The cost of living for the average household increased by 7.2% in the 12 months to June 2023, according to new figures from Stats NZ.

These figures are as measured by Stats NZ's quarterly household living-costs price indexes (HLPIs).

The principal difference between these figures and the Consumers Price Index (CPI), which showed annual inflation running at 6.0% for the year to June, is in the treatment of housing.

The CPI measures the costs of building houses (these were up 7.8% over the 12 months) - while the HLPIs measure mortgage interest rate costs, (which showed a 28.8% rise over the year).

The latest HLPIs figure, while higher than the inflation figure as measure by the CPI has still moderated somewhat, down from 7.7% as of the March quarter and from a peak of 8.2% as of the December quarter 2022.

Food prices have been a major contributor to the latest figure.

"Food prices increased by 12.7% for the average household," Stats NZ's consumer prices manager James Mitchell said.

"This was the main contributor to higher living costs for most household groups."

(Stats NZ says The HLPIs measure how inflation affects 13 different household groups, plus an all-households group, also referred to as the average household. The consumers price index (CPI) measures how inflation affects New Zealand as a whole).

"Higher prices for interest payments and grocery food were the biggest contributors to the 7.2% increase," Mitchell said.

"These were partly offset by lower prices for private transport supplies and services, things that keep your vehicle running, such as petrol and diesel."

On July 1, 2023, half-price public transport fares, the cut in fuel excise duty of 25 cents a litre, and the cut in road user charges were removed. Any impact this will have on prices will come through in the September 2023 quarter.

Between June 2022 and June 2023 prices in order of their contribution to the overall movement for:

- interest payments increased 28.8%

- grocery food increased 13.2 %

- private transport supplies and services decreased 9.9%

- rent increased 4.8%

- fruit and vegetables increased 21.2%.

Stats NZ says its two measures of inflation are typically used for different purposes. A key use of the CPI is monetary policy, while the HLPIs is to provide insight into the cost of living for different household groups.

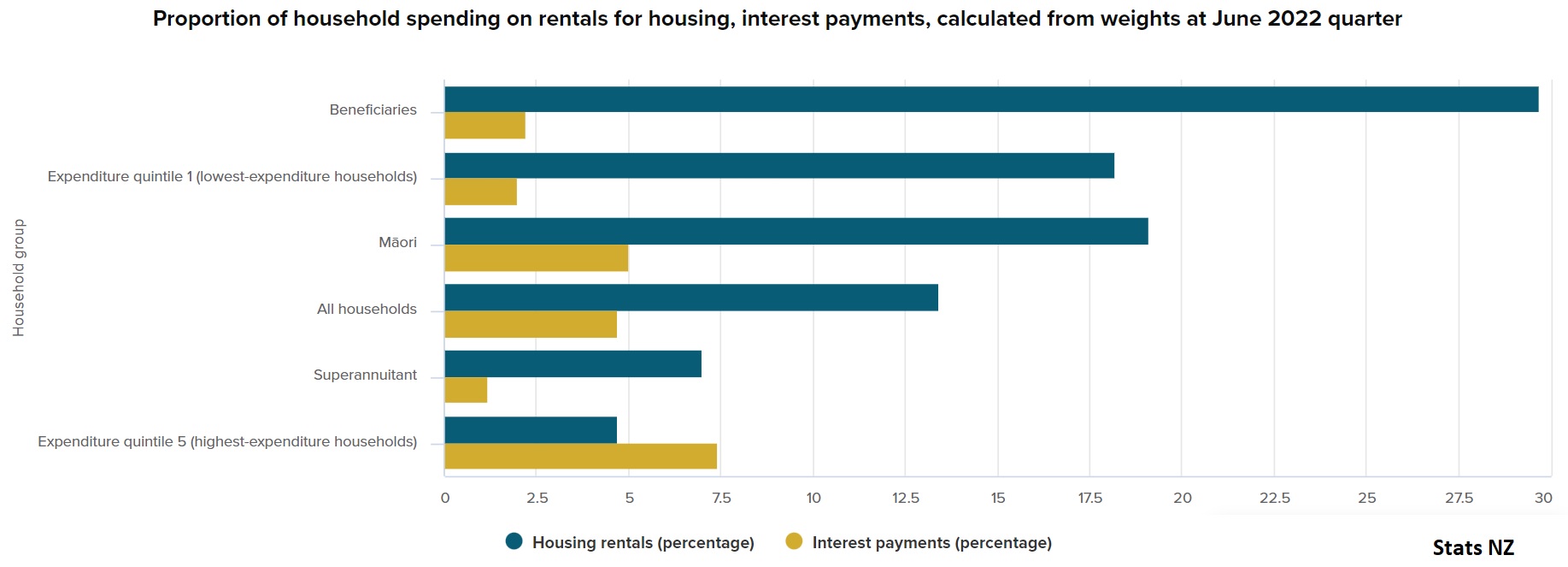

A look at the quarterly breakdown of spending on rent and interest costs shows that beneficiaries (29.7%) spent the biggest proportion of their household spending on rent, while the highest-expenditure households spent the biggest portion of household spending on interest costs (7.4%).

In terms of 'all households' the spending on rent was 13.4% of household spending, while for interest costs it was 4.7%.

61 Comments

I'd love to know what that figure is for people who a) actually have mortgages and, as a subset, b) relatively recent mortgages (which in theory would be larger and also capture a huge chunk of FHBs).

Until this changes, there is going to be continued pressure on wage increases - and this will feed into business labour costs, which is going to feed through to increasing consumer prices (either that or the businesses shrink/or fail).

It is quite the conundrum because it would appear the only way out of this is to destroy more demand from the economy - which may require even higher interest rates (as this is the only tool the RBNZ currently have), and this will just create even more of the above mentioned problem.

Until of course enough businesses fail and we reduce the demand of the typical consumer by reducing their wage and consumption demands.

Who would have thought that such expansive fiscal and monetary policy in 2020 could cause such a headache?

We probably have a decade ahead of us of the RBNZ etc trying to engineer, and maintain, the fabled Soft Landing. That's attempted by all of your above comment and trying to hold current overinflated asset price steady as all other components catch up. e.g. the price of a home falls from 7 to 6 to 4 time household income etc. But what are the chances of that in an economy beset by political advantage? Virtually none. So interrupting the Soft Landing will be periods of escaped Inflation and, yes, interest rate rises charging up behind them until prices are again reigned in.

Are interest rates going to fall? No. And after each chase, to catch threatening asset price rises, they will stabilise at a higher level each time. The ideal would be not to let prices escape at all, and keep rates slightly 'overtightened' at current affordable levels. But that's hard to see happening.

I think we have such an infrastructure and service deficit here now, that any pull back in 'discretionary' consumer spending is going to be gobbled up, and then some, but central and local government.

Looks about right. And in an economy as tiny as ours, there's only so much Debt that can be assumed at the gross national level before the cost of new borrowing takes off. And retail rates will be out in front of those.

Our productive capacity is fairly limited and low-skilled mass migration is actually making things worse adding more to aggregate demand than economic supply. Our current account deficit is only doomed to grow or stagnate at unsustainable levels until foreign money markets force a correction upon us.

“low-skilled mass migration”…. It seems you go by what you read in comments and potentially don't understand what it takes to migrate or what real shortages there are.

And no, I'm not referring to short term seasonal work. Engineers, doctors, nurses, teachers, business analyst… the list goes on.

The thrust of advisors beef with migration is super high skilled, high earning migrants are in the minority.

The rest arent adding value, other than providing the likes of advisor a range of affordable goods and services, to free him up to dedicate more time to highly productive pursuits. Like complaining about migration.

Of the current 143,000 people in the country on work visas, only 12,000 of them are Essential Skills visas. What are the rest doing?

True.

There are hidden costs of falling behind on new infrastructure, which only increase as the deficit grows. For one, an infrastructure deficit will put more pressure on existing assets and erodes its condition, leading to higher maintenance costs.

We're in a paradox where we lack the skills, discipline and funding to build large infrastructure projects, especially since these cannot be delivered within the 3-year election cycle.

Meanwhile, politicians don't feel excited about smaller or unsexy projects (3-waters, fixing potholes, putting up dividers on highways, etc.) that help plug the infrastructure gap in small increments since these don't offer the photo op that cutting ribbons on major visible projects do.

Builders make above average income in New Zealand. Say land cost 1 year of average income that leaves 2 years of average income for materials, consenting, engineering & architecture and 1 year of average income for the builder to get your house up. If a builder makes 1.5x average income it means 1 builder working for 9 months on his own would need to be able to complete a house to hit your 4x average income figure. If the builder would like things like annual leave, administrative staff, ird compliance, sick leave, etc it would mean an individual builder needs to be able to complete a house on his own every 6 months, less if he needs sparkies, plumbers, gib stoppers, painters, roofers, etc. essentially the wage of builders and trades set a floor under the cost of housing.

The productivity of the average operator sets the price.

They would be engineering a world record. As a "soft landing" has never successfully occurred in recent history.

The closest anyone has come to a soft landing was Canada through the period 1990 - 2000. During this period inflation was tamed and the housing market stagnated but didn't really crash too hard. This meant that someone who purchased a house in 1990/1991 would make a loss if they sold prior to 2000 (taking into account realtor fees etc).

I'm still waiting for someone to produce reasons why the same thing won't happen here over the next decade.

This is the outcome the US Fed is determined to avoid. Which is why they have pencilled in another 2 rate rises, which will take US rates higher than NZ, even though their inflation rate is currently 3% compared to our 6% (or 6.6% if you want to just focus on domestic inflation). Either the NZ or US central bankers doesnt have a clue ..... hmm, wonder which one it is?

“The worst outcome for everyone would be not to deal with inflation now. Not get it done. Whatever the short-term social costs of getting inflation under control, the longer-term social costs of failing to do so are greater. The historical record is very, very clear on that. If you go through a period where inflation expectations are not anchored, where inflation is volatile and interferes with people’s lives and economic activity, that’s the thing we really need to avoid and will avoid,” Powell said" [from this weeks Fed minutes]

Your critical reasoning and understanding of macroeconomics has matured a lot IO.

Thanks TK - appreciate the compliment.

When the solution to our economic woes is to destroy businesses, livelihoods and stored wealth - is it possible the system is a tad broken?

The system is broke. China no longer wants to import our inflation. This was the backbone of our economic model. What are we going to do now? Make products or something...

Make products or something...

Yikes, I don't think people have actually designed and made stuff in the entire history of this country, swapping food for other goods practically the entire time. There was a brief period a few decades ago when we assembled imported components into finished products for our domestic market (the reason why I mentioned design).

The experiment to move us on from food exports (without proper leadership and clear direction I might add) has failed terribly with food & fibre currently making up less than 11% of our economy but 69% of total exports.

What about Fisher & Paykel Healthcare and Appliances? Still have design offices here although manufacturing now offshored.

Healthcare still manufactures here.

Appliances do a lot of offshore rebadging of their parent company’s products, if that counts as manufacture

It was broken at the GFC when the solution was to entrench inequality via excess debt creation/asset bubbles.

It is time to restore the middle class again. You know those people who go to work doing a normal job and can afford to buy a normal house.

The world and our economy doesn't need to be this way.

But it may require a more even sharing of the economic pie (and no I don't promote socialism - but we appear to have a system of socialism for the already rich, and a horrible form of capitalism that punishes the middleclass and the poor).

The middle class don't really have much of a place when the labour market is billions of people.

Or maybe the system is just doing what would naturally happen (ie catastrophic market crash) but staging the destruction in a slower, more controlled manner. Flattening the curve, so to speak…

I do wonder if it could ever work in the long term though. The more patches you add to the balloon, the heavier it gets and faster it eventually falls.

We may look back on this time in history as “the era in which governments thought they could artificially control the economy by manipulating interest rates”…

As a comparative benchmark using the ol' Truflation, yoy price inflation for 'food at home' in the U.S. is running at 5.92% - approx half the rate of 'food producin' Nu Zllun.

"the highest-expenditure households spent the biggest portion of household spending on interest costs (7.4%)"

This seems like good news, our inflation fight is primarily hitting those that can afford to pay.

Yes it's interesting and suggests the nice-to-have margins on the supply side have less stress.

7.4% to the wealthy is nothing in terms of impact on daily life compared to the same for those who don't have a dollar to spare at the end of the week. Those interest rates will be via investments like housing where they will offload some of the rise to the occupying tenants, thus reducing the already lesser impact.

interesting

Agreed, those on basic wages living payday to payday will be increasingly struggling, and yes, the wealthy will not be greatly impacted especially those cash rich and partly being able to off-set rises with increased TD rates.

Although, not so sure about those with investment properties. From memory, a recent interest.co article indicated for the past year a $50 week increase in rents which is hardly going to off-set very significant increases in rates, insurance and mortgage interest costs . . . . and especially, for this financial year, the level of mortgage interest deductibility reducing from 75% to 50%.

However, there will be no sympathy for property investors on this site. :)

Cheers

However, there will be no sympathy for property investors on this site. :)

With any investment decision, there should be an element of stoicism. Put it like this. You could have 2 different mindsets:

1. House prices go up every 7-10 years because that's what they told me in the seminar and it's validated by Granny Herald.

2. Worse-case scenario is that this investment could go to zero and I will lose everything I invested....and more.

#2 punter is in a far better position to deal with reality and different outcomes.

Punter #2 will never make any money because he/she will be too scared to invest.

The person who will be successful is the one who understands both, point #1 AND point #2

The house always wins.

Understanding #2 means you understand #1 by default Dr Y. But let's be frank, you're more attuned to the Ashley Church school than widely read in the worlds of Robert Shiller and Nassim Taleb.

You don't seem to grasp them, or Stoicism.

Shiller thinks ol' ratty tat tat tat is bupkiss. You wanna hold the guy up as a genius we should listen to, while at the same time overlook where his views conflict with your own.

The inflationary doom loop continues until the epic bust of the 21st century. The silent generation is the only living generation to experience what is about to happen within the next 12 months.

My Dad was there in the 1930s (in the UK back then). He says he's never seen conditions as tough and unpredictable as now.

And the wild ride is only getting started.

I see TPM are going for a wealth tax. Have they consulted their own Iwi on this? The tribes own a fantastic amount of assets.

I'm sure appropriate exemptions will be made.

Lab/nat/act govt

I’d love to know how many ‘shovel ready projects’ are still pumping massive amounts of money into unfinished projects - and the huge ongoing funds committed to reform programs which are now stalled, treading water or under further review - and add the huge insurance stimulus which will need to come towards rebuilding after the cyclone - combined with constrained productivity out of the primary sector due to it having been reasonably successfully re-oriented around environmental aims rather than productive pursuits (which will largely cap productivity for now- think carbon etc) - and the recipe for longer running inflation looks pretty potent. Don’t forget that the only way big spending by governments ever really gets whittled into history is largely via inflation, growth or higher taxes. Growth has nowhere to go and higher taxes have been ruled out - that leaves only one thing.

Auckland Transport & Council seam to be putting projects on hold on account of there books. Other councils are in a similar boat. So we have a situation where both the private and public sector are slowing down at once. Not good Keynesian economics

No need for councils to stop wasteful spending though.

The gist of this paywalled article is that about $127m of this went to law firms while AC has 65 lawyers on its payroll at a cost to ratepayers of $9m a year. This wasn't known to the councillors or the mayor until recently.

Gets more interesting, some councillors are connecting the dots and alleging that those accounting firms are being contracted to keep such wasteful spending items hidden from councillors, the mayor and the ratepayers in creative ways.

USA inflation @ 3% today. Yet the Fed just increased their OCR to 5.5%

NZ inflation @ 6% (but really 7.2%) OCR 5.5%

I'm picking further movements upwards for the OCR. The whole point is to reduce borrowing and significantly reduce the amount of new borrowing. But on the other hand, we still have 6 months of people rolling off 2.x% mortgages to 7.x and 8.x% mortgages.

Orr has not been correct in any of his guesses for the last 3 years. So you can safely assume that anything Orr says about the future will be incorrect.

It's going to get nasty. However, I suppose many of those who haven't bought in recent years and can afford to will pay the same fortnightly repayments and simply lengthen their mortgage term. This going forward would mean a higher interest portion and a lower principal repayment.

So, they have no real reason to cut discretionary spending and all that the rate hikes will have achieved are higher margins for banks.

technically the banks will not have higher margins because of higher interest levels. because they would also buy "credits" from the market on higher interest rates.

the only thing change regarding their profits is credit volume. and the higher interest rates, the lower volume.

The whole point is to reduce borrowing and significantly reduce the amount of new borrowing. But on the other hand, we still have 6 months of people rolling off 2.x% mortgages to 7.x and 8.x% mortgages.

That just kneecaps the bubble. The problem is that too much of the nation's wealth is wrapped up in houses. There's a trade-off.

Well this is the big problem because rising rates do not affect everyone across the board to the same degree, increased mortgage rates see more money going out the door with zero return but those with TD's have money coming in the door for doing well basically nothing. Really its the ultimate wealth transfer isn't it ? The rich are getting dramatically richer while the working poor get poorer.

....but those with TD's have money coming in the door for doing well basically nothing.

Cash does not protect one against inflation. Never has. It's very useful in deflationary environments where it holds its value. Japan has been like that until quite recently.

The working poor don't have mortgages.

I think everyone is going to be poorer, just some more so than others. Maybe you are thinking of Banks and Supermarkets?

That's it. We've had decades of creating tokens (demand), which has not increased supply, and actually buggered supply by suppressing and driving away young workers. So there is a huge unravelling underway. All the govt can do now is fiddle about trying to influence the distribution of losses.

We must increase inflation to fight climate change, so says one of the a chardonnay socialists James Shaw, indirectly.

https://www.newshub.co.nz/home/politics/2023/07/climate-change-minister…

I'm with K Gurunathan's column this week on Stuff - let's keep fighting climate change, but change the balance towards adapting before we don't have the money to pay for adaptation.

Food costs were not the biggest contributor to the annual figure. Clarification from stats NZ below:

Between June 2022 and June 2023 prices in order of their contribution to the overall movement for:

- interest payments increased 28.8 percent

- grocery food increased 13.2 percent

- private transport supplies and services decreased 9.9 percent

- rent increased 4.8 percent

- fruit and vegetables increased 21.2 percent.

Those damn landlords...

What is the weighting for each? Last I looked, rent was 9%, though a far larger % of outgoings for those affected. Don't forget the median mortgage was less than half the median rent - coupled with higher incomes amongst the mortgaged - there's plenty of room for rate movement (and increased payments amongst that cohort) yet.

What if you add #2 and #5 to come up with "Food" costs?

Fresh food & vege is the current killer. Doing a lot of carrots. Doesn't sound like it's much different in most other places. I'm just glad we don't have get our wheat from the Ukraine.

I wonder if there are regulations on how many parts per million of shrapnel wheat can contain?

Given how much we import in the way of basics, that the US Federal Reserve has recently hiked rates to our level must surely mean our inflation is going to stay elevated, no matter what the RBNZ does.

Domestic inflation has barely budged in 18 months, so yes, it looks like inflation is going to remain elevated. If rates dont go higher the NZ dollar will tank, so we will import inflation that way as well.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.