(This is part two of an article. Part one is here).

If a politician came to you and said he thought he should tax the income from your retirement plan today, right now, at 50% (no matter where you are in the retirement process, that would certainly hurt the ability of your portfolio to compound), what would you think (other than that he was completely Looney Tunes)?

But that is exactly what the Federal Reserve has done. They have reduced the fixed-income returns in your retirement plans and the broad pension plans upon which so many people are dependent to practically nothing in the name of propping up asset prices. They have painted us all into the mother of all corners, from which there is no rational exit.

Rather than allowing rates to normalize years ago when they should have, the Fed and other major central banks have now unbalanced the financial system so badly that the markets very likely will have another tantrum – no, make that a grand mal seizure – when rates start to rise. And that means your bond funds will get killed as well as your equity funds. It is going to be an unmitigated disaster for retirement and pension plans, and any right-thinking person understands that.

That is precisely why the Yellen Fed is having trouble coming to the point of actually normalizing interest rates. They know the reaction from the stock market is going to be really, truly, unbelievably ugly. And because they have been the pushers of the heroin of ultra-low rates, they are going to be blamed for the withdrawal.

Larry Summers went on a full-throated rant last week in the Washington Post. It’s instructive reading. His title is:

“The Fed thinks it can fight the next recession. It shouldn’t be so sure.”

He points out that despite all the happy talk from Janet Yellen at Jackson Hole, the Fed doesn’t have any ammo left. His paper and others point out that typically the Fed reduces interest rates by about 550 basis points in a recession. If a recession kicked in tomorrow, that would plunge us to the breathtaking interest rate of -5%. As I wrote last week, a footnote that Janet Yellen cited approvingly in her paper suggested that rates should go to -6% or -9% during the next recession to be effective. Now here’s Larry, teeing off:

My second reason for disappointment in Jackson Hole was that Federal Reserve Board Chair Janet L. Yellen, while very thoughtful and analytic, was too complacent to conclude that “even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.” This statement may rank with former Fed chairman Ben Bernanke’s unfortunate observation that subprime problems would be easily contained.

Rather I believe that countering the next recession is the major monetary policy challenge before the Fed. I have argued repeatedly that (1) it is more than 50 percent likely that we will have a recession in the next three years (2) countering recessions requires four to five percentage points of monetary easing (3) we are very unlikely to have anything like that much room for easing when the next recession comes.

And here is where one of the highest of High Priests and I agree. Models have serious limitations, and we should be very skeptical of policies based on models that rely on past performance:

There is an important methodological point here: Distrust conclusions reached primarily on the basis of model results. Models are estimated or parameterized on the basis of historical data. They can be expected to go wrong whenever the world changes in important ways. Alan Greenspan was importantly right when he ignored models and maintained easy policy in the mid-1990s because of other more anecdotal evidence that convinced him that productivity growth had accelerated. I believe a similar skeptical attitude toward model results is appropriate today in the face of the clear evidence that the neutral real rate has fallen. I pay attention to model results only when the essential conclusion can be justified with some calculation where I can see and follow each step….

I suspect that prevailing views at the Fed about the efficacy of quantitative and forward guidance substantially exaggerate their likely impact. I don’t think the Fed has taken on board the lesson of the three-year period since QE ended. If longer-term rates had risen after QE and forward guidance ended, this would surely have been taken as further evidence of their potency. It follows that the fact that term spreads have fallen substantially since the end of unconventional policy, as shown in Figure 3, should lead to more skepticism about their efficacy.

(And hot off the press – it literally just landed in my inbox as we were about to send this letter out – here is another, possibly even more heavyweight indictment of economic modeling and the state of the economics profession in general, from Paul Romer, chief economist of the World Bank and former NYU and Stanford prof. He just released this version of his paper today, and he notes that it’s a work in progress.)

What is new in the Fed’s (and other central banks’) performance is the sheer magnitude of monetary manipulation in recent years, and the very constrained maneuvering room the Fed now has as a consequence. And of course it’s questionable whether they should even be trying to maneuver the economy to the degree that they are. The current predicament is a direct result of mistakes made during and after the last financial crisis.

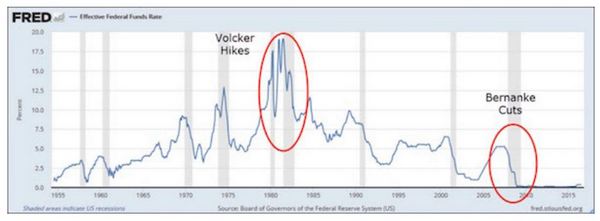

Here is a long-term chart of the federal funds rate, the Fed’s main policy tool:

The gray vertical bars represent recessions. You can see how the Fed has historically dropped rates in response to recessions and then tightened again when those recessions ended. I red-circled the particularly drastic loosening and retightening under Paul Volcker in the early 1980s and Ben Bernanke’s cuts to near-zero in 2008.

To this day, the Volcker rate hikes are legendary. No Fed chair has ever done anything like that, before or since. You hear it all the time. Problem: it’s not true.

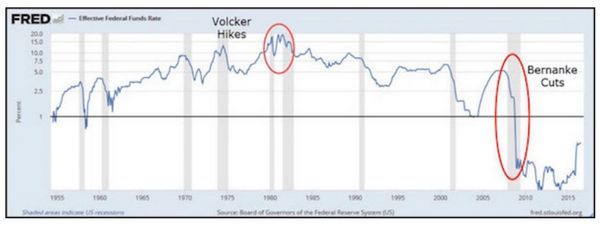

Here is the same chart again, this time with a log scale on the vertical axis. This adjusts the rate changes to be proportionate with percentage rises and falls. The percentage change between 5% and 10% is the same as between 10% and 20%, since both represent a doubling of the lower number.

Looking at it this way, the Volcker hikes are tame, almost unnoticeable. Meanwhile the Bernanke cuts dwarf all other interest rate changes since 1955. Nothing else is even close. Bernanke’s rate cuts were far, far more aggressive than Volcker’s rate hikes.

Why did Bernanke et al. cut rates to zero? Because moving rates up and down was all they knew to do. It had always worked before. If it wasn’t working this time, they figured more of the same should do the trick.

Well, more hasn’t done the trick over the longer term, either. It might have worked for a year or two, but after that the Bernanke-led Fed was so scared of a negative stock market reaction that they kept rates artificially low for eight years – and decimated fixed-rate income returns of pension funds and retirement plans for the middle class. Central banks all over the world did the same, and more. The suffering caused by this bone-headed policy approach has intensified for all these years. You may not be suffering yourself, but I bet someone close to you is. And I flipping guarantee you that your retirement funds have suffered.

Now, would the markets have screamed bloody murder if the Fed had raised rates back to 3% in, say, 2010 or 2011? For sure, but then the members of the FOMC are the High Priests who have taken it upon themselves to make these weighty decisions. They are not there to be popular; and whether they know it or not, they are not there to worry about the level of asset prices.

In any case, the result has been nearly a decade of return-free risk for millions of savers and investors. Those living off of fixed-income portfolios – never mind simple savings accounts or CDs – have grown steadily more desperate as each holding matured and couldn’t be reinvested at a decent rate.

And so they have created a bubble. My friend Louis Gave writes:

But there are “lows in bond yields”, and then there is the reality of a third of outstanding OECD government bonds offering investors negative yields. This latter proposition makes no financial sense whatsoever. Who would willingly pay a percentage, year after year, to have money taken off their hands? The answer suggests that one candidate for the definition of a financial bubble would be:

1) The establishment of prices that, by any historical measure, make no sense whatsoever.

2) The broad financial community, although acknowledging that these prices do not make sense, persuades itself, perhaps through the use of new valuation metrics (remember market cap per eyeball?), that in some greater scheme of things they can in fact be rationalized.

Now, the Fed will argue that the low rates did work. The economy emerged from recession. Unemployment drifted back down, however slowly. Yay for us, said the Fed.

Don’t buy that statistical economic garbage. The economy recovered in spite of Fed policy, not because of it. The economy recovered because business owners, entrepreneurs, and workers rolled up their sleeves and made things happen. It involved a lot of pain: layoffs, asset sales, lost customers, and more. But the hard-working citizens of this country slowly and painfully pulled themselves out of the nosedive. Those are the people who deserve the credit. As they have for every recovery since the Medes were trading with the Persians.

Of course the High Priests and the politicians take credit for the recovery. But to borrow a phrase, you did not build that. Even while talking up the need for economic growth and for businesses to thrive, they disdain the actual workings of the free market, not giving it credit when it, not monetary policy, is actually the driver of the economy.

Look where we are now. The supposedly humming economy is certainly going to suffer another recession in the not-too-distant future. What then? The Fed can’t cut rates again unless it first raises them considerably from here. And they can’t do that because then they would no longer be supporting those “decent equity prices” that are so important to Stanley Fischer.

So, for lack of anything else to do, the Fed is preparing to send interest rates below zero when the economy next needs goosing. That was clearly the message from Jackson Hole. Fed economists truly think that negative is the right direction to go with rates, and that we plebeians should simply trust them to puppeteer the economy.

And they point to the data. Or their interpretation of it. They are correct that they lowered interest rates and kept them low overlong and that the economy has kind of, sort of, modestly recovered. Yes, both of those things happened at the same time. There is undoubtedly correlation, but the High Priests see causation. They think that the one thing (low rates) led to the other thing (recovery).

Central banks were trying to get the economy going again, and the mandarins at the major central banks think that low rates are the driver for employment, so it is worth reducing interest rates, which destroys returns for retirement plans, pension funds, and normal businesses that need fixed returns, in order to drive up employment. The fact that there is no evidence other than correlation to demonstrate that low rates were actually the cause of lower unemployment and recovery does not slow them down a bit. If any science student resorted to the same conflation of statistical correlation and causation, his paper would be thrown out and he would fail the course. But that same nonsense passes for academic excellence in economic circles.

An economist sees what he wants to see and disregards the rest, to paraphrase an old song. The Fed is plenty willing to disregard the “financialization” of the economy, which has made it cheaper to buy your competitors than to compete with them and has resulted in reduced capital spending and lower employment. They would say that without their lower monetary rates there would have been even less capital spending. The fact that credit spreads are at their lowest level ever and capital spending is punk doesn’t seem to fit in their equations. They fail to see that correlation. But it’s not a lack of capital that is the problem. It’s the lack of decent opportunities, even at ultra-low rates, to put capital to work.

Admittedly, that is not just a problem with the Federal Reserve. Opportunities are also constrained by the ridiculously overregulated business environment, a tax structure that makes no sense, and debt that is exploding not just in the US but globally. The whole world is upside down.

I should note here that there is considerable disagreement about central bank behavior in economic academia. There are many accomplished economists who viscerally disagree with current central bank philosophy. Much of the argument falls into the “How many angels can dance on the head of a pin?” category, a debate over relatively meaningless trivia having to do with largely nonsensical topics, but you can find serious contention occurring at even our most high-falutin’ universities. So please don’t think I’m labeling all economists as arrogant Philosopher Kings. No, just the ones who advise and run central banks.

I should also note that many of the Federal Reserve regions deliberately choose centrist or independent regional presidents who are not in sync with the Governors of the Federal Reserve. There is a similar lack of consensus at the ECB. And at the Bank of Japan. But, by hook or by crook, the reigning central bank paradigm has clearly shifted toward policies that just a few decades ago would have been seen as utterly radical and unhealthy. Who even muttered the words negative rates in the ’90s, or even in the depths of the crisis in 2008?

How in Hades did we arrive in a place where negative rates were considered a good idea?

One of the most patently stupid ideas ever cooked up in academia is now seen as rational and globally applicable. I equate that sort of thinking with the rationality that says, if five leeches sucking blood out of the patient works, maybe we should use 10. If one virgin sacrifice helped satisfy the Volcano God and kept him from blowing his top this year, maybe next year we should give him two.

The problem today is that if you call into question the High Priests’ interpretation of the data, you are consigned to the economic basket of deplorables. In their minds, you simply don’t comprehend what is to them self-evident. And because they control the levers of power, they are going to do what they think they should do.

And that is to balance the interests of savers and retirees and pension funds against the interests of banks and stock market investors – and then lopsidedly favor the latter. The imbalance started with Greenspan and the so-called “Greenspan put,” but Bernanke doubled down with his total capitulation after the Taper Tantrum, rather than looking the market in the eye and saying, “Deal with it.”

So coming back around to what I told Newt [Gingrich] in my letter (and then followed up on with a two-hour phone call), yes, the economy is rigged. But it is rigged by an economic priesthood that is in the seat of power at central banks around the world, and particularly at the Fed. Wall Street (and, admittedly, small-scale stock market investors) are simply the beneficiaries of the policy. Of course the big boys on the Street do hire former Fed economists and governors as consultants, so the entire setup is incestuous. But since, in the current mania, Federal Reserve policy drives the markets, it makes perfect sense for Wall Street to hire people who were once in the belly of the beast and can still read the entrails and tell their bosses what is likely to happen so they can make sure to run ahead of the curve. It would be foolish and an abdication of their fiduciary responsibility to their shareholders and investors not to do so.

What should we do?

There are not many options. Maybe someday we’ll elect a president who will replace Federal Reserve governors with those who favor allowing the market to set interest rates. Or maybe we could get Congress to remove the Federal Reserve’s mandate to achieve full employment (as if interest rates that are far lower than natural market-driven rates can make much of a difference on employment) and take that responsibility for themselves, rather than trying to blame the Federal Reserve for employment numbers. And in the absence of those unlikely events, perhaps we can rally some members of Congress to really put the heat to the Federal Reserve about negative interest rates.

Let me make it clear that if somehow or other I was made the Head Philosopher King and decided to allow the markets to set interest rates, the ensuing volatility and problematic markets would be serious for more than a few months. My idealistic move would likely precipitate a serious recession as markets adjusted. There is no magic wand to get us to normal. If there were, I’m pretty sure the Federal Reserve would wave it at once, because I think everybody realizes that rates should already have been normalized – and that to do so now is going to be problematic. We really have come to a place where there are no good choices.

At the end of this letter (which is coming, I promise) I will give you a two- or three-paragraph summary of what I think the country should do, as I did in this letter a few months ago. And even that summary will be chock full of economic heresy that I find myself struggling to accept, because of the untenable situation we find ourselves in. We will be only a few years into the next recession when total US debt tops $30 trillion. Wrap your head around what the interest-rate bill on the federal debt will be if rates are normalized. Yes, everybody can see that that would be ugly, too, and create its own crisis.

What will happen from here

Here is the most likely scenario I think we are facing. We are going to go into the next recession with interest rates still stuck in the sub-1% range, not giving the Fed much ammunition. There have been numerous studies from within the ranks of economists who could certainly qualify as High Priests that show quantitative easing didn’t really do anything, other than maybe goose the stock market. There is also no data demonstrating any positive benefit from the so-called wealth effect, which was all the academic rage at the beginning of this process. Forget the wealth effect – the stock market going up does not trickle down to the average guy on Main Street.

(I find supreme irony in the fact that the very economists who derided supply-side economics as trickle-down economics have adopted trickle-down monetary policy. Seriously, that is so messed up on so many levels.)

My friend Dr. Lacy Hunt has identified some 15 serious research papers that say the money multiplier for government spending is very low or even negative. Of course, you can also round up many neo-Keynesian papers whose authors see a fabulous multiplier for government spending, so Paul Krugman and friends go on urging ever more deficit spending.

But the Federal Reserve will not sit on its hand and do nothing. We will get quantitative easing on a scale that is currently unimaginable, blowing out the Fed’s balance sheet to a level that is unrecognizable. Unless there is considerable pushback from Congress – and I do mean considerable, not just the usual suspects on the far right of the Republican Party grousing about an out-of-control Fed – we are going to see negative rates in the world’s reserve currency. Then there will be a regular snowstorm of papers from the High Priests, conclusively demonstrating that negative rates will have all manner of positive effects on the economy and employment. And none of them will be worth the electrons used to publish them, because their conclusions are just theoretical blather, based on outmoded assumptions about the way the world works.

The central bankers of Europe who are experimenting so exuberantly with negative rates came to Jackson Hole and told everyone that the rates are working wonderfully. Never mind that the hoarding of cash in Switzerland is at astronomical levels. (It’s a fascinating arbitrage: bank rates are -75 bips, and you can insure your cash in a safe deposit box for about 10 bips. And in Switzerland you can find a bill worth $1000. It makes total sense.)

Negative rates will drive consumer spending down, not up. They will result in less income in retirees’ pockets, forcing them to save more, work longer, and spend less. A negative rates regime must be aggressively opposed by the public to the point that the Fed does not feel capable of actually initiating such a program. Our battle cry must echo William Jennings Bryan:

“You shall not crucify the retiree and saver on a cross of negative rates!”

The next 10 years will see an explosion of government debt and an implosion of the ability of governments to fulfill their promises. Any economic or investment model based on past performance under previous economic conditions will be worthless. As in, just as worthless as the Federal Reserve’s models. We are truly going to have to go outside of the box if we are going to figure out how to get our portfolios from where we are today to the other side of the coming crisis. There is truly no way to predict what our investment portfolios should look like six months or one year or two years or six years from now.

I see no way for Europe to avoid that crisis. The US might if we made radical decisions in 2017. You can ask yourself how likely that is. Ben Hunt, the brilliant writer of the Epsilon Theory letter, came into town Thursday night, and we spent four hours at a local watering hole talking about the current situation and what the likely outcomes are. Our views are pretty similar. He calls the current economic philosophy “magical thinking.” I see it more as religious thinking, but that may be because I went to seminary and Ben opted for a more secular academic path.

I am telling you, this is not going to end well. You cannot assume that your investment returns are going to look anything like the average for the last 20–30–40 years. I know there are those out there who will tell you that is exactly what is going to happen. Many of them are my friends, and I enjoy sitting and talking with them over a bottle of wine and a great meal. But I will look them in the eye and tell them that they’re walking into economic hell with their eyes closed. And anyone who is following them is going to see their portfolio go up in smoke.

This is going to be the most difficult investing environment of the last 100 years. Modern Portfolio Theory was created in 1952 by my friend and Nobel laureate Harry Markowitz, who argued that diversification among asset classes is the only true free lunch. I think MPT is going to become problematic.

We are still going to need to diversify, but I think we have to diversify among trading strategies that diversify among asset classes. Being long or short anything these days on a buy-and-hold basis is just plain dangerous. Maybe the investment turns out wonderfully, but I think the risk versus reward of a one-way strategy is now much higher than most people think. In my view, if you are in a standard 60/40 portfolio, you are going to have your portfolio derrière handed to you.

Then again, I could be a Cassandra. I could be wrong. The world could go along just as it has for the last 70 years, and we could pile up all the debt in the world and the markets wouldn’t care. In that case the diversified trading strategy I will propose will underperform the never-ending bull market. It will not do poorly, but it will not match an S&P that compounds at 15% forever. So I guess you have to decide how much you think the S&P can compound from where we are today, given roughly 2% annual growth in GDP.

I said I would give you a few paragraphs on what the country should do.

1) We should radically alter our tax policies. I would drop the corporate income tax to no higher than 15% and preferably 10% on total global income. But no deductions for anything. Not even oil depletion allowances. That would make us competitive with the world. If we created that corporate tax so that it looks like a business value-added tax, our corporations could deduct the tax for their products manufactured in the United States when they sent them overseas, which would give us a monster manufacturing advantage, along the lines of what Europe already has. Sorry Europe, I am being a total homeboy now.

2) To get really creative, increase that business consumption tax to the point where we can get rid of the Social Security tax for both employees and employers. Employees get an increase in pay (especially those at the lower end, reducing income inequality), and the measure is relatively neutral for businesses. Deductible at the borders for exporters. That will go a long way towards helping the income inequality situation while still providing a safety net.

3) That allows you to radically reduce the income tax, which is the most destructive of all taxes, in terms of incentive. Properly constructed, you could actually not even charge income tax for incomes below $100,000 and make it 20% above that level. No deductions for anything. Period. We can quibble about the numbers, but you get the idea.

4) Completely replace the FDA and other destructive bureaucracies that function as prison guards of the past. It’s the 21st century and we should begin to act like it. I would not argue that we don’t need drug and food, financial and banking, environmental, and a host of other types of regulatory oversight. However, oversight has become overkill. The bureaucracies have become an innovation-killing force unto themselves, forever expanding their own fiefdoms. Pare them back. Forced them to eliminate 5% to 10% of their rules every year for 4 years until they get down to the essential ones.

5) Finally, the true heresy: If we change the policies currently driving the Federal Reserve, it is highly likely that the economy will fall into a recession sooner rather than later. If we do nothing of the sort, it is also likely that we will fall into a recession. I know that recessions are part of the normal business cycle, but it is difficult to watch large numbers of people go unemployed. No president wants a recession on his or her watch.

So the only thing you can do is to hit the fiscal spending button. But in a recession we are already running up massive debt. Where to get the money without creating even more of a burden for taxpayers? As president, you sit down with the Federal Reserve and the senior lawmakers in Congress and you say, “I want you to authorize a bill allowing the Federal Reserve to issue US government-guaranteed, one-percent, forty-year infrastructure bonds to any self-funding city, county, or state project approved by a bipartisan commission with no politicians on it.

There must be serious guidelines for getting access to this inexpensive funding. No one gets to build a bridge to nowhere in their district. We know that we need at least $3 trillion and maybe closer to $4 trillion of infrastructure building just to bring up our water systems, ports, electric grid, roads and bridges, transportation systems, and so forth up to snuff. The money for infrastructure rehab is going to have to be spent sooner or later anyway, so let’s do it now in one massive 5- to 10-year program and put 3 million people work in good-paying jobs.” Yes, I know that some of the projects will be boondoggles. There are no perfect solutions, but we must rebuild if we want to see the future more evenly distributed and our children’s infrastructure needs taken care of.

The Fed can slowly sell their Ginnie Mae bonds, which the market will snap up and convert into the 1% infrastructure bonds. It will take a while to ramp up the infrastructure projects that I’m talking about. But within two years the infrastructure construction business could be booming. Congress will have to authorize that. The president will have to beat Congress over the head during his or her first 90 days in office to force this through. And Congressman on the wings of both parties will want to attach all sorts of bullshit riders to the bill. The speaker and the majority leader must not allow that to happen.

Short of this massive infusion of fiscal spending, we are going to go into an even deeper recession than we did last time, and it is going to take longer to recover. If you think your portfolio was slow to recover this time, don’t hold your breath next time. Do you want to wait another eight or nine years to get back to where you are right now? How does that play into your retirement plans? I sigh as I write this, knowing that the bulk of the American populace – and its leadership – is going to sit and do absolutely nothing. And I do not know what to do to change that. The prospect truly saddens me.

What we should do is going to be the subject of numerous letters here in the next month or so. Yes, I am getting around to it. But now it’s time to hit the send button. I truly appreciate your attention if you made it this far with me.

---------------------------------------

* This article is taken from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. It first appeared here and is used by interest.co.nz with permission.

19 Comments

Thank you for putting up the Mauldin essay.

No one wants to hear the truth. Let's just pretend it's all good.

Dear John, Yer a bit late coming to these conclusions, many here, including Ergophobia, have been pointing all this out, in a more succinct and hairy-chested fashion for years - but better late than never. Ergophobia for one wrote to Ben Bernanke in 2008 graphically warning him of the folly in his policies would produce. I guard the reply ready for the great I TOLD YOU SO.

Yr only plan: to hit the fiscal spending button... will just add fuel to the fire. There is now, no orderly way out of this mess.

Ok John. If taxes are to be altered with no deductions as you suggest why not go the whole hog and abolish all current taxes and deductions and replace them with a financial transaction tax on all Bank, Bank being widely defined, deposits to be collected by the Banks to pass them on to the Governmemt. Such a taxation system would be very transparent and mean everybody, all businesses, corporation and individuals, would be contributing to the running of a country. People say that that would produce an industry of swapping. But surely that is easy to stop. Both parties would forfeit, to the state, the item that was swapped.

Another example of the trendy bullshitartistry of the elites: "In a wide-ranging interview Mark Carney, one of the main instigators of the so-called ‘Project Fear’ campaign ahead of the UK’s European Union referendum, presented a more upbeat picture on the outlook for global trade than before the vote.". How do these prats keep their jobs?

I don't believe the glabalist likes of Carney, Tony B Liar and co have got a clue. Ordinary folk are waking up to it hence the rise of the likes of Trump and the Brexit vote.

A very good insight in the WSJ for which I only have a part (paywalled):

Les Déplorables

To repeat: “racist, sexist, homophobic, xenophobic, Islamophobic.” Those are all potent words. Or once were. The racism of the Jim Crow era was ugly, physically cruel and murderous. Today, progressives output these words as reflexively as a burp. What’s more, the left enjoys calling people Islamophobic or homophobic. It’s bullying without personal risk. Donald Trump’s appeal, in part, is that he cracks back at progressive cultural condescension in utterly crude terms. Nativists exist, and the sky is still blue. But the overwhelming majority of these people aren’t phobic about a modernizing America. They’re fed up with the relentless, moral superciliousness of Hillary, the Obamas, progressive pundits and 19-year-old campus activists.

Evangelicals at last week’s Values Voter Summit said they’d look past Mr. Trump’s personal résumé. This is the reason. It’s not about him. The moral clarity that drove the original civil-rights movement or the women’s movement has degenerated into a confused moral narcissism. One wonders if even some of the people in Mrs. Clinton’s Streisandian audience didn’t feel discomfort at the ease with which the presidential candidate slapped isms and phobias on so many people. Presidential politics has become hyper-focused on individual personalities because the media rubs them in our face nonstop. It is a mistake, though, to blame Hillary alone for that derisive remark. It’s not just her.

Hillary Clinton is the logical result of the Democratic Party’s new, progressive algorithm—a set of strict social rules that drives politics and the culture to one point of view. A Clinton victory would enable and entrench the forces her comment represents. Her supporters say it’s Donald Trump’s rhetoric that is “divisive.” Just so. But it’s rich to hear them claim that their words and politics are “inclusive.” So is the town dump. They have chopped American society into so many offendable identities that only a Yale freshman can name them all. If the Democrats lose behind Hillary Clinton, it will be in part because America’s les déplorables decided enough of this is enough.

http://www.wsj.com/articles/les-deplorables-1473895470

These are the IYI's I'm talking about, Nassim Taleb:

What we have been seeing worldwide, from India to the UK to the US, is the rebellion against the inner circle of no-skin-in-the-game policymaking “clerks” and journalists-insiders, that class of paternalistic semi-intellectual experts with some Ivy league, Oxford-Cambridge, or similar label-driven education who are telling the rest of us 1) what to do, 2) what to eat, 3) how to speak, 4) how to think… and 5) who to vote for.

The IYI pathologizes others for doing things he doesn’t understand without ever realizing it is his understanding that may be limited. He thinks people should act according to their best interests and he knows their interests, particularly if they are “red necks” or English non-crisp-vowel class who voted for Brexit. When Plebeians do something that makes sense to them, but not to him, the IYI uses the term “uneducated”. What we generally call participation in the political process, he calls by two distinct designations: “democracy” when it fits the IYI, and “populism” when the plebeians dare voting in a way that contradicts his preferences. While rich people believe in one tax dollar one vote, more humanistic ones in one man one vote, Monsanto in one lobbyist one vote, the IYI believes in one Ivy League degree one-vote, with some equivalence for foreign elite schools, and PhDs as these are needed in the club.

https://medium.com/@nntaleb/the-intellectual-yet-idiot-13211e2d0577#.o4…

Right in our back yard we are having our democratic representatives hijacked, neutered by this very class of PHD ning nongs; the so called super city. Whose idea was this particular work of evil? Rodney Hide? I suspect a quiet coup by these self serving IYI's.

http://www.nzherald.co.nz/politics/news/article.cfm?c_id=280&objectid=1…

Anyone who doubts this should take the time to attend a council meeting any day of the week. The council meets as committees of all, or nearly all, members all day, just about every day. The poor members are fed fat agendas full of long reports of nebulous, mind-numbing vacuity.

Most of their evenings must be taken up reading it all and at the meetings they wade through it all, having a desultory debate on a minor point and knowing all along there is not much to decide. Christine Fletcher has complained publicly about how little time the interminable meetings leave for her to meet constituents and attend to people's real concerns.

The mayor and council are a democratic facade, maintained for appearances while professional staff make all the real decisions. You don't have to go to a meeting to see the ignorance in which the elected members are kept, it becomes apparent every time something goes wrong.

The example that sticks in my head was the Pt Chevalier school that was going to charged for a picnic in a nearby park. This came as complete news to our elected representatives.

Doubtless, they had at some point approved a broad policy parameter that they were assured would be harmless. Probably none of them asked if the hiring of parks would apply to schools. Councillors are no longer accustomed to considering operational implications, as the "governing body" they are not supposed to.

The text book says their proper role is "governance" not "management".

It was Parliament that applied this strict separation of roles to the Super City and now is proposing to extend it to all councils.

Yes Minister

Great discussion Dave. The bureaucracy is an unseen force with it's own agenda. It seems to grow and flourish when power is centralised. The bureaucracy is then distant from the effects of their self serving policy and immune to feedback.

One simple takeout from all this - Portfolio Theory has been upended and bonds will be poison for retirees. It's been obvious for at least the last year.

It's pretty concerning. Bonds will likely be toxic and damaging for a lot of retirement funds. The capital gains have been good and hopefully those gains have been diversified. What will be concerning is once the interest rate increases gain momentum in the US, some funds will be rolling investments into bonds while the plummet in price (maybe even to their face value).

Then again shares will suffer similar losses too.

Before the GFC interest rates were too low, money was too cheap, debt was too high and asset prices were too high.

This caused the GFC. The GFC should have been the event which reset prices, and brought reform.

Instead major central banks lowered the interest rates, and debased the money (QE). They made money cheaper.

It was the worst possible outcome. Debts then got higher, and asset prices got higher. Moral hazard abounded.

Reserve bankers being human have a low interest rate bias, to try and generate growth on their watch. The path of least resistance. Any fall in the market, they are there to compensate, lessening the need to reform whether it government deficit spending, or repricing of an asset. Creative destruction has been put on hold.

All major asset classes, equities, bonds and property have been inflated with poor yields, this gives no good investment choices as well as a lot of downside risk.

Reserve bankers have painted themselves in a corner, they cannot raise interest rates as there are too many overpriced assets and big debts, because they held interest rates too low previously.

The whole world economy has become a heroin debt junkie… just some more cheap money fix, or it will hurt, even as things creep to worse.

The financial system should be built on the soundness of money, allow creative destruction, and avoid moral hazard. To have a goal of good yielding assets for pensions and savings.

A signal from these inflated assets & debt should drive interest rates higher automatically.

You Nailed it. Yet, in just about all MSM and elsewhere (certain so called economists) you will not hear or have this most basic fact highlighted. That demonstrates the real lack of credibility. To not have the ability to admit failure is the highest of arrogance

You can take a different view point on whether it is failure though.. Because the rationale behind all of this is To keep (Oil) producers producing Oil so that the economy (and food) doesn't STOP. If the Oil stops, everything stops, they know this. The only way to keep demand going and holding commodity prices up is making borrowing cheap ... it gives more time - It wont avoid a crash but the alternative is really ugly; insolvent Oil cos and STOP.

They don't have any choice. All thats left to come is massive Govt "investment" stimulus ... to create capacity which nobody needs,

this is a good article along these lines

http://www.artberman.com/oil-prices-lower-forever-hard-times-in-a-faili…

"The future for oil prices and the global economy is frightening. I don’t know what beast slouches toward Bethlehem but I am willing to bet that it does not include growth."

The essay tells a good story regarding the lemming like behaviour of the elite central banks, and their Treasury and other institutional facilitators. The NZ system is equally intellectually dishonest or self delusional. Really for at least all of English's and Wheeler's time in office it has been increasingly obvious that raising property prices to have a trickle down effect is the only monetary game in town. The NZ heroes really have been the trading businesses that have sustained themselves while every time they become competitive the exchange rate is lifted to cut yet another percentage of margin away.

Mauldin nearly gets there with some solutions. His tax changes may make some sense in the US, although in my mind are a different subject red herring. He seems by the by to be advocating increasing GST/VAT dramatically while reducing corporate and income taxes. No wonder Gingrich is one of his mates. If you do do this, it needs considerable emphasis on reducing taxes for low to middle income people, but you sense his plans are to merely reduce the top rate, but that is an aside.

Printing money to spend on infrastructure is the blindingly obvious solution that the US should have been doing so as not to have wasted the last crisis. Never mind. They need to get on with it. Mauldin himself seems guilty of some of the entrenched paradigm elitism he criticises others for. He is still wedded to the idea that the Fed must loan these trillions to the US Treasury, as though they are materially different entities. They can of course directly print and grant the money. But at his theoretical 1% it doesn't make much difference, and even then, the 1% gets repaid to the Treasury in an annual Fed dividend.

You sense that Trumponomics may be informed on this basis- none of it makes sense otherwise.

There is very little to like about Trump- his offensive and awful lowering of political rhetoric is enough reason not to vote for him.

But economically the US needs to break some paradigms; ideally Hillary could get there, but I concede is less likely to.

"normalise" It seems you blame the Fed for keeping the economy floating instead of letting it go and drown. Once drowning then rates would simply collapse as even fewer people/businesses would invest without any likelihood of a return.

"more of the same" they being economists as most dont get it. Dont think of an economy in terms of money, money is an IOU for energy, think of an economy in terms of energy and when you have less energy you have less economy. The only way to camouflage that is using money debt but that is a call on future energy when you will have less.

"A negative rates regime must be aggressively opposed by the public" so you would be happy to drive us into A 2nd Greater Depression?

"I said I would give you a few paragraphs on what the country should do. " libertarian clap trap, lets just move the deckchairs about a bit....it deserves one place, the bin............."plonk"

After the big collapse in 2008 they moved rates the wrong way. They should have put rates up not down to reflect the risk of default.. How much longer can we keep pretending we're all rich? Asset prices are only held up by low rates. What i would say to anyone is beware what you think your house is worth when you are borrowing against it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.