By Gareth Vaughan

In this low interest rate world, how can banks justify their interest rates on floating mortgages?

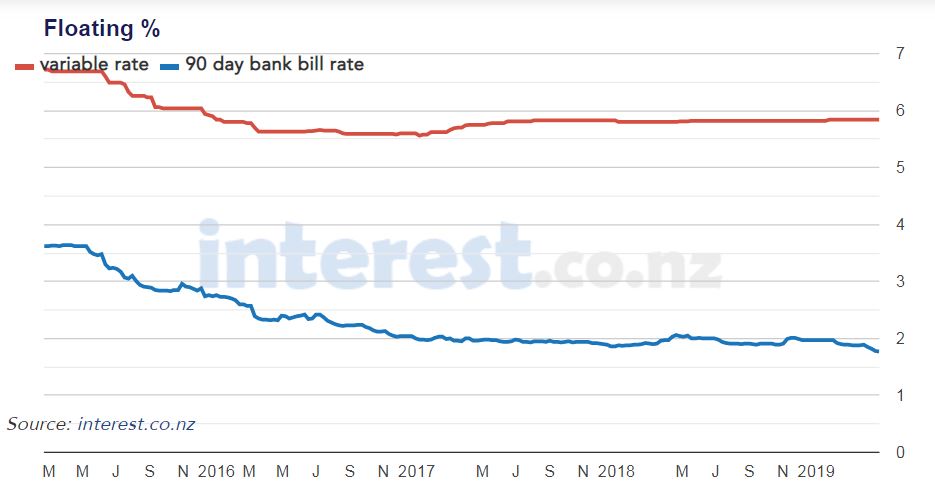

Most banks currently have their floating rates around 5.80%. This with many economists expecting the Reserve Bank to cut the Official Cash Rate at least once from its record low of 1.75% in coming months, and aggressive marketing of fixed-term mortgage rates, with all significant retail banks having at least one fixed rate below 4%.

At the time of writing the 90-day bank bill rate is at just under 1.80%, and one to five year swap rates range from the 1.68% two-year rate, to the 1.81% five-year rate. Meanwhile, the latest annual Financial Institutions Performance Survey from KPMG showed New Zealand banks' funding costs down 13 basis points to 2.69%, the lowest they've been in the 32-year history of the FIPS.

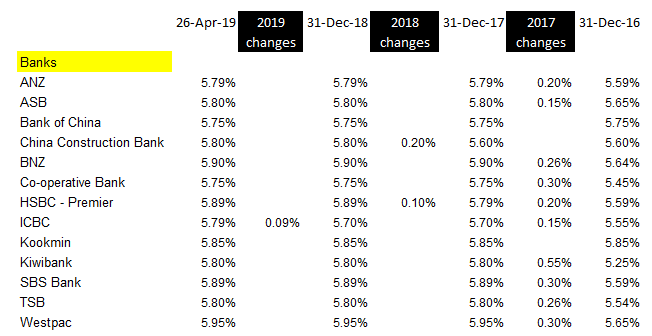

The last OCR change was a 25 basis points cut in November 2016. Yet as the table below shows, the changes to carded, or advertised, floating rates since then have been increases. Additionally, banks' revolving credit interest rates range from 5.75% to 6.75%.

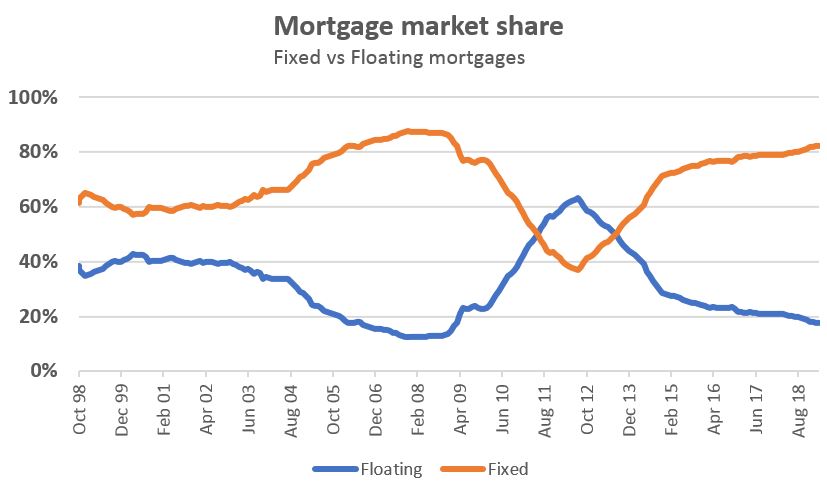

While most mortgage borrowers are currently on lower fixed-term rates, the chart below shows this hasn't always been the case, and a decent chunk of borrowers - 18% - remain on floating rates. These will include SME owners using their houses as loan security.

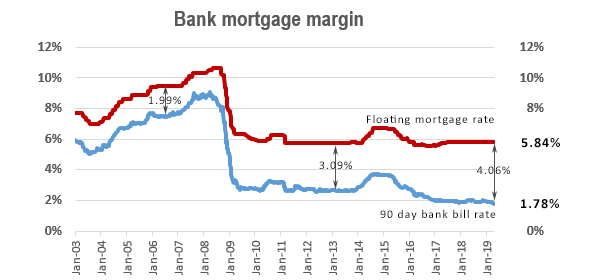

Like credit card interest rates, floating mortgage rates appear hard to justify. While banks may be battling it out in the fixed-term mortgage market, they appear to be pocketing some decent margins on floating mortgages.

See all banks' advertised, or carded, mortgage rates here.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

5 Comments

I have two floating offset mortgages, with 1% and 0.75% discounts off the posted floating rate, so 4.90% and 5.15%.

I wonder how many other people with floating rates have some discount applied.

Floating offsets are great! Gingerninja suggested to use one and so far have saved thousands of dollars on interest. Lots of fun, I'm surprised the banks let you do it. Would've thought it was even taboo, like doing bad stuff with a friend in your parents' bed.

BNZ offers 5.05, and even miserly Westpac offers at least half a percent discount. 4.9% is great going though Lanth!

Not sure that the rate is of any consequence. If you have even 20% saved up then more of the repayment reverts to principal repayments anyway.

At the end of the day, how fast you pay off depends on your savings rate.

Tldr: floating offset is a crucial tool on the pathway to early retirement.

The optimum mortgage setup is to float the amount you think you can pay off in the year and fix the remainder for 1 year, then repeat each year. This gives you the benefit of rapid payment and low rates.

I didn't think you paid off a floating offset as such. The entire amount remains available as a "overdraft" type credit, regardless of how much you pay. You will of course pay less interest the lower your balance is , so I guess that is paying it off in a way .

It seems that the banks have widened their margins on floating rates steadily since 2008. About time some pressure is applied to address this gouging.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.