Home ownership became even less attainable for first home buyers in November, as prices at the bottom end of the housing market continued to climb further out of reach for young people on average pay rates.

In fact home ownership is now the most unaffordable it has been since interest.co.nz started compiling its Home Loan Affordability Reports in January 2004.

The heart of the problem is that house prices are continuing to increase at a greater rate than incomes, and that problem is now becoming so severe that it is increasingly pushing home ownership out of reach for people not just on low wages, but on average wages as well.

And the problem is no longer just an Auckland one, it is spreading to other parts of the country as well, with little relief in sight.

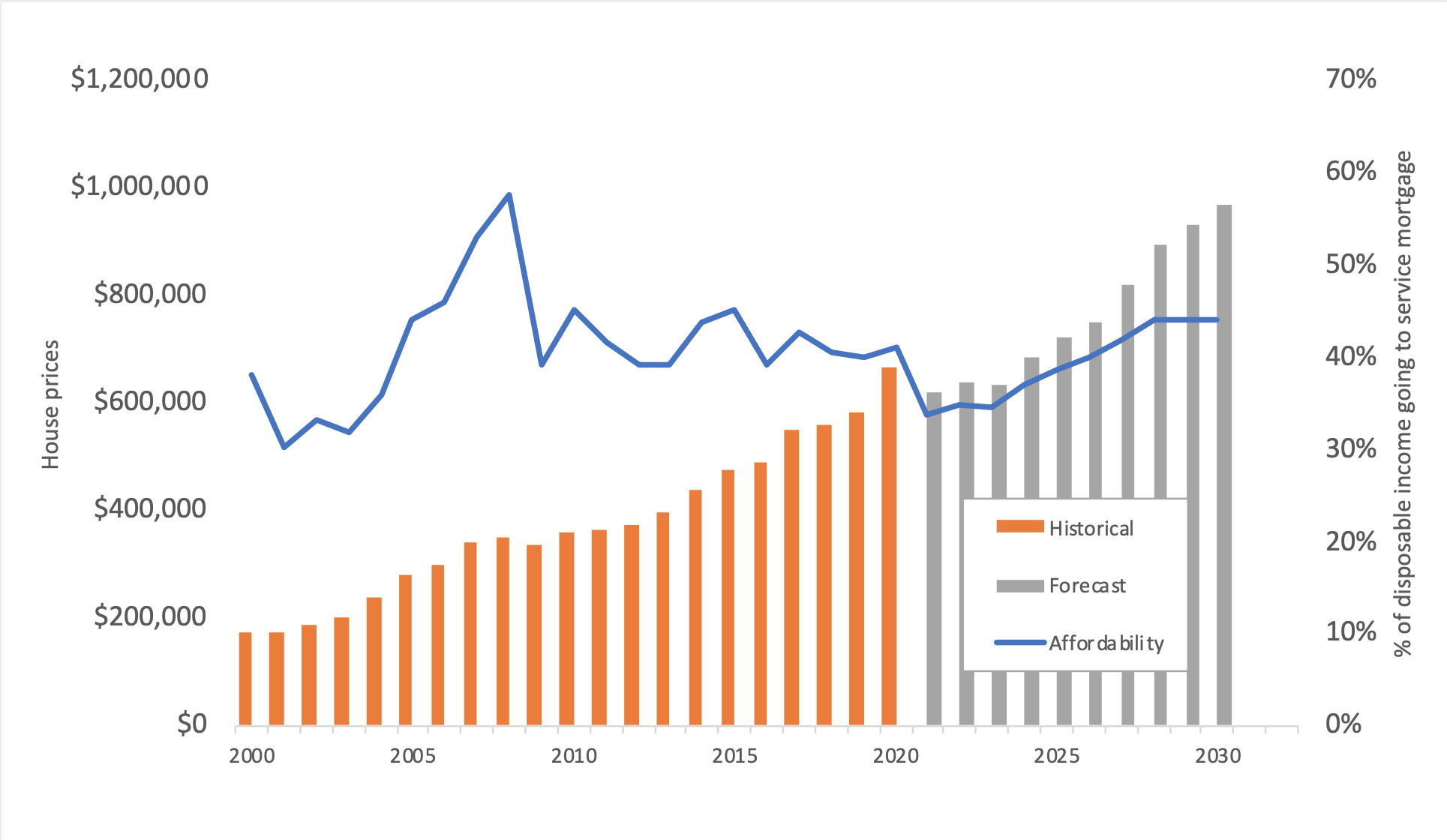

The Real Estate Institute of New Zealand’s national lower quartile selling price increased by $20,000 in November, rising from $650,000 in October to $670,000 in November.

In Auckland the lower quartile price continued its climb towards the million dollar mark, rising from $930,000 in October to $970,000 in November, a $40,000 increase in a month.

The lower quartile price is the price point at which 25% of sales would be below and 75% would be above, representing the most affordable end of the housing market.

House prices rising much faster than wages

The problem facing prospective first home buyers is that house prices have risen much faster than wages over the last few years, pushing the amount needed for a deposit or to meet the mortgage payments on a lower quartile-priced home into unaffordable territory for those on average wages.

Over the last two years the national lower quartile selling price has increased by $220,000, from $450,000 in November 2019 to $670,000 in November this year.

In Auckland the lower quartile price has risen by $275,000 over the same period, from $695,000 in November 2019 to $970,000 in November this year.

That in turn has pushed up the amount required for a 10% deposit on a home at the national lower quartile price from $45,000 to $67,000 over the two year period and you can double those figures for a 20% deposit.

It has also pushed the amount needed to be borrowed for a 90% mortgage from $405,000 to $603,000.

The effect that has had on first home buyers has been complicated by movements in mortgage interest rates.

Initially, over the period from November 2019 to August 2020, the effects of the higher house prices and the resulting bigger mortgages needed to buy them were largely offset by falling interest rates, which meant although first home buyers would have needed to borrow more to get into their own home, there was very little change in mortgage payments over that period.

But from September 2020, lower quartile house prices started increasing faster than interest rates were falling and this started having a dramatic impact on mortgage payments.

That situation was made worse when mortgage interest rates started rising from the middle of this year.

The average of the two year fixed mortgage rates charged by the major banks bottomed out at 2.52% in May this year and has increased in every month since, hitting 4.08% in November.

Up, up and away

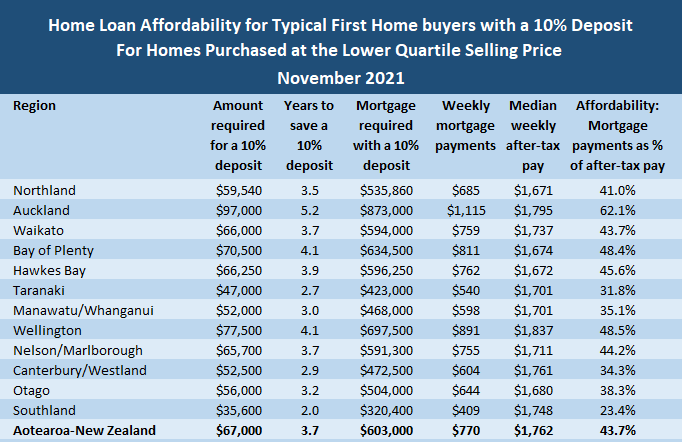

The net result of all this on prospective first home buyers is that over the last two years the national lower quartile selling price has increased from $450,000 to $670,000. This has pushed up the amount required for a 10% deposit from $45,000 to $67,000, and the size of a 90% mortgage from $405.000 to $603,000.

After allowing for changes in interest rates, the amount needed to be set aside for the mortgage payments on that would have risen from around $483 a week in November 2019 to $770 a week in November 2021.

That’s an increase of $287 a week, up 59% in the last two years.

Unfortunately interest.co.nz estimates that the combined after-tax wages for typical first home buying couples have only risen by $69 a week (+4.1%) over the same period, based on the median rates of pay for 25-29 year olds and assuming both are working full time.

So the percentage of their weekly pay packets that would have to go towards their mortgage payments would have gone from 28.5% in November 2019 to 43.7% in November 2021.

That’s a worry because mortgage payments are considered unaffordable if they take up more than 40% of take home pay.

The problem is particularly acute in Auckland, where the amount required to service a 90% mortgage has increased from 43.2% of take home pay in November 2019 (already unaffordable) to an excruciating 62.1% in November this year.

That effectively rules out home ownership in Auckland for all but the highly paid.

Using the same measures, home ownership would also now be considered unaffordable for typical first home buyers on average rates of pay in Northland, Waikato, Bay of Plenty, Hawke’s Bay, the Wellington Region and Nelson/Marlborough.

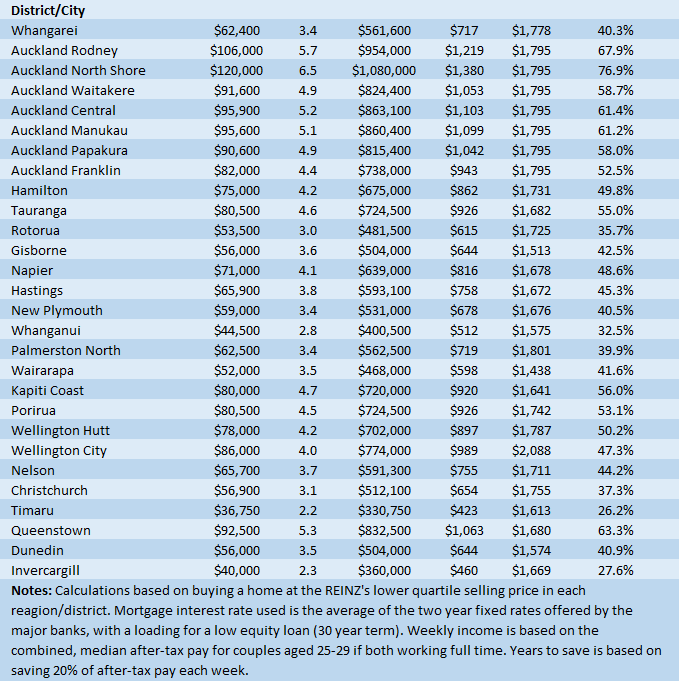

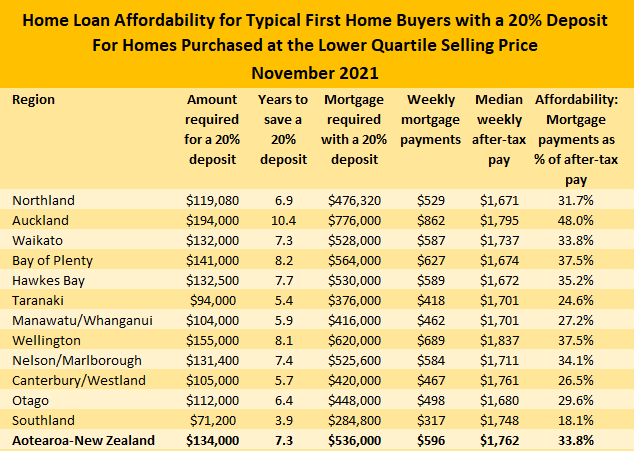

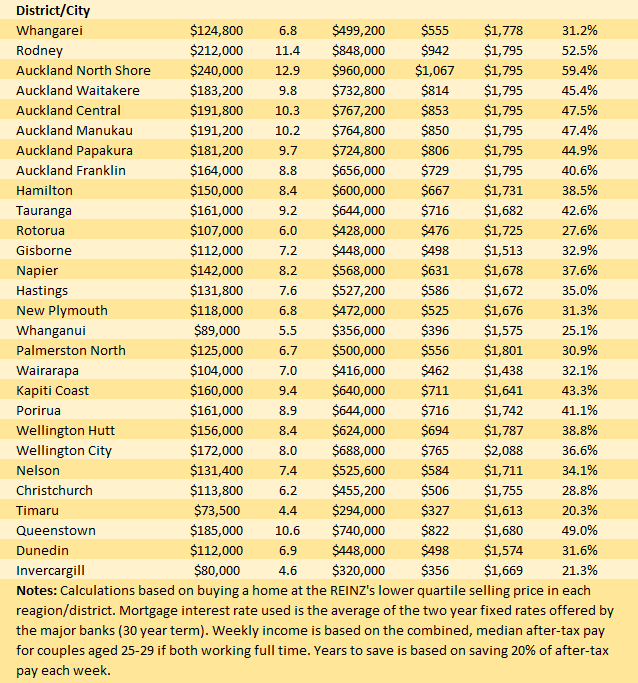

The tables below give the main affordability measures for all major urban districts, with either a 10% or 20% deposit.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

154 Comments

The final straw that saw me dragged away from drinks last night? The 50 something y.o. woman who proudly told us "I've found a loophole. I'm getting the (2) kids to withdraw their Kiwisaver and getting them to buy their first home with me, so we can all share the profits!"

I got as far as forming my lips to ask a question, and apparently it was time to go....

Only in New Zealand would they do something so mind bogglingly braindead as allowing retirement savings to be capitalized into house prices.

Your anecdote sounds like a keeper for the tales of peak bubble.

It was so much more than that though. It was a John Key trick. Allowing people to use thrier own money to bribe themselves to vote for National, brilliant. When point out that's what was happening the supporters at the time would head off on a great anti labour, can't tell us what to do with our money, rant. Great shot in the arm for house prices too.

Yeah, at least it enabled older asset owners to receive higher prices! Great we could consume yet more of the younger generations' wealth.

As always redcows, house prices balloon outrageously under Labour Governments. Just a lazy 70%+ under this one. So, would you consider that to be a bribe? But still, the biggest whiners about house prices continue to vote Labour. They get what they deserve.

Only in NZ, Australia (FHSSS) , UK (Lisa) , Canada (HBP) and no doubt many more. But don't let facts get in the way of a good rant eh Brock.

Australia FHSSS is capped at $30k and the funds must be contributed into a separate fund.

UK Lifetime ISA has nothing to do with retirement funds or pensions.

Canada HBP is capped at $35k and the funds must be repaid.

They are all retirement savings vehicles and allow you to capitalise into housing.

To a very limited degree.

That lifetime ISA is worth £1000 a year of benefit lol.

This kind of stuff to me, I find really sad.

Complete lack of ability to see the bigger picture. All our spare cash going to ever increasing house costs, how many 20 to 40 somethings are actually, meaningfully (diverse) investing for retirement?

You add stuff like this, to things like nz has a declining population without migration (who can afford kids when two full-time salaries are needed to pay a mortgage).

These are signs that our society, if not broken, needs a makeover. A lot of people here will label it dgm, but We need a housing crash to reset this mess and our collective attitudes. A little blood right now would go a long way..

There's even less chance of people saving for a retirement if they end up underwater on a mortgage.

But things are so insane that a 25% drop only takes us back to 2019 levels.

I get we could spill blood now for the sake of the future, but after years of being told to suck it up and that it's just how it is, followed by a huge political policy failure like Kiwibuild, and having finally gotten into a home, I fail to see how it is equitable that it be my blood.

New Zealand is not an equitable country.

Under Labour it’s easy. House prices of their parents house/s will keep going up and up and that will fund a great retirement when their parents fall off the perch. It’s even better if they put their KiwiSaver into a house and pay it off by the time they retire. For us we will also buy a house each for our two Grandsons

My wife and I have bought and sold 10 residential properties over the years, some before the '87 crash, some before the '08 GFC.

Every time we had people saying "Don't buy. Bad time." in the long term they were always, without exception, wrong. The best

time to buy is now. Whatever you can afford. Just get it as early in your life as possible. We all have friends who know the best

two times to buy are five years ago, and in five years time. Never now. They are now too old to buy. Condemned to be renters for

all their days. Anyone who says this is better than owning is deluded or lying. Our children own eleven residential properties between

them. Just ordinary kids doing stuff that anyone in NZ is allowed to do. If stupid people want to live their lives being stupid, I am all

for it. Just don't let them blame me or our "system" for stopping Them doing what they could also do if they were brave enoiugh, or

diligent enough. By the way, we gave our kids no financial or equity or security help. What we did give them was a good solid childhood,

and example. And we showed them the link between work, money, and the choice to buy stuff, or save.

Stop talking common sense mate, no room for it on here. Will not help most here anyway they are all leaving for Aussie apparently.

You are right Sit and it's going to trigger this community. I will add that it is most definitely harder now than in the past, but not impossible.

"Time in the market beats timing the market"

I honestly can't tell if this garbage-dump of a post is satire or not.

It's good general advice for life.

But it doesn't change the fact that what we are doing via policy is abhorrent and we need not be living off the wealth of the next generations as we are currently.

We subsidise property investment with taxpayers' money. We exempt it from reasonable taxation. We have artificially constrained supply. We have taken retirement savings to fuel the fire. We have used monetary and govt policy to keep prices up and fuel the fire.

That's good general advice for life, but we can still stop being parasites via our policy.

Hear that kids?

Be Quick!

It's fair enough, the only fatal flaw in what you say is the implied assumption that it is actually possible. For many potential FHBs, even if what you say is true, it simply can't be done now. The prices are too high, as well as the deposit requirements.

That's a big problem.

It is absolutely possible. Don't be so defeatist.

Minimum wage after tax: $667/week

Weekly costs $510/week

A couple investing the leftover in the NZ50 has a $200,000 deposit in 8 years.

If sit23 is right, what sort of house will a 200K deposit be able to buy in 8 years time?

Probably the house sit23's grandkids wanted to buy, but they were out-bid - not fast and committed enough - losers.

Whatever...

And then what, a 700-800k plus mortgage at 4-5% for 30 years? Not readily doable unless you have a very decent household income, and how about kids

And the other flaw is that it is dependent on most people not being able to do it. If everyone could and did, then it is self-defeating.

Good point.

He/she is trivializing the issue, by making out that anyone can do it so long as they have the desire and commitment.

It's nonsense.

You’re right, it’s impossible to do it. People who have (like me) are lying about it. It’s the system that’s against you. See where that attitude gets you

Boring.

By the way, I own a house.

But how??? It’s impossible to buy a house!!!

It was less bad in the past. For most people, it is impossible to buy a house, at the current nosebleed prices.

The article above, in fact states:

"In fact home ownership is now the most unaffordable it has been since interest.co.nz started compiling its Home Loan Affordability Reports in January 2004."

It's a sad indictment that so many people feel the need be such pricks about it to those who have had less fortunate timing in life.

For people who choose owning a home as a priority in life it is possible to buy a house. It is more difficult than it has been in the past.

Depends on the income they can command and how quickly the goalposts keep moving.

For a lot of people, in fact, most people, it's now more or less impossible.

I’ve shown the math, multiple times. I’ll leave you with this which applies to you and housemouse perfectly:

”I’ve made up my mind, don’t try and confuse me with facts”

And you've overlooked the major problems with your "math".

This comment reads like a Stuff article on young people on minimum wage purchasing a $1m home; much detail is missing.

Works every time, until it doesn't...

She's right. It's not actually illegal so long as they keep the house for at least 6 months and she's not on the title as a former home owner (assuming that's the case). If she gifts a deposit for presumably renovation funds then banks will probably approve it.

Only problem with her scenario is... timing.

Can't help but think that poster who moved to Perth is laughing at us.

A big problem indeed. Interest's motto is

"helping you make financial decisions"

So what is the advice or what can one learn from the above article to help people?

Leave the country??

Yep, or move to Timaru?

Places like Timaru have pretty limited job opportunities.

As long as there is broadband I'm ready to go:

https://www.broadbandcompare.co.nz/l/timaru-internet-providers?utm_cont…

If I had moved there 4 months ago and kept the same Webex background my workmates would not even have known.

I hear Queensland is nice.

If you don't mind the spiders, snakes and Australians.

Australians are great.

No they are not. They are even with Croc's but at least you expect the Croc to try and eat you.

You should be reported for racism.

"prejudice, discrimination, or antagonism by an individual, community, or institution against a person or people on the basis of their membership of a particular racial or ethnic group, typically one that is a minority or marginalized."

why?

Yes.

If you go to Aussie, Brock, you won’t be missed.

TTP

Thanks Tim,

I'm glad that despite the challenges of your spectrum disorders, you have been almost able to accurately express your true feelings.

I will keep posting here just to make sure of it.

Now that's funny! lol

That sums you up.

What's wrong with Australians?

I have a nice little (wee) house in Bundaberg. Happy to swap for a house in Christchurch with some cash your way ???

You lived there? Great access spot to fishing etc, I heard it's improved a lot. Probably still rather commute from Noosa though!!

Since 2008 I've been working from wherever I feel like, although lately mainly from my rural property in Hawkes Bay, and no one at work knows or cares where that might be. The joys of remote working.

That's great but most people don't have that flexibility.

HM, be more flexible, you often find reasons why things can't be done (like for example saying there are not enough jobs in Timaru). I used to have the same "can't do, can't be done mentality" which I inherited from my parents, I didn't even realise it. If I didn't meet my wife who has an absolute "I can do anything mentality" I'd still be working 9 to 5 and struggling to make ends meet.

I say this candidly, honestly, truthfully and with the best of intent

Screw Timaru then. Let's all move to Gore.

Bugger Gore...lets ALL move to Haast.

Brock, Frank, it's a shame we can't have an adult conversation about being more flexible

You're right, but if we take away "most" from an equation of millions then we're still left with a surprisingly large number of people, mainly "white collar" workers.

Around my area there are people working remotely for some of the largest companies in the world. Someone from my own company works from Germany. My solicitor is hundreds of km away and we've never met face to face. When the tokens of trade are bits and bytes, or pieces of paper, then the limits to location can be drastically reduced. Remove those people from the higher density areas and it gives more opportunities to those who are required to be there.

I know this pushes up prices in the areas to which these white collar workers would move, and with the current building supply constraints it's only getting worse, but if/when life returns to normal and prices moderate the option remains for those who can. In Havelock North, for example, there's well-advanced plans for hundreds of new houses just waiting for Auckland/Wellington evacuees. Same goes for Hastings, Napier and possibly Clive too.

Yes it's a no brainer for a lot of people.

Yep, for many young people by far the best 'financial advice' will be to leave this country.

That prices rise and fall, on average house prices increase 7-9%. Yes, the last couple of years have been crazy but in the long run it'll average out.

Don’t vote for blue or red?

The lower quartile median price of tinpot-town Tumeke Mackeral is now within a whisker of the AVERAGE price of alpha-city London at 1 GBP = 1.96 NZD.

https://www.gov.uk/government/news/uk-house-price-index-for-october-2021

Nothing to see here. This is totally normal. Not a bubble.

Be quick!

Misleading. You are comparing different types of housing.

Please elaborate. The London data is composed of detached, semi-detached, terrace and apartments. So is the Auckland data.

The distribution of housing type differs pretty wildly between the cities.

In some ways, but I'm also comparing lower quartile to average, and much of the housing being built here is actually equivalent these days.

London approx 43% live in apartments

Auckland approx 25%

That's actually not that great a difference and the apartments in London are generally more a bit more spacious than the ones here.

We are still faced with the conundrum that London (a global economic and cultural hub) has an average price that is about the same as the lower quartile price in Auckland.

You can nitpick over details. But its absolutely friggen nuts.

It isn't nitpicking details. The breakdown of type of housing matters. If London had the same types of housing as Auckland the average price would be much higher.

I don't think this is true. Could we have a source for this statistic please? Also which London population or area are you using for this?

Cost of finance much lower there too.

But London has a much greater weighting of apartments. As anyone who has ever lived in London will know too well, the quality of accom there is shockingly bad. It is a comparison worth making though, 25 years ago a 4 bed house in Remuera was equivalent to a 2 bed apartment in central london, now that same Remuera house could buy a house in a premium London suburb. Some of that is the exchange rate and some is house prices rising faster here. Plus Brexit and Covid.

There are a lot of dated interiors in London. But the houses are built to last unlike the wooden tents here.

Do you mean the old houses that are being torn down and being replaced by units? Not sure what you mean by "wooden tents"

He means well built homes that keep the water out.

So, less than .1% of houses in NZ?

And the heat in.

Serious question… do you think the current housing situation is a positive thing? I’m just curious. My personal view is that it’s a national tragedy that people are sleeping in cars and motels (emergency accommodation) due to affordability issues. Id like to see this addressed, what’s your thoughts on it?

The current housing situation is horrible, that's undeniable.

However, there are some good things that are happening. Old, cold, damp houses being torn down for multiple new houses is one.

Addressing the affordability issue isn't as simple as "make houses cheaper". I would argue we have a serious problem with NZ being net borrowers and not teaching budgeting and financial education in schools.

Thanks for the reply. You are right about the current intensification developments, it is a positive thing. I also agree with the schooling comment. Basic budgeting should be a fundamental in the curriculum… really good point

More townhouses and less older dwelling are generally supported by council allowing for higher density and more rate payers with more dwellings on the same size lot i.e. 4-6 townhouses on a 1000 sqm lot vs. a moulding wooden shack on a 1000 sqm lot.

Many flats in London are conversions where what was once a single house has over time been turned into apartments. Unless you have seen them, you cannot believe how compromised living is when kitchens and bathrooms are shoe-horned into something they were never designed for. Like California, NZ built with timber partly due to earthquake risk.

Life can't be that bad Brock, surely?

Yeah there are a few flats like that.

Why did you write "Life can't be that bad Brock, surely?"

Because I have never seen a comment from you that wasn't negative or complaining, and you seem like a decent person.

Is commenting on the existence of an obvious financial bubble on a financial website under an article about that bubble negative? or is it complaining?

My semi-detached house in the UK (although not in London) is 120 years old and still going strong. Brick with slate roof (still the original roof, too, with occasional patching). No earthquakes to worry about, of course.

Excellent article, Greg. I always enjoy these analyses since they put things in real terms.

That’s an increase [in mortgage payments] of $287 a week, up 59% in the last two years.

That's not a trivial increase.

It's unbelievable how long this has been allowed to go on for, and still, we have no action being taken by Govt & RBNZ.

At last!... some real world analysis.

No biggie, with Omicron pounding at the door we are now back to "regularly scheduled programming" - frightening the living daylights out of everyone so issues like FHB affordability are swept even further under the rug.

Have six friends (vaxxed) now who have tested positive for Omicron and all of them have said its almost nothing. Very mild cold.

Rod Jackson's head just exploded.

Yeah that's not how the govt is going to spin it... We must live in fear.

I dunno. I agree with it being a serious systemic risk to because while it's not serious at an individual level it's so contagious and with such a short incubation that all the load on the health system from the very few who get properly sick is going to come at once.

But trying to keep it out is only delaying the inevitable.

So the big question is, if you catch Omicron and then its a non event and recover, do you technically have immunity ? So obviously no need for the Jab from that point on ? Your one of the same as the vaccinated ?

I'm still waiting for the first "Person catches Delta after recovering from Omicron" article.

Not immunity, but protection for sure. The optimal way to get your immunity is via vaccines and then exposure - all the benefits of enormous protection without the risk of taking the exposure up front.

Incorrect. The optimal way to get your immunity is a good diet, exercise and sunlight, not via an unproven gene therapy. Once infected your antibody response will give you better protection. You possibly could have an argument if it was a 'vaccine' and you had proof of a clinical trial performed by a company not connected to or paid for by Big Pharma. And that takes 4-6 years. Otherwise, it is misinformation.

Vax doing its job ok then. That's good.

Why would they get tested?

So was Delta, a mild cold but I was unvaccinated, so imagine how sick I would have been if I was vaccinated. Could have ended up in the hospital on a respirator choking on my mucus....

If this is NOT a bubble, then homes will continue to transfer into the hands of fewer and fewer.

So many don't get this - we need it to be a bubble and we need it to burst.

If not, the pace of wealth transfer will keep accelerating.

It became very clear to me over a year ago now that the powers that be simply wouldn't let house prices crash and thereby bring down the economy with it. There simply will be no sizable price drops, you may see a small correction next year of 5% and a flatline. To many worldwide factors pushing prices up rather than providing downward pressure.

If only the other "powers that be" throughout history had been blessed with that degree of insight. Rather than stand by and watch an asset price bubble burst, you simply don't "let" it happen. Brilliant.

Im curious as to how you think 'the powers that be' will prevent a crash....what specific actions will they take?

If average wage earners can’t afford a starter house who is going to buy them. In Auckland 10 year to save for a deposit, most people get married to have a family how can this happen if you need both salaries to pay mortgage this is after you have saved for ten years, and if prices do go up in that10 years you will need to save for another 10 years it just goes on. If the house prices do not fall you will see more and more people sharing with other family’s

So far 4 out of the 21 lots auctioned this morning at the main Barfoots auction have sold. There are 48 lots listed will be interesting if they get over 20% sale rate today. In another auction the one lot sold for. $1.7 million preauction offer with no further bids. What is the point of making a pre auction offer if it goes to auction anyway? Why not wait and see if you could get it for less?

Carlos67 - While ‘the powers that be’ can try, it is rarely possible to stop a speculative bubble crashing. However, some (many?) people may not actually realise NZ’s housing market has become a huge speculative bubble. It is grimly amusing when bank economists and others predict a gentle landing or very small declines. Speculative manias like this rarely end well IMO.

That median weekly income (net) is for a "household" too. Best I find myself a sugar mummy.....

"Prices at the bottom of the market continued to rise steeply in November pushing home ownership further out of reach for those on average wages"

...and they say expecting...feeling.....probability.....But data/hard facts suggests otherwise.

Mr Orr has been saying since March that Housing market is cooling.......is $4000 per week rising and that too at lower end ...is this cooling as per Mr Orr.

Question is, have we mised the top?

Tax equity release as income. That is all anyone needs to do to sort out the New Zealand housing market. Of course a leader with backbone who can stand up to the property market lobby is required, along with media who interview SMEs other than those with vested interest in property, and a reserve bank that is not suffering state capture by the same crowd.

Even though I own the place I'm living in freehold and probably should otherwise feel happy, I actually instead feel pretty hacked off about this.

I voted Labour in 2017 with them pledging to address this societal issue as a high priority. Boy was I in for a disappointment. What have they done to correct this? Basically Diddly squat! So much for the year of Delivery.

House prices it would appear have managed to escape earth's gravitation pull and are shooting further and further away from earth.

Increasingly as time passes, I'm starting to wonder what the value of working is if the value of a simple home is going up several fold more than one could ever earn? Why bother contributing to this nation's economy? It's no wonder I'm seeing more and more of my peers packing up and departing for Australia. Who can blame them?

Yeah, it's a slow train wreck.

Don't blame yourself too harshly for voting Labour. I undermined them by voting TOP and diluted their power. 🙁

I haven't voted for Labour but I did vote for John Key for the same reasons and was likewise very disappointed.

You never own it freehold. Try not paying your rates.

No surprise, because those are the houses people can afford and they've learnt over the last 3 decades that the longer you wait to buy (and hope for a 'crash') the harder it will be to buy a home to live in.

I fell for this trap for many years, I finally bite the bullet and bought a home at 'record prices' which kind of hurts to be honest - however if the past 3 decades taught me anything, it is that in 10 years time, I will be in a better position than I am today.

Yeah. Now imagine where you'd be in three decades if you invested in crypto instead of housing.

Imagine where you'd be if you walked in to Skycity and put it all on black.

You'd only double your money.

Brock

If you see crypto as an investment strategy then it really explains your limited decision making and as to why you will continue to struggle to afford a house.

Your lack of reasoned investment strategy is simply relying on hope and luck. You need to get smart,

Most investments rely on hope and luck. Have you read "Fooled by Randomness" by Nassim Nicholas Taleb? The housing market, stock market, bitcoin and the casino. There are winners and losers, but the winners shouldn't give themselves too much credit, a lot of it is down to chance.

Waikato

Largely bollocks.

Yes, luck and good fortunate have a part to pay in any sound investment but one can increase one's chances considerably by considering substantive reasons . . . but substantive reason is lacking at the roulette wheel and in crypto.

I suggest you read some of Talebs works before discounting this as bollocks. I once won at roulette by betting black, 1/3 of the table and 1 single number. The 1/2 and 1/3 strategy slowed my loses and my single number came up twice that evening. Never tried it again as I was just lucky.

Waikato

Yes, simply lucky.

Basic premise of statistics . . . no mater how many times a coin comes up heads, the next time the odds remains heads 50%.

What is likely to happen to the housing market in the next 12 months . . . well there are plenty of substantive reasons indicating that it is not going to continue to increase at the same rate as the past eighteen months.

I agree with your prediction for the housing market but how will you use that information to make money? I decided to buy a family home and pay down the mortgage rather than leverage to get an investment property. This is because I am risk averse. If I had done so in 2015 I would now be able to cash up.

Coming from the UK I thought the NZ house prices in 2015 were daft compared to what I was used to in England (I was also in Ireland just before the crash). Good on those that took the risk and made a return, but I still think it was more good luck than good management.

Hi Printer8,

Why do you insist on writing braindead drivel like "it really explains your limited decision making as to why you will continue to struggle to afford a house."

What evidence do you have of:

a) Limited decision making

b) Struggle to afford a house

My crypto investments are up *check notes* ~2500%. Biggest mistake was not buying more.

Please explain your smart alternatives?

Brock

Sorry, son; you need to stop . . . your response reinforces my contention.

Cheers

So in other words.... you are just attempting to make petty teenaged insults and have nothing to back up your idiotic claims.

You'd think that somebody your age would know how to behave better.

The Fourth Cure: Guard thy treasures from loss.

Arkad advises against taking a risk of loss and investing get-rich-quick schemes: "Is it wise to be intrigued by larger earnings when thy principal may be lost? I say not. The penalty of risk is probable loss. Study carefully, before parting with thy treasure, each assurance that it may be safely reclaimed. Be not misled by thine own romantic desires to make wealth rapidly".

I'm guessing Printer8's evidence of b) is your constant complaining about house prices and quality.

Most unaffordable ever house prices and the lack of quality are, in fact, the subject of this article.

Printer8 has zero evidence. It's just garbage.

It depends on the metric used:

https://www.squirrel.co.nz/blogs/housing-market/beyond-2020-the-next-ho…

And the article doesn't mention housing quality which is improving, rapidly.

That aged like milk didn't it.

{kind=link}

Be honest Brock, the average investor has what, a few hundred bucks in Crypto ? Who cares if it goes up and down like it has been of late, you still have bugger all. The time to make serious money in crypto was years ago when they were giving it away. If you had made serious money you would have cashed out and bought a house with it or at least used it to cover the deposit at least 12 months ago as its turned out. If I had serious dollars in Crypto I would have sold half of it recently when it peaked.

It's never too late Carlos. The bankers aren't going to stop printing. Why on earth would you sell to invest in something as lousy as a house?

Leverage, tax benefits, a place to live?

IRONY: Deriding fiat currency because governments keep printing more, when (according to coinmarketcap.com) there were no less than THIRTEEN new cryptocurrencies registered in the last 24 hours alone.... and it's a weekend.

You can only know a peak in hindsight.

Brock - With Crypto they probably will end up with nothing.

No matter what happens to the housing market, home buyers will have a house they and their family can live in, as long as they can keep up mortgage payments.

This sounds exactly like me five years ago. I should have put a lot more of my house savings into crypto in hindsight.

In the long run, crypto is sound money and fiat is toilet paper.

Brock - Crypto is fiat too

Depending on the coin it's not going to be printed to oblivion though.

The RMA continues to restrict the availability of land for construction, government continues deficit spending and retail mortgage rates remain very low.

Hi Brock,

don’t know if this is permitted here but would you be open to contacting me via email. If agreeable Ill post an email addy up in this thread. If not no problem as this is understandably rather random.

Can anyone provide a link to lower quartile price data (NZ and/or Auckland)? My googling can only find random monthly snapshots of Lower quartile prices. Something similar to this Live graph below for the median price would be ideal:

https://www.interest.co.nz/charts/real-estate/median-price-reinz

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.