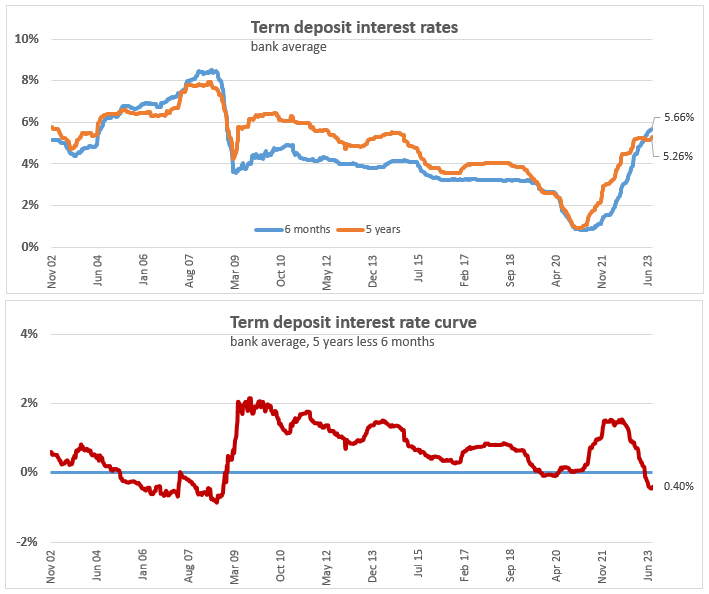

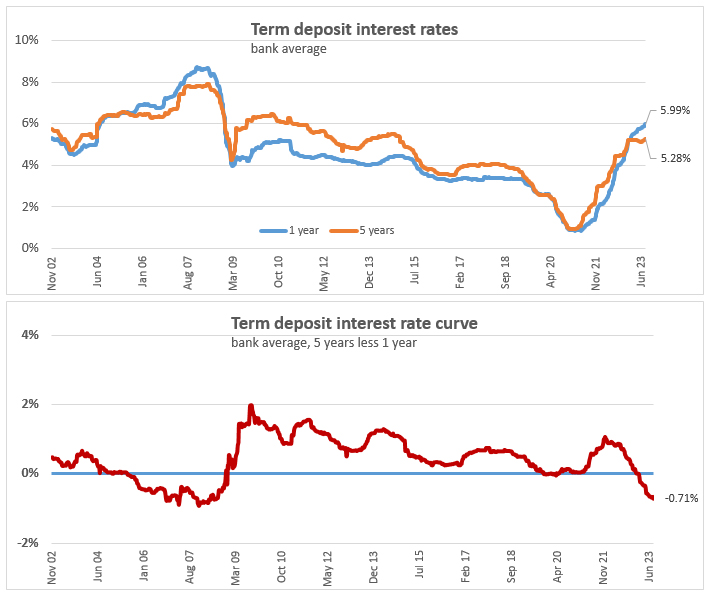

The average bank six-month and one-year term deposit rates are higher than the average bank five-year rate for the first time since the Global Financial Crisis (GFC) era.

As the charts at the foot of this article demonstrate, the average carded, or advertised, bank six-month and one-year term deposit rates were closely aligned with the five-year rate for a time in 2020 during the early period of the Covid-19 pandemic. But they haven't been above the five-year average since the GFC nearly 15 years ago.

At 5.66%, the average six-month rate is currently 40 basis points higher than the 5.26% average five-year rate. And at 5.99%, the average one-year rate is 71 basis points above the five-year average.

A similar scenario is at play with wholesale interest rates. At the time of writing the five-year New Zealand swap rate is at 4.73%, with the one-year swap rate at 5.81%. That means the one-year swap rate is 108 basis points higher than the five-year rate. As explained in our look at one and two-year mortgage rates being higher than five-year mortgage rates earlier this week, the same thing happened during the GFC period.

A swap rate is an interest rate based on where financial markets' participants think interest rates will be in the future. Swap rates allow the likes of banks to manage their interest rate risk by locking in a fixed rate for a set time period.

Term deposit rates typically rise when swap rates rise as banks need to secure a high level of retail funding to meet Reserve Bank requirements and don't want to be overly reliant on wholesale funding. In a rising interest rate environment banks sometimes come under pressure to increase deposit rates, as they did from the Reserve Bank earlier this year.

"Deposit rate increases continue to lag the increases in wholesale and mortgage rates, resulting in a further widening of bank margins between lending and deposit rates," the Reserve Bank said in February. "Higher deposit rates are a critical part to encourage savings, which takes inflation pressure out of the economy."

Inversions, where longer-term interest rates are below shorter-term interest rates, are historically associated with investors believing a recession is coming. The Reserve Bank's changes to and guidance for the Official Cash Rate (OCR), NZ's benchmark interest rate, influence short-term swap rates, while longer term rates take their cue from international influences such as the US Treasury yield curve, which has also inverted.

The Reserve Bank has increased the OCR to 5.50% now from 0.25% at the start of October 2021 as it strives to rein in inflation, something other central banks around the world have also been doing. NZ inflation, as measured by the Consumers Price Index, fell to an annual rate of 6.0% in the June quarter from 6.7% previously. That remains well above the Reserve Bank's 1% to 3% target range as the war on the highest inflation in three decades continues.

Heading into the GFC the OCR was at 8.25%, the highest it has been since its introduction in 1999.

See all advertised, or carded, term deposit rates from one to five years here. And see all rates from one to nine months here.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

1 Comments

Why is demand for loans among European busn esp. small & mid-sized at an all-time low (20yrs)? It is NOT rate hikes. Rates rise and so does lending during real inflation. In Europe, lending has crashed. Yes, crashed like 2011-12 and 2008-09. https://buff.ly/43IiYin Link

Is it any different in NZ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.