Today's Top 10 is a guest post from Kiwibank chief economist Jarrod Kerr.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

But there are risks to the outlook, there always are.

Here’s 10 of the biggest risks that could derail our economy. Trade wars represent the biggest threat, but make sure you are aware of risk number 10…

1. Weak income growth persists.

Since the global financial crisis (GFC) of 2008, we have all been disappointed with our income growth. Global growth has taken far longer to recover than most expected. A financial market crisis takes a lot longer to recover from. And a global financial market crisis takes even longer. The banking crisis of the 1890s was remarkably similar to the banking crisis of 2008. US unemployment spiked from 4% to 18.4% in 1894, and only returned to 4% in the early 1900s. 11 Australian banks went bust during the 1893 meltdown. It took over 10 years to recover.

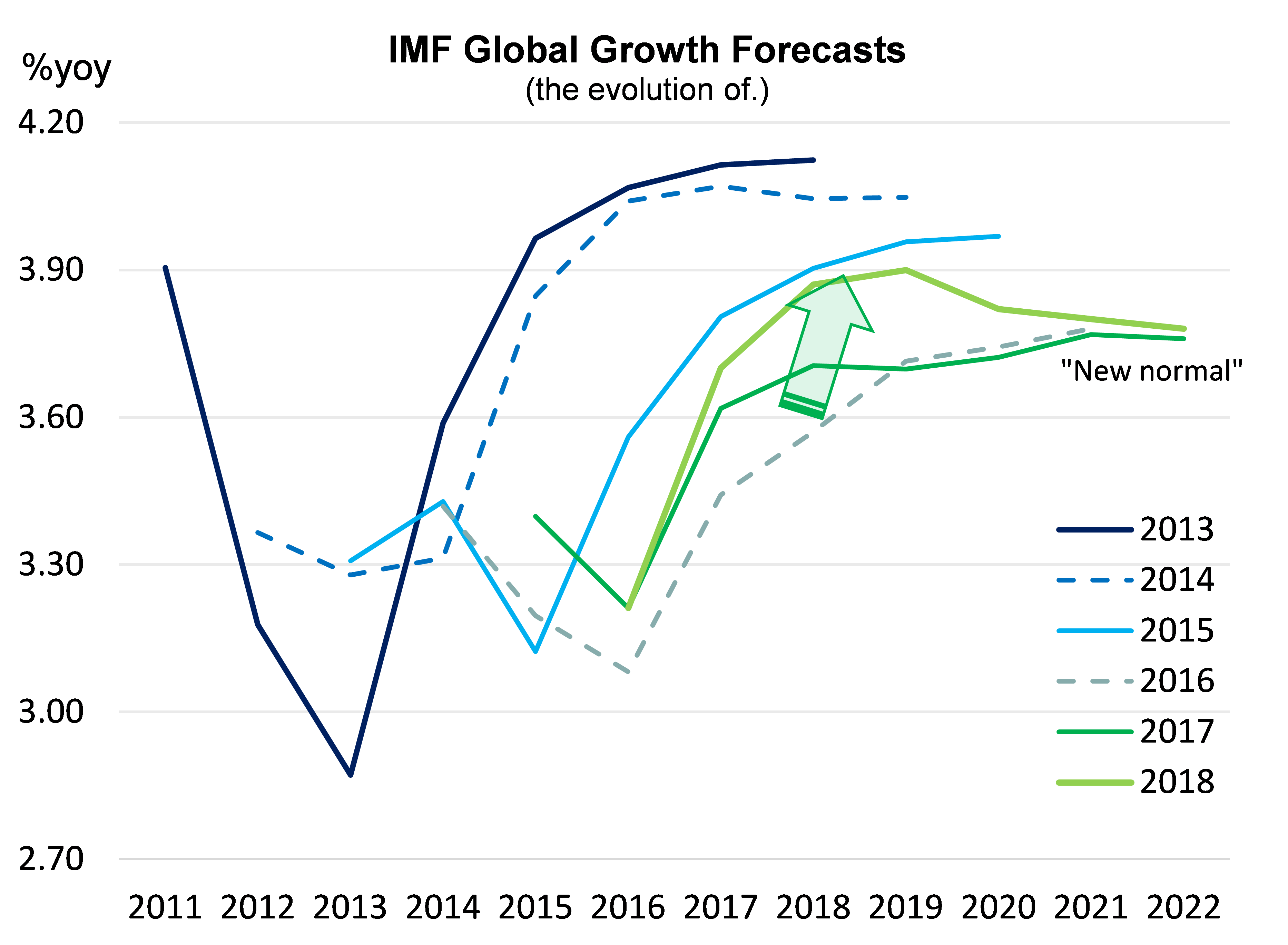

History lessons don’t help those who have had to postpone their retirements. And it certainly doesn’t help people with larger debt-to-income, as property markets outperform. Global growth is strong and spreading. Growth cures a lot of problems. The International Monetary Fund’s (IMF) forecasts are being revised higher, see our first chart. Income and wages growth is projected to lift. If not, we’re in trouble…

Weaker growth will further frustrate forecasters and businesses alike. Without a sustained lift in wages, people will become frustrated. “The system is stacked against us.” When you don’t like the machine, you rage against the machine. You become a populist.

2. The rise in populism continues.

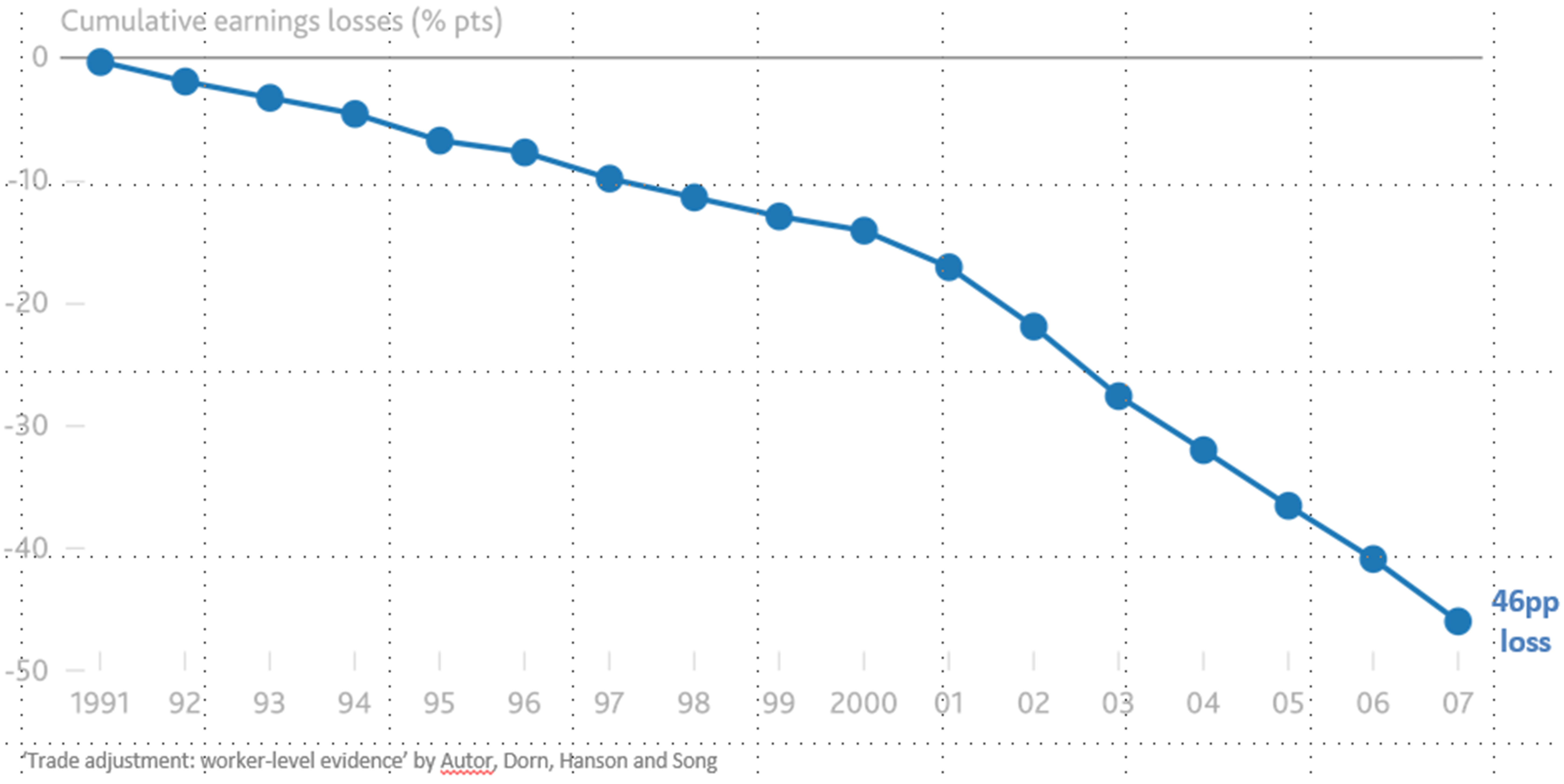

The lack of income growth over the last decade has people demanding change (Grexit, Brexit, Frexit, Nexit and Trumpit). Brexit is the most striking example. The Brexit vote can be boiled down to an anti-immigration vote. The Bank of England (BoE) produced the second chart. Incomes for those impacted by the EU’s free movement of labour have effectively halved. The Polish labourer and nanny, for example, have slashed blue collar incomes. It is great if you’re wealthy and employ these services, it is far from great if you’re employed in these sectors.

The Brits are not the only ones voting in anger. The so-called “rust-belt” in the US turned up to vote for change in Trump. Anti-EU politician Marine Le Pen also received a much larger voter base in France. When you’re angry, you vote for change (at any cost). We saw a similar rise in populism following the 1893 banking crisis, and in the 1930s. The rise of populism in the 1930s led to a trade war, and another world war. Trade wars are our biggest threat.

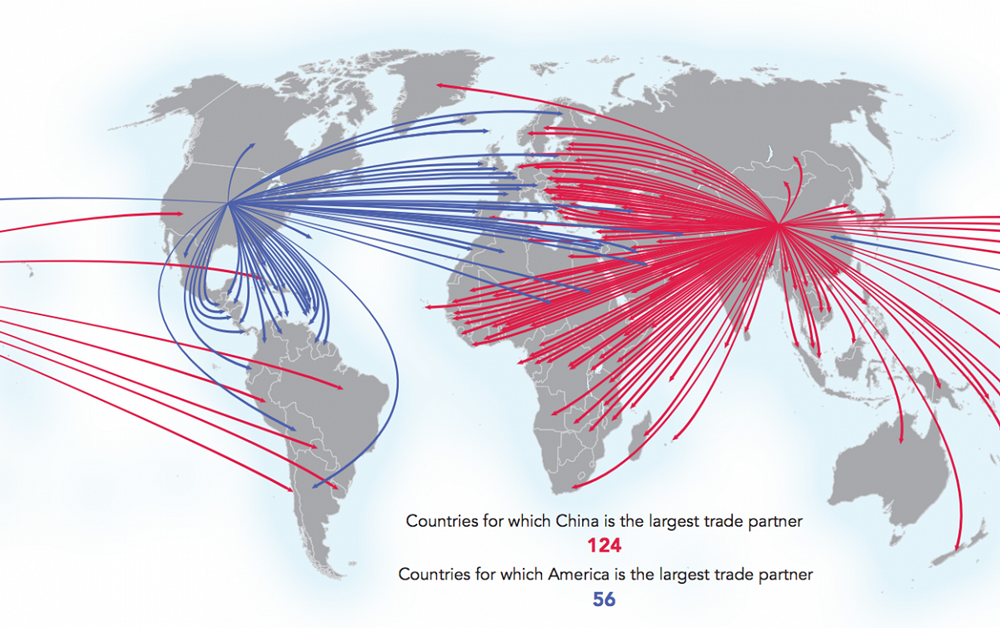

3. BuFGs enter a full blown trade war.

Our biggest fear is trade war. The two heaviest hitters, China and the US, have exchanged some ugly words. But recently, some great news has developed. China is addressing US$200bn of the US trade deficit. China makes more money out of the US in bilateral trade, hence the US deficit. But China will look to increase imports of US agriculture and energy, to better balance the books. Trump announced an immediate hold on newly imposed tariffs.

For now, the BuFGs (Big un-Friendly Giants) are playing nice in the global sandpit. Let’s face it, when they start throwing toys at each other, we all get hurt. A truce of sorts may be developing. A truce of sorts will fuel global growth. A truce of sorts will help Kiwi exports. In terms of economic allsorts, that’d be great. But the risk is clear. If the BuFGs start throwing Tonka trucks at each other, the Antipodes will be collateral damage. We are leveraged to China, and Asia, like never before. China is the world’s most dominant trading partner. We need them to do well.

4. Weaker inflation, forever…

Weak inflation has been a global problem. The soaking up of spare capacity is needed to push price pressures. But if the Amazonian, or technology, driven forces continue to hold pricing back, we may be disappointed for longer. We have growth, we now need inflation.

The RBNZ’s own work suggests we, developed nations, are intertwined, and therefore at the mercy of global inflation. The RB estimates 70% of the variance of developed market (OECD) inflation is explained by a global inflation factor. Inflation is low globally. Wage pressures are also weak globally. So we are all looking for the same answers. It’s hard for a small central bank like the RBA or RBNZ to generate inflation when global inflation is holding us back. Weak inflation, seemingly forever, would feed into our psyche and we simply wouldn’t expect pay rises anymore. The Japanese have experienced years of pay cuts. But they have a declining population, and very low migration.

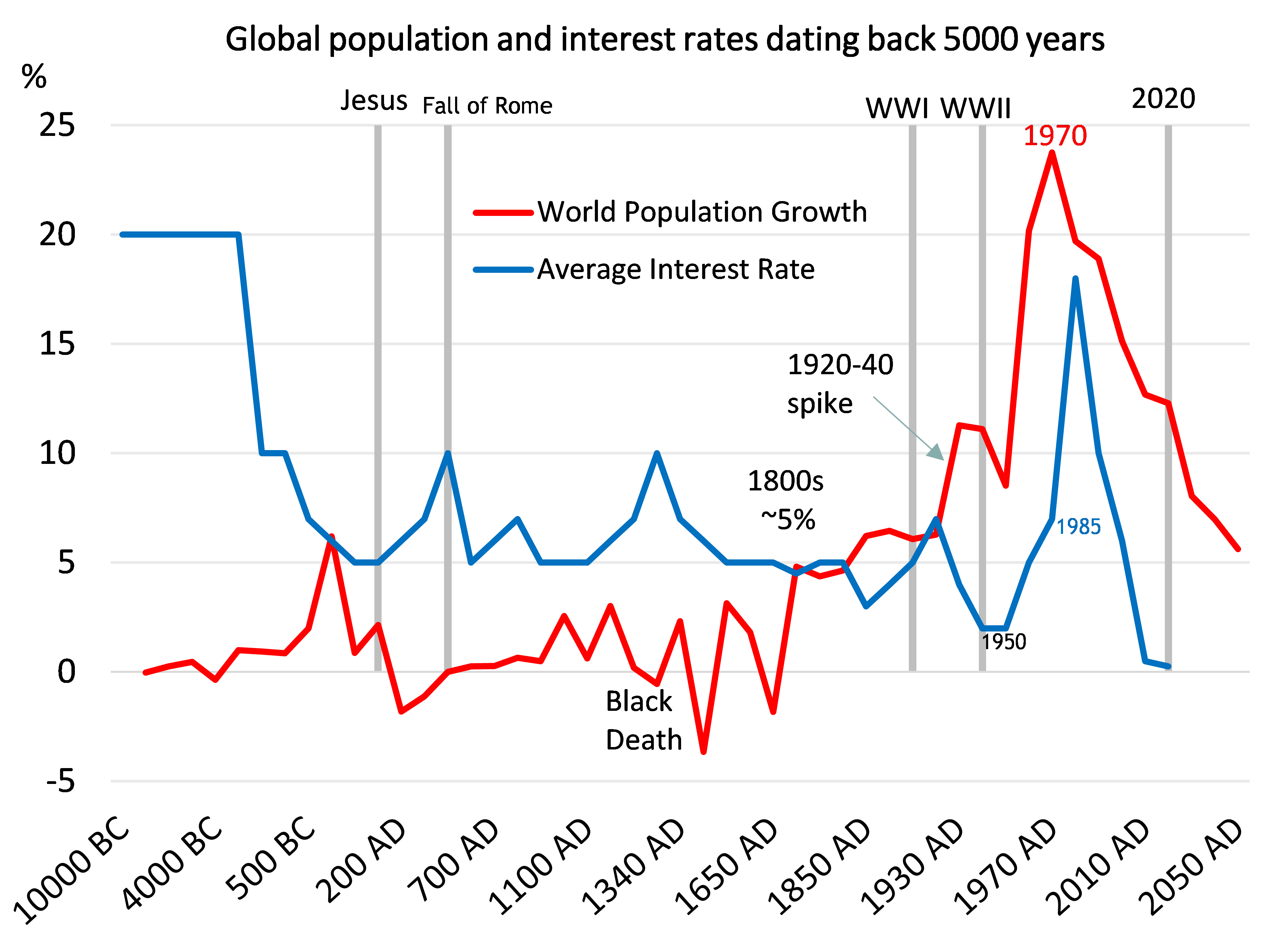

There are demographic forces at work here. The coolest chart in the history of economics shows global population growth against global interest rates, going back a bit (see below). It’s pretty clear the largest baby boom, ever, led to the largest spike in interest rates since the Egyptians leveraged up on their pyramids – great scheme that was. So the slowdown in population growth, and reversal in large parts (China’s population peaks soon), has reduced our projected “potential” growth rates. Don’t fear interest rates of the eighties, or even early naughties. But do fear fatigue. We’re not going to end up like Japan, because we import people. But we do remain at the mercy of global developments, which could be unbearably slow.

5. The return to, what? Are you kidding me!?

For the first time in a long time, central banks around the world are facing the same direction. They all want to follow the Fed. The great financial crisis led to the great financial experiment, and the advent of negative interest rates. Negative interest rates are a first in the history of mankind, and we have 5,000 years of history. Unwinding the loosest policies ever prescribed will be challenging. The US led us into the great financial crisis, so the Fed will lead us out of the great financial experiment. And the Fed has picked up the pace.

Of course it can end in tears. The last time the Fed tried to hike rates, too slowly, was under Alan Greenspan. It was the Fed’s tightening that uncovered the debacle of “highly rated”, but then highly stressed assets. We don’t really know what bubbles or poor practices have developed over the last 10 years. Equity markets have performed well. Bond markets have performed really well. And so have property markets. That was the point of QE. Print money to buy interest rate product, and drive interest rates to never before seen lows. Low rates fuel everything else.

If I won lotto tomorrow, I’d keep working just to see how this ends. Ok sure, I’d work part-time, on a superyacht. But my point stands.

Stronger-than-expected global growth and inflation may see faster unwinding of accommodative global monetary policy. But the removal of extraordinary stimulus brings extraordinary risks. We’re in the age of regulation, post crisis. And we have never seen such an extraordinary amount of money printing (QE). Quantitative Tightening (QT) is a known unknown. As monetary policy is normalised, central banks will be challenged by the possible haemorrhaging in vigorously regulated financial markets.

Increased volatility in financial markets is likely. The greater the volatility becomes, the slower stimulus will be withdrawn. It is a dynamic path, with continuous feedback. If QT leads to extreme volatility, and/or falling equity markets, QT will be postponed or stopped indefinitely. There is no pre-set course. Central banks have more control than they are given credit for. And central banks have decisively, and effectively, reduced volatility to boost confidence in the recovery. Ultimately, growth and inflation will drive the pace of QT. If QT hurts growth, QT will stop, until growth proves resilient. The risk of QT causing unforeseen volatility is one that may postpone the global recovery, but not end it.

Remember, central banks want reflation. Ex-Fed Chair Ben Bernanke put it best when he said: “One benefit of reflation would be to ease some of the intense pressure on debtors and on the financial system more generally.” Reflation, or inflation on top of solid growth, solves a lot of problems and flatters debt metrics. QT is a known unknown. And we simply don’t know how it will end.

6. An EU break up would be ugly.

For reasons stated above, tensions remain within the EU block. The EU is more than just an economic experiment, it is all about creating political harmony. Since the end of WWII, we have seen an unprecedented period of peace on the continent. The political glue has seemingly superhuman strength. But there are many, serious academics, around that see the end as simply a matter of time.

Germany benefits immensely from the Euro. Imagine what a Deutschemark (German currency) would be trading at relative to the US dollar… it would have to be double the Euro. That would send the price of all German manufactured goods through the roof. Great for the Japanese car makers I guess. But the point is Germany has the largest current account surplus on the planet. They make a lot more from us than we make out of them. And they are (arguably) not paying their share to the rest of the EU.

Without fiscal unity, the bloc has problems. Let’s put it this way, in the United States of America, they are American first. In the united states of Australia, they are Australian first. Not one New South Welshman cares that they have paid a cheque to Tasmania since Federation. The same can be said for the united provinces of God’s country. There’s been an earthquake in Christchurch, fix it. We don’t care where the money comes from. They’re Kiwis, help em out.

The problem with the EU is that they are not Europeans first. They’re French, German, Italian, and Greek first. Germany doesn’t want to write a cheque to Greece for the next hundred years, even though they should. The risk of an EU break-up is too high. An EU break up would be the very definition of madness in financial markets, and a global recession. We think the political glue is strong enough, but you never say never.

I read an interesting article that stated lawyers would take around two years to rewrite all the contracts within the EU, from simply Euros (the common currency), to all of a sudden Lira versus Francs versus Drachma etc… It sounds like a gross exaggeration, but at least currency markets would be fun again.

7. Risks to our agricultural industry.

Mycroplasma bovis is consuming headlines, as it should. Risks to our proud dairy and meat industry feed directly into risks to our general economic outlook. The government’s plan to eradicate the disease comes at a cost, around $850 million-to-$1 billion. If successful, the impact should be minimal in percentage terms, and well mitigated. Although the risk is we get a wider breakout and much worse outcome. We are only one of two nations where the disease isn’t established. And we are more efficient without it. For now it is a matter of waiting and watching.

Our dairy industry carries a lot of debt. The expected cost is around 15c per kg/MS, off a healthy Fonterra forecast of $7 per kg/MS. Some farms will struggle with the cost. Hopefully most farms will take it in their stride. Our industry is arguably the best in the world. And each challenge dealt with makes us stronger in the long run.

Other diseases and bad weather (like droughts and cyclones) are also impossible to predict, and potentially devastating for our industry. Unlike in Australia, where they can keep digging - rain, hail or shine.

8. The Panda passes out.

As mentioned above, NZ’s economy has become increasingly exposed to China over the last few decades – and Asia more broadly. China has undergone a phenomenal ascendancy in the global economic rankings, and is now NZ’s largest trading partner.

However, since the GFC significant policy stimulus by Chinese officials, to keep the wheels turning, has lifted the level of debt held by local government and corporates in the world’s second largest economy. A primary concern for NZ is if the wheels come off. For now, officials have had the resource to prop-up highly indebted and inefficient local government entities.

China has a heavy warchest of foreign assets, earned over years of chunky trade surpluses, and the “management” their currency. They have over US$1.1trn in US Treasuries, for example, that they can draw on to plug holes if and when needed. But they are not immune to a slowdown, and possible spike in local defaults. There is always the possibility that a shock to the Chinese economy, stemming from say a trade war, could trip up officials. A China slowdown will impact Asia, and an Asian slowdown is likely to hammer the demand for Kiwi goods and services exports.

9. We rely on the kindness of strangers.

One of the Achilles’ heels of Australian and New Zealand banking systems is the partial reliance on foreign funding. Developments in foreign funding markets can significantly impact the cost of banking domestically. And it is generally the cheapest source of bank funding. Regulation has forced a reduction in the reliance of foreign funding.

If funding costs blow wider, interest rates offered throughout the economy rise. The spread between the RBNZ’s cash rate and mortgage rates, for example, widen. If persistent, the current monetary policy setting becomes less accommodative. And if that occurs at a time when the economy still needs support, the RB will lower the cash rate to keep settings as they were prior to the blow out. A risk we think will dissipate near term. We will watch with interest. And we’re heading into the rugby world cup. If the All Blacks win again, foreign investors may stop buying Kiwi bank paper…

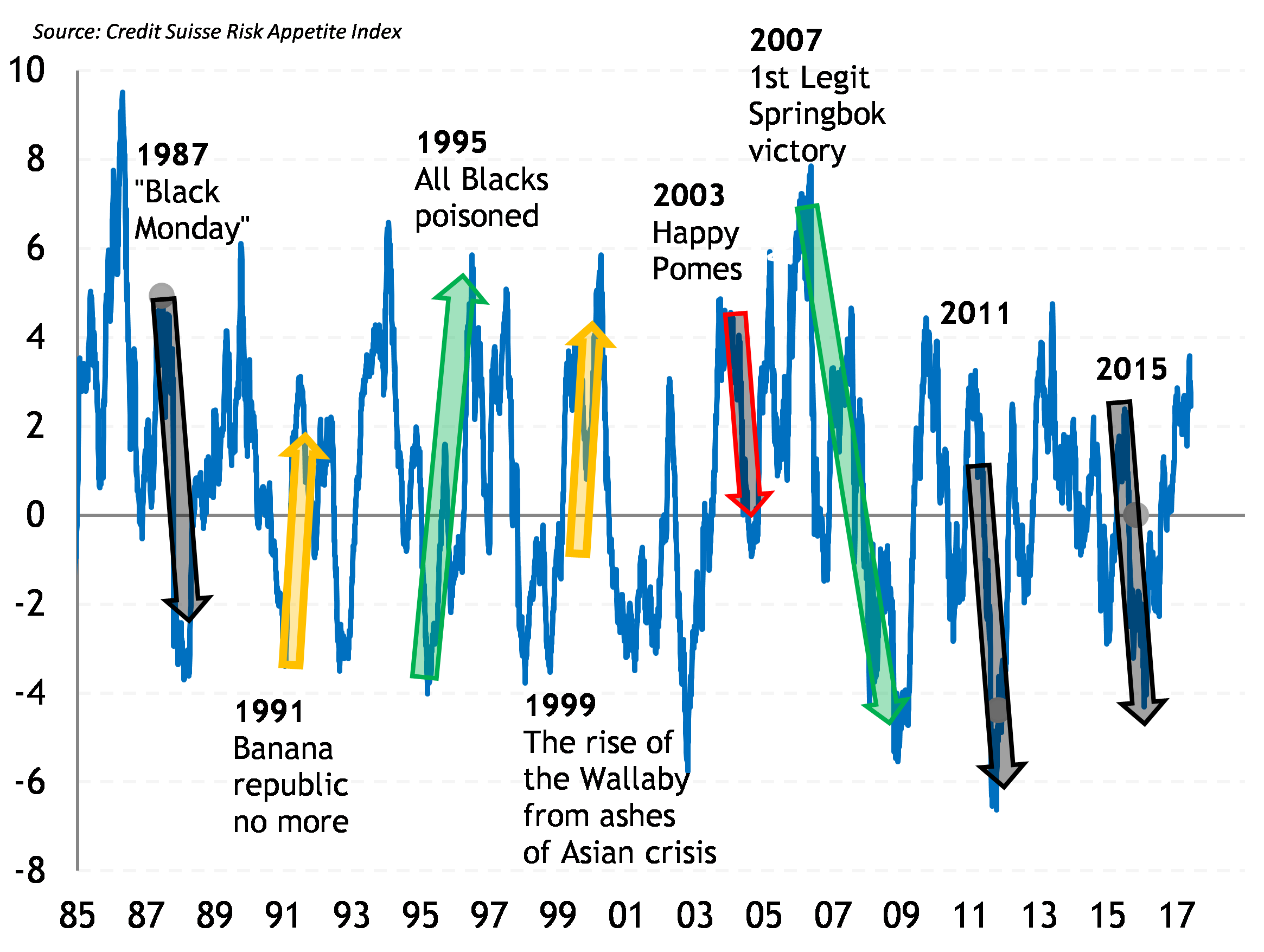

10. The risk of an All Blacks, or worse Springbok, victory.

Not many people realise the impact of the most successful sporting team the world has ever known. The rugby world cups drive financial markets, or at least we have a cool chart that shows they do. What the world needs is an All Blacks defeat. What New Zealand needs, is an All Blacks victory. It is us against them, and geez do they throw a tantrum when they lose.

Every All Blacks RWC victory has led to a tantrum in financial markets. The first RWC AB victory in 1987 led to Black Monday, initially called “All Black Monday”. The AB’s victory led to one of the most severe equity market collapses in modern times. The two victories in 2011 and 2015 were a kick in the back for financial markets hobbled by the Springbok induced 2008 global financial crisis.

The dark horses of world rugby, the Springboks, have caused much controversy and the greatest financial market crisis since the Great Depression! Firstly, in 1995, the blatant poisoning of our men in black enabled a surprise victory that caused one of the great “bull” markets of our time. They even made a movie about it, excluding what actually happened (poisoning). Typical Hollywood.

But there were larger forces at play, it was Mandela’s time. But when the Springboks actually won their first RWC in 2007, things had changed. It seems half of South Africa now lives in Auckland. My wife has 65 immediate family here. They were very vocal when they won in 2007, but surprisingly I haven’t heard much from her brother since 2011.

The world’s financial markets took the Springbok victory very badly. Offshore traders burst into tears, spat the dummy, and sold everything. And markets haven’t fully recovered since, thanks to the ABs storming run since 2011.

What the world wants, for reasons unbeknown to this humble economist, is a Wallaby win. When the sandpaper wielding underarm bowlers took over the rugby field in 1991, the world rejoiced. Risk appetite (investors’ willingness to buy more dodgy stuff) surged. The same reaction occurred following the Wallaby win in 1999, effectively ending the Asian crisis. Although the Wallabies haven’t been officially credited with ending the Asian crisis, our chart shows they clearly did…

Now I know what you’re thinking, what happened when England won. Well in order to draw a line, you need two dots to link. England has one dot. All I know is the suffering we all felt when the Poms won led to a spike in tinnitus.

I don’t know if we’ll ever find out what happens when the French win… although to be fair, they’ve been in more finals than most, and deserve a win one day. Just not in my lifetime please.

18 Comments

Fun column, thanks.

Re population and interest rates, weren't the very high interest rates driving in large part by the US's financialisation - i.e. pushing up interest rates to draw money in and create a financial industry (Wall Street) following the US's crossover from a surplus nation to a deficit nation?

Interest is first and foremost a tool of wealth extraction and redistribution. They do not create wealth, they suck a portion of that created by someone else. Interest rates simply reflect the rate at which that extraction will occur, which you might like to think of as the natural rate of interest. Hitting the peak interest rate is simply hitting the maximum possible rate of extraction.

Imagine a world where the US suddenly stopped string up all geo-political conflicts globally and handed back its printing-money privilege from private banks to government.

So, China as the new imperial power.

Low inflation and low interest rates forever then?

I guess you read what you want to read MortageBelt?

Great article, tells it like it is. Kiwibank has a good chief economist in Jarrod Kerr.

Great column.

#2. Populism. Much derided but also means folk have woken up to being shafted. Why should they put up with lower incomes in the interest of a better economy, whatever the hell that is.

#3 USA v China. That lovely diagram indicates the USA is becoming increasingly irrelevant. More so in the last few weeks as the USA shoots itself in the foot by starting a trade war. And they also went feral over Iran, leading the European leaders to turn their back on the USA, to continue the Iran agreement.

#9. Time to finance our own stuff. We have to run a surplus in New Zealand to avoid the risks, both individually and government.

Further sign of economic decline spotted in Auckland today. One of the vacant shops in High Street is being fitted out as...a $2 Shop. https://qz.com/1120552/the-retail-apocalypse-isnt-just-amazon-its-that-…

Following on behind the likes of West City mall out in Henderson, is the decline in spending power of NZ's younger generations now hitting High Street?

You boomers better get out there and spend some of those tax-free wealth gains, eh.

That's a bit sad.

As long as Unity Books stays, I'm ok though.

Further sign of economic decline spotted in Auckland today. One of the vacant shops in High Street is being fitted out as...a $2 Shop. https://qz.com/1120552/the-retail-apocalypse-isnt-just-amazon-its-that-t...

Still a long way to go. Japan's Daiso has an average price of NZD1.50 across their product portfolio. For many low-involvement products, that's incredibly cheap. Daiso is everywhere and many private label brands are competing aggressively.

#7

When will some ballsy media type ask the obvious question to Nathan Guy

"Why wasn't the massive non compliance of NAIT enforced by MPI with all the listed fines as legislated with the intro of said system. Second question should be why were the obvious NAIT fine tuning required not done"

After Guy stammers for a while he then should quietly resign. National cheer leaded dairy and the environment to destruction. Double output by 2025, clean the rivers by 2288, get rid of all pests sometime after that- indeed, what a Guy.

Yes Culpability. That great NZ Quality.

Last time I saw it, it was somewhere between the unicorns and dragons. Next to the flying pigs.

#2 ref the Bank of England chart - does MBIE have anything similar for the main jobs in their working visa category? Are chefs, bakers, bus drivers and care workers better or worse paid since new entrants became dominated by immigrants?

If so the " It is great if you’re wealthy and employ these services, it is far from great if you’re employed in these sectors. " applies to NZ too. Rational for the Nats but Labour need to watch out before their vote shrinks.

Great article. I'd like to hear more from him. Low wage inflation is a big problem bubbling to the surface, msm reporting now as the working poor. Populism could strike nz next election, watch for the far left and right sprout some characters.

Nice article.

#6 - Good on you for pointing out the foreign exchange subsidy Germany and the north-European countries get from their struggling neighbours. It is blatant exploitation, but is rarely commented on. It always makes me chuckle in disbelief when the EU is held up as a vision of what the world should become.

Just with number 9, they don’t just cut rates to offset the rise in bank funding pressures offshore. They actually have to generate a monetary policy response around 6-7 times larger with the cash rate, to offset a single 1bp rise in the finding cost

Hmm. I see the capital flows a bit differently. The reason China has a lot of US debt is it was forced to buy it to enable its current account surplus. Double entry bookkeeping. If it had not bought $1 trillion of US debt it would have sold $1 trillion less goods and the currency would have adjusted accordingly.

In the same way, if NZ had borrowed $300 billion less we would not have bought $300 billion of stuff we didn't really need and house prices would probably be more aligned with earnings. The current account deficit equals the capital account surplus, you can't spend money you don't have unless you can borrow it first.

Looking at current account surpluses and deficits at the same time as looking at their conjoined twin capital account deficits or surpluses throws a whole new light on the discussion.

Michael Pettis is the man to read.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.