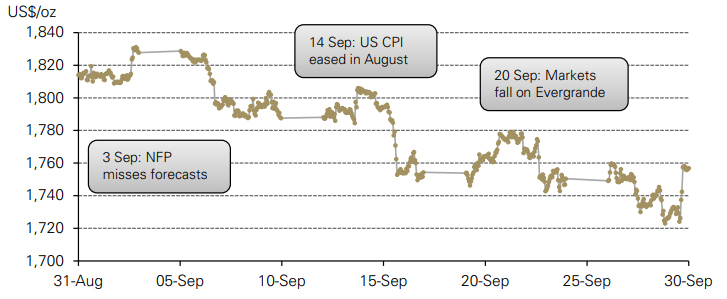

Hourly spot gold price*

This content is sourced from the World Gold Council.

Key highlights:

Looking Forward:

Investor questions:

Concerns over stagflation seem to be rising, so how might gold perform in such an environment?

With the possibility of real rates rising sooner than some expected, how could this affect gold?

Gold fell in September amid general weakness in financial assets

Gold fell in September by 4% to around US$1,743/oz.1 This was the second consecutive month of declines, with gold now over 8% lower y-t-d. Gold wasn’t alone however. Treasuries, corporates, US- and non-US equities all fell in September possibly as a result of deleveraging. The Q2 level of margin debt for equities was at a record high. It would be understandable if some leverage has been removed as we head into the historically volatile month of October. And, in our view, it’s quite possible that this deleveraging has affected most assets (energy and industrial metals excepted).

Chart 1: Gold failed to generate momentum in September

Hourly spot gold price*

*Data to 30 September 2021.

Source: Bloomberg, World Gold Council

Gold’s performance in September was marked by three sharp price reactions (Chart 1):

A general apathy towards gold was also reflected in the futures market. Sentiment towards gold – via net long positioning on COMEX – dropped as the month progressed. Global gold ETFs registered another month of outflows in September, although less than in the previous month (Table 1).

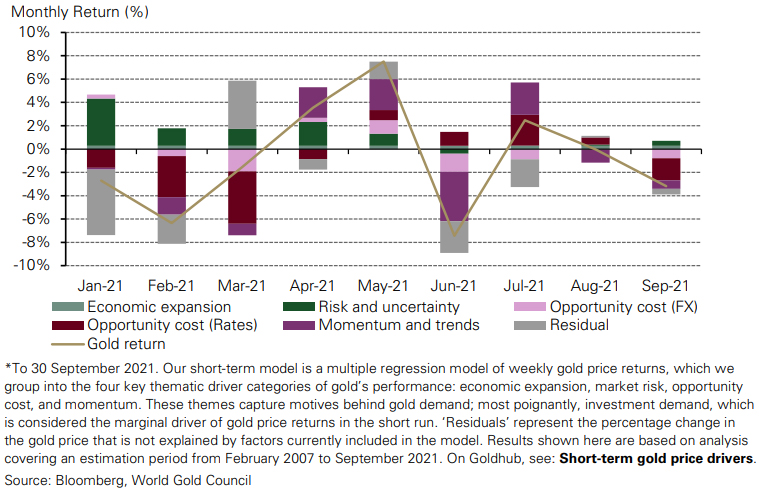

Our short-term model suggests that movement in the US 10-year yield – captured by ‘opportunity cost’ – was a major driver in gold’s weakness (Chart 2). However, , gold’s reaction was relatively muted when yields rose almost 25 basis points in the last week of the month. Futures positioning was also weaker during September along with negative ETF flows, both included in the ‘momentum’ category, but the net contribution to gold’s negative performance was moderate. Equally, dollar strength, as given by a rise in the broad US dollar index, increased the opportunity cost of gold, but its effect was comparatively smaller.

Chart 2: Quarter-to-date high interest rates, ETF outflows, and a stronger dollar drove gold prices lower in September

Contributions of gold price drivers to periodic gold returns*

Looking ahead: shifting policy environment may challenge gold

Following months of speculation, the US Fed finally signalled that it was almost ready to begin tapering asset purchases – perhaps as soon as November. This hawkish turn comes as concerns grow that inflation may be far less transitory than initially expected. The imminent reduction in asset purchases, and likely subsequent interest rate hikes, will almost certainly be a headwind for gold. But other factors are worth considering.

Other regions continue to receive central bank support. The European Central Bank and Bank of Japan, for example, both maintain an accommodative approach, which should benefit gold in those regions. What’s more, as inflation runs hot – in the US and Europe especially – gold’s historical performance as a hedge against a reduction in purchasing power could come into focus.

Gold’s performance will likely remain choppy as the markets continue to assess the potential impact of economic indicators on central bank policy. The need for portfolio protection and diversification is ever present, but the more optimistic economic outlook could weigh on gold investment and sentiment.

Regional insights

China: Early data for September paints a moderately positive picture for gold demand. With the peak season for gold consumption approaching,2 physical demand has shown signs of improving: average daily trading volumes were 32% higher than in August. This helped keep the Shanghai-London gold price premium healthy at US$7.5/oz, 29% higher m-o-m. And as stock market volatility increased, local gold ETFs saw inflows.

The latest data from China Customs shows 77t of gold was imported in August, 16% higher m-o-m. Imports were boosted by higher demand ahead of the seasonally-strong Q4 period and a rising local premium.

You can read more about the Chinese gold demand in September later this month on the Goldhub blog.

India: Gold demand remained firm in September, having strengthened in August. It was supported by wedding-related purchases and the release of pent-up demand following lower local gold prices. The local price remained at a small premium of US$1–2/oz over the first half of the month. But retail demand slightly softened with the onset of Pitru Paksha3 from 20 September – considered an inauspicious period for gold purchases – and resulted in the local premium finishing the month flat.

You can read more about the Indian gold demand in September later this month on the Goldhub blog.

Central banks: Initial data shows central banks bought a net 28.4t in August. Interest was limited to a small group of familiar names, with recent buyers India (12.9t), Uzbekistan (8.7t), Kazakhstan (5.3t), and Turkey (2.8t) all adding to their gold reserves during the month.

You can read more about the central bank demand in August on the Goldhub blog.

ETF Commentary

Gold ETFs saw net outflows of 15.2t (-US$830mn) in September, reflecting the headwinds gold faced during the month (Table 1). Outflows in Europe and North America were only partially offset by inflows into Asia. At the end of the month, global holdings stood at 3,592t (US$202bn)4 – the lowest tonnage level since April.5 Read our full September gold ETF flow commentary on Goldhub.

Table 1: Regional changes in gold-backed ETF holdings*

| AUM (US$bn) | Holdings (tonnes) | Change tonnes | Flows (US$mn) | Flows (% AUM) | |

|---|---|---|---|---|---|

| North America | 102.4 | 1,827.4 | -6.6 | -348.6 | -0.3% |

| Europe | 87.9 | 1,568.7 | -11.5 | -640.0 | -0.7% |

| Asia | 7.8 | 135.2 | 2.4 | 134.6 | 1.7% |

| Other | 3.4 | 60.6 | 0.4 | 24.5 | 0.7% |

| Total | 201.5 | 3,591.9 | -15.2 | -829.5 | -0.4% |

*To end September 2021.

On Goldhub, see: Gold-backed ETF flows.

Source: Bloomberg, Company Filings, ICE Benchmark Administration, World Gold Council

Most-asked investor questions

Here are our thoughts on the key questions we have received from investors during the past month:

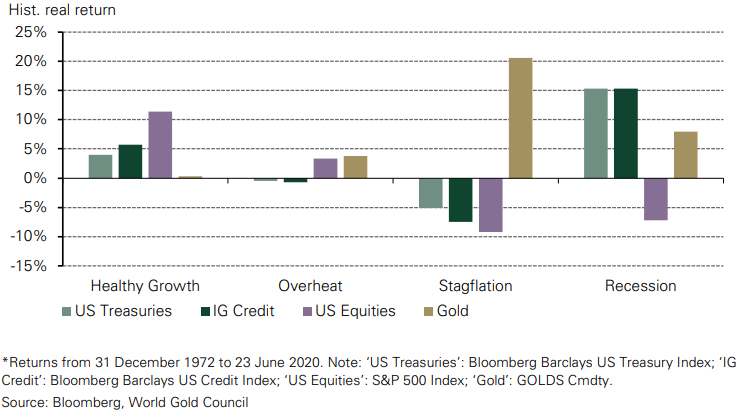

Concerns over stagflation seem to be rising, so how might gold perform in such an environment?

According to some recent indicators, the H1 economic recovery could be slowing. Meanwhile, inflation remains elevated. Some argue this phase will be short-lived, but nonetheless it could be damaging to investors if future cash flows of financial assets are impacted by the double-whammy of low growth and higher inflation.

Historical analysis finds that defensive assets are the best performers in a stagflationary environment, where the opportunity cost for non-yielding assets is lowered. Gold has seen good returns in these periods, boosted by an elevated risk environment, equity market weakness, low real interest rates and a weaker US dollar.

You can read more on this in our upcoming report on stagflation, to be published later this month.

Chart 3: Gold performed better during periods of stagflation*

With the possibility of real rates rising sooner than some expected, how could this affect gold?

It’s intuitive that gold should perform well in negative interest rate environments, given the opportunity cost of holding a non-yielding asset. This means that higher real rates should lead to lower gold prices. But our analysis shows that US real rates would need to rise above 2.5% for there to be a significant long-term negative impact on gold (Table 2). A return to a real rate environment of 0–2.5%, meanwhile, tends only to result in slightly lower real returns on gold compared to its 6.2% long-term average.6

Table 2: Gold has outperformed its long-term average in moderate real- and nominal-rate environments

| Interest rate environment | Annualised nominal gold return | Annualised real gold return |

|---|---|---|

| Absolute real rate level | ||

| All | 8.0% | 3.9% |

| Negative | 18.7% | 10.8% |

| Moderate | 9.5% | 6.2% |

| High | 2.7% | -0.6% |

| Rate direction | ||

| Falling | 7.1% | 4.5% |

| On Hold | 10.5% | 6.8% |

| Rising | 5.1% | -1.3% |

*31 January 1970 to 31 August 2021. Interest rate environments classified by US 10-year interest rate yield.

Source: Bloomberg, World Gold Council

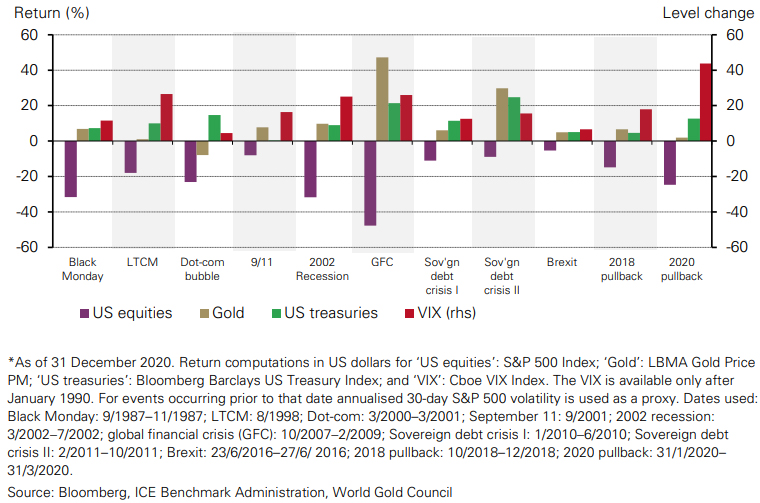

How can gold help if we see an equity market correction?

The rally in equities since the pandemic erupted in March 2020 has been very impressive. But there are concerns that valuations have reached levels far beyond what the underlying economic fundamentals would suggest. And a more pessimistic view of global growth underlines the risk of a sharp correction.

The need for diversification is therefore hugely important. However, many assets become more correlated in times of heightened uncertainty meaning not all diversifiers protect portfolios when they need it most. Gold, on the other hand, behaves differently. Its negative correlation to risk assets increases when they sell off. What’s more, gold can also exhibit a positive correlation to risk assets when they are rising.

Chart 4: The gold price tends to increase in periods of systemic risk

US equities, treasuries, and gold versus the VIX index*

Gold market monitor

Table 3: Gold return in key currencies during 2021*

| USD | EUR | JPY | GBP | CAD | CHF | INR | RMB | TRY | RUB | ZAR | AUD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (oz) | (oz) | (g) | (oz) | (oz) | (oz) | (10g) | (g) | (oz) | (g) | (g) | (oz) | |

| July | 3.6% | 3.6% | 2.4% | 2.9% | 4.4% | 1.5% | 3.7% | 3.5% | 0.4% | 3.7% | 6.1% | 5.8% |

| August | -0.6% | -0.1% | -0.5% | 0.4% | 0.6% | 0.5% | -2.5% | -0.5% | -1.9% | -0.5% | -1.7% | 0.0% |

| September | -4.0% | -2.2% | -2.5% | -2.0% | -3.7% | -2.2% | -2.4% | -4.0% | 2.6% | -4.6% | -0.1% | -2.8% |

| YTD | -7.7% | -2.5% | -0.2% | -6.4% | -8.2% | -2.6% | -6.2% | -8.8% | 10.4% | -9.1% | -5.4% | -1.4% |

*As of 30 September 2021. Based on the LBMA Gold Price PM in: US dollar (USD), euro (EUR), Japanese yen (JPY), pound sterling (GBP), Canadian dollar (CAD), Swiss franc (CHF), Indian rupee (INR), Chinese yuan (RMB), Turkish lira (TRY), Russian rouble (RUB), South African rand (ZAR), and Australian dollar (AUD).

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

Download Gold Market Commentary, full report

Footnotes

1Based on the LBMA Gold Price PM as of 30 September 2021.

2A higher levels of weddings and the long National Day Holiday – a major shopping event - occur in October

3Pitru-Paksha is a 16-day period in Hindu calendar where Hindus pay homage to their ancestors.

4We regularly review the global gold-backed ETF universe and adjust the list of funds and holdings based on newly available data and information.

5Based on the LBMA Gold Price PM as of 30 September 2021.

6Based on the US 10-year Treasury Inflation-Protected Securities (TIPS) yield.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe, log in or Register, and sign up in your Account page. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Nice write up, Thanks!

Bitcoin flows compared to gold, it has just stayed flat

https://twitter.com/Bloqport/status/1446193298314571777?s=20

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.