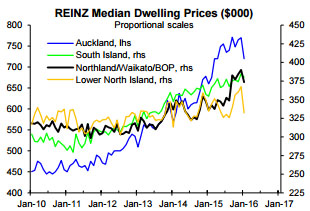

It is also questionable whether the falls in median house prices reported by REINZ in recent months accurately reflect underlying price behaviour.

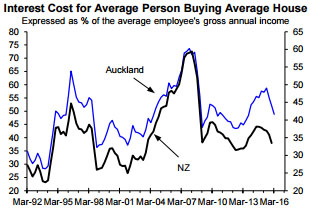

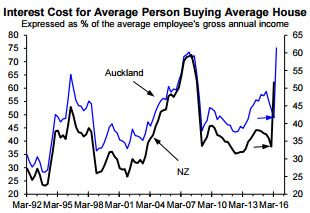

When I look at interest costs faced by new buyers in Auckland and nationally as percentages of incomes, there is no housing affordability problem.

Low interest rates have made housing as affordable for new buyers in Auckland as has been the case on average since 1992, while in the rest of the country housing costs, in terms of interest outlays as a percentage of incomes for new buyers, are below average.

High house prices relative to incomes don't in themselves pose a threat as long as interest rates remain low.

The consensus view is that interest rates will head lower this year and remain quite low. Unfortunately, the consensus view is more often wrong than right.

The Raving highlights this in the context of the consensus view on inflation prospects versus my view. What happens to interest rates will ultimately be of most importance to house price behaviour, with what happens to migration of secondary importance, as covered in our pay-to-view housing reports. But this is in the context of the current starting point being one in which the national demand-supply balance in the housing market is still strong and likely to strengthen as buying by foreign investors recovers.

A surprise this year and beyond should be that house price inflation remains more resilient than the Reserve Bank expects, even when Governor Wheeler is eventually forced to hike the OCR.

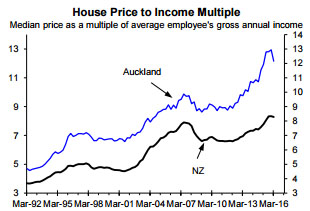

Low interest costs largely justify high house prices relative to incomes

People predicting large falls in house prices because prices are high relative to incomes overlook the massive impact low interest rates have had on housing affordability. The left chart shows median dwelling prices reported by REINZ as multiplies of median individual gross incomes for New Zealand and Auckland. The national and Auckland price/income ratios are well above the levels that existed in 2007 before the last sizeable fall in prices. In August 2007 I wrote the Housing Hell Raving that warned about downside risk to house prices. But do high house prices relative to incomes mean a large fall in house prices is inevitable, especially in Auckland?

It is a very different story when we look at interest costs for new buyers relative to incomes (right chart). The right chart assumes an individual with the median income buys a median-priced house using 80% debt and paying the average current interest rate, with the interest cost expressed as a % of income. Nationally, interest costs relative to incomes for new buyers are a bit below the average since 1992; while even in Auckland the interest cost as a % of income is close to the average level and dramatically below the peak level in 2007.

The irony is that at the same time as solving the housing affordability problem, low interest rates have played a key part in driving house prices higher and making the underlying housing affordability problem worse (i.e. rising house prices relative to incomes). As an aside, I am wary of the recent falls in median house prices reported by REINZ and the related falls in house prices relative to incomes reported in the left chart above.

In the Housing Prospects reports I show the demand-supply balances in the national and Auckland market, as well as assessing house price prospects for most cities. In the March report I showed that the tax and Auckland LVR changes have dented the case for upside in Auckland house prices, but have far from killed it, while in most of the rest of the country the case for upside in house prices remains strong.

Two very different views on interest rate prospects

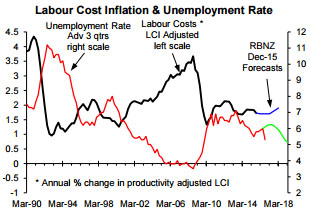

While a rear-view-mirror-based assessment of inflation prospects says the governor should cut the OCR more, a forward-looking approach focused on the core factor relevant to medium-term inflation prospects is starting to politely ring warning bells about inflation rising. The "surprise" fall in the unemployment rate from 6% in the September quarter to 5.3% in the December quarter - red line, left chart below - shouldn't have been such a surprise to the economic forecasters given the rebound in leading indicators of employment growth (e.g. the surge in online job ads reported by the Department of Labour - right chart below). However, the fall in the reported unemployment rate may partly reflect random variation and could be partly reversed this quarter.

The labour market (i.e. wage and salary inflation) is central to medium-term CPI inflation prospects. The left chart below shows the unemployment rate, leading or advanced by three quarters, as a useful leading indicator of the productivity-adjusted measure of labour cost inflation the Reserve Bank (RB) focuses on, as well as the RB's forecasts for both. As covered in our monthly economic reports, there are good reasons for expecting employment growth to be stronger than predicted by the RB and the bank economists, so even if the reported fall in the unemployment rate in the December quarter partly reflects random variation, a key theme going forward should be an earlier and larger fall in the unemployment rate than predicted by the RB (green line, left chart), which will imply earlier and more upside in labour cost inflation.

In the mid-2000s I was a lone voice warning about the upside risk to interest rates, with history repeating itself on this front, although the upside risk this time around isn't as large as was the case in the 2000s, as outlined in our monthly economic reports.

With interest rates so critical to housing affordability, having quality insights into interest rate prospects and the implications for the demand-supply balance in the house market is critical if you want a forewarning of when the current boom in house prices will end, when downside risk to house prices will emerge and whether there will be the risk of a sizeable fall in house prices. These insights are contained in the Housing Prospects reports, while our monthly economic reports provide more detailed insights into what the RB and bank economists are overlooking. Prospects for economic growth, employment growth, consumer spending growth and interest rates are currently very different from the consensus view, which is nothing new given the poor forecasting track record the RB and bank economists have (e.g. use the following link to a related Raving - http://sra.co.nz/pdf/TradeSecrets.pdf).

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

68 Comments

Anything is affordable is the period of repayment can be extended, and this is the prime component that he has forgotten. In the 80's and 90's mortgage periods were 20 - 25 years, today they are more like 50. Some have no hope of repaying their mortgage during the remaining term of their working life - and this is affordable? Banks will love getting their hooks into buyers, as debt is where they make their money. Bottom line I have one question - which bank, real estate agent or property investor group paid you for this article?

"In the 80's and 90's mortgage periods were 20 - 25 years, today they are more like 50"

Rubbish. Most people are borrowing based on 25 to 30 year terms.

Rodney Dickens must either be a property investor, works or has interests in a real estate company or is a friend of the National Party if he does not believe there is an unaffordable problem with housing in Auckland.

We are tired of all this propaganda.

There is no unaffordable housing if you are a wealthy overseas or local investor.

20 years ago the maximum period was 25years at a 80% LVR. A few years ago (pre 2008) 30years and 95% would seem normal.

Exactly steven. I bought my first home in 2006 with a $10,000 deposit... a 5% deposit for a unit in central Auckland. Now 11 years later a FHB'er would need a $100,000 + deposit. It would seem lending is far tighter today than in the past. If I recall correctly it was a type of "no doc" loan.

When did you last get a mortgage? I was not offered 50 year terms when shopping around last year and this year. I might add though for the first time in years I was able to borrow money at less interest rates than I was able to earn on the properties I purchased. I might add these were not houses either. I purchased properties that enable people to work and earn a living from.

Investors be they be into property or industry need to survive. Using sticks and laws to control things is what Chairman Mao in China failed at. Punishing and abusing landlords is witch craft.

hehehe, not 50 years but 30 now seems quite acceptable to the banks.

Meanwhile this paid shill is totally forgetting that repayments aren't the hard part, it's actually saving the deposit and on an avg Auckland property, that can range from 80 to 160K. So who paid you to write this article? I see the Herald is going on full damage control mode and wrote a second article in less than a month about Ron Fong Choy

Foreign buyers, and proxies of foreign buyers, and immigration, and international students (indirectly), is an insatiable demand factor driving house prices in Auckland.

Millions of well-off refugees from restrictive regimes & chaotic semi 3rd world countries are pouring their money into NZ property. With insatiable demand, then interest rates are secondary, & supply will never meet demand.

Other western cities have interest rates of 1.5 or 2% and their prices are no worse if not better.

Saw an article in Stuff a couple of days ago about Wellington market going batsh!t, which included a crappy little shack in one of the least swish suburbs going for nearly $600,000 and another place for $1,000,001. Suggestive, eh?

Interest rates apply only apply to those who have a mortgage. The foreign buyers that have entered the market(many with dubious original sources of the funds) are not interest rate sensitive as they are cash buyers and are literally using housing as a warehouse for their money.

Taking that even further, in a system where 70%+ of money expansion happens through residential mortgages then cashed up non resident buyers will contract the money supply by retiring a local mortgage.

But as can be seen in the M3 money supply, inflation is kicking along strongly at 8%, and has been at 6% average for the last few years.

if money expansion is still happening while measure core inflation is low then the only answer probably left is that the gap is being made up by locals having to borrow more to buy a house. ie: the offshore buyers are increasing the debt burden of locals and compounding the inflationary effect on this asset class.

Agree I suspect..

Stop being a dingis! Go and buy your first home on interest only, and explain how that works. Most banks wont give interest only loans for FHB's and if they do, they are being criminal. Halving the interest rates does nothing to answer the question of how you pay back the principle.

Not to mention the use of some of the most misleading charts I have ever seen. This entire article is PURE SPIN, designed to manage perceptions.

Personally I think the Russian version called 'reflexive control', is far more effective then western 'perception management', but thats a propaganda debate for another day.

I agree being a dingis justifying the massive bubble in house prices is ridiculous.

"Low interest costs largely justify high house prices relative to incomes" No it doesn't. The bottleneck in obtaining consents to build delays new construction. Supply of new housing is heavily constrained which means multiple bidders are chasing the existing housing stock. That is not a justification, it just shows how broken things are.

This article is complete rubbish.

Agreed, existing house prices should in the long run be dictated by the next alternative -the cost of building new houses.

Other long lasting consumptive goods -furniture for example -do not change value because of changes in interest rates. Why should housing?

Which publication represents the young and the lower income people of this country? With this government and this media they really don't stand a chance.

The Standard? but really its, um awful. But if you read it as a comic strip it might be worth a laugh.

Craccum?

People loan as much as one can when interest rates are lower, but income remains the same, static (dependent on job security).

Banks, real estate agents and media band together to manipulate higher returns from what ever source pays the most. Government and council support this by constraining supply by zoning, consents and infrastructure.

The report doesn't acknowledge or understand human behavior when one needs a secure roof over their heads.

I like Rodney's work. He is paid by his subscribers so is encouraged to be useful. His writing style is a bit hard though. Basically he is saying that when the unemployment goes below 5% we will get above target inflation, eventually followed by interest rate hikes. So house prices will party on until then.

The conclusion is correct but the reduction in unemployment isn't going to happen until the Government reduces regulations around building and resource consents. It would be nice to have a right wing Government again.

I used to think MMP was a good idea, and it would be except that it fosters stagnation to the benefit of those who gain from the status quo.

Seems to me we are all rather good at believing in impossible things, like change under MMP. We have mistakenly adopted the US principle of constitutional political stalemate and abandoned the wisdom of the organised chaos of the Westminster system that our forbears developed for us.

It's unfortunate that scoring political points has become more important than helping the country but here we are. It also converted our left and right parties into centre parties that have lost their way.

The worst thing about MMP is that it allows MPs who do not represent the people. You may want to vote, wrongly or rightly but it is your right, for someone of your own ethnic group and the party will select a minority candidate for some SJW or fashionable reason. These candidates are unlikely to act in your best interests.

Hmmm,

MMP is normally used in a two house electoral system but our upper house is strangely silent.

Must make our lower house MP 's job a lot easier though.

Were we sold a pup?

I think he's wrong on inflation, peak oil was a paradigm shift, economy no workie like it used to any more.

I subscribe to Robert Ashton's "Rob report" on house sales in Remuera & Parnell. Rob is an experienced, long standing agent at Bayleys. I was surprised, even shocked to read the following data for the latest Median sale price:

Nov 2015 $1.61 Million (70 sales),

Dec 2015 $1.39 Million (also 70 sales),

Jan 2016 $1.00 Million (40 sales).

Not 1 single month of 2015 had a Median sale price as low as Jan 2016.

This is a quite staggering drop !

I don't know how to attach the link to his email

I checked some of the Harcourts auction results where it states that they achieved an 80% success rate.

Of the four houses sold in Epsom I could look up three and compare their 2014 GV with the sale price.

1690K CV sold for 1900K,

1203K CV sold for 1601K

1950K CV sold for 2325K

Looks normal to me. Spot checks on the others are the same with 100-400K over CV

The sighting of four swallows does not necessarily mean spring has arrived Zach. I think you will find that the owners of average homes in average locations are getting very frustrated over the fact no one is ripping in and buying their houses. My niece has still not sold the property she purchased for close to $2 million last year. Harbour views and the ability to carve up into three sections. Getting close to four months on the market.

I have been doing this checking regularly for the past year. My specialty is lower priced houses made of good materials in Central Auckland though. I do have one in Te Atatu South which I keep a close eye on and sales there show the same ratios if not better. The quote is "one swallow does not a summer make" but I have seen flocks. Don't make me go through the entire list! Would not your niece's property be the single swallow category? Can you tell us the current CV is and what she expects to sell for? I find this is all pretty scientific.

Zach you obviously have no sense of humour. I know the quote very well but was just playing on the four Epsom homes sold. I will be more accurate from now on in order to assist you. Let's just wait and see what the REINZ say later in the week. They are biased but not as biased as yourself. My niece bought in the first half of last year. I think she went one step too far. Put it on the market before Christmas and still not sold. We all know the market is down 8.2 % since October but you obviously cannot accept that fact because if you did you would have to accept the fact that your precious homes are not as valuable as you thought they once were, on paper of course.

You guys test my sense of humour because you appear to be deliberately talking down the market for reasons unknown. Of course this would not make me happy. It is interesting that you are not prepared to reveal the CV. If your niece paid too much and then wanted to sell less than a year later I would expect a loss as normal. I always think I paid 10% too much but I always keep for a few years to counter that.

I would not call you a good investor if you pay 10per cent for your investments Zach. You are down 10 percent October and dropping. Might get o 20 per cent. I hope you did not buy last year.

I probably didn't make myself clear. After purchasing a property I always have the feeling that I paid too much for it. I'm actually quite pessimistic and calculate the worst- case scenario. The vendor didn't accept my good offer and squeezed more out of me. If I had to sell within 12 months the agent's commission and loss would be a blow. However I have no intention of doing this, so all good.

With Gordon's niece I suspect the purchase had an element of emotion and if you really want a place you need to pay over the odds to secure it. This means a loss is generally inevitable if you need to sell within a year. I've known several people do this.

Of course she paid too much for it Zachary. Bought in April last year. Market is now down 8.2per cent since October 15. And will probably be down more when the REINZ bring out their February figures. We are not talking it down. It is down as people got greedy and forgot about how markets operate. The idiots who bought last year in Auckland will only have themselves to blame when some of them are forced to sell.

gordon, please check out recent clearance rates for auctions. Your niece is in the minority category. She is obviously asking too much. With over $100k agency fees to buy and then sell she is on the back foot selling in less than a year.

I think the boil has come off the top end somewhat but fairly priced properties in the affordable category (ha - can I say that about Auckland?) are definitely moving. This is more likely the reason for the declining values you are seeing.

gordon there is only 2 reasons something doesn't sell...1 you have a crap product or 2 its overpriced...

Average family in auck vs. anywhere else in nz, may earn 10% more income, but thats irrelevent.

Look at fhb example with kiwisaver.

3%+3% @ 40K (outside auckland) x2 (couple) x 5 years = 24k.

BUT, add 5k + 5k fhb kiwisaver grant = 34k. Welcome home loan at 10% dep = 340k first home without having to save a cent, which outside of auckland,welly,chch generally buys an above average house, certainly can get a stand alone 3 bed on full section which we all aspire to. WITHOUT SAVING A CENT. easy.

Or at 45k salary in auckland = 27k. Add 5k x2 grants = 37k. Welcome home loan up to 370k. Might be able to buy a studio apartment in auckland but that's it.

To buy 3 bed on full section would be 700k plus. An extra 33k required to be saved. But the real catch: servicability! (Plus kiwisaver limited to around 600k in auckland anyway, so this sort of house simple not on the cards).

AND: 70k dep, 630k mortgage! If using FHB grants and welcome home loan, income is tested and can not be more than 120k (I think?) combined? Which when run through banks 7% servicing test means you wont ever be able to relie on govt. help to get into a stand alone house in auckland.

Technically the argument is right but only insofar as the interest cost is low.

Bring in the capital commitment and it all falls apart.

It is far better to have a $400k mortgage at 6% than it is to have a $600k one at 4%.

The extra $200k still has to be found eventually and the future value of the house is indeterminate.

A small monkey is still less heavy than a large one.

"A small monkey is still less heavy than a large one."

Love this!

From an investment perspective, I'd much rather buy an undervalued asset with a high interest rate, than an overvalued asset with low interest rates. And I think a lot of the commentary around Auckland housing is far to short sighted.

When an asset is undervalued, generally speaking its price will increase. And when interest rates are high, they will generally reduce. Equally when an asset is overvalued (and you have to say housing in general is right now) generally they will correct, and when interest rates are low, the will rise (at some point in the future).

However where we find ourselves with Auckland is incredibly overpriced assets in a time of low interest rates. What will the future bring? Well we don't know for sure. But if history holds any truth, it is most likely that Auckland house prices will correct at some point and it is equally likely that interest rates will rise. For anyone entering the market recently and intending to hold onto your asset (ie not speculating), its most likely that you will loose capital at some point in the near future, have a very large amount of debt to service, and chances are that over the next 25-30 years you'll be paying a higher rate than you are at present. It makes no sense.

In my humble opinion, I'd say rent (for now....)

Yes, we landlords like people who rent. My experience of thirty years in the market in Auckland has been corrections have been minor and short lived. By the way the word is "lose' and not "loose" - this is a spelling mistake that must be stamped out before it becomes the accepted spelling.

Danger Will Robinson! Danger!!

Never fear, Smith is here!

It must be an older demographic in these parts as so many remember my childhood hero.

I'd rather invest I a well researched niche. Make good profit, find the next one before the first one tanks. They all tank eventually. And when everyone is doing it there will be no happy ending.

Wow, a lot of financial ingnoramuses commenting in this thread.

Rodney is absolutely correct that interest rates have a massive effect on house prices, as it's the interest rates that have a non-linear affect on the budget that a buyer has, meaning the marginal price setter has more ammunition to throw at a purchase.

Using a loan calculator, instead of the usual method of putting the Loan amount in to work out the monthly payments, we will make the monthly payments fixed at the maximum a buyer is willing/able to spend - let's say 50K for the purposes of this argument. The loan term is maximised at 30 years.

Then using a range of interest rates, you can fill in the missing variable which is the "budget" they can spend on a house.

Here are the results (rounded to nearest '000):

@8% interest rate - 568k

@7% - 626k

@6% - 694k

@5% - 776k

@4% - 872k

Note i have ignored the deposit, which is undeniably a factor, but the truth is banks are still doing high LVR lending, it's just being rationed. So the effect is particularly pronounced in the higher salary space, and/or those who can source higher deposits through family or second tier lenders.

So in a way, you're saying that low interest rates justifies greater ending more to citizens. I think it needs more thinking as to why interest rares are so low and more focus on why it is OK for people to take on greater amounts of debt when it seems that the future is becoming less reflective of the past.

In short it's easy to say that low interest rates are inflating a property bubble. The non-linear relation to interest rates just adds fuel to the fire.

Exactly, it's a cocktail. I don't discount immigration and land supply, but i think they are the icing on the cake rather than the cake itself.

The same weekly payment gives a higher capital budget as interest rates decrease. If interest rates got back to 6-7% in the next couple of years with no wage inflation, middle class Aucklanders simply won't be able to pay these colossal mortgages.

I think they will be able to pay - just not be able to buy food, clothing, and run a car. The original article is disingenuous, interest rates are everything.

The contagion of loss of confidence in central banks and governments is spreading as people realise that they have used all the tools in the arsenal and the economic situation is no better - only the helicopter is left.

If there is a correction it will be forced on the country - in some ways NZers are no better than the Greeks - who over borrowed and don't wish to take the pain. While only a percentage of home-owners have a mortgage - the rise or decline in house prices affects everybody. If the market collapses even those who owe no one will feel poorer and spend less - a loss of confidence.

For the most part I find this website nothing more than a fraud - people presenting opinion as fact with no evidence ( in the medical world it's called "evidence based medicine" - otherwise why don't you just use a ouija board).

Joke time - ask 12 economists for an opinion - get 13 opinions.

This site isn't a confidence scam. Just go and buy another house to build your confidence.

I never said a confidence scam - I said a fraud - there is a difference. And why would I want to buy property - it is not an investment - it's a gamble - which comes with costs......

Hugely one-sided article which seems to ignore the wildly-inflated-total-investment $ aspect, conveniently.

If one considers the matter from the ground up:

- Land prices at north of 30-40% of total house plus plot value are historically way out of whack

- if land prices are wrong, so is everything on top (a favourite saying of the absent Hugh P)

- building costs are controlled by a cosy duopoly

- building costs are inflated by increasingly crazy Elfin Safety imposts: fencing ($5-15K), scaff ($10-20K), meetings to plan the day's hazard mitigations (direct loss of tradie time at $100/hr oncosted) - $10K here, $10K there, pretty soon it adds up to real money...

- building is a 'cottage' industry - only 5 housebuilders do > 100 units/year, so inherently low efficiency

- Gawd-awful performance (variable quality, interminable time, unpredictable cost) from consenting authorities

- common taters may care to add their favourite cost component peeves downthread

then the real issue becomes - sure the interest rate is low but just how much is that Principal inflated by all the ticket-clippers?

Spot on Waymad, and as 'Dictator' also noted above, low interest rates just add fuel to the fire. If we didn't have to pay so much for our firewood to begin with, then interest rates don't matter.

Interest rates are low in Texas as well, yet house price to income mediums are not much above 3x.

Main difference between us and them is that their less restrictive zoning rules allows the supply and demand curves to almost lie on top of each other. This means that speculation for capital gains (without adding value to the property) is almost impossible, hence very little speculation. Rental owners are in it for the yield which as a % of value is higher than in NZ.

Rodney's analysis is always good, but only as a justification of the status quote. There is no universal law that says we have to have housing this expensive. It's a choice.

Having to because of vested interests is another story.

While you guys bicker I have just put an offer on another of my antique villas but this time in Wellington. Fixing my interest for 4 to 5 years. Hopefully any corrections and or interest rate rises will be washed out with inflation. But please continue to bicker as I need to sign my P&A and don't need you to bid.

I think you are doing the right thing keywest. Wellington is an interesting city and scored in the top ten of that 'most livable cities' list recently, a little behind the 'super city' of Auckland. I think prices will go up.

Was not successful, Wellington on a run at the moment...

Damn, that is bad news, it seems you always have to pay what seems like too much. I have bought houses and have been absolutely distraught with buyer's remorse while I wait for settlement day. Turns out a few years later that it was my best buy ever.

Prices are silly enough now with record low interest rates. How will people afford their 25 year mortgages when interest rates return to something more normal around 8%?

That is easy, we'll never see a 6% OCR that 8% retail implies ever again. In fact I doubt 4% OCR, not unless the RB goes kamikaze for 6 months and destroys our economy.

k

How

Why is it if the market has gone down 8.2%, property is still selling 20% or more over CV?

Fishingwell ,you need to work on your mathematics and stop drinking as much given your propensity to post

Well that's a fact and you don't like to hear it.

Why is it if the market has gone down 8.2%, property is still selling 20% or more over CV? - fishingwell

That's a very good question. There are a lot of kooky commenters on this site who, no matter what facts and figures you present or what you see with your own eyes by actually attending auctions and trolling through TradeMe and walking the streets and studying reports or what rational arguments you raise will still latch on to one tiny bit of negative news like it's going to save their life or something. I don't understand it, it is truly weird.

Fishingwell ,you need to work on your mathematics - cowpat

Cowpat is right about working on your mathematics though. Here is what I found from the Harcourts Auckland auction sales list for last week. It is not all the houses as some I could not find the CV for. I also excluded the two plaster houses as they are not typical. 39 Houses in the Auckland region excluding the rural properties.

Total sale price was 42,875,000 and total CV was 30,868,000 giving us an average of 38.89% over CV. Yes folks that is almost 40% over CV!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.