They are not quite there yet, but the main banks are getting much closer to offering a 6% term deposit (TD) rate.

ANZ has now stepped up to match BNZ and Kiwibank with a 5.90% one year TD rate. That is its highest rate since just before the Global Financial Crisis.

Update: And now Westpac has matched these same rates with a set of +10 bps rises.

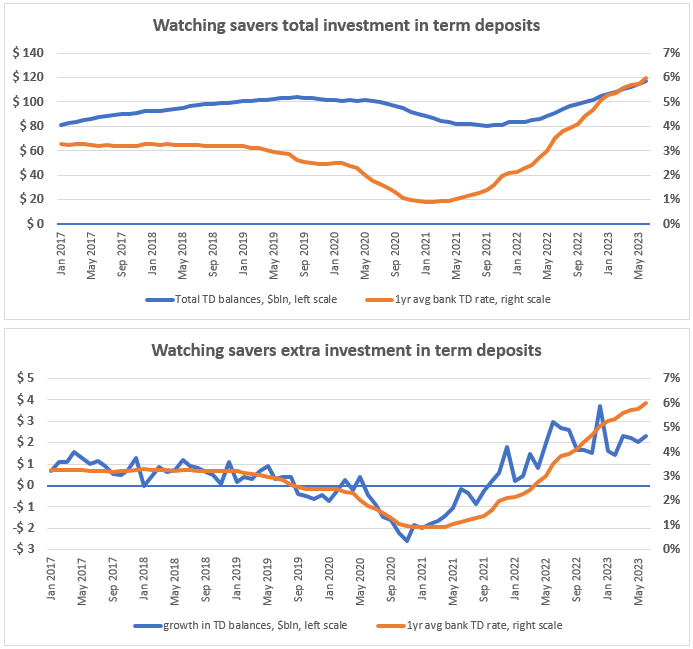

Higher rates are motivating savers to shift funds from low-yielding current accounts and savings accounts. They are also helping grow customer deposits.

The spreading of higher rates to the main bank offers will enhance that shift. And it should get a new push along when main banks start offering rates of 6% and more. (Or maybe that should be "if" main banks start offering rates of 6% and more).

But 6% rates are available now from many challenger banks.

For nine-month terms, Bank of China offers 6.08%, Heartland Bank offers 6.00%, and Rabobank also offers 6.00%.

For one year, way out in front is SBS Bank which offers 6.50%. Heartland Bank offers 6.10% for 12 months. Bank of China offers 6.18% for 12 months. Kookmin Bank offers 6.00% for a minimum $10,000 deposit, but 6.10% for a minimum $100,000 deposit. China Construction Bank is also at 6.00%. TSB does too. But Rabobank offers 6.15% for a one year term deposit.

Only one bank, Rabobank, offers 6.00% for a longer term, out to 18 months. Otherwise offers from all banks fall away fast from there. There are more details on how and why here.

One risk savers should watch is the cost of wholesale money and you can do that looking at swap rates. You can do that here. Earlier this week the one year swap almost touched 6.0% again. It did that first in May. We have had a long almost three year run up in background money costs. The Official Cash Rate rises have been part of that. If this trend reverses for any reason, the pressure on rates to savers will ease making those who locked in longer rates look good. Wholesale swap rates haven't shown any sign of pushing up bank to the 6% level in recent weeks.

Almost all banks are pricing longer rates lower than their one year offers, and that inversion is growing.

An easy way to work out how much extra you can earn is to use our full function deposit calculator. We have included it at the foot of this article. That will not only give you an after-tax result, you can tweak it for the added benefits of Term PIEs as well. It is better you have that extra interest than the bank, especially if you are in the 39% tax bracket - PIEs are taxed at 28% flat.

* Kookmin Bank's 6.10% one year offer is for deposits of $100,000 and more. For a $10,000 minimum it is 6.00%.

The latest headline rate offers are in this table after the recent increases.

| for a $25,000 deposit July 27, 2023 |

Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 4.30 | 5.75 | 5.80 | 5.90 | 5.70 | 5.50 | 5.25 |

| AA- | 4.20 | 5.65 | 5.65 | 5.85 | 5.75 | 5.70 | 5.60 | |

| AA- | 4.30 | 5.75 | 5.80 | 5.90 | 5.70 | 5.50 | 5.20 | |

| A | 4.20 | 5.75 | 5.80 | 5.90 | 5.40 | 5.20 | ||

| AA- | 4.30 | 5.75 | 5.75 | 5.90 | 5.50 | 5.40 | 5.20 | |

| Other banks | ||||||||

| Bank of China | A | 4.70 | 5.88 | 6.08 | 6.18 | 5.80 | 5.50 | 5.30 |

| China Constr. Bank | A | 5.00 | 5.85 | 5.90 | 6.00 | 5.85 | 5.50 | 5.40 |

| Co-operative Bank | BBB | 4.20 | 5.70 | 5.75 | 5.90 | 5.65 | 5.60 | 5.50 |

| Heartland Bank | BBB | 4.00 | 5.90 | 6.00 | 6.10 | 5.35 | 5.30 | 5.30 |

| ICBC | A | 4.70 | 5.65 | 5.90 | 6.00 | 5.80 | 5.45 | 5.40 |

| Kookmin Bank | A | 4.40 | 5.60 | 5.70 | 6.00* | 5.20 | 5.20 | |

| A | 4.75 | 5.90 | 6.00 | 6.15 | 6.00 | 5.70 | 5.60 | |

| BBB | 3.90 | 5.50 | 5.40 | 6.50 | 5.35 | 5.35 | 5.35 | |

| A- | 4.25 | 5.30 | 5.40 | 6.00 | 5.50 | 5.50 | 5.25 |

Term deposit rates

Select chart tabs

Term deposit calculator

90 Comments

This will only increase the reason to sell off those rentals .

These rates appear to be becoming the new normal. For the leveraged, Land-lording is now a money pit.

National / ACT better start doing the sums and work out how much the taxpayer is going to be giving landlords back in mortgage interest rebates with the interest rates so high... something will have to give

All Nat/ACT would have to do is freeze the rebate at 50% (current level) and they'd be offering twice the rebate Labour are offering come 1 April, and an infinite amount more the following year. Anyone who bought after 27 March 2021 is already toast.

If rates keep climbing then obviously it's going to start losing the govt money though.

The current government's wasteful spending is what will be gone!

Yay, I will be getting 4% after tax!!! Wait, that's below the rate of inflation isn't it?

Depends on your tax rate. Inflation is not relevant, it affects everyone at different levels. I'm better off now at 6% than I was only 2 years ago at 1%. All depends on the size of the TD, I don't think those with millions in a TD are crying about inflation.

Real returns after tax are all that matters. Not sure you are much better off now than 2 years ago (when inflation was much lower). True, everyone's CPI is different but hard to argue that inflation is immaterial to larger TD investors either.

A flat rate of tax (eg 10%) for all savers would help make TDs more desirable.

So the rich get even richer?

Tax on your TD should be zero. The tax on the first $18K of income should also be zero. Tax on people earning over $150K should go through the roof, these are the people making all the money not someone trying to survive on low income or a TD in their retirement.

But it is people on those high incomes that are actually making the decisions, so don't they have a vested interest not to have higher rates for higher income earners? Australia have a higher tax rate than NZ which is hardly every mentioned, I wonder why.

Well we keep getting these stories that the wealthy want to pay more tax, but like you say when it actually comes down to fronting the cash there is no action to change the status quo.

Which is exactly why the OCR should be above the CPI by some margin. That's yet to come. Not for the tax-offset benefit, but it's the only way to get on top of the CPI rises. You know, the OCR in its normal position above Inflation.

Unfortunately a high OCR, while benefitting some (ie the TD savers), bring the country to its knees by destroying small businesses and farmers.

How does a high OCR destroy small businesses ? I own an SME, sure sales are down, but we are lowering stock levels and banking the cash. Not feeling any pain at all.

I take it that you don't have a business loan?

Savers have been suffering a lot longer than that

If your are debt free and your expenses are way less than your TD's returns, you are not doing too bad

That’s one way to look at it. The other is that it’s money for nothing. Stress free, time free, risk free investment on top of your professional earnings.

short term thinking

Awesome. Several months later than I expected but we pretty much got there now.

Oh that's right, now the rates are more favorable than risky rentals, you've conveniently found some TD's in your sock draw?

Love it!

Never said I had rentals, pretty decent TD however.

Of course you do!

And on-call savings account are not even at the OCR rate. Disgusting rip off.

That want to remove your liquidity, that's why!

At last, normalisation of monetary policy. It's been a long time coming, may we never ever go back to the crazy experiment of the last 10 years. Let asset markets (globally) find their equilibrium.

So, so, so many people do not realise this is a normalisation. Far too many are expecting rates to come down.

Yes, this is the unfortunate collateral damage from the experiment.

well said

Spruikers scoffed when we stated that TD rates will touch 6%... infact, we are the optimistic ones

Maybe overly optimistic but can see the 1Y rate crossing 7%.. with the next round of inflation hitting us..

yep I have been shifting some of my lesser shares over to TD's now they are close to 6%, just trying balance portfolio up a bit.

Money is going to start pouring into TD's now at 6%.

That's the idea. It removes liquidity from The System. Part of "the higher the OCR goes, the less we have to spend" equation.

The problem comes when you do want or need to spend, and then realize that your money is locked away for a year!

As I suggested - that's the idea.

Imagine how much liquidity will be tied up; not available to fuel Inflation today, if the infamous Inverted Yield Curve normalised, and if instead of locking-in at 6% for a year you could fix at 15% for an alternative 5 years.

6% TD is not keeping up with inflation. True.

But it sure beats 1% TDs. Not so long ago.

And vastly better than some scuzzy rental going backwards at $20K a month.

I dunno

An elderly person might do well with lower costs than the TD earnings

If property price go up 5% next year, on a $1M property you would still be a making 30K but guess time will tell

You might make $30K on paper but you cannot actually spend that $30K without selling the property. TD's over 6 months pay monthly and that's money you can spend.

It’s not even that you can’t spend it, it’s that your standard of living is unchanged. The only way you get that money is by selling and buying a lesser house.

Rising house prices are a fallacy unless you lower your standard of living…. oh, and your kids without houses just got poorer. Great.

dont need to , you should have that much as your emergency fund. Its call Fin planning

Exactly. Interest paid on time. No maintenance, no healthy homes standards, no tribunal and zero stress. Give me 6% any day

We flicked on 3 of our lesser performing rentals a couple of years back, and are about to roll off a 12 month term at 4.2%. Our wealth manager reckons he's going to be able to get us up around 7% for the next 12. That's better than at least half of what we're still holding on property - if the market wasn't so depressed I'd be tempted to sell a few more!

Depressed is a relative term, of course. It only matters what the prices will be tomorrow. Would you hold on if you got the queezy feeling that perhaps property would halve in the next 5 years, just because prices are lower today than yesterday? I doubt it. The trick is, as you did, to see what's going to happen before the pack does.

Chinese property developers are now fleeing Australia in droves...Country Garden has joined the retreat of debt-laden Chinese developers from the Australian housing market after putting one of its last remaining local projects, a giant estate in Melbourne’s west, up for sale with an asking price of $250 million...purchased for $400 million in 2017. (AFR)

Why are they selling the undeveloped parcel so 'relatively' low? Not because they see the prices as higher any time soon.

Country Garden, like many other Chinese developers, is on the skids and is probably a fire sale directed by their bankers/government regardless of where they see value in the future.

or it could return to 5% pa growth , no one knows just like no one knew post covid

"Wealth manager" --- do it yourself and you'll find you will keep more of your own money

Depends. They maybe able to get better rates, just as mortgage brokers can often get better rates.

When challenger banks offer term PIEs then they become relevant. Or Rabo could just set their TD rate to 7.0% that would be equivalent to what ANZ offer right now.

I have noticed that some of the rates of some of non big four banks haven't been increased for a long time and are now not looking good compared to the rates being offered by the big four. So they need to up their game. Likewise on call or bonus saver rates are still quite low.

If term deposit rates are below inflation and taxed to boot then surely it's a foolish strategy to convert all your assets into term deposits. Oh look I'm making -3% on my investment, how wonderful!

lol!

Why is that funny? It's fool's gold my dear Poppy.

Just running a rough thought experiment, say inflation rate is 6% and TD is 5% but tax shaves off 2 then you are really only returning 2% in a 6% inflation environment. You'll lose it all long term like playing Blackjack.

If property bottoms out then a rental property could yield 4% plus 6% appreciation making 10% -3 for tax = 7% returning 1%. An investment, once stable, that is a hedge against inflation.

Property or shares or something else will do better over the long term whilst term deposits are likely to do worse making the outcome even more disparate.

Term deposits are for silly old fools.

Zachary, now you've become the entertainment. You're obviously paying it whilst I'm receiving it. Technically, you're paying me interest - thanks :)

I remind you again about that sizeable 5-year 4.27% (interest paid monthly) TD that I took out with Rabo in Jan-2018 came out earlier this year. Perfect timing don't you think? Now I'm into the one year rollovers.

by Retired-Poppy | 19th Mar 18, 2:10pm "in January I took out a TD @ 4.27% with interest paid monthly

edit

It's like "Investing 101". Would be interested to know other people's thoughts.

Nah, you're just trying to stir. Property will no doubt make a come back. In the mean time you'll just have to endure years of either losses or at best, property seriously underperforming the prevailing rate of inflation. Those interest rates when paying it, it's nose bleed territory. There's just no compensation for that kind of dead money and on a declining asset too mind you.

Brain fade from Zac, low carb diet.

Those who lose least win most here now. Perhaps you are spending too much time looking at yourself in the rear vision mirror Zachary? "Experience teaches us that earnings estimates, especially those of a longer-term nature, are not particularly reliable" Arthur Zeikel

I held off buying in 2021. Currently its down by 33% since then.

I would take TD over that purchase thank you very much.

Agree about assets in an inflationary environment but consider this

if you are a 70 year old single retiree, and your expenses are less than 70K you will be earning soon , you would be doing ok.

Well RP as much as I hate to say it we agree on that.

Zwifter, there had to be common ground for us somewhere!

Well you did strike it lucky going long back then, I stayed short term and paid the price. Now short term rates are high and long term rates are lower so what's the call ? Still tempted to go the 12 months at near 6% ?

For the big one that came out in Jan, I'm getting 5.5% till Jan 2024. Other smaller TD's with Rabo I'm getting 5.75 - 6%, none at 6.15 yet. As I'm following the interest rate up, I'm only taking out the yearly ones at the moment with interest paid at maturity.

Term deposits will never be a hedge against inflation. Prove me wrong!

I never said they were Zac. Hedging against inflation seems to be your obsession not mine. I am happy with my lot as gains are already banked, earn further interest and right now in these testing times, its a great place to be :)

My wife and I got to be in this position by living well but still within our means and not obsessing over beating the publicized rate of inflation. Our outgoings are low and inflation has put no dent in our prospects or choices. Our interest income is decent and we both work full time. We are among the fortunate financially.

Hope this helps you understand.

Weird how so many don't get it. I guess you need to get in that financial position before you do.

Having a savings account is hardly investing.

Good-on-ya Zac....

There are times in the investing cycle where return of capital beats return on capital, particularly if you need that capital to survive.

Simply because one sits just behind inflation doesn't mean that day-to-day they don't enjoy a better lifestyle from their investment returns that they would without them. On paper you can say yes, they are worse off in terms of purchasing power, but purchasing power on paper is one thing. The lifestyle your level of income affords via whatever means, including TD's, as long as you are happy with it, then that is fine for you. Everyone's experience in life is subjective based on their own values.

Maybe not but inflation before the GFC was under 3%, but interest rates were as high as 8% if not more with banks like Rabo at the time with bonus saver accounts. This is just a point in time and things can flip very quickly.

Indeed in moments of time things vary . However, I'm looking at it with a long term perspective.

I asked ChatGPT this question:

If you put $20000 in term deposit in 1980 how much would it be worth today compared to the same amount in equities using historical averages?

The reply:

- $20,000 in term deposit with a 5% interest rate would be worth about $118,512.06 today.

- $20,000 in equities with an 8% average annual return would be worth about $312,454.17 today.

And if you put $20,000 into a house in 1980, what does it come back with ? Let me help you out, about $1.4 Million.

So you agree with me then?

My sister bought a house for 20k around 1980. It's worth about 800k now. Of course if it was rented out all that time much more money could be added to that figure.

Perhaps we need to continue incentivising growth of native hardwoods so that our housing is built for longevity like yesteryear. Then again, the return on this would be horrible given everyone is hooked on cheaper fast growing pine that can be treated.

But why is that? So in 40 years time will the same appreciation occur? Maybe if the interest rates go down to zero or negative, but that would be totally crazy for houses to cost so much. But then again they are saying the same thing now. 40 years ago many households only had a single income earner as the wife used to stay home to look after the kids, and my grandma said that if you didn't it was frowned upon.

But why is that?

Inflation mostly.

And Inflation has thoroughly destroyed your purchasing power

https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

20,000 in 1980 is equivalent to 118,000 in today's dollars, with a loss in purchasing power of 80%+

Inflstion is theft. Opt out by buying Bitcoin which will have its inflation rate cut from 1.8% to 0.9% next year

I find it confusing. Why are banks competing for TDs when they must already have way more than they used to need?

Looming 'bad debts' - they can accurately working out which clients are in real trouble - are punching holes in their regulatory capital ratios?

Any one investing locking their money with non-banks are taking a huge risk now, especially with main banks offerings now

Heartland bad debt book has skyrocketed over not much assets.

https://bankdashboard.rbnz.govt.nz/summary

The rates on offer are but a 'price'. Without an indication of actual 'sales quantity' they mean little.

Just like when the banks were offering 2.99% for 5 years. When people applied - banks turned the majority down using their 'commercial judgement'. Classic 'bait and switch'. The banking inquiry will show some enlightening results.

One wonders how many banks are looking at their regulatory capital ratios both now and in the next year and are getting just a tad concerned.

About time, switch bank of necessary.

Last time we had inflation this high, term deposit rates were nibbling at 8% and mortgage rates exceeded 10%.

We cannot go there now because the level of debt in the housing market is to high. The strategy now is push the rates to the max which is what we have now and the side effect of that is you now have to wait much longer for inflation to come down. Its like a simple control loop, we are applying low gain and we will eventually get to the set-point, it just takes longer.

We could be sitting at inflation of 5% to 7% for the next 5 years if the reserve bank doesn't get serious.

The huge increase in wealth of retired folks, compared to 30 years ago, is upwards of 600%. They are much less likely to be negatively impacted by high inflation (especially if they have significant savings in term deposits). How do you get the portion of the population that controls 65% of the wealth to stop spending??

Basically its now impossible to target everyone equally because society is no longer equal. The higher mortgage rates are only going to smash a small percentage of the population. If rates go up from here then only some get totally smashed and the harder you smash the people at the bottom the better off the people at the top become. You have to fix the tax brackets and stop those at the top evading tax because its only worth it for those the top to evade it due to the amounts involved, the average punter on PAYE just coughs up every month.

I'd be interested in any evidence that retirees are spending their "wealth" up large.

Most of us are finally in a relatively stable economic position after a lifetime of frugality & sober habits that we cannot seem to break.

Agreed, you generally have money later in life because of your lifestyle of not blowing it. Yes its hard to change but when you cut loose now and again it does feel good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.