Much that has been written about the behaviour of Auckland house prices since the property tax and LVR changes last year is nonsense.

Auckland house prices were reported to have fallen significantly in the few months after the policy changes and most recently Auckland prices are reported to have surged, fuelling calls for more policy interventions.

Changes in the composition of sales between higher-priced and lower-priced properties will be the main driver of the recent behaviour of reported Auckland house prices rather than changes in actual prices. Attributing the changes in the reported Auckland median house price to the policy changes makes as much sense as commentary on the random weaving of a drunk driver.

I leave commenting on the random tumbles and spikes in reported median dwelling prices as if they have any meaning to the journos and bank economists.

In our quarterly Auckland housing reports and our housing reports in general I focus on the factors that will drive actual prices.

This starts by quantifying the balance between demand and supply in the market, while I also highlight when changes in the reported median house prices reflect random variation rather than changes in actual prices.

This Raving looks at the demand-supply balances in the Auckland and rest of the NZ housing markets. It provides some insights into what these mean for near-term house price prospects and provides some other insights (e.g. why Wellington probably has some of the best house price prospects in the country).

Random variation explains much of the recent behaviour of reported Auckland prices

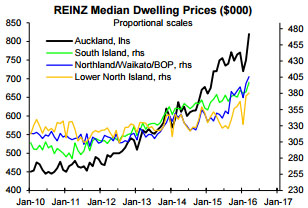

Based on the median dwelling price reported by REINZ, Auckland existing dwelling prices fell 7% between September 2015 and January 2015 (i.e. after the October introduction of the property tax changes aimed at especially foreign investors and property traders and the November increase in deposit requirements for Auckland investors). It is superficially understandable that the fall in the reported median dwelling price has been widely attributed to the policy changes.

Based on the median dwelling price reported by REINZ, Auckland existing dwelling prices fell 7% between September 2015 and January 2015 (i.e. after the October introduction of the property tax changes aimed at especially foreign investors and property traders and the November increase in deposit requirements for Auckland investors). It is superficially understandable that the fall in the reported median dwelling price has been widely attributed to the policy changes.

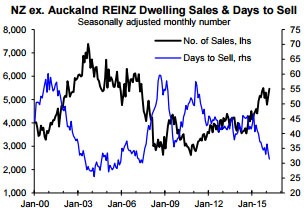

However, it only requires a quick look at the past behaviour of the reported Auckland median price to realise that the fall between September and January is no different to past temporary tumbles that have been followed by spikes (see the black line in the top chart). Spikes and tumbles in the reported Auckland median dwelling price reflect normal behaviour and will be the result of changes in the composition of sales between higher-priced and lower-priced properties. REINZ and real estate agents are well aware of this behaviour, as should be journos and the bank economists, but too often the latter two groups comment on random variation in reported median prices as if it reflects changes in actual prices.

However, it only requires a quick look at the past behaviour of the reported Auckland median price to realise that the fall between September and January is no different to past temporary tumbles that have been followed by spikes (see the black line in the top chart). Spikes and tumbles in the reported Auckland median dwelling price reflect normal behaviour and will be the result of changes in the composition of sales between higher-priced and lower-priced properties. REINZ and real estate agents are well aware of this behaviour, as should be journos and the bank economists, but too often the latter two groups comment on random variation in reported median prices as if it reflects changes in actual prices.

By chance the reported median dwelling prices for all four areas reported in the top chart fell after the policy changes and have rebounded in the last two months. But it just as much nonsense to suggest actual prices in Auckland fell 7% between September and January and rebounded 14% between January and March as it is to say that actual prices in the lower North Island fell 10% between December and January just to rebound 15% between January and March as reported by REINZ (gold line, top chart). REINZ accurately reports the median or mid prices each month, but it can't control how many higher-priced versus lower-priced properties sell each month. However, the journos and bank economists could stop commenting on this random variation as if it is the real thing.

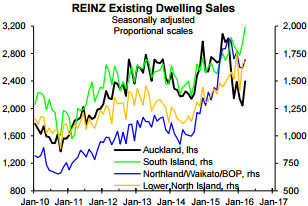

The numbers of dwelling sales reported by REINZ also exhibit significant random variation from month-to-month as can be seen in the chart above. Most notable recently has been the spikes and tumbles in the number of sales in the lower North Island that will reflect random variation (gold line, chart above), as most likely will also the fall and rebound in the number of sales since September 2015 for the South Island (green line, chart above).

The 17% increase in the seasonally adjusted number of Auckland sales between February and March may seem impressive but when viewed on the context of the past spikes and tumbles in Auckland monthly sales it may reflect no more than random variation (black line, chart above). Most importantly, the number of sales in Auckland has been bouncing around over the last several months after falling sharply following the policy changes, with sales in March still 21% below the September level.

In my assessment the behaviour of the number of sales more accurately reflects the impact of the tax and LVR changes for Auckland and the impact of the tax changes for the upper North Island (i.e. Northland, Waikato and Bay of Plenty) where investors were particularly active prior to the October 2015 property tax changes (i.e. the requirement for buyers and sellers to supply bank account and IRD numbers and the introduction of the two year "blight light" capital gains tax rule aimed at tax-dodging property traders). While there are reasons to expect sales to improve in Auckland and the upper North Island over the next several months as outlined in the respective regional reports and the Housing Prospects reports, for now the policy changes are still having a significant negative impact on demand in these two areas.

The demand-supply balances and some related issues and thoughts

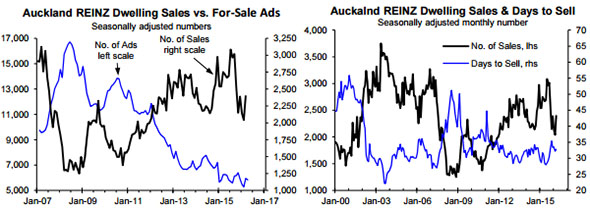

The only sound basis for assessing the prospect for house prices in Auckland or elsewhere is first quantifying the demand-supply balance and then undertaking quality analysis of the factors that will drive demand and supply in the future (i.e. the sort of analysis contained in our Auckland and other housing reports). With high-price-paying foreign buyers largely deserting Auckland auctions after the October tax changes it is likely actual prices fell in pockets of the Auckland market, but even after the large fall in Auckland dwelling sales late last year the Auckland demand-supply balance remained strong enough to justify upside in prices, albeit at a significantly slower rate (two charts below).

The left chart compares the number of dwelling sales reported by REINZ for Auckland (seasonally adjusted), which largely reflects demand, with the number of dwelling for-sale ads on www.realestate.co.nz for Auckland (seasonally adjusted), which measures supply. When the number of sales is above the number of for-sale ads the demand-supply balance is supportive of near-term upside in Auckland house prices in general, with a strong link between prices in different parts of the super-city, and the larger the positive gap the more prices in general will increase. Based on this measure of the demand-supply balance the Auckland market has gone from an extremely strong demand-supply balance to a balance that is still supportive of house prices increasing at somewhat above a 10% annual rate in the near-term.

The right chart above provides a second means of assessing the demand-supply balance in the Auckland market. It compares the number of sales with the median number of days dwellings are taking to sell via real estate agents. When the number of sales is above the number of days to sell the demand-supply balance is supportive of Auckland prices in general increasing, with the larger the gap the more the near term upside for house prices.

Based on this chart the demand-supply balance deteriorated significantly following the property tax and LVR changes, but remains strong enough to warrant moderate upside in prices (e.g. prices increasing at around a 5% annual rate in the near-term). Based on the state of the demand-supply balance in the Auckland existing housing market it should be no surprise that house prices in general are still increasing albeit at a significantly slower rate than prior to the policy changes. There is not a basis for believing prices in general surged 14% between January and March while in parts of Auckland there was a basis for believing prices will have fallen somewhat as a result of foreigners deserting auctions although there was not a case for generalised downside in Auckland house prices given the state of the demand-supply balance.

Based on this chart the demand-supply balance deteriorated significantly following the property tax and LVR changes, but remains strong enough to warrant moderate upside in prices (e.g. prices increasing at around a 5% annual rate in the near-term). Based on the state of the demand-supply balance in the Auckland existing housing market it should be no surprise that house prices in general are still increasing albeit at a significantly slower rate than prior to the policy changes. There is not a basis for believing prices in general surged 14% between January and March while in parts of Auckland there was a basis for believing prices will have fallen somewhat as a result of foreigners deserting auctions although there was not a case for generalised downside in Auckland house prices given the state of the demand-supply balance.

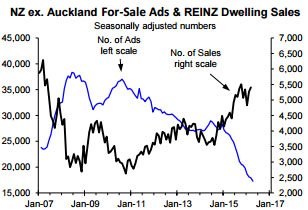

In the rest of the country on average the demand/supply balance is very strong whether I assess it by comparing the number of sales relative to the number of for-sale ads (adjacent chart) or by comparing the number of sales versus the number of days to sell (left chart below). Wellington is currently one of the most interesting parts of the country based on an improving demand-supply balance, prices being cheap on a relative historical basis and the prospect that stronger economic growth than predicted by Treasury and the economic forecasters more generally is a positive for the local housing market because it will bring forward when the government goes from purse tightening to increasing spending, including especially in Wellington (this issue and more are covered in the Wellington reports).

In the rest of the country on average the demand/supply balance is very strong whether I assess it by comparing the number of sales relative to the number of for-sale ads (adjacent chart) or by comparing the number of sales versus the number of days to sell (left chart below). Wellington is currently one of the most interesting parts of the country based on an improving demand-supply balance, prices being cheap on a relative historical basis and the prospect that stronger economic growth than predicted by Treasury and the economic forecasters more generally is a positive for the local housing market because it will bring forward when the government goes from purse tightening to increasing spending, including especially in Wellington (this issue and more are covered in the Wellington reports).

The Auckland and other regional housing reports cover the national and local factors that will drive house prices beyond the near-term outlooks implied by the current demand-supply balances (e.g. interest rates, population growth and relative housing affordability). The reports include quite a bit of analysis of residential building and section market prospects that will in time be quite important to existing house prices in especially Auckland because of the role the Housing Accord and the 154 Special Housing Areas approved as a result of the Accord will have. An important theme in Auckland is the focus of immigration policy on work visas and the dominance Auckland has in new economy (i.e. technology-related) job creation - the two together mean Auckland will continue to attract a disproportionate share of immigrants including Kiwis returning from OE.

Outside of Auckland important themes are the roles cheaper housing relative to Auckland is playing in boosting housing demand (see here) and the housing booms fuelling the local economies and job creation. The focus of this last year was most on the upper North Island but it should spread further afield this year including to especially Wellington. Fuelling the local economies will help reinforce the housing booms for a period as will greater buying by investors searching for better value and greater prospects for capital gains than offered by the Auckland market. Stronger housing market and employment growth will help fuel stronger consumer spending growth than the Reserve Bank and bank economists are predicting, which will help fuel the GST tax take, while the stronger employment growth will help fuel the GST tax take (see this link that reports the government's accounts improving more than predicted by Treasury). The Wellington housing market will be a beneficiary of this.

A national theme that has relevance to all regions is the misguided game being played by Governor Wheeler, which has significant parallels with what Governor Bollard did last decade (i.e. misguided OCR cuts in 2003 that were followed by 13 OCR hikes between 2004 and 2008 and a major housing downturn). For many regional housing markets this game and what happens to external migration will have more bearing on house price and residential building prospects than will developments in the local economies that aren't related to either interest rates or external migration. External migration measures the numbers of immigrants including Kiwis returning from OE less the numbers of local residents heading overseas on a permanent or long-term basis. Most parts of the country experience stronger and weaker population growth as a result of cycles in external migration at around the same time and by similar magnitudes.

A key strength of our regional housing reports is that they incorporate analysis of the national and local drivers in assessing prospects for house sales, house prices and residential building. Only by doing this is it possible to provide useful insights. Investors and firms operating in regional housing markets will be flying partly blind and at risk of experiencing unexpected and at times unwelcome developments if they don't have access to the analysis contained in our sharply-priced regional reports.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

12 Comments

Danger Danger Dr Smith. An informed article scares us interest.co common tators. Avoid it. You will have more fun just making facts up.

I don't think that the article should be described as "informed", but it is "data based" following a model based on supply / demand. Also, Rodney doesn't clearly describe his predictive model (but maybe you have to buy the report to get that content).

However, that doesn't mean people should not be "scared." That is a natural response when you have a market that looks very much like it could be a bubble. I'm not sure how how Prospect Theory applies here, but I would suspect that any short term correction would not scare the horses as the theory that people are averse to selling at a loss.

Its is an informed article , and well written , what is of concern is that my home has doubled in rateable value in 3 years , and now Dickens reckons will go up another 5% this year (off a really high level.)

The compounded growth is just staggering , if it increases by 5% on the now doubled value , my real $ growth is around 10%................. and I just cant believe it. My unrealised "gain' would be $250,000

The growth in $ value is more than double what I could earn in a year by going to work every day

I wish it was still mortgaged , my return would be in multiples 100's of % points on my deposit amount .

Its now so far out-of-kilter that it must crash at some point

Don't go back and get that Mortgage Boatman. You are only going to make the same return in dollars. Of course your percentage would be bigger but what can you do with a better percentage - eat it.

This is an excellent analysis. Most academics, experts and statisticians are aware of the issues surrounding the REINZ monthly median. While it provides up-to-date information it bounces around due to the nature and amount of houses being sold. The statistical knowledge needed to understand its weaknesses is quite advanced hence the problems of reporting to the general public. This sounds elitist but popular journalism often struggles with complex issues.

That is why the stratified index exists

Well argued, but just more blah... , some will nod in agreement while others will scoff.

In an ideal situation "supply" would be where a new dwelling was built and offered to satisfy a "demand" from a new entrant to the market requiring a roof for their family.

In the Auckland context, while I am sure this is a portion of it, the bulk is made up of "Supply", where speculative sellers( including developers) are marketing their asset for maximum return, seeking to capture the capital gain accrued and "demand" is from those speculating that there is still gain to be had.

Any commentary on that is just so much speculation in and of itself.

Nobody "needs" to live, work or own property in Auckland but a great many "want" to.

That was interesting and I enjoyed it.

But it was also a really long way of saying just look at the stratified median index.

I see that data through a different lens. The entire Auckland market is now utterly dependent on foreign capital to prop up the nose bleed house prices. Even top 5% working professionals can’t afford the median Auckland price. I know because I am one. We got a tiny glimpse of what it would be like if the Chinese left the market late last year. The Chinese pull back was in part foreign (crackdown on capital flight by the CCP) and partly domestic (due to well-known IRD changes).

From March 2015 to March 2016 there must have been immense pressure on mainland Chinese to get their money out of China and bare in mind that was happening while the falling CNYNZD made it more favourable for the Chinese to buy NZ houses. Through that whole period you could still see zerohedge articles about the Chinese buying multimillion dollar shacks in Canada. We have never actually seen a Chinese pull back where they voluntarily remove capital from the NZ housing market.

NZ real-estate is now dominated less by domestic credit creation and more by capital flows. Capital flows from China are the most important, followed by capital flows from the wealthy baby boomers. In that context its easy to see why Auckland, Tauranga, Nelson are doing well. Wellington is harder to justify. Just my humble opinion anyway.

Here's the kicker .......... we still don't even know who has bought these properties because we don't keep proper records of where they are resident

aussie banks have cracked down on foreign borrowers

http://www.smh.com.au/business/banking-and-finance/commonwealth-bank-of…

Yep and when I sold a house in Auckland the other day the buyers name on the S&P agreement was completely European. Strange thing was that I was told by agent that the buyer was Chinese. The purchasers lawyer was manalaw.co.nz. No amount of Bayesian analysis is going to figure out who purchased my house.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.