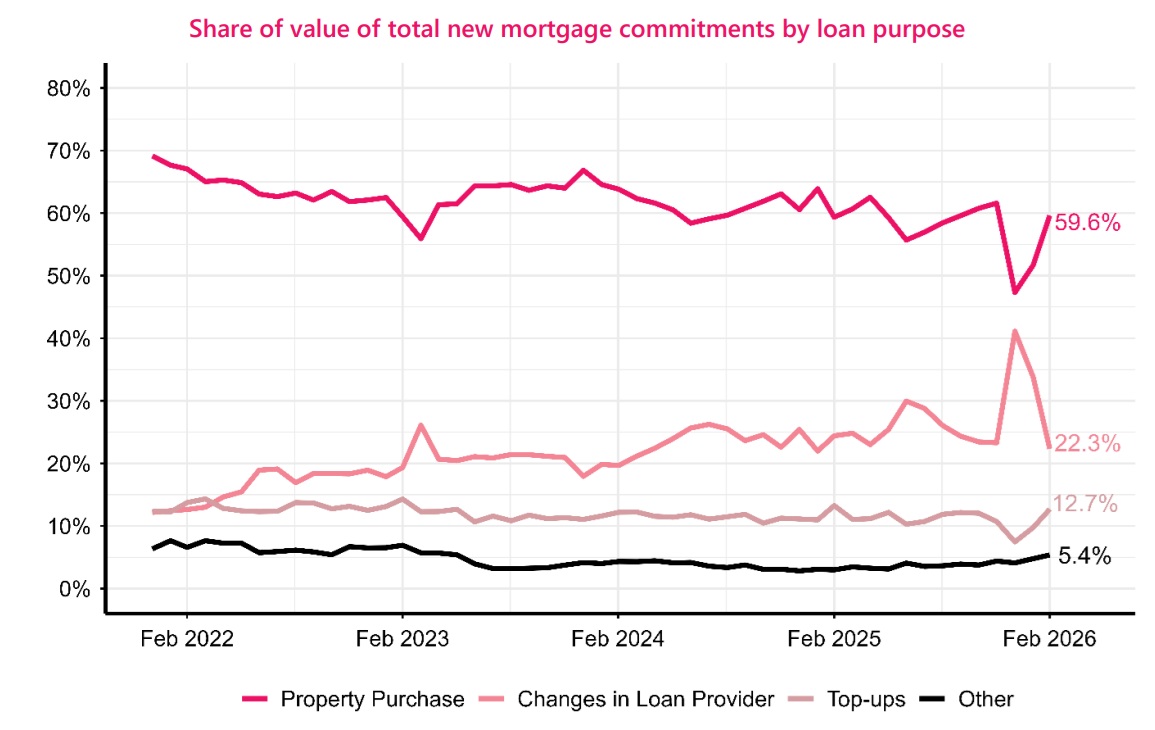

The massive moves by mortgage holders to switch loan providers are now abating and the mortgage market is returning more to a form of normal.

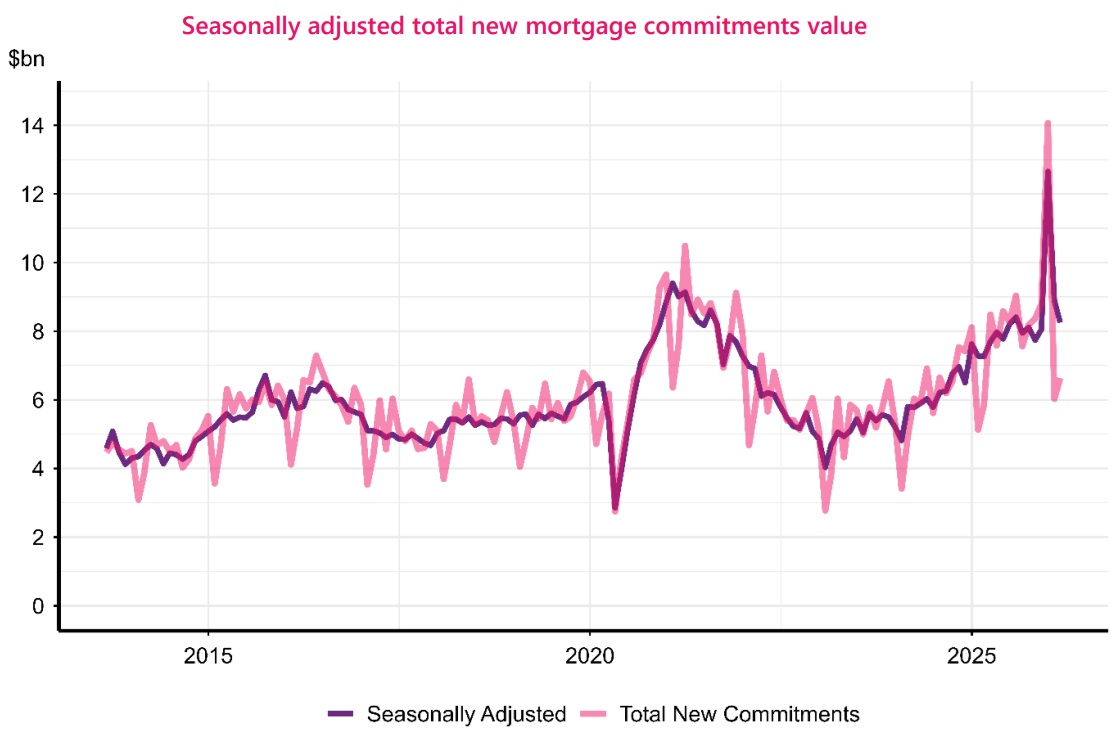

Latest Reserve Bank figures (for February) show that just 22.3% of the $6.635 billion worth of 'new' mortgage commitments made in the month were due to customers switching loan providers. On a historic basis, that still remains quite a high figure, but its actually the lowest such share since January 2025.

And it's all a far cry from December 2025, when a record 41.1% of new mortgage commitments were a change of loan provider. The $5.785 billion worth of mortgages changing banks in December helped push the overall tally of new mortgage commitments in that month to a new record high for a month of $14.066 billion.

December was a high point for home owners refixing their mortgages because very many of them had held off fixing for long terms while they waited to see what the Reserve Bank would do regarding the Official Cash Rate in October and November.

October brought the double-banger 50-basis point reduction in the OCR, taking it from 3.0% to 2.50%. But while the November RBNZ OCR review brought another 25-point cut to the current 2.25%, it also brought a surprising bucket of cold water for those looking for still more falls - with the RBNZ indicating clearly it was 'done' with cuts, barring any surprise developments.

Everything's been turned upside down

This surprising (for the market) slamming of the door produced an opposite reaction, whereby wholesale interest rates started moving up, sufficiently to prompt banks to start raising mortgage rates again in December - a rude shock for homeowners playing the 'how low will they go' game.

And of course since then the world has been tipped on its head and we now face the prospect this year of both higher mortgage rates - of course, already happening as we speak - and of a higher OCR whenever the RBNZ decides the oil shock inflation impacts are maybe entering a 'second round' of inflationary impacts. Loads of room for speculation on when and whether that all happens though.

But back on those February mortgage figures, the fact the huge wave of re-fixing is now subsiding has seen the overall mortgage figures settle back into a more 'usual' pattern.

The $6.635 billion of mortgage commitments was up 13.5% on the $5.87 billion in February 2025.

But in terms of comparing the February 2026 mortgage figure with those from January 2026 - bearing in mind January's a historically quiet month - the February 2026 figure was up just 10.1%.

And after the RBNZ had applied seasonal adjustment, the February figures were actually down a pretty solid 7.2%.

In terms of who was borrowing in February, the RBNZ's summary of the figures (from which the graphs in this article have been taken), says the share of new mortgage commitments to first home buyers rose from 17.7% in January to 20.9%

But investors went the other way, dropping their share to 18.8%, down from 21.6% the previous month.

The mortgage figures so far this year are (not surprisingly) mirroring house sales figures thus far.

The sharp change in interest rate sentiment immediately before Christmas clearly knocked the market.

And all the more recent news is bad. The RBNZ's monthly averages of banks' advertised 'special' mortgage rates show that a lot of rates bottomed out in October 2025.

It's all getting away...

Since then the six-month rates have gone actually a little lower. But if you were looking at a longer rate, things have got away a bit. The three-year rate that was 4.8% in October, had risen to 5.07% by February, and a glance at the rates on interest.co.nz shows you might still get 5.3% for three-years now, but it's going fast.

Likewise the two-year rate, which has seen a resurgence in popularity recently, was 4.5% in October, up to 4.8% by February and is, according to latest advertised rates now around 5.1% with most major banks. That 5.1% rate by the way compares with an average market rate in March 2025 of 5.06% - so, so much for mortgage rate falls.

Economists are now starting to forecast actual house price falls this year, (with ANZ coming out on Thursday with a new -2% forecast for calendar year 2026).

All in all then, it will be interesting to see what happens with the housing market and mortgage figures over coming months. It will be particularly interesting to see how those who may have been keeping a 'go short' policy with their mortgages react in coming months. Stay short? Or go longer? Bearing in mind that the longer rates are going up and may well continue to do so.

Interesting times...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.