Anybody remember the old 'Claytons' adverts?

These advertisements for a non-alcoholic drink that nobody remembers featured a line that is remembered: "The drink you have when you are not having a drink".

I was instantly reminded of that when looking at the proposals from the Reserve Bank for the introduction into its 'macro-prudential toolkit' of a debt-to-income ratio measure.

The background is important here. The RBNZ said it wanted a DTI. The Minister of Finance Grant Robertson said he was fine with a DTI that applied to investors but didn't want it to apply to first home buyers.

The Reserve Bank's answer to this arm wrestle is seemingly a DTI measure that will be applied generally - but be set at a level that won't impact first home buyers.

The RBNZ regards a debt-to-income ratio of five or above (IE a loan of five times annual income or higher) as being a high DTI.

Internationally, DTI measures that have been introduced have targeted levels of five, or even four.

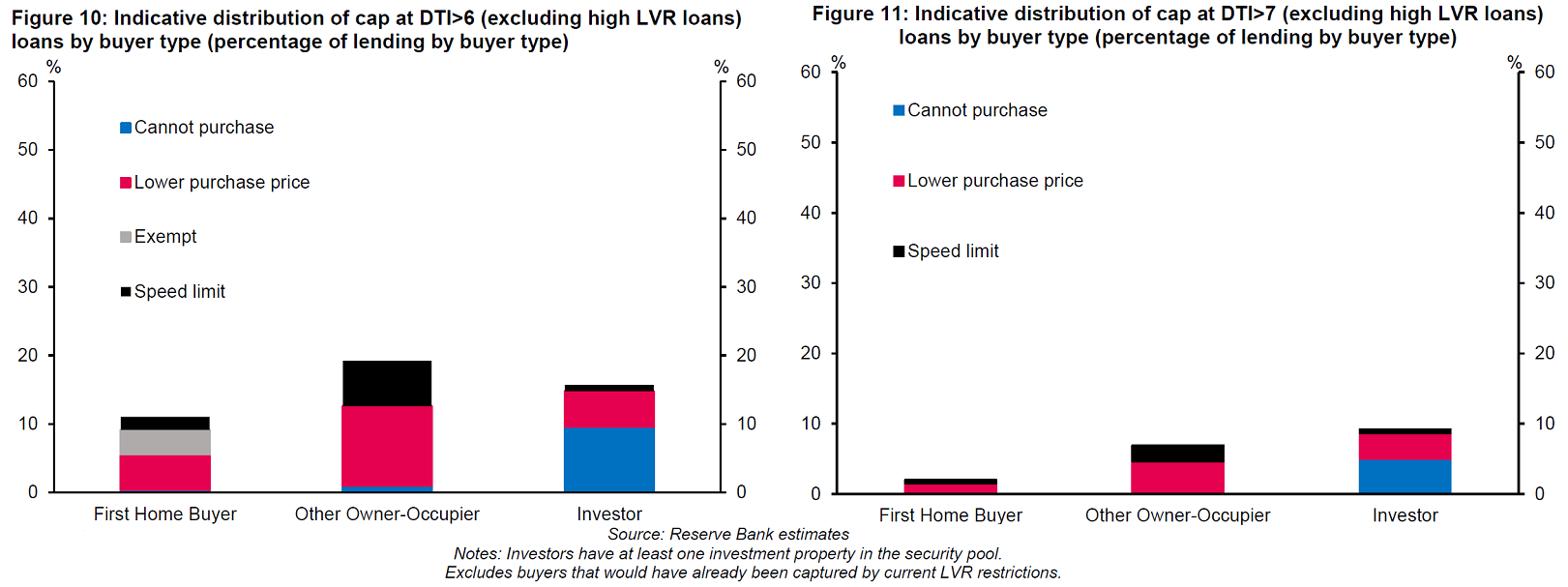

It seems clear from the supporting material that the RBNZ issued on Wednesday that it's now aiming, at least initially for a DTI of no less than six and possibly even seven. And it's produced figures that show if a DTI was set at seven it would not stop any FHBs from buying - but would be effective against investors.

The RBNZ has been collecting information on DTIs for a little while now.

And these figures have been blowing out quite alarmingly in recent times.

And of course at the centre of it is the FHBs. But Robertson has said he doesn't want them touched. Problem.

So, potentially by setting the level of the DTI above that which might affect the FHBs, the RBNZ is hoping to at least get the DTI measure officially introduced into its macro-pru toolkit and then once it is there then so it shall stay.

It has been a struggle of course. The RBNZ first tried to get a DTI measure included in 2017 and was knocked back by the previous National Government.

The latest iteration of a DTI measure is then what the RBNZ feels it will be able to get through, although clearly there's still water to go under the bridge and final sign off by Robertson required. And clearly he's still going to take some convincing.

Assuming this does go ahead and we do get a DTI applied - possibly within a year - then it's going to be set at a pretty high level that will in effect only really inconvenience investors.

Again, I do wonder whether the Finance Minister's 'hands-off' approach to FHBs might not end up doing anybody any good. It does mean that, assuming all goes ahead as currently intended, the FHBs will still be able to borrow at pretty high DTIs into a housing market that has risen by 30% in the past year and in the face of potential interest rate rises from next year.

It's risky.

The flipside to all this is what impact another measure aimed at investors might have on the whole housing market. It does run the risk of becoming the old sledgehammer to crack a walnut thing. Albeit that the walnut, in the shape of NZ's housing market is proving pretty resilient.

Anyway, presumably the RBNZ's thinking is that once it has a DTI as one of its registered macro-pru tools then it will have it for good. And presumably the levels at which the DTIs could be targeted could be reduced at a later date.

In the meantime its just going to be another thing aimed at investors and the FHBs are going to be left to their own devices largely. I just hope that all goes okay.

72 Comments

What nobody seems to realise is that first home buyers can have more restrictions and still be better off. Encouraging astronomically high debts with an artificially constrained number of houses is not what anyone needs. If the debt is reined in, houses can return to sensible values and DTIs, and then fhbs will be back in.

I think their aim is more to do with increasing FHB % stat, and doing this without reducing house prices.

You don't want to put an end to the hunger games, but giving the weaker players bigger weapons might make the games more fun

FHB have not disappeared, quite the opposite, Interest publshed an article showing the proportion of FHBs has doubled in the last 7 years, which is great

The thing is that existing property owners love FHBs, because they are the ones who need to buy in at these insane high prices. So if they stop buying, then the market could crash, as often when someone is buying a house, they have to sell a house, and at the end of the chain is often a FHB. So the government don't want them not being able to afford to pay these insane high prices.

Yep. All of the insanely high prices I was offered last year were from FHBs. So were the high ones for that matter.

Arguably First Home buyers have a lot of control. If they all group together and refuse to buy houses at these crazy prices, they could stall the market and potentially cause house prices to drop. But getting a huge mortgage in NZ seems to be like a badge of honour.

Also what nobody seems to take into account is that the RBNZ's primary responsibility is that of financial stability. First home buyers being able to significantly overstretch e.g. have a different DTI ration, would not be in keeping with that mandate.

Even from financial stability point, DTI should have been implimented long time back but still better lafe than never.

If RBNZ was doing their job properly to maintain financial stability they would have ended interest only mortgages. But instead they are trying to convince us all, like we’re a bunch of idiots, that there isn’t the slightest bit of risk there.

Exactly. Robertson needs to stop pretending DTIs are a curse on FHBs, and start seeing them as a blessing.

Equally so do FHB. The screaming and crying that accompanies any hint at an attempt to stop FHB over stretching and pull the market back is pretty over whelming for even the most dogged poly

All this macro-prudential pfaffing around will achieve is to keep interest rates very low and create a moat between those in the market and those not.

If you're plan is to sit and wait for the RBNZ to bring prices down, you need a plan b.

Robertson is not interested in the genuine welfare of first home buyers. He is interested in harvesting votes first and foremost and the typical voter does not have a very developed ability for critical thinking.

When you look at his actions through the lens of virtue signalling makes more sense. Totally unfit for office.

I agree, people are spending what they are allowed to borrow, rather than what they can truly afford and this is driving up prices. Reduce the ability to borrow and the price comes down. UK DTI is generally 4.5x household income. In most areas of the UK you can buy a better house than in NZ for equivalent money. I married a Kiwi so moved to NZ for love, not for a warm dry and affordable home!

You cant compare UK and NZ housing markets as UK home buyers can walk away from mortgages by simply handing over keys to banks . Saw this in early 90's when i worked there. Try that in NZ at any time and the outcome is completely different. Assuming a DTI of 6 is not going to make any difference to FHB's in any of the major cities as it wont get you a shack.

If you were to open up the market via immediate RMA reforms you might achieve something in terms of supply but this government has no idea what its doing in terms of strategic planning. Look at Kiwibuild and the subsequent performance of the Min of Pies.

By the time they get around to implementing DTIs prices will have increased so much that even 7x will not be enough for first home buyers.

Imagine how much of a better place New Zealand could have been with a competent finance minster and reserve bank.

Robbo's got a pretty thin CV. Done sweet FA after being groomed for politics after graduating from Otago University (some prize plonkers in OUSA politics over the years but it always seems to open doors for people later on, even if you are average or mediocre).

Who is to blame J.C.

We the people. People voted and got what they deserve for their poor judgement.

@alittle 100% true

Unfortunately Labour are likely to be voted back in. A lot of the older generations are doing wonderfully though, PM Ardern is even building them their own special boomer bridge.

I actually wouldn't be surprised if towards the end of the decade, NZ gangs are running large chunks of NZ, it really is the only logical conclusion at this point.

Unfortunately Labour are likely to be voted back in.

Yes. Not sure what really makes a good Minister of Finance anyway. You would think an accounting background for a start, but you then also need a good head for economics. Robbo's got neither, particularly the latter. He just does blindly accepts and adheres to the Anglosphere dogma that is driving inequality and potentially sending the economy to ruin.

We hardly have much choice do we. A choice of mediocre centrists vs mediocre centrists, in terms of the main parties.

Q:What to do when you get a tool that enables you to do something you don't want to do (restrict lending):

A: Set the level so high it doesn't actually have any effect.

Finance minister looks to be doing something, RBNZ looks to be doing something, ponzi continues - everyone's a winner!

Remarkably, even at a high level like 7 to 1 this would have prevented 33% of debt raised by investors in March. A useful tool. With any luck the levels can be brought down over time as the market adjusts.

Anything is better but will this men act. Doubtful. Will try all trick to delay and avoid.

A tool from a tool.

There must be plenty of investors that either don't have any real income (live off their capital gains etc) or don't have enough income to buy another house at almost any DTI. So it is definitely possible to set a level that does not touch FHBs but does stop the worst investors.

Either way, it is another bullet to the chest of property investors. At some point they will realise that the machine gun is going to keep firing until they surrender.

It's a crude execution of how Trump lives, except NZ is a nation of baby Trumps. The banking system is geared to lend more money into existence based on an existing housing stock. The more of the piece of the pie you have, the easier it is for the banking system to grant you more credit (on their fictitious 'money'). Not really any great obligation to pay it back as long as the regulators are sweet with it all (the banks control the regulators anyway and the RBNZ seemingly kowtows to the banks). It's all quite farcical.

Most investors do have day jobs, they invest on the side. They need cashflow from the day job to justify being able to get a loan

But at 7x DTI you would need a very good day job to buy more than one or two rentals.

From what I have seen is those investors already live outside the warm blanket of the regulated banking market and work through second tier lenders or private money. Will this push more investors in that direction? Probably. When theirs money to be made and people willing to invest, they'll find a way as long as the risk is priced in and the return justifies.

I agree, with a rental yield of 5% and a loan of 60% of the property value, you're effectively buying at a DTI of 12. You can put income from your regular job towards it, but that will only stretch so far, and you probably have the house you live in weighing against that too.

"Daddy, what's DTI?" It's called the stitching up of the Kiwi FHB.

"The Reserve Bank said that as of March, 33 per cent of investor borrowing, but less than 7 per cent of borrowing by first home buyers, was at a DTI of more than seven."

It is clear who is being targeted here. No doubt we'll hear lots of whining from investors crying crocodile tears for FHBs as they know they'll get no sympathy themselves.

Check out the comment section on Stuff on the equivalent article. Don't forget your tiny violin though.

"Grr Government bad! Manipulating the market grr! I'll sell. I swear I'll do it! Any day now..."

He has signed a document saying he has agreed “in principle” to add the tools “on the condition that it is understood that the Minister's agreement is predicated on any implementation being designed to avoid impact, as much as possible, to first-home buyers”.

This DTI talk is just to distract from housing ponzi attention that is now covered by even world media.

If serious DTI would have been implimeted and both Mr Orr and Mr Robertson would not play cat and mouse game - running in circle.

DTI of five is alarming but still in this high market, is required but to think of six or seven violates the very purpose of DTI. This bunch of jokers are making fool out of everyone with no real intent.

Need of DTI is now to put a break on house price - to test if it will work or not and not in distant future.

Both this gentelmen have time and can sort out to impliment from July, even if it does not help will atleast send a signal that this #$%@ are serious ( sorry have to use but this type of people understand no other language).

If one reads the article, gets a sense that everything is HYPOTHETOCAL.....really what were they doing till now.

Mr Robertson and Mr Orr should sit together instead of shitting and sort it out in a week as does not need ages with all information and data in public domain for them to decide.

Mr Orr is doing politics to satisfy his bloated ego.

The fundamental question is "what is the main purpose of the DTI's" ?

1) is it to protect buyers from over leveraging and getting in trouble when interest rates rise?

2) is to to stop investors buying houses to provide rentals in the hope these houses will be bought by FHB's ?

DTI is must to protect buy from over leveraging under FOMO - which is such a strong emotion that rational thinking takes back seat.

Investors may not be much be effected as have rental inome to add to their exissting earning but speculators / flippers may be effected.

Still feel that interest only loan - though is good tool for emergencies will be the best tool to target speculative demand. Mr Orr is very well aware so will never act on it.

Since ages Mr Orr was asking for DTI, knowing very well that politician will not give in but now when Mr Robertson has agreed reluctantly with deep heart, Mr Orr will play hard to crack.

No it is 3: Stability of our financial system. That should be the start and end point of why the RBNZ implement such policies. If this has a by product of also affecting 1 and 2, so be it.

If no one can afford the house due to dti measures, inevitably the price heads south. Land will lose value.

Hopefullly both

But hang on a minute how is this going to work when the average house is a million bucks and say you have a combined income of $120k x 5 as mentioned DTI =$600k that means you will have to save $400k for a deposit. Thats going to be a complete balls up.

It's ok. The wonders of modern medicine mean that we all live longer and can spend more years saving and servicing a mortgage before finally retiring in comfort at the venerable age of 115.

Having had 5 years mortgage free

That's around the limit of our body's ability to repair itself. Still, your 85 year old children can inherit your house and flat together for the next 30 years

https://www.nature.com/articles/d41586-018-05582-3

1 mill purchase ,200k deposit ,800k loan. DTI of 7x ,on 120k combined income,ALLOWS 840k loan, So it is doable for FHB

Investor buying additional 1 million rental,using recent equity increase on current home and investment portfolio...still, do they need to have an additional 120k of annual income showable,when the rent on the 1 milliom ROTbox is only 35k a year ,and assessed by the bank at 70 % of that?... Investor stopped in their tracks.( And what happens to dear Investor when wanting to re-arrange existing inter-connected mortgage securitues ,across the rental portfolio...does thecwhole shebang come unwound as they have 5 million of loans but only 100k of assessable rental stream?... Haha,hope so. Investor fully fooked

Exactly. This is a very targeted change. Does Orr have the stones to implement it. Will be interesting to watch the stock price of NZ banks over the next couple of months.

2 * 60k income with student loan and Kiwisaver gives $7k net / month.

Mortgage repayments on $840k at 5% interest over 30 years is about $4500 per month.

That's not "doable", that's grossly irresponsible. Throw in rates and insurance and you're living in poverty.

Try again. At 2.25% those payments are down to $3200/month, and half of that is principal repayments.

Why is that house a million bucks again because its clearly not driven by income. Its been driven by cheap debt leveraged speculation.

If you cant meet the new equity outcomes (most wont), the speculative position has to be exited at a price point where the market can afford. Speculators have been avoiding tax as part of their model and all vote national so this wont cost many votes. Ill bet a lot of accountants are getting calls today.

Yup,agree fully,it has many beautiful facets ,this DTI game,if implemented,as capitilised yield is going to require that artificial 1 mill box to be back around 650k, and thats not including no interest cost deductibility,at all,in 4 years time,( whicj might put it back around 500k,perhaps..) and FHB'S should rejoice at the prospect. Keep saving!!

Hilarious good luck with your wish but you'll be wishing for a very long time.

400K DEPOSIT needed,80K FOR AN EV and rent of $500/$600 a week,no sweat saving a deposit.

That's the whole point! If the average house is $1million and then suddenly a whole bunch of people can't afford that, then the house is no longer worth $1million! It's worth what people can afford to pay for it. This will be good for everybody.

How does it work. If an investor buys a house can they use the income from the housing rental in there calculation of income? Or is it only there personal income.

Yes,they can ,and they do,but it is a fairly limited and decreasing additional benefit,and decreasing per each new acquisition. Hence DTI affects the investor disproportionately to FHB .These are all simple sums.

Is there much evidence of corporate pension funds buying up residential property in NZ, e.g.,

https://www.wsj.com/articles/if-you-sell-a-house-these-days-the-buyer-m…

https://www.theguardian.com/commentisfree/2021/jun/15/do-millennials-pr…

Australia is going ballistic

https://www.youtube.com/watch?v=VDTL-MqTz04

When can this end...can't we have a price drop for a change. Aren't we getting bored of continuing house price rising.

INTEREST RATES NEED TO RISE....NOW!!!!!!!!!!!!!!!!

Well, better than nothing. Even at 6 or 6.5, it's going to crimp the middle part of the market and also take out many investors.

.

So DTIs are now in vogue and LVR out the window.

DTI will make no difference. The market is slowing naturally because the recent gains are simply not sustainable. Expect it to really flatten out by the beginning of 2022. There is a lot of uncertainty being generated in the market so it will hit pause. The government will of course claim success but in reality its already to late anyway. They could have nipped this in the bud 6 months ago by raising interest rates but they sat on their hands. We have a problem when the powers that be see rising house prices as being good for the "Economy".

Carlos. Even if prices only go flat why would investors stay. There is no money in renting, the benefit comes from capital gain.

No price rises and the "For Sale' signs will go out. Good.

As Ive said a number of times...

DTI in the only tool that sets the housing market to wages, so is easily the best option.

You can always start with a DTI of 6.5 or 7 and then reduce it by 0.2 per year until you end at your desired setting. putting a DTI in now at 4 or 5 would be too disruptive

This is another example of adding inefficient & ineffective complexity to the system.

Using DTI is an example of costly micro-management by this government.

Increasing interest rates is the obvious way to control house prices.

The government’s effort to improve affordability for First Home Buyers has failed & resulted in a crisis for renters and those in emergency accommodation.

Rents will rise faster than they would have if interest deductibility rules had not been introduced forcing more people into costly emergency accommodation.

Supply of lower end rentals will diminish as landlords abandon this type of investment due to the tax changes & risks around getting good tenants. For these people this will be a crisis never seen before in NZ.

If the government had carried out due diligence with a benefit/cost analysis on this it would have never gone down this path. Almost no benefit for First Home buyers & a huge disbenefit for a large number of renters.

The real solution is to get out of the way of the market. Allow builders to build. Let the supply catch up with demand.

Where the are banks (the people who actually lend the money) in all this? Clearly they're happy with the risks they take (possibly given the short tenure of management and their incentives) and set their DTI's higher - but collectively, if they're wrong we're all in trouble. The better solution is not DTI's but to impose even greater capital charges on riskier borrowing and let market forces decide where to allocate scarcer capital. If that means lending via shadow banking and informal channels then that's OK because the lenders won't be bailed out.

Okay David, what you and Labour and RBNZ and all you reporters and economists miss, is that this crack down on property investors, being similar to what was done to a certain racial group in WW2 germany, is basically shooting yourself in the foot. Housing supply is the issue, and who creates that, well its mainly property investors with funds. The more you limit property investors lending, cashflow, legislate against, the many attacks against them. The ability of property investors, to build more units, create more housing, is savaged. Resulting in LESS houses, and a greater problem. If investors are helped, instead of attacked, they have the ability to create new housing stock, in fact, they create so much, that supply then exceeds demand and prices go down. Since Labour started cracking the whip, all its done is increase house prices. If you look at the shortfall of housing in Wanaka for renters, that was caused recently, by Labour, no investors want to rent out their houses as they might not get them back, they are all going short term stays, or not even renting them. What happened to the backbone of our country, the free market capitalist, we are now run by socialist communists. Who is going to build the houses, when Investors and developers are spanked out the park. No one. Which first home buyers are they trying to help, most cant manage their monthly phone payments, how can they manage a house. Its really only a marginal group of complainers who cant be bothered saving or living in Massey in a shit box for 2 years like I did, they want to start off in a nice house and nice area.

what a funny post...

go on...we could all do with a bit of laughter from another perspective

the free market capitalist who gets 3$B a year in rental subsidies...

the property developer who cant build a house that kiwis can now afford...

the property developer who needs the reserve bank to lower interest rates to keep the whole show running year after year...

crying for the free market

too funny

If you want high house prices and high rents, keep doing what their doing. I dont mind. If you make land easier to build on, council easier to work with, people able to go about their own business without being punished and red tape, then more cheaper houses will be built, too many, and house prices will go down, as well as rents. Just like happened in 1996 with the Asian Crisis. Once rents go down, house prices follow. All the socialists and communists are doing comrade GNX is making those things more expensive.

Interesting theory. Isn't it incredible that despite the attacks on investors you compare to the Holocaust, we're building more houses than we have in decades?

https://www.interest.co.nz/charts/real-estate/building-consents-residen…

Perhaps the disconnect is because most investors don't build houses - they just buy existing homes. New measures like interest deductibility deliberately exclude new builds to encourage investors to be part of the solution rather than part of the problem bidding up existing houses.

As a side note, I'm an investor in a genuine developer, CDL Investment (CDI on the NZX) who are trading at pretty much an all time high. Actual developers are doing absolutely fine in the current environment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.