By Bernard Hickey

The Reserve Bank is back in a familiar place: between a rock and another rock.

For a third time in three years the Reserve Bank faces conflicting objectives where achieving one could obstruct or destroy the other.

Our central bank is unusual in that it is responsible for both monetary policy, which means keeping inflation between 1-3%, and for financial stability, which means ensuring the banking system is stable. That is both a curse and a blessing. It worked brilliantly during the Global Financial Crisis, but now it's a pain in the proverbial.

The Reserve Bank is now in a sadly familiar situation.

It needs to cut the Official Cash Rate to stimulate the economy to get inflation back up into that target range, and more specifically, up around the 2% mid-point specified in Governor Graeme Wheeler's Policy Targets Agreement with Finance Minister Bill English. Inflation figures out this week showed annual Consumer Price Index inflation of 0.4% in the March quarter, which means it has been below the bottom end of the bank's target range for a year and a half and below the mid-point for four and a half years.

But at the same time the Reserve Bank has to keep the banking system stable and has been worried since at least 2013 that Auckland's over-valued housing market could fall sharply and stress our big four banks. It knows that ever-lower interest rates will encourage more borrowing to buy houses, potentially pumping more air into a bubble and adding to the stress in the event of a slump.

This conundrum drove the Reserve Bank to bring in two rounds of controls on mortgage lending. The first round in November 2013 introduced an 80% Loan to Value Ratio limit on all borrowers and the second round in November last year tightened that limit to 70% for rental property investors in Auckland.

Along with the Government's two year bright line test to tax the capital gains of speculators, the Reserve Bank's second round slowed the Auckland market for all of five months, and may actually have fired up the housing markets in the provinces. That's because the November 2015 changes included a loosening of the 2013 limits outside of Auckland and seems to have encouraged Auckland investors to gear up their Auckland equity gains with 80% loans to buy rental properties and sections in the likes of Tauranga, Hamilton, Wellington, Napier and Dunedin.

The Real Estate Institute's March figures released last week removed any lingering hopes that last year's measures would take some of the steam out of the market for longer than a few months. Auckland is off to the races again and the provinces are galloping along in its wake.

The Reserve Bank now faces an ugly combination of double digit house price inflation nationally, falling mortgage rates and a rising currency. It has already forecast one more Official Cash Rate cut, possibly as early as this coming Thursday, and most economists think it will have to cut for a third time this year to 1.75%. That will push fixed mortgage rates substantially below 4%.

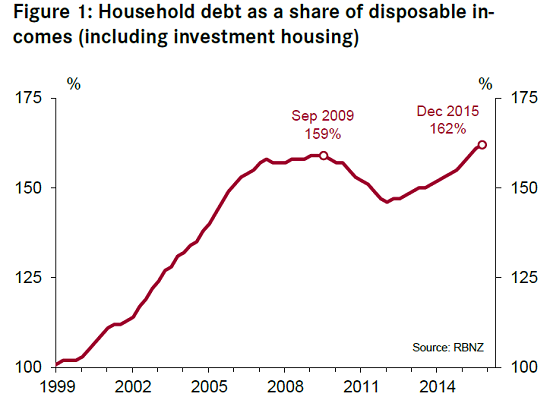

Until now, the Reserve Bank has been in reactive mode and has been a reluctant restrictor of lending. It had hoped that once or twice would be enough. As recently as March 10 Governor Wheeler said he was not considering a third round of lending limits, but that was before the latest housing market surge and the currency's rise this week to 10 month highs over 70 US cents. It was also before fresh figures showing New Zealand household debt has hit a record high relative to incomes and the amount of borrowing is now growing just as fast in nominal terms as it was during the 2002 to 2007 boom.

Economists are now predicting a new round of limits that could include reducing the Auckland LVR threshold for investors from 70% to 60% and/or extending the LVR limits for investors beyond Auckland to the rest of the country. Other options include increasing the amount of capital banks have to hold against mortgage lending, or lending generally, and banning the use of interest-only loans to landlords.

It's time for the Reserve Bank to get ahead of the curve and take a more strategic approach. It should make clear to banks and borrowers alike that it will have to progressively tighten lending in line with further cuts in interest rates, particularly while house price inflation is rising at double digit rates.

Our Reserve Bank is rare in the world of central banks that it has yet to cut interest rates to 0% or lower, and it has yet to start other unconventional measures such as buying Government bonds to lower long term interest rates. Given the persistently lower than expected global inflation, the persistently stronger than expected New Zealand dollar and the ongoing failure of Auckland housing supply to meet demand, the bank should signal that progression of tightenings to reset expectations just in case.

At the moment, New Zealand's landlords see a one-way bet. They see central and local Governments failing to allow enough new house building to meet supply. They see interest rates falling despite years of warnings from officials about the risks of rising interest rates and they see little political appetite to tax either capital gains or land. The only thing standing between landlords and yet more easy money is the ability to leverage up their ample stocks of equity.

It's time the Reserve Bank took on that responsibility, if only to give itself some breathing space between those two rocks of very low CPI inflation and very high house price inflation.

A version of this article was also published in the Herald on Sunday. It is here with permission.

203 Comments

Our central bank is unusual in that it is responsible for both monetary policy, which means keeping inflation between 1-3%, and for financial stability, which means ensuring the banking system is stable. That is both a curse and a blessing. It worked brilliantly during the Global Financial Crisis, but now it's a pain in the proverbial.

Are you sure, you are not commiting an act of revising history?

CPI rose from around 1% in 1999 to 5% at the crescendo of the GFC storm. View graph

Over the same time frame a residential property my family purchased rose in price by 87%, according to QV. I believe a sale in 2007 would have netted 100% - a mere doubling in value.

BH , why do you amongst others show a RBNZ chart of national household debt against income . Its the unequal regional spread of household debt that is the problem. Aucklands household debt has risen sharply from 2009 yet the graph appears to show all is well in fairytale land . Again commentators like yourself are unwilling to look at the data in a rational way.To suggest all things being equal, the chart shows Aucklands debt/income is around 162%is pure folly.

The devil is in the detail.... It would be interesting to see the breakdown by region.

By lender more like it.

They are the tier one enablers.

Both

Does anyone really believe that an OCR of either 1% or 3% would have any real effect on the Auckland housing market?

Other factors are having a far larger effect.

The Reserve Bank now faces an ugly combination of double digit house price inflation nationally, falling mortgage rates and a rising currency. It has already forecast one more Official Cash Rate cut, possibly as early as this coming Thursday, and most economists think it will have to cut for a third time this year to 1.75%.

Isn't insanity: doing the same thing over and over again and expecting different results?

Maybe a revision of which CPI components are more desirable than others to achieve the stipulated PTA outcome is called for? Read more

The dubious efficacy of the Japanese experiment surely warrants further investigation before New Zealand arrives at this shambolic nonsense:

The rumors today were that the Japanese central bank may offer funding subsidy to banks that are now being penalized by NIRP. The Stimulating Bank Lending Facility, ironically named, currently offers Japanese banks collateral funding at 0.0%. If the whispers are true, BoJ policymakers are considering dropping that rate also negative especially if the other whispers about deeper NIRP all prove founded. These people just will not stop. Read more

Maybe a revision of which CPI components are more desirable than others to achieve the stipulated PTA outcome is called for?

Yes, indeed - particularly given education costs are skyrocketing;

Consumer Price Index (CPI) figures released this week show the cost of tertiary and other post-secondary education rose 2.9 per cent in the first quarter of this year. Inflation over the same period was 0.4 per cent.

Primary and secondary education rose by 3.7 per cent, the same data shows.

It's got to be a very narrow-minded government who chooses to sweep this sort of thing under the carpet. Point is, they have no intention of meeting the cost of inflation in this sector .. so it makes sense for them to emphasize just how low their definition of CPI is ... after all the health/well-being of future generations matters zilch to them.

I'm curious that Christchurch (for the most part) has been bypassed by this recent bout of "irrational exuberance" . House prices while increasing, but at a modest rate ( and depending on which set of statistics are used) . There is a supply of new subdivisions that are potentially coming on-line in the next few years which is most likely moderating any dramatic surge in house prices. The rebuild has supposedly peaked , more building related company's are getting into trouble, unemployment is rising and lets not forget the agricultural sector. Is this what could happen to the rest of the country. As the economic tide turns - as was famously said "when the tide goes out , you get to see who's swimming naked" . The process has only just begun in Christchurch - it will be interesting to see what happens in the future.

Regarding Wheeler and his options - I favour the saying "Speak softly and carry a big stick; you will go far". Introduce more restrictions - doesn't really matter what - any policy implemented is going to have positive and negative effects, and doing nothing is not an option.

the problem is we have two economys in NZ. Auckland fueled by high immigration and selling house and the rest of NZ.

we also have Auckland now spilling out to Hamilton and tauranga

But that is the issue - it is spreading. Don't set rules for one area and not another - people just game the system. One set of rules that cover all of New Zealand.

and Wellington...

"Doing nothing" has defined National for the last 6 years.

Yes I know - they've had it good but now things are changing.... Will be interesting to see what happens if things get really bad - i.e. a recession. I think Key is a fair weather leader.

Nothing is changing in the short term i.e next 1 to2 years . More money being printed, more illegal Chinese money, National polling at 50%. Everything is hunky dory for those who own property. For those who don't....

I'm not sure it is for those who own property - there is a real risk out there of a collapse in the property market.

Not in the short to medium term. And people who own nothing, like myself, have no chance, we have been left behind.

Invest for the long term, and not in property. Also invest on a regular basis even something as simple as reasonable dividend stocks will consistently perform. There's ups and downs but over the long term you will do well. I've assumed you aren't close to retirement. Note you could just invest in index funds as another option to get a mix of capital gains and income from dividends.

I only bought a house two years ago and purchasing prices have risen at an unreasonable exponential rate. If you can't raise a deposit at a rate faster than house prices are going up then don't bother. Just invest and get compounding gains.

It's not that simple. It makes me just want to quit working. No point working if the only thing I want is out of reach.

The other way around. By investing and getting compounding growth you can eventually get a deposit together. You can also wait until the housing market goes flat or if there's a crash property will be cheaper.

There's nothing wrong with renting, most house are a giant money pit anyway.

If you truly want a house first homes can still be purchased with a 10% deposit, or 5% if you have someone cosign the loan. Although the interest rates are pretty harsh the lower the deposit. Also being in kiwisaver for 5 years will put $10k towards the mortgage itself as well as being able to use a chunk of kiwisaver funds for the deposit.

I thought that saving more was prudent. It wasn't. You cannot save faster than people will borrow.

Given that house prices are going up in an exponential manner you have to ask yourself would I be buying at close to the top of the market? I don't recommend buying a house right now as it's expensive and risky. Even trying to get building work done costs twice as much as a few years ago. The construction industry is running hot with all the money that's about.

Save, invest and wait until the right time to buy. Alternatively do what I did and go around putting in low offers. You don't need to rush in to pay too much for a house.

Hi dictator! Ok so I disappeared for the weekend for a 3 day yoga retreat to get away from the mess in Auckland and the mess in my head. I randomly brought a book by Jame Altucher, I knew nothing about him but after reading a few chapters I realized I had read some of his stuff before. You could say it was a weird twist of fate but his book I'm reading is talking about thinking outside the box. I'm outside of the box right now (in the wilderness I've found two bars of Internet to type this) and I read you comments above. I'm interested (and always have been) to know more about what you have said above about shares etc but, I've never once pretended on here to be all that smart. Anyway in the spirit of ZS (who also has given me lots to think about despite the heated debates) has inspired me to ask more and use the Internet to my advantage. I wonder if there's a way I could ask you more out in the 'real world' about some alternatives? Gotta go as my signal here is weak. But when I'm back I'll be back on here. I'm really trying, really trying to make sure I don't get swallowed up and spit out by all this.

Stay focused on your yoga and get the best out of the environment you are in.

The main book I recommend is The Four Pillars of Investing.

http://www.amazon.com/Four-Pillars-Investing-Building-Portfolio-ebook/d…

The reason I recommend this is it's very accessible (unlike his highly technical attempt at this). Once you've read the book you understand modern portfolio theory. It teaches you to be diversified, how to rebalance your portfolio, etc. He does focus on index fund performance.

Overall you will tend to do well with reasonable performance, following the approach won't make you super rich but you'll have reasonable gains. The book also has a lot of past history and ties into statistics, the historical parts stop it from being too dry. It is a book that will change your perspective.

e: If you already have a handle on this then ask some specific questions.

Shocks and scares - Mugs game. What do I do for a job? Work for an investment bank. If you arent a professional, doing it for a living - you're dumb money. Buy property in major cities in areas with little or no social housing and wait.

Being dumb is putting all your eggs in one basket.

At least Ive got a basket.

The answer is that nobody knows where the top of the market is. I would wager that it's some time away, probably not until Yuan Key is replaced. What you say is just as true as it was one year ago and two years ago. But here we are with another 250k and two years down the drain since then.

Being a saver is pointless and futile. Your future debt burden is just growing at 10k / month. When you have spent years and years saving, delaying having kids, working overseas, it takes a toll on your mental health.

It does sound like you need to question your approach and change direction. If it's taking that much of a toll maybe save a bit less, and maybe look at buying elsewhere. If you are chasing property prices in Auckland and it's doing this to you look farther afield.

My common sense is the issue to overcome.

SpaceX....things go in cycles. Keep yourself prepared for when the next one commences. The boomers are all ageing...their rentals are all deteriorating, few have budged for depreciation let alone cap upgrades. As the economy tightens cash flow will be king. They may well all need to offload within the same timeframes. Just be ready.

Why do we run a country which screws people who just want to save a deposit, get a mortgage, buy a house and live happily. They are the guts of this nation.

It matters not what Wheeler does because Key and English have much bigger sticks available to them and which they refuse to use lest it castrates their political ambitions.

In many eyes they are already political eunuchs anyway.

The illusion of control

Tony A just released his report and it says one thing. China is going to do more stimulus, that money will end up here and capital outflow restrictions will be eased.

What makes you think it will end up here ?

The fact that it has in the past? And Tony A just confirmed that Chinese capital outflow restrictions are going to be relaxed

@ BadRobot; Oh I think it will endup here if Mr Key has anything to do with it: http://www.nzherald.co.nz/residential-property/news/article.cfm?c_id=76…

One man wants to buy one house......

If it's on the internet it must be true.

I thought the Chinese spent all their money sponsoring the tea-towel flag. This website sure isn't in a hurry to remove it.

This website is an extension of the National party.

And Tony A is the chief economist of the BNZ. I think that adds some credibility.

Certainly the editorial stature of DC is emasculated by his National bias no matter how much he may protest.

Joke time - assemble twelve economists and get thirteen opinions. Sorry the track record of economists is poor at best and fraudulent and worst. While some of the money may end up in New Zealand , it is no guarantee.

That's a silly joke

There are economists and economists, specialising in different fields

Just as there a Doctors who are Dentists and Veterinarians and PhD's

If you had gangrene of the big toe and consulted Dr Nick Smith, minister for housing, PhD in landslides, what sort of diagnosis would you expect?

Nick Smith. That's something to bring up next time somebody claims National is better than any of the alternatives.

It makes one ashamed to recognise that another engineer (by degree) could obtain a PhD and then end up as a politician able to make himself look a complete dork in just about everything he does.

He doesn't seem to know how to do anything. He can't answer anything himself so he deflects questions. He's doing as bad a job as the previous minister who ran MBIE into trouble (well he didn't do anything when he really needed to).

Tony Alexander's Weekly brief - pretty accurate observations

More Chinese buying likely as the Beijing leaders opt to stimulate growth through looser credit conditions.

improved growth increases the chances restrictions on capital outflows will be eased later this year.

Foreign buyers getting to grips with the IRD number requirements,

Banks across the Tasman are cutting lending to offshore buyers, and

Australian rules affecting foreign buyers of residential property being tightened and applied

Australian moves will channel Foreign money toward Auckland

Was Tony A one of the economists who predicted that the foreign buyers would return - could be seen as a little self serving. The moves in Australia may make foreign buyers more reluctant to buy there - but it does not necessarily follow that they will buy in Auckland.

Without reproducing his entire article - should have included this

means we are likely to see SOME previously Aussie-bound buyers shift our way instead as we become one of the few residential markets left around the world completely open to foreign buyers.

and (in my words)

The last commonwealth country with no Stamp duties or Capital Gains Taxes

The TPPA or China Trade agreement legally prevents the introduction of Stamp Duty in NZ.

We are losing our ability to govern our own country.

As admitted by the PM this morning

Nothing really in context of todays topic, I apologize, but I think this documentary is worthwhile viewing:

The Wall Street Code (VPRO Backlight)

A thriller about a genius algorithm builder who dared to stand up against Wall Street, Haim Bodek, aka The Algo Arms Dealer, from the makers of the much praised Quants: The Alchemists of Wall Street and Money & Speed: Inside The Black Box

Define short to medium term - New Zealanders don't think in these terms - they have no idea what they mean. If they did they would be taking a more strategic approach instead of waiting for next months real estate figures in the hope (and I use that word purposefully) that the "value" of their real estate portfolio has gone up. Investing is a long term objective - ten to fifteen years or longer and across a diversified portfolio of assets.

It's called "Hopium"

I like that word

Most NZers see Lotto as an investment. Most aren't interested in reading a book on investing and understanding what they are doing. The only thing that's long term for most is kiwisaver or buying a house. Too many people are locked into their thinking and are unable to adapt.

Diversity, portfolio and investing aren't concepts in pop culture. I talked to one of my brother in laws over Christmas and I told him he should think about investing. To him investing was putting money in the savings account.

Gambling - a tax on stupidity ( actually that could be the Auckland property market). Agree about investing - I'm not sure its about picking the "right" stocks but more about the long term.

Statistically you can't pick stocks anyway. Low effort, little thinking required approach to stocks is invest in the index. There's nothing to pick except the market itself.

People just apply irrational fears and trying a get rich quick scheme.

Yes I believe a monkey can do better. than most investment advisers. Fear and greed.

:-I

'Agree about investing - I'm not sure its about picking the "right" stocks but more about the long term'.

Well, if you imply that long term most stock pics should do ok then Real Estate definitely will too. Real Estate IS one of the safest and best performing investments of all time, historically. Because if you buy it for the long term it will perform well, even if it crashes in the short term. Real estate allows the use of leverage and returns a "dividend" in the form of rent while allowing for tax benefits. Unlike stocks, even if house prices crash then you still have your asset- the house (Which will recover eventually).

Notice on Q&A this morning there was no panel to critique JKs China / property interview?

His PR minders would not allow any critique or discussion on air of his dismissal of foreign property investment.

RB: let's assume an OCR OF 1.5%. What would change? Floating rates to 4.8? Hardly much kf a loosening of monetary policy.

I read an article relating to Vancouver. Reasons why the RBNZ is looking in the wrong cupboards re Auckland. 1, Foreign buyers, particularly Chinese are pushing prices higher irrespective of the price band they purchase within. Investors both offshore and onshore are driving the market. 2, ineffective regulation , unscrupulous people , particularly real estate agents, again Barfoot and Thompson caught out, how many do not get caught. Fines for the behaviour pail in comparison to the commissions, almost a pat on the back from those that run these agencies.. 3, Technology , over the last decade has simplfied the ease in purchasing a home . 4, Money laundering , fraud , tax evasion and hiding funds, again real estate companies and banks allow this behaviour, government turns a blind eye.5, The bar to entering the real estate industry is too low, after a few weeks study, over 10000 agents fighting one another for a listing to obtain income way exceeding the work 6,Lack of unbiased information , no one wants to kill the cash cow. 7, Apparently Auckland wants to grow

Yo, you millennials need to check out this article:

http://www.nzherald.co.nz/residential-property/news/article.cfm?c_id=76…

Interested in your thoughts..

@ Zachary; Have you seen the crime stats for Otara and Wiri? I think it will take many years of gentrification to bring those area up. I had a friend who lived fairly close to Otara and his car and house was broken in to around every three weeks or so. He gave up in the end and moved to the West Cost of Auckland which is much safer and property prices were still affordable.

Surely the break ins would be compensated by free heating from the burning police cars.

The article is a bit self-righteous as I note the author has not snapped up that bargain.

My house is in a street with a fair number of former state houses, land was subdivided and my house was built new. There's quite a mixture of people not so well off, some pensioners and a number of house owners. Not the same crime rate as Otara but where I bought I couldn't imagine a snobby entitled baby boomer buying the same house that I did.

There is a reason it is that cheap.

But if you don't value sleep, anything you own which isn't tied down, or the quality of friends your children will have, it's all good, go for it.

@ Cowpat: Yes I agree, we all know that making any further restrictions on tightening up lending for Kiwi Investors will have very little to NO impact on Auckland house prices! They'll just continue to head up as there's in nothing to prevent Non-Resident Property Investors to continue to plunder our property markets and lets face it, we all know that's where the real money clean or otherwise, is pouring in from Asia.

It's just so ridiculous and we'll be reading another article in a few months time saying that the Reserve Bank still isn't able to figure out why Auckland's house prices are not slowing down!!!

Almost laughable but unfortunately that joke is on us, for not restricting Non-Resident Property Investors who continue to massively inflate our property market and price Kiwi families out of their homes.

Long live Central Planning. Ah, the joy of it; lots of bright, earnest fellows running around in circles trying to do the impossible; in this case get prices to rise (those in cpi) without getting prices to rise (in housing). Hilarious.

If the RBNZ feels obligated to reduce the OCR again they should do something immediately to limit investors from further leveraging their property investments and fueling the housing market. The Australian parent banks have no difficulty in Australia in requiring investors to pay a higher rate than owner occupiers. This is beneficial to first home buyers as well as owners of a home they occupy. This also improves the prospects for banking stability should things deteriorate.

And perhaps the depositors of banks woud not need to be the ones immediately get interest rate cuts to fund the lower mortgage rates that the RBNZ and most all politicians feel so important. (Not to mention the wide range of those who constantly comment so passionately here on self-interest.co.nz for lower mortgage rates when they are already the lowest in NZ history.)

The RBNZ has been light handed and lax and ineffective in slowing down investment in housing - which seems to be the main NZ industry at the moment.

Are the RBs restrictive measures against NZ house buyers and borrowers (LVR etc) actually designed to help foreign or foreign-linked buyers. It does have senior staff with strong Internationalisation/Globalism backgrounds. The Governor from the World Bank.

Perhaps, like the current Govt, there is no longer any loyalty to our nation state or sovereignty from our Govt depts or RB.

No, never put down to planning what dogma and stupidity can achieve IMHO. This applies to the RB and successive govns.

a) I think for 10 if not 20 years they made a serious long term policy cock up, ie biasing investing into property as its 'safe" and not businesses making a good.

b) Opening up our markets to foreign investment has ended up as dis-advantaging our NZ owned businesses from what I can see, ie NZ companies get hobbled with taxes that foreign capital can avoid.

The question no-one seems to be asking is what proportion of foreign buyers even use mortgage funds? It could be that many of these are cash buyers so the whole loan restriction argument will only make it easier for them to buy more property as their domestic competition will have been reduced by the restrictions. Yuan Key's need to act is long overdue, as too many Kiwis are losing the ability to live as they should be able to, in owned homes. I can't imagine Helen Clark as PM would have stood around in denial doing nothing on this subject as long as Key has. It's a poor show really.

Helen Clark and her cohorts were just as responsible for the last housing boom given they also opened the immigration floodgates.

How much money went into housing to offset the higher tax rates that Labour introduced? How much of WFF went into housing?

The immigration standard has as far as I am aware not been changed much in 20 years, ie you need 28points. Ergo I fail to believe that HC opened any flood gates.

WFF actually stopped the growing inequality in NZ. If you actually look at the boost in housing its in the "well to do areas" the JK tax cuts are therefore far more likely to have had the biggest measureable effect.

Yes, I think HC et al are just as responsible as National ie they should have acted to quieten the housing market and failed to do so in order to buy votes, certainly the growing accommodation supplement went straight into Landlords pockets from what I can see.

Actually the Q on foreigners taking out foreign mortgages (I assume you mean) has been asked quite a bit, we dont know, I odnt think they are taking much NZ ones out? cant see why considering our rates are higher plus I think its all cash stashing.. If you read posts around the world on what is happening there in housing, say Vancouver and London there seems to be a very similar pattern of "well to do" foreign cash buyers. I wish we knew just how big this effect is, certainly I suspect its quite large.

It would appear that we have ahead of us a period where the NZ and Auckland median price could easily increase 15% over each of the next two years and there is nothing anyone can do to prevent it.

The Reserve Bank are responsible for most of the increase outside of Auckland with their rules that have now pushed investors into those towns and cities, that a year ago they would never have considered. Now Auckland first home buyers invest in a rental outside of Auckland and stay renting in Auckland.

Back in Auckland the well heeled investors with big equity across a portfolio of homes are not effected by the 30% rule - in fact it has made it easier to buy as it has wiped out many of the competitors - ie first home buyers.

Throw in massive net migration gain, Chinese migrants buying a home for themselves and maybe a couple of investment properties, a government that is failing to put in place anything that will see more homes built, interest rates going lower and all the fuel is there for perhaps a 20% increase in house prices in Auckland by year end.

By which point the Auckland housing unicorn will be more precious than Sydney and London.

Not saying it won't happen of course. It's a vote of confidence in Auckland after all.

No it's a vote of how stupid people can be.

That was key-speak in case you missed the sarcasm :)

Ahhhh sorry

I dont see why there should be confidence in Auckland

Cities have their day in the sun and fade.

Think Dunedin or Detroit.

Its not as if its a Capital city that can live off the nations taxes.

Detroit's population dropped from 1.8 million to 700 thousand over a 60 year period.

Auckland's population is growing.

A lot of investment is going into Auckland. Did I mention the Waterview connection?

Auckland is a tourist hub. For some reason the Chinese have decided they want to see the world and are travelling like crazy.

Sure it may not last for ever but right here and right now it is booming.

Auckland regularly rates highly in all the surveys.

Auckland is NZs super-city. It makes sense to have a degree of confidence in it.

Why not have confidence in it? Do you have something better to do?

Zac,

If Auckland was ring fenced it would make no difference to me and possibly many other NZ,s.

In general its existance just makes life harder for the regions.

Also you probably dont understand that Detroit once had a reason to exist, its position on the Great Lakes and its amazing development of the automobile, you probably drive one. However times changed leaving it in ruins.

Auckland seems to exist to satisfy the international desire for financial safe haven and that could vanish well before the automobile, leaving an underutilised infrastructure.

Consider NZ migration from Auckland exceeds NZ arrivals so you must be expecting Auckland is an international haven, how long will that last?

I understand what happened to Detroit all right. No city in NZ is going to overtake Auckland in the foreseeable future. It is and will remain the hub of NZ.

You may have misunderstood the question.

Are you satisfied if NZ,'s are forced out of Auckland due to it being promoted as a international financial safehaven?

How long do you think that situation will last?

I don’t necessarily accept the premise of the question.

However, if I did accept the question's premise I would say I am not satisfied and I don't know how long it will last.

Unfortunately my satisfaction is of little consequence so I just ride the tiger over the ruins of the British Empire.

Obtaining 100% finance to purchase a rental property anywhere in NZ is a relatively simple process right now for those who already own real estate and a quick shop around the banks will likely see a cheap 3 year fixed mortgage available on an interest only basis at 4.05% - this will probably drop to 3.85% if the OCR is slashed again this week. No chance of a market correction this year or next. The GFC only saw a minor reduction in house prices and the Reserve Banks rules have not prevented house prices reaching record highs - good luck Mr Wheeler.

This paragraph by Bernard is spot on:

"At the moment, New Zealand's landlords see a one-way bet. They see central and local Governments failing to allow enough new house building to meet supply. They see interest rates falling despite years of warnings from officials about the risks of rising interest rates and they see little political appetite to tax either capital gains or land. The only thing standing between landlords and yet more easy money is the ability to leverage up their ample stocks of equity."

The rich get far richer under Mr Keys watch.

IT IS AN UNREALISED GAIN.

I am comfortable with the notion of unrealised gain otherwise known as ample equity. Unrealised gains are a good thing because you can't go out and spend it which is one of the reasons why owning a house and having a mortgage is good for most people. They can't easily blow it on an extravagant holiday for instance. I found when I didn't have a mortgage that I wasn't any happier.

Only problem is that the exit is a fairly small hole. If the market turns and the foreign buyer deserts the country your unrealised gain may turn into a very real negative equity if you have a mortgage. The other thing is that people have a tendency to bolt an ATM onto their house....

Kiwis have a tradition of just hanging on. Some people on this site seem to think people should sell when they make 500k or sell at the first whiff of a downturn. I think most owners instinctively know it is not a good idea to be too jumpy. People on this site are trying their best to freak others out while their counterparts talk the market up. People are being accused of being greedy while being advised to sell to realise the profit by the very same people making the accusations. It is pretty obvious that they want people to rush to the door.

I agree about not selling when there is a market downturn - if you are investing in the share market it's a time to buy more (unit averaging). The reservation I have is that while debt can magnify your gains it can also magnify your losses,

All of us knew there was a bubble. But a bubble in and of itself doesn’t give you a

crisis.... It’s turning out to be bubbles with leverage.

—Former Federal Reserve Chairman Alan Greenspan, CNBC Squawk Box, 2013

I agree about people and their "vested" interests on this site - all I am saying in the end is pay down your debt and as Warren Buffet said be "fearful when others are greedy and greedy when others are fearful".

Trouble is we have a 50/50 split of greedy and fearful here.

That what makes for such interesting debate.

It bothers me to see the "GFC only caused a minor reduction in house prices" line. MASSIVE interest rates cuts and bank bailouts and money printing saved the housing market. There are no rates to cut next time.

Another 9 cuts of .25 before we get to zero.

Then we have NIRP.

Then we have QE, & looser Govt fiscal policy.

New Zealand is a basket case now. It's not as if New Zealand has a lot to fall back on if things go south. If New Zealand has to rely on the policies you list... were in deep brown stuff.

Everyone else has been doing it for 5-6 years and they are all OK.

Whom for example....

Britain, America and Europe have hardly descended into the dark ages because of QE. When the rate gets to 0 in NZ it will be used.

Something like six trillion dollars of "wealth" was wiped out by the GFC in the US alone. Depending on where you live many people are still living with negative equity in their homes. It was and is a total disaster. Talk about myth making.

So 700b of QE is no big deal if 6T was lost in the GFC then? Lots of American cities are dying anyway so it enivitable that some prices are lower than 10 years ago. Im curious, how old are you? If you think that's too personal tell me to go jump. You think just like I did 15 years ago and I'm wondering if we were the same age with that mindset.

I'm 51. I accept that some US cities are in decline - Detroit is a well known example. The Dot-Com bubble destroyed five trillion dollars in "wealth" but the effect to the US economy was relatively short lived. The GFC has been much more destructive in terms of it's long term effect (asset bubbles with leverage are far more destructive) and while the economies did not collapse they aren't all that peachy either (and what other problems have been created).

Just to highlight something (not disagreeing)You know why it was short lived? There was no "too big to fail" mantra applied. As there should never be

The logic in the paper was that the Dot-Com bubble mainly affected the rich and mostly didn't involve leverage.

Interesting, Im 41 and had that mindset in my late 20's early 30's.

& you put on weight

Please understand that 5 trillion of wealth did not get destroyed, what happened is 5 trillion dollars was transferred to other people that would disagree with you, when in fact there are people now people who are 5 trillion better off...money is zero sum and does not disappear...

Not sure you're 100% correct there as speculation/perception of value can be destroyed. Much 'theoretical' wealth is based on this principle. And wealth can also be destroy by inflation making a currency worthless over time.

When you say 5 trillion in 'wealth' what construct are you setting that value by? USD? Real estate value?

Wealth is not exactly like 'energy'

Fair enough and what I am saying is when people say stock market crash is actually stock market win for those that sold at the high price

Well there is a silver lining; the NZD will be much weaker that will help our export market and increase tourism as it allow tourist more spending power making NZ a more attractive place to visit.

Thing is we really have to stop relying on property prices rising to keep our GDP growing as it's just not sustainable.

Yes, the dollar will be lower. Another subsidy from consumers to exporters. Good thing consumers have no other pressures on their wallets, like...oh I don't know, runaway housing costs?

Would any of that fix the fundamental problems? I don't think so and I can think of a few examples right now as also you should be able to highlight this fact.

But there is QE. Its worked elesewhere and the RBNZ will follow the same path. There is still 2% of rate cuts to go first. That could take 12-18 months.

Bollocks - QE hasn't worked - all it has done is put a great deal of money into circulation which is looking for "safe haven assets". And all the other acronyms that followed which would "solve" the problem.

Id love to see how how the GFC would of turned out without QE.

True - but that doesn't mean it "worked", it just created other problems..

Every action has a reaction. There was no alternative at the time. It was a choice of create another asset frenzy or have 3/4 of the population living on the streets was also an easy choice to make.

No sorry they made the wrong decisions. "Too big too fail" will kill it all now anyway. All they have done is kick the can down the road a bit longer but now the hurt will be so much more painful.

Are "too big to fail" bailouts and QE the same thing? I thought they were separate attempts to address separate problems.

It has, ie we would be way worse off without it.

Well, the QE money never left the primary dealers' H3 reserves ledger at the Federal Reserve. Furthermore, the same primary dealers declined to leverage the fractional reserve facility whereby the $2.358680 trillion registered free reserves would be reclassified as required to support ~$21.2281 trillion created credit at the current 10% reserve ratio.

At any rate it shore up the banks who have lent it out.

That is relative.It has created enormous problems that still have not been addressed - threats of deflation , stagflation, unemployment - rocketing asset prices that don't bear any resemblance to peoples incomes etc etc.

Bankers / economists didn't know what they were doing in 2007 and still don't know.

- Deflation is from over production.

- China with Steel and other crap we dont need.

- The wests proxy war with Russia where they have stopped importing dairy products.

- Fracking from the US to drop oil prices to hurt Russia

Unemployment - What?

- US 5 years, dropped from 10 to 5%

- UK 5 years, dropped from 8 to 4.9%

- NZ 5 years , dropped from 7 to 5.2%

Rocketing asset prices are better than dropping asset prices.

Not everyone believes that same thing , not everyone thinks the same way - BadRobot

No Steven, all the bank rot would be gone. That would be better for all of us in the long term. Saving fraudulent practices is never a good or sound idea

UBI is still to come, helicopter money direct into people's bank accounts.

Inflationary yes, solve anything? No. What is needed is a total across the board disincentive to hoard and flick property. That means putting aside conflicts of interest and personal gratification and incentivise real ethical industry that produces jobs and innovations. If that proves impossible then we will eventually welcome a bloody revolution or WW3. Just my opinion. The conclusion being that promotion of inequality leads ultimately to conflict across the class system whose is inevitably produced.

I think the ultimate conclusion of the capitalist system is total war.

capitalism alone yes, thus we must have a bit of everything to keep the peace. Capitalism mixed with socialism where profits and resources are fairly distributed, and a slice communism to make sure none are left behind without the essentials to make something of themselves. As opposed to ever increasing concentration of wealth to a minority leaving the rest to fight for living scraps

Certain regions which I dare not mention are only up a few % on 2007 yet mortgage rates are HALF what they were 2005-2007.

I just bought a house mainly over the ph that nets $100 cash in pocket per week after all expenses on 100% borrowing against revalued existing properties. It's free $ in a region where prices are due for a catch up but even if they don't I'm happy to earn an extra 100 a week

As I have said before, I suspect that the assumption that there should be a linear relationship between CPI inflation and the OCR across the full range of economic conditions may well be a flawed theory when we get close to 0 or negative inflation.

For instance if we were to increase productivity by 20% across the full economy, then prices should drop 20% wrt wages. Surely this is a good thing as we could all equitably enjoy the benefits of our increased productivity. One could perhaps expect a "virtuous" cycle of even greater productivity as a result because of increased consumption/production. In our present OCR/CPI model the consequential price falls from increasing productivity would mean that a 20% fall in the CPI would be disastrous and we would be charged huge interest on our deposits and almost paid to borrow in an effort to stimulate more consumption and CPI inflation. Surely this is nonsense and in-fact one could expect that increased consumption would lead to economies of scale and further price falls!!! This is almost starting to seem like the situation that some countries are getting into and the consequential increasing liquidity has no where else to go other than speculative investment in capital assets. I think that somebody needs to have a long hard look at some of our economic management assumption and theories.

If the National voter base was concerned about this all of this they would be lobbying Govt, but they are not. They are scoring $2 billion in rental subsidies.

Everyone is distracted by China, I'm more concern by NZers. The cohort is easy to spot, European, aged 40-80, driving Audi/BMWs under 2 years old.

You're all distracted, fighting it out.

Their silence is deafening. Open your ears people

Good answer Zac,

And we all do....

What imperial britain took from us was our pride...

What? They gave us the best language in the world, a fantastic legal framework, democracy and trade for 100 odd years while we worked our way up to 1st world OECD status. How you equate that to stealing our pride makes no sense at all.

Who is "we"?

I have an irish passport....

Imperial britain threw the lot away in order to access the EU.

Hmmm,

I was watching a movie at the same time as writing and threw that line away.

As a second pitch, perhaps as possibly the youngest colonial country, we havent developed a national viewpoint that economic piracy isnt acceptable.

Our goverments dont have the tenacity of say the Greeks in negotiating on the International stage.

Does that sound better?

Breaker Morant?

Great movie

Lord Kitchener: Needless to say, the Germans couldn't give a damn about the Boers. The diamonds and gold of South Africa they're after.

Major Bolton: They lack our altruism, sir.

Lord Kitchener: Quite.

Ill watch that movie but no, "Tangarine" filmed on the streets of LA using a Iphone 5S.

Not recommended for grownups...

99cent movie on AppleTV

Key hinting at possibility of a land tax on foreign speculators apparently. Of course we know damn well that the criteria will be so narrow as to appear to be doing something but the reality will be just more minor tinkering with no real genuine effect

it will be interesting when the figures come out, my guess will be below 10% as a lot of the buying is by locals on behalf of.

as for a land tax be wary as once its in its only a matter of time before it gets extended.

and also will the proceeds go towards infrastructure, roads, rail, schools, hospitals, or into the consolidated fund(slush fund} for the politicians to spend on there nonsense projects

You know the data is not good

They have had 6 months of data and it hasn't been released

It's being withheld

Slippery John Key commented on TVNZ's Q and A

The Government is waiting for "better data" on whether there actually is a problem

Which is code for saying the data so far does not support the Govt's declared position

So we will wait until the data supports the govt's stated position - there is no problem

When the data is finally released you can guarantee it has been sanitized

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

Who exactly is compiling this data?

Dr Nick Smith says in NBR interview it's being collected by the IRD

Opposition parties have called for a publicly searchable database of non-resident buyers. Mr Smith said the information being collected by the IRD from October is “not a register” of foreign buyers

http://www.nbr.co.nz/article/smith-promises-fix-overheated-auckland-mar…

Well, If NS has anything to do with it then god help us. I see he predicts (that's all I can call it) only 1.2 % is foreign owned? That sounds like total BS and I live in Nelson where even that figure would be way under the reality. Are they just collecting data on Auckland?

10%? I reckon way less, politicians use language to lie, dodge, weave and manipulate the truth. For example the exact words he uses are "foreign speculators". Not foreign investors, not migrants or non resident migrants. Foreign speculators....even NZ speculation they have a hard time admitting too.

My view has been for some time now that a land tax of some sort is inevitable because of the macro picture, decreasing sources of unearned income. When conventional sources get bad enough, the rule of the low hanging fruit will apply. Property owners are sitting ducks really.

when you have revenue not increasing due to low inflation, a government will always look for another source of income, land tax is coming, it will start small then spread over time to all properties .

Rather than introducing new taxes wouldn't it make more sense to just remove the capital/revenue distinction from existing tax rules. If it's income, tax it. Results in a broader tax base allowing tax on labour to be reduced.

Our tax system needs to evolve with the times. The capital/revenue distinction made sense when it encouraged productive investment.

No IMHO, the thing about a land tax is I think it has the as same "stickiness" as rates? hard to dodge with clever accountants. It also then means foreign owners pay tax, which they probably pay little if any right now?

Everyone else around the world is starting to realise they have to do something to kerb foreign money inflows. Hong Kong and Singapore with their 15% and 10% stamp duty for overseas buyers have calmed their property markets down. 10% seems a good level to pitch it at.

And so too is John Key I suspect....

But he just doesn't want to admit it...

The fact that the government has investigated the problem suggests it is on the radar and looming large.

It's ok, The PM doesn't think foreign buying of houses is a real problem:

"His own "gut instinct" was that Chinese buyers in the Auckland market were New Zealand-based"

Technically maybe, but the source of the finance/buyers is definitely offshore.

and what are income tax and salary levels like in those countries.

if monetary policy is too loose, you can concrete over the entire length and

breadth of the NZ and house prices would still rise. There is no shortage of housing. What

there is, is an imbalance between demand and supply and demand is excessive because

of crazily loose monetary policy.

The increasing and considerable demand from foreign and related parties is not subject to NZs monetary policy. They have cash.

'Loose' monetary policy has been in effect for decades in NZ. Our interest rates are double every other western country.

Even increases in OCR and increased LVR have no effect under the seige of offshore money pouring into NZ buying 1000s of houses.

Just to clear something up, money does't "pour into NZ". People don't arrive with sacks of NZD.

Actually, some $$$ does actually arrive in paper cash.

12 extended family members x $10,000 = $120,000 times 3 or 4 trips backwards & forwards from Mumbai or Shanghai.

Other more circuitous methods include multiple transfers via friends, contacts, family and 'paid electronic mules'. The variety of methods is astounding.

Regardless, these foreign or offshore- related, using PRs or citizens, or not, are buying AucklNd houses without necessarily needing to borrow from NZ banks.

No. They buy NZD first, then they buy houses, unless they're buying houses in yuan.

They bring US dollars, then exchange.

@ Mortgagebelt

I agree. Our mortgage rates are higher than other parts of the world but historically they are still cheap and the amount lenders find acceptable to lend in relation to income is now much higher than historically.

We are seeing huge property price increases from a combination of inflowing foreign money looking for a safe haven and a considerable number of NZ nationals mortgaging themselves to the hilt with multiple properties....( buying to rent ).

So it will not matter how many houses are built the demand will be supported by the macro enviroment of cheap enough money and ability of foreigners to move money easily.

This is a bubble that will burst when or if interest rates rise substantially and we also manage to stop foreigners bringing in money to invest in our property.

One thing is for sure the government seem to have gone very quiet on this. I am hoping they are waking up to the growing anger and frustration. Well done to the media who are finally starting to reflect this discontent with New Zealand as a place to live. Such a shame what has happened to the young people in this country over the last few years.

You do have a lot of freedom in NZ. The equality of people in regards to race, religion, gender, sexual orientation and place of birth is now enshrined in law. However that freedom comes at a cost. No one is given special treatment just because, say, they were born here.

Consider Singapore where they ensure that young Singaporean families have access to housing. And I mean only Singaporeans and 'normal' families, not mixed couples or gay couples. Young men have to do two years compulsory military service as well.

Recognition of same-sex unions in Singapore

National service in Singapore

I would consider swapping our system for theirs but would you?

In Singapore, access to public housing is the biggest benefit granted to married couples and is officially recognized as key pillar of support for relationships. Public housing is the most affordable type of housing for the middle and working class due to the high price of housing in Singapore.Purchasing a HDB flat is a major step towards married life for almost all couples intending to formalize their relationship and is entrenched in Singapore society. Upwards of 80% of Singaporean families live in public housing apartments sold by the government Housing Development Board.

Same sex couples in Singapore, whether citizens or foreigners, cannot own their own homes through the public housing scheme, and many rent as they are unable to afford private housing. Same-sex partners - both must be above 35 and Singapore Citizens - can purchase a flat under the Joint Singles Scheme.

Private housing, a type of property typically 1.5 to several times more expensive than public housing, but open to the public and foreigners, may be purchased by same-sex couples both Singaporean and foreign.

Legal and immigration rights are not awarded to binational couples, where one partner is a Singaporean or Singaporean permanent resident. Dependent visas, which are usually issued for heterosexual spouses, are not available for same-sex couples. Tax rights, wills, and spousal insurance benefits do not include LGBT couples. There is no recognition of same-sex couples in most areas of concern such as hospital visitation and Central Provident Fund benefits.

Of course there are still wonderful things about NZ which makes it all the most difficult as it will be a hard place to leave. But when it comes to home ownership there is a systemic failure here. You are not acknowledging that failure, Zachary, as the system favours you.

It is really only Auckland that you have a problem with. I just think it is probably not enough to found a revolutionary movement on. NZ should perhaps encourage people to get other places more established. If Auckland was made more affordable for everyone it may not be able to cope with the growth. We are already getting gridlocked. It would make Auckland even bigger and the provinces even less desirable

I have just heard this morning that my neice is looking at buying her first place in Hamilton for 330k. With 33k down and getting in a flatmate this seems very doable

I have my own small business reliant on Auckland specific clients and I also employ a couple of Aucklanders. Next suggestion.....

Buy a place you can use as your business premises like an old shop? Buy in Hamilton and rent it out? Keep renting in Auckland and focus on building your business?

It wouldn't work. Not with my business - need to have daily access to CBD. And I hear it is hard to buy houses in Hamilton too now. My point is that for most of my generation in Akl the choices are 1) stay in Auckland renting with no hope of home ownership 2) leave our businesses, jobs, families to live in another city where we know no one and where the locals, quite rightly, may not welcome us with open arms 3) move overseas where we know even less people and realise other countries have major problems too. This is why we are angry. I am hoping that the RBNZ will do something to stop the market in its tracks but I am not holding my breath. Have long given up on the government and will be voting for the Greens unless Labour change their stance. Can I just add that I provide a valuable service to Auckland, employ local people and that I love it here despite this situation.

Taint just Awkland....it is a Global phenomenon. A little interest....suddenly becomes a lot.

http://www.telegraph.co.uk/personal-banking/mortgages/will-millions-of-…

I wonder whether the property market is subconsciously factoring in much lower mortgage rates ahead. I see in the UK a 10 year loan with 35% deposit is 2.75%, less than half that available in NZ, and shorter terms like 1-3 years are much, much lower than that even. It seems inevitable that interest rates will reduce again here, and soon, to boost inflation and preserve our currency's competitiveness.

Is there any plausible reason AGAINST inclusion of real estate price inflation in the calculation of the CPI?

Is there any plausible reason why our so-called government does not reduce the quantity of low skilled immigration? Skilled people might have a realistic chance to make it in the hinterland, but petrol pump experts and check out professionals necessarily will find more jobs in AKL.

And what is wrong with 0.4% CPI in the first place? Oh sure, if it is suddenly 2% due to central planner manipulation NZ will instantly turn into a land of milk and honey.

I find it unnerving that Hickey et al keep flogging the dead cow. Stupid interest rates and money printing have not helped Japan, will not help Europe and have not helped the US all the much either. You need creative destruction in a market economy. If you keep broken business models alive thru political and central planning bank interference, you only cement eternal low growth, Japan style, because people and capital are not forced to move into more promising investments after the old ones are bankrupt.

The CPI includes rents and the cost of new houses (excluding land).

The key point is that the CPI excludes land value inflation. That is where almost all of the increase is coming from, land value not improvements value. After all, the land component of real estate (and its factors location, accessibility and nearness) is what is scarce and in demand relatively speaking, not the depreciating bricks and mortar placed on top of the land.

So why does CPI exclude land value inflation? One reason may be that it is nationally very inconsistent by nature, and would therefore make a nonsense of a national CPI figure.

Consumers don't buy land on a daily, weekly, monthly basis so land price increases don't affect the majority in any given quarter.

But they pay for that land through mortgage payments on a daily, weekly, monthly basis or spend less on consumer items to ensure they make their mortgage payments.

But a) that amount doesnt really change unless its the Interest rate component which is going down (or up) and hence deflationary in effect right now, freeing more money for some ppl to spend. b) not everyone has a mortgage, some rent, quite a few are debt free. Therefore they are not paying for their land at all, except rates which I believe is counted (or rent).

Then on top of that quite large parts of NZ are not seeing much of a price increase, some still dropping? so we are in effect cutting more and more of the effect out of CPI. Oh and on top of that the Auckalnd suburbs going crazy probably have a % who are cash buyers or landlords and CPI is consumer price index not business price index.

Then its considered housing is an investment and rightly so IMHO.

The CPI is, at best, an inexact figure - representing a fixed basket of goods and services which may not reflect any particular group's purchases or lifestyle.

The price index universally understates the actual cost of living increases which are more difficult to measure than a basket of goods.

It takes no account of quality of goods or materials or services or changes in what services are provided for a certain price. Cheaper (but lower quality) building materials will lower the CPI. A house which leaks in five years requiring significant additional cost is not considered. etc.

While it a measurable index - and much revered by those wanting to reduce inflation, it does not necessarily relate to quality of items or quality of life or real increases in cost of living.

No, I dont agree, in fact I think you are wrong, end to end. CPI universally reflects the cost of living. What it doesnt do is reflect the costs across demographics nor socioeconomic well, but its there for a trend to watch for the changes which it does do well. So maybe you could make it more accurate for say demographics but does that help? not for what the CPI is intended to do, indicate the state of our economy overall.

"no account....of changes" actually my understanding is yes it does as best it can.

If cheaper non-preforming building materials are used then the owner can claim the materials do not comply and the work did not last, and get repairs/compensation.

The very idea of CPI is its comparing like with like and not "OK" with "crap"

I see in the UK a 10 year loan with 35% deposit is 2.75%

I mentioned that to friends who have a London Flat , they said why fix for so long, their 1 year fix is only 1.75%, thats 57% more interest to pay. They don't believe rates are going anywhere.

They are right in as much as the central bank would cause carnage if rates doubled and then would have to do more QE.... I see their biggest risk being a Brexit and the UK having to raise rates to stabilise the pound.

I don't either, and I think many don't,and that is one of the key factors of driving inflation apparently, that ppl expect it and put up prices / wage claims in anticipation.

An astute analysis on increasing interest rates causing more QE, quite correct IMO.

My understanding is that in the UK the banks are clawing some of the money in with high set-up fees this would be a repeated charge on fixing for 1 year at a time but a '1-off' charge on a 10 year mortgage.

I confess to having a small mortgage on a property in the UK. I pay 0.26% above base rate. Ie. 0.76%. Took it out in 2007.

The main reason the Auckland property market is booming is the accelerating collapse of most other western nations, along with several 'developing' nations.

The grossly incompetent self-serving bureaucracy that now has a stranglehold on NZ society via local and regional councils is able to present a façade of success in the short term by 'borrowing from the future', thereby exacerbating numerous long term predicaments.

Needless to say, even as the financial, economic and environmental evidence indicating we are on a path to absolute catastrophe mounts by the day, the NZ Government ignores everything that matters, and keeps up the pretence nothing is wrong.

An alternative source for ice data now confirms the unprecedented meltdown recorded earlier by NSIDC is continuing, i.e. lowest-ever ice cover which is declining at a phenomenal rate.

https://ads.nipr.ac.jp/vishop/vishop-extent.html

The repercussions of this accelerating meltdown are enormous. Meanwhile, atmospheric CO2, the driver of many environmental catastrophes, continues to surge, and is up a staggering 5.39 ppm in the latest year-on-year data.

Most of the catastrophes that will ensue from the insane short-term policies promoted both in NZ and overseas (environmental, social and financial) will not fully manifest for a while, of course.

This article states that: It's not the Governments fault for the Auckland fiasco and out of control housing market - it's actually our own fault!

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

Who initiated this 'angle'? Nationals spin doctors?

Unbelievable reversal of responsibility!

Hmm, I read the article and I think you totally mis-interpreted his overall message, and I could not find that sentence you say is stated anywhere?

He DID state this:

"What we lack is the political motivation to enact the right combination of these solutions with the kind of urgency that will have an impact."

Hmm, I read the article and I think you totally mis-interpreted his overall message, and I could not find that sentence you say is stated anywhere?

He DID state this:

"What we lack is the political motivation to enact the right combination of these solutions with the kind of urgency that will have an impact."

Hmm, I read the article and I think you totally mis-interpreted his overall message, and I could not find that sentence you say is stated anywhere?

He did state this:

"What we lack is the political motivation to enact the right combination of these solutions with the kind of urgency that will have an impact."

Hmm, I read the article and I think you totally mis-interpreted his overall message, and I could not find that sentence you say is stated anywhere?

He did state this:

"What we lack is the political motivation to enact the right combination of these solutions with the kind of urgency that will have an impact."

"But there is no point blaming our politicians for reflecting the will of their most reliable voting block."

He lets the Govt off the hook, as they are simply following/reflecting home-owners & PIs, & need their votes..

Ok, he contradicts himself. Remember in the U.S. after 2008 how people were trying to blame the sub primers for the bank collapses? A similar argument will be pushed here I'm sure if things go belly up. We don't have subs of course but we do have irrational borrowing

It is our fault, us and the generations before us who allowed ourselves to be lead into consumerism and materialism, allowing a banking system to create "money" out of thin air and charge interest on it, by not demanding better leadership from our governments and institutions, by being greedy and selfish and buying into the notion of being individually "rich" rather than asking why can't everyone be rich, by believing in the trickle down theory, by believing in the economic growth model and economic theory itself.

Sorry about the repeated postings there. It appears I had a server issue

The double postings could be fixed by tiny bit of javascript to disable the submit button after click.

They could also remove the tea towel flag while they are at it.

Yes, that tea towel is starting to annoy me. Like someone can't accept a democratic result

especially on Anzac day when we remember those that fought for our freedom under our flag

bad form

Comment #200. Did JK get permission from China President or vice-versa re the land tax.

Or did polling indicate time for a policy shift?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.