By Elizabeth Kerr

Growing up I thought I was pretty average.

I wasn’t the best at school but I wasn’t the worst either.

I wasn’t picked last for the team but I was never first.

I think I lived in an average house and had an average kiwi upbringing.

This averageness continued on through high school, and to some extent I'd say the world was designed to encourage and reward me for being average.

However as an adult the pursuit of average with your finances is going to end up putting you in the poor house.

Average is just not good enough anymore, and what’s worse is that it’s a moving baseline.

The average house price just 5 years ago was $393,231 now its $542,277!

The average and endorsed way of managing your finances is to spend as much as you like as long as you have enough income to meet all the repayments.

The average way to save for retirement is to make the minimum contributions to Kiwisaver and hope that’s going to cover it, or to access your equity by moving somewhere cheaper.

Let’s look at average as it plays out below:

- Girl leaves university at 22 years old with an average student loan of $19,000

- She gets job with the average graduate salary of $42,000 and gets an average of 2% pay rise each year.

- She makes the average contribution to kiwisaver which happens to be the minimum 3%.

- She makes the minimum repayments to her student loan taking her 8 long years to pay off.

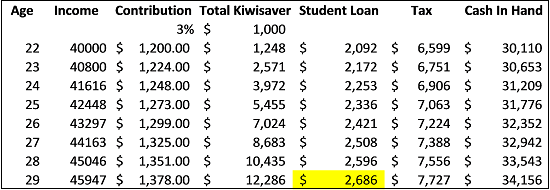

Her first 8 years look like this:

So, without doing anything out of the ordinary we can assume she will receive just $30k in the hand or $2509 per month and it increases slightly every year.

Once we take out money for her non-negotiables such as rent, eating, mobile phone, bus fare (totalling $1033 conservatively) she is left with $1475 per month to clothe and entertain herself.

She could put more towards her student loan/kiwisaver or start investing – but she doesn’t. This is also unbearably average.

After she has paid off her student loan she meets an averagely good looking, average earning husband and they want to buy a house. Together they spend the national average of $542,277 on their first home. By the time they can afford a 20% deposit ($108,455) using their savings and kiwisaver contributions they are now 39 years old. They have $433,822 to go and they lock it in and pay the minimum each month of $2536. It takes them 25 years to pay off the home. They pay it off aged 64. Just in time for retirement. They thank their lucky stars they didn’t remortgage and buy a bigger house when their 1.9 children asked them to.

Aged 65 they only have $97k each in their kiwisaver plus the pension (if its still around) to live off until they die at the average age of 91 for her and 88 for him.

Suddenly average starts to become really hard. Many people manage on much less but they had high hopes of achieving much more.

You see, shooting for average left them with not enough in the end.

But what could she have done if she wanted to make things much better? Now she might have married a rich social media app developer and lived happily ever after in the beaches of California but that’s as likely as winning lotto (1 in 38 million).

The more realistic answer is that she manipulates the variables at her disposal. Her first house could have been so much, much cheaper.

She could have worked for a year or two to pay for her uni, or even studied for free in Invercargill SIT.

When she did complete her studies and start working she could have saved more of her earnings, paid off her loan faster, or even started a hustle on the side.

What would have happened if she had saved her $1000 extra per month into her money machine instead of spending it when she first started work?

What if she totally forgets she receives a payrise each year and just lives off her graduate income instead?

Or what if they were both totally committed and created a lifestyle that lived off half their combined income when they married, or they raise their Kiwisaver contributions to 8%?

Things then start to get better than average.

Sure, she might have looked a little strange to her friends blowing money at cafes and on gym memberships, but attaining your own money machine requires you to be radically different - you just can't have it all.

Of all of the major financial lifestyle choices you can make you need to consciously choose where you fit into the range and based on your incomes and unique values instead of being swept up with society’s expectations and pressure to keep up with the Joneses, even if they are just average.

(Before you start telling me that their house would be worth enough to downsize, not every township has enough capital gains to make this choice worthwhile; and not every old couple wants to leave their family home and community for a cottage in Levin).

In closing this week; my average couple earn collectively just under $5 million over their entire working lives. $5 million!!! Surely they could have carved out a quality early retirement with that? But they didn’t. They started their journey positive that their averageness would provide for them in retirement as long as they didn’t shoot too high on the way. They started their journey with entitlement and left all their savings AND investment until the later years. They missed all of the benefits of compound interest and had to make a lifestyle adjustment when they stopped working.

Thinking about ALL of the money you have, and will earn, over your entire lifetime is quite good for figuring out what you can and cannot afford to do with the big financial decisions. Starting with the end (retirement) in mind will ensure you know how to avoid a drafty caravan and dry Weet-Bix.

Go on, why don’t you give it a go for yourself? If you need some help email me at Elizabeth.Kerr@interest.co.nz or find me on Facebook.

37 Comments

You state that the average graduate salary is 42,000 but then use 40,000 as your first tier in your chart.

Also as at 2015 the median graduate salary is closer to 44,000 as per http://www.careers.govt.nz/tools/compare-study-options/

You are quite right - i did muck up the numbers. However the median graduate salary on that site is $44k AFTER 2 YEARS. It's actually closer to $37k after one year... so i just took a stab around the middle. :)

My apologies, you are correct.

For a couple just starting out, the property prices in good suburbs in Auckland are so outlandish that there is no way that buying makes any sense at all.

Your first car doesn't have to be a "Tesla Model S P85D", you would generally get something more affordable first. Similarly your first house doesn't have to be in a "good" suburb, get something more affordable first. If you really "need" to live in a good suburb, buy in an affordable suburb, rent that property out and put the rental income from that towards your own rent.

This method is always going to be the second best option but done right can work well. By renting out the property that you own you can reclaim the tax you paid on the interest component of the mortgage as well as maintenance expenses and deprecation. Bear in mind that if you rent the property back to yourself or a relative it might be viewed as tax evasion by the IRD.

Landlords often also prefer fellow landlords as tenants because they understand some of the many headaches that we get from being a landlord. Additionally being a landlord generally shows sound fiscal management ability which I personally always find desirable in tenants.

At Sadr001. Yes i hear what you are saying, but unless it is part of a wider property investment portfolio then why would you pay $1.00 only to get $0.30 cents back in tax and still live elsewhere?

1. The property that you purchased will move along with the market (ie. if the market shoots up 30% so will your property's value) this is your so called foot on the ladder. Keep in mind that if your property's value goes up 5%pa and it would have taken you 5 years longer to save for your "good" suburb than to purchase in a "bad" suburb ( we are going to ignore the compounding effect of the capital appreciation for the sake of simplicity here ) then you'll have gained 25% of your property's value towards a deposit in your "good" suburb house. For example ( with a 20% deposit you buy a $300,000 house ) after 5 years at 5% pa (not compounded) your house is worth $375,000 giving you $75,000 + whatever equity you paid down over the 5 years towards your new house (add the original $60,000 as well if you plan to sell in order to buy the new property in the "good" suburb)

2. This way you have the flexibility to quickly downsize / up size to suit your circumstances (by virtue of not being tied to the property with a mortgage). When it is just the 2 of you, you could effectively "flat" to reduce your costs and when little Johnny is born you could move to renting a bigger place in that "good" suburb you wanted.

3. You build equity while renting for little to no extra cost instead of just paying someone else's mortgage. ie. couple pays mortgage > their tenant pays rent > that rent + tax refunded from cost of rental business ( interest on mortgage, depreciation, etc...) pays the couple's rent. The specifics will vary with each set of circumstances ( while flatting the rent that you make might be greater than the rent that you pay, when you move to the bigger place the opposite might be true)

Has anyone here done this? Email me at Elizabeth.Kerr@interest.co.nz.

@ Uninterested. Agreed. No Aucklander wants to have to choose between the mortgage or kids but if one doesn't pay attention to the order with which one does these things then quite possibly both will be out of the question.

You forgot to add kids in at 28,30 years of age.

As the lady gets older, chances for complications in pregnancy rise - down syndrome etc - remarkably at 30++ years. Our financial system has broader ramifications for the family unit.

The average age is 30-34... but they were too busy saving for a deposit so they missed out. But you are right, inserting the 1.9 kids into the numbers means that things start to look worse not better for their retirement incomes. This doesn't imply that only the rich can afford kids; it implies that saving the minimum into Kiwisaver and living beyond your wages... even if its only averagely.... means your retirement requires a major lifestyle change.

it means that we can't have a normal life in this type of world. Without 'ending up in the poor house'.

.

Meanwhile the government allows our water to be exported, free of charge, and hocks off everything in sight to the lowest bidder.

And we wonder why things are so difficult for the average family?

This is a great article. So many New Zealanders want to do just what everyone else does, but never stop to think where they will end up if they do that. The wealthiest in New Zealand are in the minority. That means they have not done things the same way as everyone else. If you want to get ahead you have to do something different to what all those around you are doing. As you pointed out Elizabeth, this means saving more than average or investing more than average.

Exactly :)

...if everyone follow your advice, then they will all be average.

If everyone follows my advice I will write a new column called "Being average means being awesome!!". *wink*

No amount of scrimping on coffee and gym memberships is going to make up for the cost of housing going up 150k year after year. You were either fortunate enough to catch that boat or you are screwed.

Passive income is a good of course, but that's going to come in realistic amounts by starting a business not squirrelling away a worthless salary and praying that returns are significantly above the rate of inflation.

Get a bunch (lets say 4) of your mates together, start a rental company into which you each put $30,000. with your company's $120,000 you could buy a property worth $400,000. This property would move with the market and prevent the market from running away from you. You'd gain 25% of the increases in the property's value, while you only need 10% or 20% as a deposit for your first house.

For example if you did the above and after 1 year the property went up by $150,000, your share of that equity would be 37,500. Add this to your initial 30,000 equity and you'd have 67,500 of equity or enough to buy a 337,500 house with a 20% deposit. After the second year ( assuming your 150,000 pa increases ) you'd have another 37,500 of equity (105,000 total), which would be enough to buy a 525,000 house. Note how the year 2 house is worth 187,500 more than the year 1 house, this shows that what you can afford goes up relative to the market (because of the leverage effect) and means that the market is no longer running away from you.

In the real world we would use % increases per anum instead of fixed dollar amount increases, but the same principles that I've elaborated on above would apply.

Leverage can be a powerful tool. It's a double edged sword though, watch out if the market goes the other way.

By purchasing as a group of 4 every individual would be shielded 75% from the effect of the drop in property value. Additionally other properties would then be within reach of your ordinary savings meaning that you can still become a homeowner ( very likely of the same house that you would have bought using leverage if property values were climbing) albeit the paper value of the house would be lower.

Talk about voodoo economics. If the house loses 50% of its value, you lose all of your share of the capital, if its still negative equity and you borrowed then the bank demands you make that up? Sure houses may now be cheaper but if your capital was wiped out in the first round you cant invest.

the same would happen if you purchased solo with a 20% deposit. buying in a group spreads the risk. The bank will generally allow you to keep the property as long as you continue to service the mortgage on time.

If you are looking to buy a house $30,000 is unlikely to be all of your capital. The relative value of cash assets goes up when property values go down, any remaining cash assets after the property price drop should be well positioned for purchasing a house if you are that way inclined.

Ordinary savings above should be read as cash or cash equivalent assets and investments.

Well sadr thats what is called 'Counting your chickens before.............' And very precisely.

If the market crashes then presumably no one would be moaning about the market prices of houses running away from them? If you are concerned about this eventuality then there is a powerful financial tool called hedging that you should look into. Hedging will generally come at an opportunity cost in the event that the market does move in your favor and is widely considered to be too complex for regular mom and dad investors.

I disagree re "not squirrelling away a worthless salary". Remember it comes down to what you spend. And if your salary is $500k and you need $250k it will take you the same time as someone who needs $25k and earns $50k. No salary is worthless, unless you need more than that to get by... then you're positively screwed. It comes down to the percentage of income that you can save.

The pennies are as important as the pounds. :)

There are lots of really nice parts of the country that haven't experienced such great capital gains. Its not like that everywhere.

Great article Elizabeth. I guess what I took from it is that one has to establish an edge. And the earlier the better. An example of edge would be doubling ones mortgage repayments. Or running Kiwisaver at 20% contributions. Challenging as those things are to do, without such an edge one is doomed to average and that isn't viable.

Precisely.

yes if you are capable and have the opportunity, discipline and awareness, although most people simply do not have this. This whole thread is worthwhile to the capable in this context...who usually are not average. In the current environment, the average have been doomed for at least the past ten years starting out in NZ.

"Elizabeth Kerr says 'average' is a moving baseline and if you aim for that you'll end up in the poor house"

.

This is not how the world is supposed to be. people should be able to live (without al the trappings of the rich, just LIVE) without having to work your fingers to the bone, without having to turn every cent 3 times.

Whatever happened to a dry, warm house, plenty of healthy food to eat, enough time to relax to enjoy your family and friends?

What kind of world have created, have we allowed to come into being, where in order to not end up in the poor house we have to live by rules like the ones set out in this article?

I hear you. But if a warm dry house and health food and other non-negotiables were the only things people spent their money on then everything would be a-o-k. In order to stay out of the poor house don't spend without knowing the consequences.

I don't think you do hear me, really.

Then try me again.... Your point of view is important too.

@DFTBA, are you saying that it would be preferable if we didn't have to go without what have become almost the 'necessacities', ie sky tv, iPhones, lattes, modern cars, big houses in order to be able to afford a reasonable retirement.

Thank you Elizabeth for the great arcitle again. This is the first time I post a comment, but I have been following your article and advice since April. I cancelled my gym (970$ a year), stopped having coffee and lunch out (15$ a day) and cook and bring my own lunch to work. I cut down on other spending like movies, buying clothes, eating out and buying lotto (managed to save 70$ something a week!). At the end of October, I magically find myself nearly 4000$ richer. I am so excited to find new ways to cut waste further, like reducing waste in food, cooking in bulk, walking more to reduce bus cost and switching to a power supplier with lower rate. I'm in my early 30s. If I keep doing this, I will be able to save 10,000+ more each year, cut my mortgage free age by at least 10 years, and have my money machine set up long before retirement age. I am so grateful. You're right, if everyone follows your advice, then the average will be awesome!

That is AMAZING!! You are awesome!!! Its exciting isn't it?? Cutting your mortgage by 10 years is EPIC!! Stay tuned for next weeks column and there will be a little something for you :)

Great topic EK. Have so many thoughts on your post and the related comments.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.