with no guarantee of pay increases matching higher inflation) meaning the amount of pay left over to service a mortgage is reduced?

Or is it assumed that if we're at 7% mortgage rates, that wages are going up proportionally to match the general price inflation in the economy?

An interesting question. I think that banks are probably not sophisticated enough to make a link between possible future interest rates and inflation. When they look at your bank and credit card statements they could in theory forecast the likely affect of inflation on your future cost of living, e.g. That new TV/toy spending isn't going to go up, groceries/power/essentials would go up whereas entertainment costs could probably stayed fixed if you think of that number as a set budget?

At best, given that banks want that mortgage business so desperately they might have already been adding 1 to their serviceability test to see how the mortgage holder's numbers look when squeezed to a rate of 6% plus a little bit more by the pressure of inflation.

Its a quite important consideration because if stagflation is coming up, mortgage rates could be a 7% and the cost of all your bills are up by the same amount, but your take home pay is static. At that point it will be do I buy groceries and pay the electricity bill, or pay the mortgage.

There, you see you brought it back to me again: Image of shivering millionaires in dark, recently purchased, shitboxes chewing on boiled wall paper. (Dago suggested Dux piping might be more filling).

At least in the 70s they could have planted up the garden. Now the garden has 2 townhouses and a driveway on it, maybe a caravan.

It's not about people losing their homes, it's about disposable income plummeting, leading to low consumer spending, then business losses, then job losses. So it affects everyone, including those without property.

"Interest rate rises will be a big test for Kiwi homeowners

If the current wave of inflationary pressures prove to be more than just a passing flurry, the Reserve Bank will be forced to raise interest rates"

Exactly for this reason government and rbnz should prevent many from over borrowing. Many under FOMO are borrowing in extreme and any minute change in interest rate or individual situation will be a disaster. One may not drown in five feet water if does not know swimming but than any additional inch rise will be fatal.

Better to have DTI restraining from over borrowing as it is beter to be without house (though frustrating and not good) than having a house with high mortage and repenting afferwards if interest rates goes up or individual situation changes and both are likely as mortage is not for short period but for long 30 or 25 years.

To contain FOMO, it is important that demand, specially speculative demand is targeted otherwise no policies or announcement will help. Instead of passing the buck both Mr Robertson and Mr Orr should work together and DTI is necessary to avoid borrowing in extreme and controlling interest only loan is must to tame the ever rising house price and therby FOMO.

Many speculators are able to speculate only because of interest only loan and by removing it to investor, any decline in speculative demand will go a long way.

Only problem : Perception is lack of intent more by Mr Orr than by Mr Robertson.

Conclusion : Both DTI and Interest Only Loan have a role to play and will compliment each other but should be implimented as soon as without giving window of opportunity to exploit specially to new loan.

https://www.interest.co.nz/property/110455/over-two-thirds-auckland-fir…

Experts on interest.co.nz if have answere to : What is the point of having data / information and awarness of the danger possible in future, still not taking any action. Why?

No kidding? Little concern for elderly on their incomes when rates were plummeting and many don't have the ability to get a job.

Given that 30%~ of loans are being taken out on interest only terms I'd suggest doing the same calculations with that in mind.

IO loans monthly payments will rise far faster as interest rates go up.

Stop with all this scare media and writing about increases in the OCR it can not happen while the RBNZ is printing 400 million a week into NZ economy, if the OCR increases as all these so called experts which past history shows are never correct in their predications say then increasing from .25% TO .50% has just doubled the governments interest on their debt and further increases will keep doubling until the government is broke and reached its credit limit. Its not going to happen anytime soon so stop writing and making up news stories which arent not factual.

The government doesn't pay 0.25% on it's debt, and it wouldn't double overnight if the OCR went to 0.5%. You could start your research here if you want to be a little more educated on the topic - particularly if you are also complaining about people making things up which are not factual. Note that the interest rate the government pays is fixed for the term of each bond they issue, so changes in prevailing rates only slowly roll into the effective interest rate they pay overall.

https://www.interest.co.nz/charts/interest-rates/government-bond-rates

I thought high inflation is good for those with lots of debt, as then the money owed is less in real terms? So any increase in interest will be off set by the money owed in real terms? I suppose this assumes that wages keeps up with inflation.

Quite a lot of talk about stagflation coming up - rising costs, but static wages.

The current inflation will last as long as the the stimulus continues. Hopes in continued inflation depends on a new QE.

Amazing how all of the caring DGMs are now out for blood at the first hint of a potential head wind. Law of the jungle is OK when it benefits them and their rapidly devaluing house deposit in waiting. Unfortunately for most however, they will continue to convince themselves the great reset is coming to justify sitting on hands. Only room for so many in the property party- positive attitude and a bit of foresight needed. Sorry Tom and Beck you miss out!

Behind all the bluster I believe you are worried. The inflationary pressures are just beginning to build. Short term thinkers can’t see their hand in front of their face.

There are 2 generations now of 'caring DGMs' after blood. It will go their way eventually, either market driven or politically driven. They will get their turn after being screwed by their parents and grandparents.

Hyperinflation coming hard right now. If Orr fiddles while NZ burns he is absolutly not representing NZ tax payer interests, instead choosing to burn NZ at the altar for global debt interests and proxy speculator risk. Aka a sell out.

Will be interesting to see what happens. Popcorn.

My expectation before interest rates rise is that the target range for inflation will increase from 1%-3% to 2%-4%

Orr has made his bed. Unfortunately, we will all have to sleep in it.

You run a recklessly ultra-loose monetary policy, you expand the monetary base like there is no tomorrow, and then you pretend surprise at the inevitable outcomes: it would be funny if it was not so dangerous to the future of the NZ economy. I wonder if the clowns at the RBNZ are utterly incompetent or just disingenuous.

They have a stark choice now: raise interest rates now and hope they will be able to manage the coming inflation and the popping of the NZ housing Ponzi, or "see through it" and be forced later on to increase rates at a much higher level, and as a result witness a potentially catastrophic bursting of the housing bubble.

There is no free lunch: if an ultra-loose monetary policy was the solution to economic issues, then Germany's Weimar Republic or Mugabe's Zimbabwe would have had different outcomes.

An ultra-loose monetary policy now inevitably means a restrictive monetary policy later on. When I think that there even were some commentators (most of them self-serving specuvestors) calling for the idiocy of negative rates, I just shake my head.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.