ASB's own economists might be predicting house prices will fall next year but according to the bank's latest Housing Confidence Survey, the public largely disagrees with them.

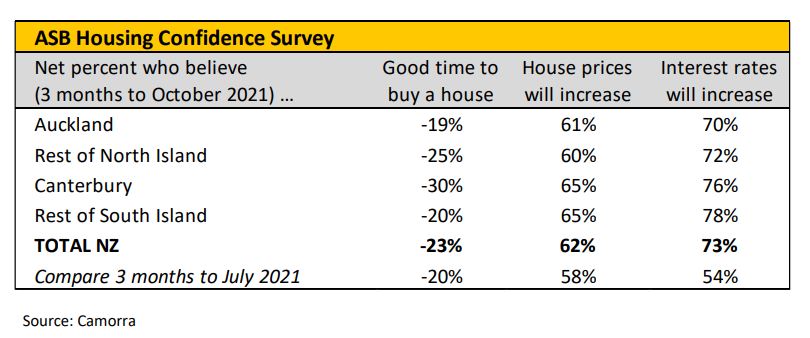

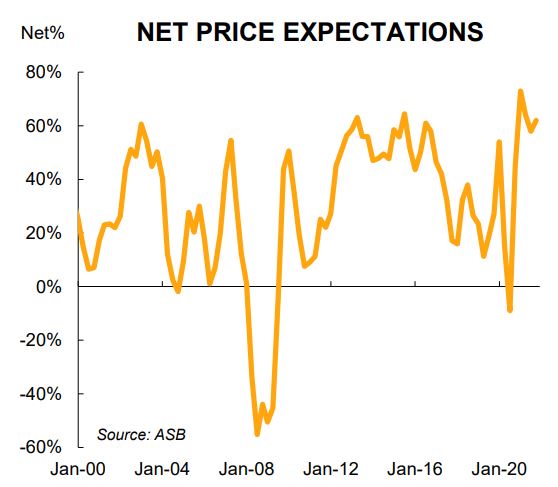

The survey, for the three months to October, shows a net 62% of respondents expect house prices to rise over the coming 12 months. That's up from 58% in the previous quarter. ASB is New Zealand's second biggest residential mortgage lender with nearly $69 billion of home loans at September 30.

"Kiwis’ housing confidence has remained stratospheric all year. Credit rationing, tax changes, lockdowns…nothing has shaken the public’s confidence that house prices are going to keep rising. And so far they’ve been right. But now that mortgage rates are rising, and fast, are we approaching the housing market’s Wile E. Coyote moment? Not according to our survey," ASB Senior Economist Mike Jones says.

The net 62% is derived from 68% expecting prices to increase, 6% expecting a decrease, and 18% expecting prices to stay the same.

Jones points out it’s not as if the survey respondents are in the dark when it comes to rising interest rates. A net 73% of them expect interest rates to rise over the next 12 months, with 75% expecting rates to increase and 2% expecting a decrease.

"That’s about as close to universal agreement as you get, being the second highest result in the 25 years of our survey," says Jones.

"Back in October 2004, a net 75% of folk expected interest rates to rise. Incidentally, they were bang on; the two-year fixed mortgage rate rose to a peak of 9.63% over the subsequent 3½ years. We don’t expect a peak anywhere near that high this time around."

"But we reckon the speed of recent lifts in mortgage rates, and the prospect of more to come, will finally put the kibosh on the feverish housing demand we’ve seen ever since Lockdown 1.0. In fact, there’s a growing risk that three big macro negatives show up at the same time next year [higher mortgage rates, tighter credit conditions and better housing supply]. Lofty housing confidence looks set to be tested," says Jones.

Jones himself last week predicted "small falls" in house prices over the second half of 2022. He's forecasting a "cumulative forecast fall of around 4%." Albeit Jones says that should be interpreted "more as a hat-tip to the risk profile than a precise point forecast," and follows a 35% to 40% surge in house prices since March 2020.

In terms of what the survey results say about the rising mortgage rate picture, Jones says the overriding message seems to be that the housing market can handle it.

"Still, it’s all making for a particularly bitter cocktail for those looking to buy. And, indeed, buyer sentiment continued to crumble in the three months to October. A net 23% of respondents now believe it’s a bad time to buy a house, a further deterioration from last quarter’s net 21%, and the lowest in five years."

Jones questions whether there's a risk of overconfidence about house prices.

"We’d be remiss not to flag a few big speedbumps we see in the distance. The Reserve Bank is no longer content to let the good times roll, and we’ve long pegged 2022 as the year we finally get some movement on the housing supply imbalance. In the least, 2022 looks like a year in which lofty housing confidence will be tested," he says.

Jones suggests there's "a good chance" the recent surge in mortgage rates ends up "rattling housing confidence a little."

In terms of buyer sentiment, Jones says: "Wildly-stretched house prices paired with steep rises in mortgage rates are not a palatable combination for home buyers."

Breaking down the buying sentiment response, Jones says just 9% of respondents think it’s a good time to buy, while 32% of people think it’s a bad time. Meanwhile, 50% think it’s neither and 10% don’t know.

"Buyer sentiment is particularly negative in Canterbury, with a net 30% believing it’s a bad time to buy there. This compares to a net 20% in the rest of the South Island, a net 25% in the North Island outside of Auckland, and a net 19% believing it’s a bad time to buy in Auckland," says Jones.

"Perceptions of whether it’s a good time to buy are now within a whisker of the all-time low struck in October 2016. We wouldn’t be surprised to see fresh lows before this cycle is done. We suspect the house price upswing has got another six months or so left to run, and the upward pressure on mortgage rates looks likely to remain."

ASB says the latest iteration of its Housing Confidence Survey stems from data received from 2814 individual respondents.

Housing confidence

Select chart tabs

112 Comments

By 2017 (&before) standards interest rates are still very low.

So house prices are likely to stay steady and maintain their elevated price levels. Especially in regional cities as more Aucklanders leave permanently and the borders reopen.

As has been noted here (and elsewhere) numerous times in the past, house prices tend to be resilient in New Zealand.

TTP

Wrong.

Around 1979 (40 years ago) the residential property prices dropped. I know because my father talked me into going in with him to build 3 x home units ('specs') and the market imploded and we lost our shirts.

Also, during the Great Depression of the 1930s Mt Eden was awash with empty villas and bungalows. My mother, her sister and parents were then renting a property at 4 Cromwell St Mt Eden (the bungalow now or was recently owned by Helen Clarke). At one stage most of the houses in the street were abandoned. (Incidently, my mother will be 98 yrs old this Friday.) You could dismiss this as a 100 yr event; well,100 yrs is not too far away.

The advice to be drawn is not to base your property price predictions on too short a period or cycle. Cycles of 20 years or 30yrs or40yrs are too short to draw predictions.

OMG this is too funny (unless you're being sarcastic but I think you're actually serious?). How much missed opportunity has it cost you to base your prediction of house prices will tumble and being wrong fon "only 30 years", 30 yea!!! It's a very long time, and an immense missed opportunity

I think you've completely missed his point.

Japanese house prices are still less than half what they were in 1990. If you'd held on in Japan for the past 30 years you would have lost your shirt and the opportunity cost of all the other investments you've missed will have been great. While NZ's experience with housing over the past 50 years has been one of an increasing trend, there comes a point at which valuations are too far removed from reality. At that point you are then in "Japan" territory and there are no guarantees that holding on and waiting will see you get out of the hole. The only question is exactly where is that point? Are we there yet, or do we need to see another 20%, 50%, 100% or 200% appreciation?

So ? We're not living in Japan...

"Back in the old days… when great grandma got her first telephone, house prices did drop, therefore I will conclude that buying a house is a bad idea"

Wrong as an example. The value of a home on paper in a banks eyes can be easily ignored, (even massive drops still did not destroy the home or force foreclosures to widespread homelessness) or survived, (most could easily get finance or hold more debt than the previous generation before them), but you still need to live in a home somewhere so the inherent property value of that home, (& it's effect on your physical health to be housed), and that value relative to the demand of buyers, & population needing to be housed, remain and actually increased in that period according to rising population rates back then. You would need to go back further to when the population dropped severely say in levels similar to the black death outbreak. Where the inherent value in a home was not as high as it once was. Could be far less people were actually living in most areas anymore. Housing was far less of a valuable thing compared to other more basic needs.

I know. You've heard all this before. Many times from me!

All bubbles share common characteristics. During the euphoric expansion, participants are richly rewarded...The common characteristic when bubbles pop is the eventual bottom is far lower than anyone believes possible. This confidence in the bubble's permanence permeates the entire system and encourages a faith that 'buying every dip' will continue to be the road to easy wealth. ...When euphoric risk-on switches polarity to risk-off, buying every dip becomes the road to ruin as the eventual bottom is incomprehensibly lower...History is full of examples of 80% declines, 90%, 95% and yes, 99% declines. No one predicts the eventual capitulation low because such declines are inconceivable. Any decline could not possibly be more than three or four correction; a nightmarish fall into a chasm can not even be imagined....

And so here we are, witnessing the switch from risk-on to risk-off in real time. (CH Smith)

and when do you expect this 80 to 90% drop in houses prices to occur bw?

It doesn't really matter to me, as long as you know it's not going to?

“I don’t know when, but when it starts, I’ll know”.

I promise you, buyers in Tokyo in 1987 didn't buy then because they thought that 90% of their investment would evaporate with 2 years.

Well worth a read (it's dated) but as a reminder of how messed up 'things' are.

Financialisation must be paid for, it's not free and results in an ever-increasing polarisation of the population from those with assets to those without. The debt path is easiest to sell to the populace and fund current lifestyles, until it’s not. The vast majority of us are the proverbial turkeys being fattened and waiting for Christmas, happy with the status quo and delusional to the true state of affairs, so down that path we go.

https://www.macrobusiness.com.au/2018/04/deep-t-explores-end-australian…

Well bw, I think timing does indeed matter because at some stage in the future house prices will definitely go down and at some stage in the future they will also definitely go up. How much have the younger generation who did not buy a house 3, 5, 10 years ago in anticipation of a price drop, missed out on?

Some just don't have a choice they just can't afford, when celery, cucumbers and yoghurt cost 6 bucks, milk and bread cost a fortune, not to mention rent is 500 bucks ish. Where do these young people get enough to save money for a 20% deposit for a $900,000 home. Now if they have kids, might have to live in the garage at the parents.

Labour, National and Orr have a lot to answer for.

All this money hundreds of billions with which we have bought now are to be realized in the future. That's the basis of banking industry.

The houses has been bought with money that doesn't exist. The money is created when people work hard and they do something which helps the people around them.

Really who's working hard in NZ? Look around.

I might be very very wrong but all this going on doesn't seem very right to me.

Plenty working hard I assure you, ask the nursing staff getting spat on daily by meth riddle covid patients. That said there are just as many that are not. One of the main reasons the hard workers bought investment housing was for the tax rinsing effect. If you work hard, took on debt via investments, it was easy to be ho-hum about Government activity because you were rinsing your income tax into property equity. It does become a real big problem when everyone is doing it, and the entry point (price point) for any house became so artificially high. So high, that many of the future hard working tax payers voted with their feet and move to places like Queensland and Perth.

Other than the Banks, not sure who the winner was here. NZ society sure took a nose dive because of this.

Funny most those nursing staff working the hardest cannot afford housing and often cannot even afford to save for investments because their wages have been forced down to be worth less than they previously did. Could be all those who crow about gains in property being from working hard are are actually driving the massive inequality in housing & the corresponding nursing crisis when nurses who often are the hardest workers, facing some of the largest health risks, cannot even get into rentals that house their families. Many nurses being brought in from overseas often despair about how hard it is to find basic affordable housing or indeed any housing for their families where they are working. It is curious why we bother training nurses in NZ at all anymore when the best thing for them to do for their future family is to leave the country at the first opportunity to save enough money for a home with more rational wage, house cost ratios.

We don't need nurses and doctors, the property gods will provide, it solves everything.

Sometimes I wonder if people confuse "survey" with "vote" and choose the outcome they would like most, rather than the one they think is most likely.

Rates remain low, RBNZ has signalled only a slow ascent next year, government have showed little intent to use the fast track consent process (or other tools) to meaningfully pressure the market and you have border reopening applying more pressure through the first half of next year. Why wouldn't we expect house prices to continue their ascent?

Tax hikes to come, the billions of “covid funds” have to be paid for and there’s not a lot of investment to show for it

RBNZ has signalled a slow ascent next year. Of the OCR?

We've already seen several times in recent years that the banks will set rates as they need to.

The Madness of Crowds

If you are up to your eyeballs in debt with all your eggs in the housing bubble you probably are going to believe that the market will continue upward. Anything less doesn't bare thinking about.

Yes, mass delusion.

A small tweak to an Upton Sinclair quote springs to mind.

It was jaw dropping when a young family member dropped 1.2mil (1mil debt) on an old ratty 1960 property (sold for ~400k in 2016) in a poorly connected area with an oversubscribed public school quite a distance away and no public transport suitable to work or community areas, with less than 100k income and a second baby on the way... I would say NZ is quite screwed but that would be by far an understatement and the fallout across all families and community networks from the housing crisis is like a bad time trap with the explosion going off repeatedly and echoing through the generations to come (the intergenerational trauma issues created in NZ will be writ large).

Over the past 5 years I have been impressively consistent in my incorrect predictions about the NZ housing market. But undaunted, I am going to have another crack at it. Looking at the volumes coming into the Auction rooms (up to 60 in a session at B&T this week) and the increased passed in rate. I would be very surprised if the fall is only 4% from peak. I am going for between 10 and 20% reduction from the top of the market. A stopped clock is correct twice a day.

Likewise. You sound like me, except I predict a sturdier drop ;)

Meanwhile new builds stall.

Placing more price pressure on existing houses.

Many people are now hesitant signing a contract for a future build.

We keep hearing that new builds could suffer but where are you finding this data?

Facts please to corroborate assertion.

https://www.stuff.co.nz/national/126828936/unfinished-homes-as-severe-b…

here's one source pointing to house build difficulties

A 1 month old article with anecdotes?

The actual data suggests we are still building at record levels:

https://www.interest.co.nz/charts/real-estate/building-consents-residen…

-Record number of builds taking place

-Difficulty in getting skilled labour/supplies for new builds forcing projects to delay

It makes perfect sense that *both* of these things would be true at the same time, I don't know why you are disagreeing.

It is really funny you do not know that building consents do not keep up with immigration rates, investor demand and population growth.

You might as well start encouraging people to live under rocks for all the access to build there actually is. It is actually rarer than hens teeth when consents are compared to demand for properties not covered by the existing stock.

Look at Trade Me - many old houses recently purchased with "RC approved - "x" townhouses" are hitting the market. Especially in Central Auckland suburbs. Developers are seeing an over supply, rising costs and rising interest rates.

Speculators have held, and now looking to exit and take the development profit from the new zoning. Its called landbanking. Developments make money based based on cost inputs. Construction and materials are getting hammered by inflation. Can you afford to grossly overpay for the land...?

A 20% drop takes us all the way back to February values, ahh the good old days.

Haha

Only 5 years.

Amateur.

😁

I would be surprised if it drops at all, I hope it drops more than 50%, but I can only dream, (note I own properties), but I want the next generations to own them as well.

Even if it did drop 50% that would still be up on the value precovid. (Many properties have tripled since then thanks to someone feeding the investment bonfire and raising the development and land values)

Funny but very honest post Waikatome. Since you know that your predictions of price drops have been consistently wrong, would it not make sense to change your predictions?

I have never been able to accept that NZs gravity defying market can last for ever. I continue to be amazed as the prices keep increasing. It has to turn as some stage surely. But I have been wrong so far.

It won't last forever (I actually believe the bull run is ending now which will become apparent in 2022). But how much in lost opportunity has your refusal to accept that house prices will go up really cost you over the last 5 years… Sticking to one's prediction in the hope that one day you'll be correct is a very costly and bad strategy. It would be far better to be more open minded and think "well I've been wrong for 3 years, maybe I should change my opinion?"

Good on you for admitting you've been wrong, because of that it's likely you are right much of the time. No one anywhere has been right with predictions most of the time, even if some here think they have been 😀

and stop calling me Shirley...

If you already believed house prices were unsustainably high, how would a year of further crazy increases change your mind? Logically, this kind of rise can only make a crash more likely.

I guess it's no wonder why people think this way when the PM states:

Jacinda Ardern says 'sustained moderation' remains the Government's goal when it comes to house prices, as people 'expect' the value of their most valuable asset to keep rising

Our great leader has property owners backs...

https://www.interest.co.nz/property/108301/pm-jacinda-ardern-says-susta…

This would also suit Chris Luxon's property portfolio.

Thinking about it, Chris did say that he and JA have never met in person in Parliment. Could it be they are one and the same person?

National and Labour are looking more the same on housing policy, especially when they both agreed to the new high-density boundary rule removals.

Do you really trust her that she can keep backing property owners up? Who do you think she is? Xi No.2? She probably doesn't have a clue why there is an inflation right now...

She will probably notice inflation when she goes to her local coffee shop and the price of a Cafe latte has gone up 50 cents

"This level in price rise for my coffee is simply not sustainable"

lol, apparently not only 50 cents.

https://www.stuff.co.nz/life-style/food-drink/drinks/127196374/we-need-…

Not likely the NZ public picks up her tab in most places, even post employment she still reaps the benefits from NZ taxpayers.

I currently reside in what would be described as a low socioeconomic part of West Auckland. Quite scenic with the high voltage power lines everywhere.

Across the road there are 63sqm 1 bedroom plus study shoeboxes being built and sold off the plan for 810k apiece. 14 of them rammed like sardines into where there used to be two 1980s weatherboard houses on very modest sections. A bus comes down this road once an hour. The only real culture is listening to "stickman" ads and watching obese people waddle around the local Pak n Save.

A year ago I was living in Southwark Borough, London. It was ten minutes by bike from my front door to London Bridge or Westminster. Five minutes walk to a Zone 1/2 tube station. And you can spend less per square meter there, in the cultural and economic centre of the world than you can in a far flung butthole of West Auckland.

Anyone paying these prices has rocks in their head. It's a monstrous and completely unjustified bubble.

This clown show housing market is an accident just waiting to happen.

Beautiful imagery - thanks.

Yes, Good Lord, what a farce.

Perhaps I should move somewhere cheaper like London? I have a Brit passport, and, more importantly, a vaxx passport.

NZ - the penal colony without a fence. Just a big moat and an inability to travel - anywhere.

Not quite the image sold overseas.

Well written Brock...I have shared this it's so good.

We can travel very easily, but hard to come back in. Opposite of Hotel California in a way lol!

Nicely put Brock. The building approach at the moment is atrocious. If builders were compelled to consider multi-story on larger foot prints (see 1970 blocks in Putney for an example) both the quality of living and green space would be better.

While it is all quite, quite, mad a very small defence of the approach is that while you may have a rabbit hatch in a depressed area at least it would yours. You are unlikely to ever be able to own a house in London as most of them are lease-hold only.

I cannot see what holds people here other than the fear of the unknown or an inability to get a work-visa.

Putney is a bit more expensive, but very nice and leafy. Loved living down there. Over the hill in Roehampton is grim though.

The leasehold thing is a good point, but when the lease is 999 years it doesn't really matter either. It's also usually possible to buy out the lease.

The right to buyout the leasehold has been in UK law since 1967, further reformed in 2002. Cost about the same as renewing it - normally a few thousands pounds.

Unfortunately for some not how it works here. Probably less here as a percentage as well.

Nice Brock but something is not right. if things were so great in the UK, why did you return ? How did you wind up in West Auckland ? I presume your in the likes of Massey ? Things don't make sense. I have a UK passport, was born over there but no way I would go back. Its a 2 second calculation in my head, my lifestyle is way better in NZ than it would have ever been in the UK.

Hi Carlos69,

We returned because we mistakenly believed that Auckland would be a better place to raise our growing family and it would be nice to be able to have grandparents and relatives nearby. When we booked our flights home Auckland was also 40% less expensive than present.

West Auckland is where I'm originally from and it's where an opportunity for temporary accommodation came up through friends and family.

Cool. Now imagine what your lifestyle would be if you were buying into the 2021 Auckland property bubble. Even with the handouts that you got I reckon you'd be a renting for life.

Anyway, we are now leaving for Australia. Life is too short and we can do much better. Add up now?

Good on you Brock. Your money will obviously go much further in Brisbane, and you are only a 3 hour or so flight away to relatives here.

I suspect there will be many more like you.

Also I read a piece in the weekend about a mini exodus out of Auckland to places like Christchurch.

Ham real estate agents are also expecting greater interest when the Auck zoo opens. The roads out will look like boxing day at the mall.

Carlos69 hahahaha. Brock, never change mate. I love reading your posts. Full of humour and more often that not, bang on the money.

So basically a string of mistakes. I guess you have to stop and wonder how things would have been different with a string of different decisions. When you get to 50 you realize where you got to in the present was a diary of life's decisions. You will always have a few regrets, but hopefully not many.

String? Oh no, just the one, moving back. And reconnecting with family isn't a total write-off.

If you aren't making mistakes in life you aren't really trying. The key is to fail fast and learn from them.

Feeling pretty positive about the more exciting future ahead.

Brisbane is great and the schools are epic. This will be a great choice Brock well done. Also look to buy soon as Australia is about to go on a bit of a tear (grain replacing Iron, Lithium and Tin being the new gold(s)) so even if there is a global turn down the sun will still shine.

I am jealous just a little but wish you all the best.

I've already bought some land down on the coast. Building next year.

Yeah Brizzy is great.

People often forget it's a fair bit bigger than Auckland, so it's not at all a move to a hicksville of an Aussie city.

Congratulations on finding somewhere. I got to admit I really dislike the UK to live, visitings cool though, love the pubs, had some very good friends. But each to their own.

I love NZ even with outrageous House prices but I'm from a small town, 1 hours drive from Auckland, great community, good fishing, surfing, starting a home brew club to drink from friends garages. Its the community thing I like, and the country scenery with the beaches. We are setting up a business which should take care of us, which will also allow us to travel back to UK and visit.

Anyway best of luck, nice to see fellow kiwis who care about others, least not all is lost for us.

Ohh Brock.. You seem to be talking sense in this country of sheeple.

There is no justification to stupidity going on here. The free money printing is a good job which the government in power is doing and everyone wants more of it.

So the ponzi will go on and on. Why complain, just join the bandwagon and make millions along the way. So many are making them and no paying a cent in taxes.

They all want silk coffns to be buried in.

So BL, why are you living in Auckland and not in London?

Hi Yves,

Second baby arrived earlier this year. Came home for family. Now moving to Australia.

Would love to move back to London too.

Who's "Yves" ?

Some guy I vaguely recall made a big deal about quitting. Only to return a short time later.

Welcome back.

Yves as in 'Yve-vil' - get it?

Man, you seem to have zilch in the way of empathy or humanity. It's all about the $$$ right?

I totally get Brock's position.

Pandemic hits, mass economic carnage. Logical to come back to his home country with his family.

Then gets caught in the storm of a tearaway housing market, with prices rising 40% in a year or so.

What don't you get Yves?

Do you understand that it's extremely hard for households on even upper middle incomes to buy now?

Is that somehow their fault and responsibility??? That's how you portray it, consistently.

You were lucky to come to NZ as an immigrant way back when housing was affordable.

Just ignore him HM, clearly a bot developed by the Real Estate industry to keep the party going and convince us all that we are stupid if we don’t own at least 5 investment properties. Robots don’t have empathy or compassion unfortunately.

Bummer I've been found out, I'm a bot, LOL

Nah he's just some Swiss dude that thinks that because he accumulated a few properties from the 1990s onwards, when property was actually really affordable here, that he's somehow some sort of financial genius.

He's also indoctrinated in the ways of Kiyosaki, and seems to believe the rubbish that the path to financial freedom is down to YOU as an individual.

So, you know, if you are two school teachers on 150k total, you shouldn't be teachers (hey who needs them?!) or you should work two jobs, or you should live on the street and eat baked beans to save that deposit for your first (of many!) Properties.

Anything is possible in this cult-like Kiyosaki/ Yvil world, if you don't own multiple properties then you only have yourself to blame!!!

Just like if you don't get good things in life it's because you aren't praying enough!!!

(All a Load of garbage of course)

HM, I indeed believe that, if we are born in a first world country, we are responsible for our own lives and that we are where we are today as a result of the decisions we made yesterday, last week, last moth, last year

Hilariously in NZ we are not blessed with choice. When youth are selected by genetics and denied basic education and then denied employment many people very much did not get to choose to pick different genetics at birth. Try being one of those with a condition with a death rate in the early twenties and then come back crowing about how well you did at property... although the medical system decided to cut a hole into your body which went septic when medical wound care was also cut back.

Choice and opportunity is a function of socioeconomic advantage, genetic lottery, country medical systems and human bias. Yours is quite clearly not advanced enough to see past yourself. Try thinking like someone who has a different genetics and family to yours. Your family wealth is not just measured in collective attitudes at the time heavily benefiting your success but also that you relied on the success of others more than any work you ever did yourself. You relied on human bias and discrimination and have benefited from it. It does not make you better but your attitude of it only being choice does make you more morally destitute. If humans had choice who would choose to die young? Or be born or made disabled by the country laws? Or to be shot dead for walking in their community? Or to be denied employment on the basis of skin colour & age? It is easy to see where it is not their choice but the choices of others that have shaped the path for them.

So I have zero empathy because I ask BL why he's living in Auckland and not in London after he posts how much better London is. How did you come to this conclusion, weird

No people say you have zero empathy because you not only demonstrate none in your comments you are actually advocating almost pathological sadism in them as well, a negative empathy. It is quite curious that you also seem to think that advantages you with being more morally and ethically superior yet demonstrate a negative quantity of those two things, a narcissism that is pervasive and destructive. If anything these features can open anyone up to more risk as they fail to recognize the collective keys to their success, build the resilience of their network and defend against growing threats that develop as the collective fractures and disintegrates. It would be weird to not see that. Even antagonists need to understand the buttons they push to be trolls, but to not even see the buttons at all... hmm the last time I saw such was with those who had neural pathways severely changed through trauma and they would respond with what the brain injury clinic terms self centered view with a complete lack of thought about other people, high impulse and complete lack of empathy. For some it can be such a sudden change to their behaviour that it breaks relationships, ties and leads them into criminal behaviour. Again the risks part is that a demonstration of a severe lack of understanding of what other people need, provide and feel can harm long term outcomes particularly when the nursing home you will depend on cannot staff anyone so they cut basic living services and emergency support. Like it or not you do depend on others for everything you do and receive. You depend on them to live. There are no humans in this world now that are completely isolated of other human actions.

Marijuana or magic mushrooms?

yep, zero empathy confirmed.

Indeed! Interest's motto is "Helping you make financial decisions" it's not "helping you feel sorry for a total stranger"

Yes, I can read thanks. What is your motto? Let them eat cake?

No wonder people are flocking to Kiwibuild's. 1br terraced house should be no more than 600k. 810k is just crazy but somehow they are still selling

Something about tulips...

When jitters do finally appear I have no doubt the opening of floodgates will fix the problem 3x over.

Everything will be just fine when New Zealand goes Full Retard and reaches it's 'The New Colossus' moment:

Give me your tired, your poor,

Your huddled masses yearning to breathe free,

The wretched refuse of your teeming shore.

Send these, the homeless, tempest-tost to me,

I lift my lamp beside the golden door!

The market is definitely changing. Hardly anyone at the open homes I attended this weekend on the North Shore (Birkdale, Beach Haven, Birkenhead). Still very high price expectations of many vendors, but some more realistic. Lots of houses coming onto the market - many rentals, and lots of rubbish. Many houses are being passed in at auction. I’m not in a hurry to buy as it looks like there will be plenty to choose from next year.

Noticing the same. We just sold our place, had 5 people show up across 2 open homes. 12 months ago you'd easily show up to an open home with a minimum of 10 other groups, and as you leave more arriving.

This is in Masterton. The place we are selling is a very short stroll to a train station, regular commuter service into Wellington.

Hmm I remember us discussing the purchase of the house you just sold, your first home, where next for you NZDan?

We're moving into our dream home. A central location, 1930's 4 bedroom 2 bathroom villa on 1/4 Acre.

Congratulations, nice to hear.

Same here in Napier. I keep an eye on the local real estate market and properties in my area which were attracting 10 - 20 people at some open homes now get 1 or 2 cars turn up and that's it.

Until and unless the law of the land uses their grey matter and makes policies which help each and every person, this inequality will keep on increasing. We are treating country as a privately listed corporation where we have to expect profits every quarter.

This is a very wrong concept which is causing inequality.

But then who cares guys.. Keep buying from each other and beat your fellow kiwi at the auction. You be the winner. You make mansions and enjoy the money when you are old.

You will die with hands full of cash. Sorry but you can't take any into the grave with you.. That's not allowed.

https://thekaka.substack.com/p/please-crash-this-housing-market?token=e…

House Price fall - impossible as Jacinda Arden will lose power and all manipulation that Mr Orr has done will haunt him and can escape as long as the ponzi continue.

So come what may - house prices will never fall in NZ as now housing is not the only economy but represent NZ itself.

Well said Taimaiakka. " house prices will never fall in NZ as now housing is not the only economy but represent NZ itself. "

There is too much that is dependent on the property market, apart from the obvious - Politicians/ law makers are some of the biggest investors in the market.

My opinion, property market will come to a float for awhile, but as far as any significant drop in prices, wishful thinking.

If your thinking you better sell now because the prices are going to drop, best you think again.

As much as it pains me, you are correct

Unless the Govt wants ongoing rampant hyper inflation (already underway) they have no choice but to assist forcing a reset. Hyperinflation stuff's everyone while a reset just hits the banks and speculators and unfortunatetly recent FHB'ers. I would drop accommodation supplements, and recycle some of it into subsidise recent FHB'ers. The rest could go into keeping nurses, teachers, police and doctors in NZ.

Like Mr Orr who was wrong when he parroted that Inflation is Transitory, Is Prime Minister of the Country - Jacinda Arden wrong when she said that No Kiwi wants the house price to fall

https://www.newshub.co.nz/home/new-zealand/2021/12/nearly-50-percent-of…

Will they both come out in open and admit that they were wrong as cannot hide behind the excuse that were misinformed as everyone was highlighting them except people who were enjoying the benefit of ponzi scheme.

How long can they hide behind Covid19....till they come up with bigger lie to suit their narrative.

Next election, who can reduce bank profit and speculator gains the most. Clearly wont be a Nat policy.

Is ASB now worried that they are currently in a position betting against the market?

What would the exposure be for a bank that is more pessimistic than the sheeple?

I guess they could tighten lending too much (to reduce risk) and lose Ponzi share?

House prices in NZ will not drop more than 10% from the current levels ever again. If you are waiting for a big correction you will be waiting forever. NZ property is incredibly resilient and will only go up. It is also sponsored by the government so is only upside and a risk free investment.

Furthermore, the NZ Government is an all-powerful institution of omnipotent, multi-dimensional beings able to exploit and control global forces far greater than are currently at work.

This could be your last chance.

Be quick!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.