By Bernard Hickey

The Government's pre-Budget announcement of its 2-year 'bright line' tax on capital gains by property traders surprised a few people and was the major focus in the ensuing coverage.

But the accompanying news that any non-residents buying property here would have to first open a bank account here, get an IRD number and then declare their own passport and home tax details when they bought the property may actually have more of an impact.

The Government is privately pointing to this measure as having the most potential to reduce some of the foreign demand for Auckland properties and Prime Minister John Key has indicated the information gathered on non-resident buying would be gathered and published. Mr Key made clear on the day after the announcement that New Zealand tax authorities would be happily sharing these details with foreign tax authorities too.

The message was unmistakable. If the money you're using to buy New Zealand property was not earned legitimately in your home country and it's being stashed in the form of a two-bedroom brick and tile in Pakuranga or an Epsom villa then expect your government at home to find out about it.

The elephant in the room of Auckland's property debate is whether some of the money pouring into Auckland from China in particular is effectively money laundering of ill-gotten funds. Without any data, the debate is fuelled by anecdote and rumour, but it is an issue capturing more and more attention around the world.

Mr Key was personally made aware of it by the most knowledgeable source in China -- President Xi Jinping.

Last November the Chinese leader asked for Mr Key's help to track down a number of Chinese nationals who had fled to New Zealand with corruptly obtained funds. This was part of President Xi's now famous campaign to crack down on the 'tigers and flies', the officials and their cronies who have obtained funds corruptly. His first campaign was called 'Operation Foxhunt' and the latest version, Operation Sky Net, was ramped up in April with publication of a list of China's 100 most wanted.

New Zealand was the third most popular destination on the list, which estimated between 11 and 20 were hiding here with their funds.

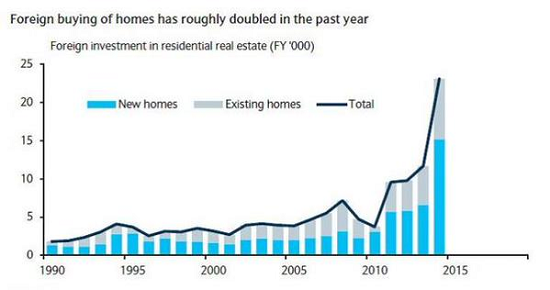

The issue of money laundering from China is heating up in Australia too, where data on how much property is bought by non-residents is actually collected (see graph below). Over 25% of all new and existing homes sold last year in Sydney and Melbourne were sold to non-residents and many are asking where the money came from. It has sparked calls for tougher laws governing money laundering.

This is where the money laundering issue becomes more topical and direct for New Zealanders, and in particular the real estate agents, solicitors and accountants who are currently handling any money flowing out of China and into New Zealand.

New Zealand introduced tough new anti-money laundering rules for banks, insurers, finance companies, share brokers, fund managers and even loan sharks in 2013 that means they have to ask much tougher questions about who they open accounts for and where the money comes from. It was a big deal for them and cost tens of millions to retrain staff and rebuild systems. It's part of an international effort led by the G7, which developed a Financial Action Task Force to push the measures along.

But a second phase of the anti-money laundering crack-down has stalled. It was designed to pull real estate agents, solicitors, auctioneers and accountants into the net so they would also have to verify the source of the funds being used to buy property and other assets here. There was initial talk it could be introduced last year, but the Justice Ministry is still only talking about doing policy work on the options for phase two.

The Government needs to crack on with phase two of the money laundering reforms to follow up its good work forcing non-resident property buyers to say who they are and to obtain an IRD number. It's another great way of reducing demand without having to introduce a politically and diplomatically difficult tax on non-residents. And it makes us a better global citizen in the eyes of the G7's taskforce, which has already had to hurry us along once before for being too slow to introduce the first phase of anti-money laundering rules.

----------------------

A version of this article also appeared in the Herald on Sunday. It is here with permission..

54 Comments

Intended consequences?

A friend in Tauranga has witnessed what the recent changes to the LVR Rules have done down there.

The property next door has just sold and settled quickly after being on the market for some time. The agent duely put the "Sold!" sticker on. Soon after, the new owners took possession and peeled the "Sold!" sticker off. They also showed 'intent' by listing it at a high rental price ( keeps those pesky tenants at bay), and....stuck it straight back on the market, with the same agent ( saves changing the signage I guess!) at $100k more than last week.

Is this what the RBNZ had in mind to protect the NZ financial system with more robust property rules?

I am hearing similar thing happening in hamilton, napier and PN now too. With interest rates seen to be low for another 5 plus years looks like equity rich aucklanders are finding the rule changes no problem; they'll just make their $ in the secondary cities instead for the next few years

Clearly the Real Estate Agent was working in the best interests of the first Vendor to get maximum price.

Ya right.

The Real Estate industry will be milking the market for all lits it worth.

After another sale last week, I have former Chinese national owners as both my neighbours in a modern estate in Rodney (Millwater, also known by me as Mingwater). The owners are usually absent. They arrive late at nights and are never seen during the daytime. I would love to know who they are, what they do, or what they are up, but their English is very poor, and whilst polite when addressed, they avoid attempts to be sociable, so I couldn't tell if you if they are dodgy or not. Neither could anyone else (could be financially innocent, they might just be vampires). I don't resent immigrants, we're all immigrants here, my area is like the UN, but some transparency and accountability, and official reassurance that everyone is here legally and fairly might help integration of those from China. I had to prove to immigration that I could speak English when I arrived in 1999, despite arriving as a marketing bloke from my native UK, so I do feel a bit short changed there. Mind you, most native NZers wouldn't have met the immigration requirements in 1999 either.

We aren't all immigrants.

We are ALL immigrants. Some more recent than others.

Na. Lots of us are not immigrants.

Everyone in NZ is an immigrant. Some of us arrived today and some of us got here around 700 years ago so by that standard compared to almost everywhere else everyone in NZ is an immigrant.

You are an immigrant if you came here from another country - you, not your mum, not your great grandpappy - you

Arrived 700 years ago. That would be the ones from Taiwan then.

If you were born in NZ by definition you are a native (remember your third form Latin...).

My grandparents were all natives, so were half of my great grandparents and two great great grandparents who were born in NZ in the 1850s and 60s (in the earlier case my great great great great grandparents and their children came out from Ireland arriving in Auckland in the 1840s).

Me? ...I'm a native of Invercargill, not an immigrant.

The result would amaze. IRD staff could start doorknocking at the start of Dominion Road . Not missing one. And ask each inhabitant where and how their rent money goes. Then follow that money trail as far as it goes. Some naive simple questions at source. ie. The doorstep. Then a remorseless factcheck through all the layers.

Feathers would fly.

The result would amaze. IRD staff could start doorknocking at the start of Dominion Road . Not missing one. And ask each inhabitant where and how their rent money goes. Then follow that money trail as far as it goes. Some naive simple questions at source. ie. The doorstep. Then a remorseless factcheck through all the layers.

Feathers would fly.

we have been naïve for far to long, if you have people coming from countries of hiding money from the government and under declaring income or profits how is our IRD going to catch them if they don't register. IRD need to have flying squad teams that go through areas and check it against their database

http://www.stuff.co.nz/national/611470/Migrant-didn-t-know-about-tax

http://www.stuff.co.nz/dominion-post/news/9537634/Kebab-shop-owner-sent…

http://www.scene.co.nz/queenstown-boss-convicted-after-160000-in-tax-wi…

They won't be able to buy without registering with IRD? So, could use a single registered person/entity as buyer, but they would still need to account for where they got the money from?

Three probable effects

(a) The available pool of willing proxies and stooges will dry up instantly

because, to act as a facilitator on behalf of the hidden and nameless will

(b) force the proxies to hold the title in their name for some years

which in turn would

(c) drag the willing proxies and stooges to the attention of the IRD

So, a) if its a tax dodge the stooge will be let with the tax bill.

b) if its money laundering end up with a criminal conviction and a tax bill.

c) If the IRD freezes his/her bank account the hidden person may send some 'friends" to recover the $s. So broken bones, missing kidneys, in jail and a tax bill.

Could go well, but yes there are ppl that stupid about.

Dont panic just yet , China's debt balloon will soon explode , its economy could implode spectacularly , and much of this money will simply dry up , and a lot will leave just the way it came

that is where the problem is, if we have another Asian stock crash like 2007, which all the signs are pointing to a lot of money will leave. then if house prices drop by only 10% they will be a lot of people in a world of pain as banks refuse to refinance and force sales

It will be a lot more than 10% when it happens. Interest rates can't be dropped as much as last time.

Paid off one of our mortgages last week. Chatted about splitting the other into fixed and floating portions. Got told not to fix for any longer than 1 year, 6 months was better - bank gearing up for significant drops in interest rates - the figure of 2% was mentioned as a potential max drop and the 'end of the year' was also discussed. We chatted about the craziness of Auckland, got told the bank was gearing up for a worst case scenario of a 50% drop, and were in the process of identifying how many would be under water; was told that we're okay as we have near 70% equity. This is a person I've chatted to quite often when doing our banking, they are on the ball more times than not. This individual was very quiet when warning me not to fix for longer than 6 months, nor to worry about what the coming crash will mean to us as we're deemed one of their best customers, i.e. we owe bugger all, and are putting every bit extra into paying off the mort.

We live in interesting times, and it will be interesting to see whether some of the timelines we discussed will occur.

I find that counter-intuitive. If there actually was a 50% drop in prices (and hence valuations) in the Auckland market - I would assume that interest rates would go through the roof as the exposed banks will have to pay through the nose to borrow offshore given the risk profile of their existing securities. I could be wrong, but it just seems to me that kind of deflation scenario would totally decouple the OCR from real-world interest rates.

Not if its a global event that triggers it, so NZ may still be in relative terms seen as safe-ish.

But, yes generally agree, NZD not a safe haven, esp if the gobal event is related to china/AU our major trading partners. If it's Greek related, who knows how this will effect us; Short term flight to safety followed by further global QE to fight of deflation could see these very low mortgage rates in NZ along with falling house prices. 50% won't happen, but Auck in an extreme risk of at least 10-20% drop at the first sign anything that might spook buyers.

I was telling people on here to buy USD when it was at high 80's, already made 20% plus on that trade, if anything big global happens I expect to be close to doubling my money used in this hedge, which could come in handy if NZ property prices fall

I wondered on that, hence have I pondered fixing for a short time say 1 year. However if it all goes very badly the bank (or its receiver) can cancel the fixed term I believe.

OCR and real rates, yes this seems so. ie in a panic the "loose" money would exit to the safe haven of the USA, at least that is conventional wisdom (so who knows these days).

I assume that no one in the NZ banking industry thinks its can get that bad, just a wee oopsie. Maybe time for the speculators to exit, na greed will win through.

I doubt it would be 50%....but if you were a bank and wondering what might be the worst case scenario, well 50% might be a figure to use. Even 20% will see a lot of people in trouble.

Apra instructed all Aussie mortgage lenders to add 2% to repayment calculations from 1st june. strange our banks same owners are picking interest rates to go the other way.

That is certainly consistent with how fixed interest securities are pricing as of Friday's lower trend close. No matter what central banks attempt to fix at the O/N end of the curve, the longer end has currently been overtaken by sellers short of willing liquid buyers.

hmm interesting

Predicting future interest rates (and exchange rates) is a mugs game. Really it could go anywhere. You might achieve some cost saving, but by good luck only. You might also cost ourself money by fixing, when the tide runs against you.

I recently did some fixing on a new property. But that's because i needed some certainty. I was not seeking to save cost.

True, if I could predict what would happen I'd look up the coming week's lotto numbers - $18 million is not to be sniffed at if you have a crystal ball!

Boatman, I don't really believe China's debt balloon will explode, because in net terms, they owe it to themselves. China is still running a significant current account surplus, and their government is unlikely when push comes to shove, to blow up their economy. They are likely to rein in the provinces, and their property and equity markets may well wobble, with some downstream effects on our property market. But they won't let things collapse as it is totally within their central government power, while they have a current account surplus, to pay or forgive whichever debts they feel like. They may have some interest in making an example of a few not so well connected "crooks", but even there they are likely to be circumspect. If we wish to control our property market, the ball is in our court.

Stephen, debt is a promise to pay in the future and credit (a surplus) is an expectation to be paid in the future. Doesn't matter if you owe money, or are owed, when the future can't pay then it can't pay.

Scarfie, Imagine scenarios where the 23 provinces of China have each overspent on infrastructure, housing, and just maybe the enrichment of some local officials. They have borrowed the money off private investors and the central government, all in Chinese Yuan. The provinces have no way of paying back the debt. The central government wants to stop excessive spending on infrastructure, and some of the local official enrichment, but doesn't wish to slow the economy too much. So what does it do? It prints money and gets it to the provinces one way or the other, is what it does. It tries a Goldilocks approach of just the right amount, and in trying to achieve that there will be some pain. But it has no need to turn the taps off. China in net terms has no debt. In the end it will correctly do what is in its best interest.

Double post sorry.

Those yuan have to be converted to USD, or something else, to buy the oil, coal, steel, or whatever other resource is required, to build that infrastructure. Growth requires the consumption of resources and China is not in a vacuum.

However, the world economy including China has no lifeboats left

http://www.businessinsider.com.au/hsbcs-stephen-king-on-the-world-econo…

The trouble may start with the 4 year concession given to new immigrants for income earned from overseas. We could start by requiring them to provide details of income from day one even while not taxing them at that stage. This would also curtail reported WFF rorts of qualifying even when living in a multi-million dollar house in some circumstances known to local accountants.

Further to sort this tax schmozzel the IRD should be given an open chequebook and base that amount only upon collecting say five times their costs. Then they should use the rules of how assets have been accumulated to determine tax liabilities.

http://www.smh.com.au/federal-politics/political-news/new-plan-to-curta…

If the Aussie pollies have the guts to implement this then perhaps ours' will too!

very unlikely labour or national would do too many fingers in the cookie jar.

it should go though it has lead to distortions and cost the country a lot of lost tax revenue.

they should also look at making sure those property investors that are over the GST threshold become registered

https://www.ird.govt.nz/gst/gst-registering/register-who/

So 25% of all new and existing homes in Sydney and Melbourne were sold to non-residents (and the existing ones are illegal without FIRB approval).

But for Auckland the authorities and talking heads shrug and derp about lack of data therefore its not a problem.

Its a safe bet its the same amount if not more due to the lack of restrictions.

or maybe more because its easier. all that will change is they will use locals to front, same as has happened in Australia that they have suddenly found out

A big danger for locals acting as a front or proxy in the property market, will draw attention to themselves and possibly be audited back 10 years or more. No longer worth the risk

Bernard you seem to miss the point which is why I seldom follow Interest any more. Going a ways back past governments attacked the supply side of the housing equation through building state houses which helped keep the average income to house value steady.

Mr Key and Co. attack the demand side of property through Kiwi Saver and first home with drawls. The young and smart by into the subsidy and vote National (the stupid ones don't). The middle aged and old buy in because they can see guaranteed housing profits in voting National.

In the mean while NZ, in general, follows it's predetermined trajectory down a financial illiterate toilet because the funds which are tied up in property aren't available to be put to a better use i.e. educated business and educated jobs.

JK and National are happy because their beneficiary constituent are the money launderers on top of the dog heap.

The Labour Party are happy because financially they are on JK's side. And they don't really want to be in power and ruin it for them self's.

Receiving stolen property is a criminal offense in this country, which makes the solution to laundered money quite simple. Ignorance is also no excuse and a missaligned price good evidence of the offense.

The stolen property also remains the property of its rightful owner. Given we have such a fair an accessible justice system, if I was a Chinese national or organisation missing funds to New Zealand then I would be pursuing the recovery of those funds via the New Zealand Police and the Criminal Justice System. Any party to have handled the stolen property would also be accountable, which includes bank staff, lawyers and real estate agents.

People go looking for crazy solutions when the tools to do the job properly are right there in front of them.

Hook a few of those retired to Omaha or Pauanui for the proceeds of the sale of their Auckland property and see what that does the values. The best bit about this is that all it takes is a complaint to the Police, something anyone could do, like Problem Solver above with his neighbours.

Nah, I think you'll find that fiat currency acquired by illegal means is not technically 'stolen property' in this definition.

For now..... I perhaps agree. But as things get tight the hunt for money will expand. Unlike the IRD's restrictions, there is no statute of limitations on a crime.

”We look at the housing market like a food chain. The first-time homebuyers are really the plankton. And if you don’t have plankton in the ocean, you’re going to eventually starve out even the big whales and the sharks. You need that first time homebuyer to buy that home so the next person can move out to buy their own home.”

And there was plenty of this plankton, namely millennials and about 250,000 immigrants per year who’re buying their first property, he said.

“There is strong demand in this country and there will always be,” Levings said. “Why? Simply because of our immigration policy. We bring in first-time buyer pipelines through our immigration policy. They are great future first-time homebuyers that become plankton.”

http://wolfstreet.com/2015/06/04/canadian-mortgage-insurer-genworth-tel…

Great link Andrew, thanks. I thought this bit was relevant to us too:

The federal government has introduced several mortgage rules since 2008 to take the froth off heady real estate markets. Shorter amortizations and higher down payments have kept the riskiest of buyers out of the market, Levings said.

The trick is for the government to keep this balance and avoid making further changes that will entirely squeeze out first-time homebuyers and poison the food chain, Levings said.

“We’ve squeezed the first-time homebuyers down into a small group who are qualified, good-quality borrowers,” he said.

http://business.financialpost.com/personal-finance/mortgages-real-estat…

the renters are the plankton. They need little capital to exist (cheap feed) but they don't contribute houses (low energy).

Without them the sharks have to feed on big fish, since there's no little fish.

But the immigrants aren't plankton, they're either wealthy enough to buy a house thus go straight to shark, or they're qualified/needed-skills so go to high paid job, and quickly pay down their first house (so they're little fish who rapidly become sharks/big fish)

So we need some fishermen

lower milk prices to New Zealand producers is poised to hit home, Fitch Ratings said, cautioning of "pressure" on asset quality at banks with significant loans in the dairy sector.

'Significant negative cashflows'

The Fitch comments come a week after DairyNZ warned that, thanks to low milk prices, "we will see most farmers facing significant negative cashflows for much of the next 12 months leading to an increase in debt and overdraft expenses".

http://www.agrimoney.com/news/low-milk-prices-to-raise-pressure-on-nz-b…

Dairy farmers are more vulnerable to rising interest rates than in the past. RBNZ data shows that floating-rate loans amounted to 72% of total dairy lending in June 2014, up from 16% in 2008. Lower milk prices could have an indirect effect on dairy loan asset quality, if lower farm incomes weigh on economic growth and sentiment sufficiently to influence monetary policy and reduce pressure for further tightening. However, this is far from certain. Read article

LOL - does the swap debacle still loom large or are all those floaters the balancing act of a fixed swap paying equation?

Nonetheless, the trend to higher corporate loan cost spreads over US sovereign debt yields will surely not pass local bank scrutiny when it comes to formulating returns on equity.

In fact, one of the oddest things I’ve noticed recently is that it isn’t only junk bond spreads that are moving wider now. AAA spreads versus the 10 year Treasury are sitting at 18 month highs. It might be that this is a result of reduced liquidity in the corporate bond market but I would just point out that the best levels in this expansion are, so far, nearly a full percentage point higher than the last two expansions. A small difference maybe but an important one I think. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.