Readers of our end of day updates will know that banks have settled into the habit of making small, but regular trimmings to their term deposit rate cards.

Usually they are -5 or -10 bps. But they come regularly.

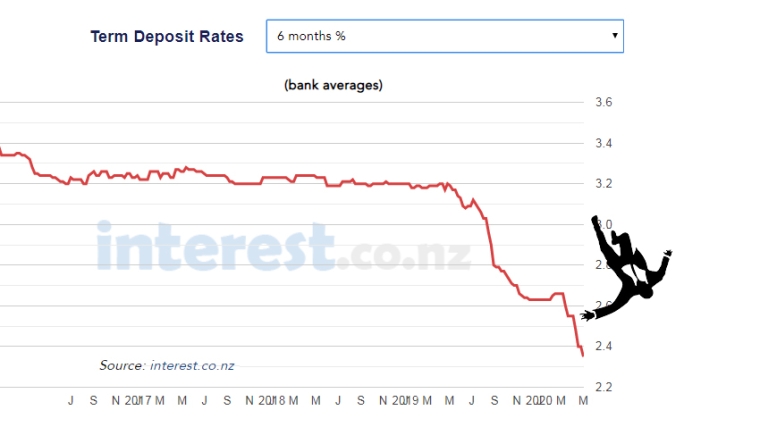

They add up. And a quick check of the chart at the base of this story shows how, on average, they have driven TD rates lower. And quickly.

At the start of this week, we have had two more such reductions, giving the trend solid momentum.

Yesterday, BNZ trimmed -5 to -15 bps from its offers of 1 month to one year.

And today, Rabobank has trimmed -5 to -15 bps for rates 1 month to 15 months.

Both banks also cut some at-call savings account rates as well.

The trend actually isn't new. It started about a year ago when the RBNZ cut its benchmark OCR rate by -25 bps, and picked up steam with the August -50 bps slash

But is has gotten new impetus as the regulator hacked off another -75 bps in March this year.

All up, that was -150 bps of rate underpinning that has been removed.

And as the chart shows, all this has flowed directly into retail term deposit rates. In the same time, 6 month term deposit rates have fallen -85 bps and the one year rate has fallen -100 bps.

It may be little comfort, but the retail banks haven't cut retail term deposit rates as hard as the Reserve Bank has cut the OCR.

Nor have they followed wholesale rates down as sharply. In the same time frame one year swap rates have fallen -167 bps - and now down to just 0.20%. And that makes wholesale money relatively cheaper than retail rates. Fortunately, bank treasurers have long memories and recall that wholesale funders became very unfriendly in the GFC. Margins became predatory. They learned that retail funding can be counted on whereas the 'smart money' can't. Since then, they have made efforts to protect their retail funding bases, encouraged by the RBNZ Core Funding regulations.

The latest headline rate offers are in this table and marking the changes so far this week.

| for a $25,000 deposit | Rating | 3/4 mths | 5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mths | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 1.80 | 2.30 | 2.30 | 2.30 | 2.30 | 2.30 | 2.30 |

| AA- | 1.80 | 2.30 | 2.45 | 2.30 | 2.25 | 2.25 | 2.25 | |

| AA- | 1.75

|

2.30

|

2.40 | 2.40 | 2.50

|

2.40 | 2.40 | |

| Kiwibank | A | 1.80 | 2.30 | 2.30 | 2.30 | 2.30 | 2.30 | |

| AA- | 1.85 | 2.30 | 2.35 | 2.40 | 2.45 | 2.40 | 2.40 | |

| Other banks | ||||||||

| Co-operative Bank | BBB | 1.40 | 2.30 | 2.40 | 2.25 | 2.30 | 2.40 | 2.45 |

| BBB | 2.25 | 2.60 | 2.65 | 2.55 | 2.50 | 2.50 | 2.50 | |

| HSBC Premier | AA- | 1.20 | 1.45 | 1.45 | 1.45 | 1.60 | 1.60 | |

| ICBC | A | 2.25 | 2.80 | 2.65 | 2.65 | 2.65 | 2.65 | 2.65 |

| A | 2.30

|

2.55

|

2.50

|

2.50

|

2.50 | 2.50 | 2.50 | |

| BBB | 2.00 | 2.40 | 2.40 | 2.45 | 2.45 | 2.50 | 2.40 | |

| A- | 2.00 | 2.40 | 2.40 | 2.45 | 2.45 | 2.50 | 2.40 |

Term deposit rates

Select chart tabs

47 Comments

Isn't it odd that as the risk of a bank defaulting rises significantly, the reward for your risk falls even further.

This is finance in reverse.

Indeed. Its like the banking model forces savers to have to do something else. The saying is safe as houses, not safe as banks...

Ponzi finance

Virtually NO Interest...

NO $$ Security Guarantee...

NO Thank You...

CASH in your Hands right now is KING!!!

Fire it off to a country that does have security guarantee (if that's an option for you).

Perth mint - can't be debased, and has a WA Govt. guarantee!

Sure, if you don't put "getting robbed at gunpoint in the middle of the night" into the risk equation.

In this modern educated age - we call that "Taxation"

This is finance in reverse.

Yes. But I think the banks know (or believe) that they can't default.

I actual look at our financial markets now like a big game of poker. Those with leveraged positions are all in and they're forcing the non-players to keep paying blinds. The house keeps adding to the pot, not realising that everyone is bluffing and nobody has a winning hand. The question will be: what happens when everyone has to show their hand? How will the pot be distributed among players? Will only those who were bluffing and kept playing be rewarded, or will those who were honest about not having a good hand, or could see the house was cheating, miss out on the addition funds put in the pot even though they were forced to continue to pay blinds?

Who is going to pay the return for lenders? borrowers. Borrowers ability to actually repay debt is impaired. So there is less demand for money. This is why cost of money is reduced to almost nil. With excess supply and shrinking demand, the reward for money must diminish too. It is true that lenders risk is increased, but rewards prospects (for borrowers) have diminished even further. So Banks do not need that much deposit, thus cut interest rates.

With depression that question you ask is not how much reward you are getting, but how much punishment you will avoid. People with cash will be punished but less than those without it who need to borrow. That is a fact.

The impact on holders of other assets is expected to be worse. But with central banks activities undermining conventional thoughts in this area, whether asset holder or cash holders will receive less punishment is yet to be determined.

I think we're now in the liquidity trap loop Believer. Pushing rates down further does nothing to stimulate the economy, it just creates more non-productive debt (i.e. the goods and services created for the additional debt, isn't enough to service that debt and it goes bad). Might be a game of hot potato to see who is left holding the debt later this year.

Thing is IO, is the cost of loans to business actually falling? I don't think it is. It may actually be going up irrespective of the cost of the money to banks, as the banks perceive (rightly or wrongly) too much risk with enterprise. I think this has been going on before COVID but has become very apparent now. To break that loop I suggest the Government needs to ensure money gets into the hands of consumers while limiting price gouging. But then a significant contraction is also needed so how do we achieve that without getting mass unemployment?

I don't think we do/can avoid mass unemployment - I think avoiding the painful experience of mass unemployment is just kicking the can down the road further, like we did in 2008.

We need a reset - clear out the unproductive/weak businesses (and debt associated to them) then start fresh. Otherwise we're going to come out of this with zombie companies and walk into the same situation in another few years....(with even more debt!)

What point is a reset if we don't rethink the ideology behind it all? The how's and why's of continually ending up where we are?

When do we consider, that maybe reducing life and living into economic values and measurements isn't conducive to the overall wellbeing of Earth and humanity?

Remind me how much support the Green party get? That will answer your proposition.

Ha yep. Live within ecological limits? That's crazy talk!

I'm not attempting to make this generational (because a certain someone will tell me to go to hell or worse...) but if you talk of such policies to certain males with a certain hair colour, you quickly get labelled as a communist! No wonder the Greens don't get much support. And no wonder we cant change policies easily giving the voting sway of said individuals. Its old school demographics...

So what Meh proposes above isn't going to fly here for probably another 10-15 years until that demographic is dribbling into their pj's at the Summerset Village.

"Baby boomers are six times more likely to dismiss climate change than members of Gen Z, and twice as likely to vote, an in-depth survey has found."

Afraid it is generational

Solution is to get out the vote.

https://i.stuff.co.nz/environment/climate-news/300003806/six-new-zealan…

Ok great to see there are stats to back up my experiences.

' Women were less likely than men to be Dismissive, and more likely to be Alarmed or Concerned. That means the Dismissive are over-represented in the older male demographic that is most likely to be running company boards, says Winton.

They are also more focussed than the Alarmed at influencing power. “The Dismissive segment is really engaged,” says Winton. “They are writing letters to politicians. We actively engaged with a few of these people and they were really good about sitting down and talking to us about where they were.” '

Yep.

The ol Male pale stale have not done the world any favours indeed.

But they have Smalltown! That segment have influenced a lot of positive change in their time so its not all bad. There are a number that I highly respect and like to learn from. Like any part of society there is an element to it that is likely making things worse for the future, but I'm sure that is true for all parts of society/demographics.

Meh is right IO, the ideology behind the current economic system has to change. But your point is taken, how do we get that change without being too radical? The ideology currently is about a few, elites, getting wealthier and more powerful. Hence we have a situation where 1% of the worlds population own or control 99% of the wealth. That must change, but the individual self-serving attitudes of the politicians makes them susceptible to lobbying from cashed up interest groups. Changing voting habits is a longer term way to address this but how?

I look to the end of serfdom and say the French Revolution. When enough people realise the likes of the government and central banks are actually working against them and not for them, then change will come. I think people are starting to wake up to that now. Current asset owners are the lords (say multiple property owners) and those left renting are the serfs. The serfs may decide they no longer want to be part of the system and revolt.

Even Ray Dalio, one of the richest guys out there who has used the capitalist system to his own benefit, thinks it is broken and that if not managed well, risks war or other violent action if the 'pie' as he puts it, doesn't get distributed more evenly.

That's the conundrum isn't it. Cash is guaranteed returnless risk, everything else may or may not be even worse. Consider Bitcoin. I'm in the camp that thinks in the long run Bitcoin goes to zero, and don't own any at the moment... but over the next 5 years? Is the risk of Bitcoin taking an 80% haircut in the next 5 years higher or lower than the same thing happening to any random NZ bank deposit?

Where do you even start with trying to come up with risk/return estimates to compare? Cash is essentially a speculative investment as well, with a massive skew to the downside.

As a rational actor, it's not much of a stretch to see an equation where *even if you think Bitcoin is intrinsically worthless*, it makes more sense to park your money there than in an NZ bank. (I'm using Bitcoin as my example but substitute in whatever you want, gold, Amazon stock, toilet paper - anything that has upside and doesn't have OBR risk). Strange times.

It costs about 3.5k in electricity to mine 1 btc currently. Bitcoin is therefore intrinsically valuable.

And everyone knows markets are about confidence. And the market cap of btc is confidence ++

Due to the calorific content of faeces, when converted into briquette form they're said to contain the same energy content, pound for pound, as coal. It takes 1 pound of coal to generate 1 kWh of electricity. When converted to metric, at $0.20 per kWh, it'll take approx 8000 kg of faecal briquettes to mine 1 btc. I agree, therefore, with your assertion that Bitcoin is intrinsically valuable.

I'm crying laughing

Where do I invest? Is the domain name faecalcoin.com taken?

Oh I didn't realise bitcoin had intrinsic value. How do I liberate the 3.5K worth of inflation adjusted electricity from the bitcoin?

The economy is dying, there are few options. If CPI is -5% then your deposit is still positive. Thats where I think we are heading.

You get the feeling we're only just starting to scratch the surface as well Andrew in terms of how bad this could get. The news of large businesses closing each day in the news is bad, but its when those people who have lost their jobs stop spending and can't pay their obligations, which will become visible over the next few months. The cycle could keep building momentum and I'm not sure right now what can be done to stop it. Government can only pay wages and give loans for so long before that load becomes to heavy for those left paying tax.

just out from Snider

https://www.youtube.com/watch?v=mA689dioNhA

Will take a look tonight Andrew - thanks.

Quickly went through the comments section and it looks like most people want to riot against the Fed. Scary times in America and the rest of the world...(*but they have a lot of guns in America...)

I can't help but feel the phrase 'locked-in' is the most appropriate.

So much suffering ahead, which will lead to anger.

No one will believe it till they see it. So here goes

Dear member,

NZ Winegrowers is acutely aware that Covid-19 is causing financial difficulty and uncertainty for many members. It is against that background that our draft budget and plan for the next year is being developed.

Drawing down on our reserves as the ‘rainy day’ has arrived for many of our members

In addition the Board has already agreed the following initiatives:

A 20% reduction in the honorarium paid to Directors.

A reduction in hours and salaries for 14 staff members of between 20% and 50%, and a moratorium on staff replacement and maternity cover.

Any idea how many people that might impact Andrew?

No I don't know ,they are saying 14, It's typical of what I'm being told across the industry. Not just the Wine industry all industries. I had a rep in today and he's worried about his job. We are going to fall down a bloody big hole.

As of right now wine is a boom, sales well over doubled in the last six weeks. Hell I've been buying 2 or 3 boxes a week. In time the reverse may happen as the wallets shrink.

But I do know I'll be buying a lot from vintage 2020 in 3-4 years, it's looking like beginning the best in memory for Pinot Noir.

Booze sells and now we're all alcoholics....

I agree. But that implies banks start popping no? In which case you're left with extremely low upside and some unknown probability of huge downside.

Everyone's losing interest. I think you're right, it could get ugly.

Buy Bitcoin. Currently at 8.5k USD. Was as low as 3.5k, but unlikely to go back there. No government interference. Only the market can regulate it. Pure capitalist tool. If you think NZD might go below 40c to USD, then well worth a look.

We are not that easily fooled , most of us have noted the daily steady decline , its always reported daily on this site on the end-of -day neews summary before we go home .

Very soon the money will be worthless from a yield perspective , and at that point it will be more dangerous to leave your money in the bank than in cash under the mattress.

Until stagflation sets in perhaps.

No need to attract foreign investments while the reserve bank is printing. Rates will continue to drop and money flows will leave the country.

A new idea to avoid the miss-management of funds.

Direct loans from Savers to fund new one Man businesses and take out the MiddleMan and their cronies.

I think they were called Banks, but really they should be called Fraudsters as they played us all for suckers...and they really sucked.

It would be interesting to see how long banks take to react to lower OCR when it comes to both mortgages and term deposits as well as the actual increase or reduction after the change in each case. It would tell a lot about each bank policies and ethics.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.