Since the implementation of the Depositor Compensation Scheme (DCS), residential mortgage lending by finance companies has risen over 30%, the Reserve Bank says, and depositors are putting more of their money into finance companies.

The DCS provides protection of up to $100,000 per eligible depositor, per licensed bank, building society, credit union and deposit-taking finance company, in the event of deposit taker failure. It was launched in July last year.

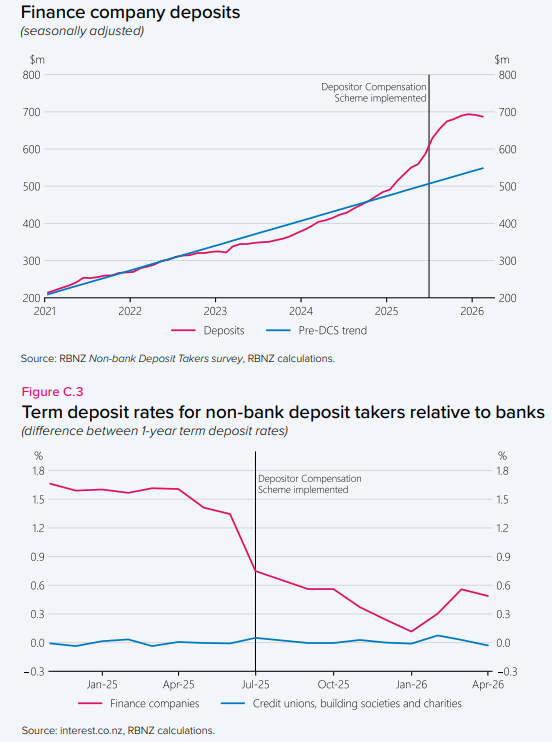

The Reserve Bank’s Financial Risk Stability Report, released on Wednesday, said since the beginning of 2025, deposits in finance companies had grown by over 30%.

“In contrast, other types of deposit takers have seen only modest changes in the total value of their deposits. This suggests that some depositors moved funds out of banks and into finance companies due to the introduction of the DCS,” the report said.

The report said deposits in finance companies reached around $700 million by January 2026, which is about 0.14% of the total deposits across all deposit takers.

Historically, depositors demand higher interest rates from finance companies due to the higher risks associated with finance companies’ business models, the report said.

But since the DCS was implemented, the report said “the spread between finance companies’ and banks’ term deposits has narrowed to around 0.5 percentage points, as eligible deposits in both types of deposit takers carry the same level of risk from the perspective of the depositor”.

“As a result, finance companies should not need to pay a much higher return than banks to attract deposits now."

“Interest rates paid by credit unions and building societies on term deposits have been less impacted as they were typically in line with bank rates even before the DCS came into effect.”

Mortgages

The report said deposit inflows have been mostly used to fund mortgages. Finance companies initially held these increased deposit flows in liquid assets like bank deposits and government securities.

“As the narrower term deposit spread has lowered the cost of funding for finance companies relative to banks, finance companies have been better able to compete with banks for lending opportunities,” the report said.

“Residential mortgage lending by finance companies has risen more than 30% since the implementation of the DCS, with these firms tending to focus on market niches that banks are less active in.”

The report said historically, customers who borrowed from finance companies often had higher risk profiles than bank borrowers.

"For example, they may have volatile income flows because of being self-employed. In addition, the loan books of some finance companies are concentrated in a small number of loans.

“However, the risks to the financial system from the increase in mortgage lending by finance companies to date are likely to be limited.”

The report said around 80% of mortgages by finance companies are at loan-to-value ratios of less than 70% at the time of “loan origination” - limiting their riskiness.

“In addition, the share of finance company loans that are non-performing also remains low. Finally, the overall level of lending through finance companies remains low when compared to overall lending in the system.

“The total value of residential mortgage lending by finance companies is around $550 million, whereas the value of mortgage lending by registered banks is around $388 billion,” the report said.

Overall, the increased finance company lending is unlikely to have materially increased financial stability risks, the report said.

The RBNZ would continue to monitor the impacts of the DCS.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.