There was some relief for hopeful first home buyers at the start of 2022, with lower housing prices at the bottom of the market and a slight decline in mortgage interest rates making it easier for them to climb onto the first rung of the property ladder.

According to interest.co.nz's Home Loan Affordability Report, the Real Estate Institute of New Zealand's national lower quartile selling price declined to $650,000 in January.

That was the second month in a row that the national lower quartile price has declined since it peaked at $670,000 in November and means it has now retreated back to where it was in October last year.

Around the country lower quartile prices declined in eight regions in January - Auckland, Hawke's Bay, Manawatu/Whanganui, Wellington, Nelson/Marlborough, Canterbury, Otago and Southland, and rose in four regions - Northland, Waikato, Bay of Plenty and Taranaki.

The biggest declines in prices were in the main centres. This was led by Otago where January's lower quartile price was down by $60,000 from October's peak of $580,000 and in Canterbury, where January's lower quartile was down by $48,000 from December's peak of $548,000.

In Auckland the lower quartile price was $922,000 in January, down $44,000 from November's peak of $966,000.

First home buyers also received some slight but welcome relief from recent falls in mortgage interest rates.

The average of the two year fixed rate offered by the major banks declined from 4.21% in December to 4.19% in January.

The decline was due to banks adjusting their competitive positions rather than the start of an easing trend and the downward move in average rates is not expected to last.

However the fact that mortgage rates did not go up in January meant buyers would have received the full benefit of lower prices.

Unfortunately prices are already so high that the improvement in affordability was marginal.

The $20,000 decline in the national lower quartile price that has occurred since November would have reduced the amount required for a 10% deposit by just $2000.

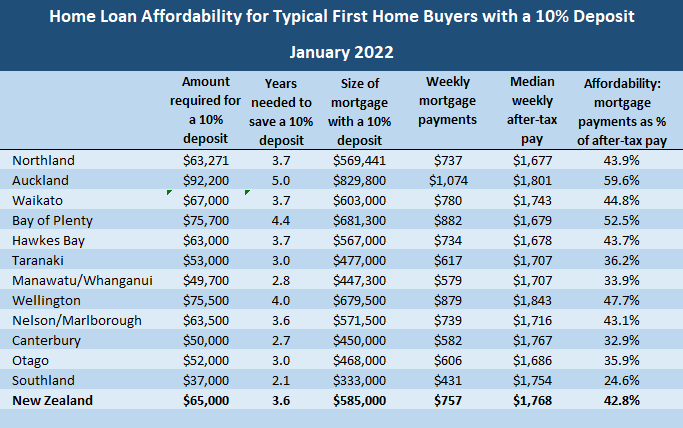

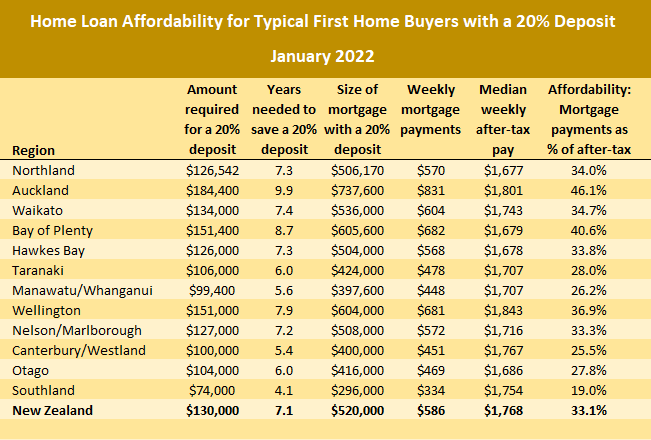

While any reduction is useful, potential first home buyers would still need to stump up with $65,000 for a 10% deposit and $130,000 for a 20% deposit to buy a home at the national lower quartile price.

In Auckland, the country's most expensive region, a 10% deposit on a lower quartile-priced home would be $92,200 and a 20% deposit would be $184,400.

And even if they could scrape together enough for a deposit, the mortgage payments would likely be prohibitively expensive for typical first home buyers on average incomes.

Mortgage payments are considered unaffordable if they take up more than 40% of the home owners' take home pay.

The mortgage payments on a home purchased at the national lower quartile price with a 10% deposit would be $757 a week, which would be 42.8% of the after-tax pay of a couple if both work full time at the median rate of pay for 25 to 29 year olds.

That's down from 43.7% in November but still in unaffordable territory.

In the highly priced Auckland market, the mortgage payments on a lower quartile-priced home purchased with a 10% deposit would eat up $1074 a week, which would be 59.6% of the after-tax pay of couples on average wages for typical first home buyers.

That's pushing home ownership squarely out of reach for people on average wages in Auckland.

But it's not just first home buyers in Auckland who are suffering.

Mortgage payments would also be in unaffordable territory for buyers with a 10% deposit in Northland, Waikato, Bay of Plenty, Hawke's Bay, Wellington and Nelson/Marlborough.

So although the fall in prices at the bottom of the market over the last couple of months will be welcome news for aspiring first home buyers, they would need to fall by considerably more before they would be back in affordable territory.

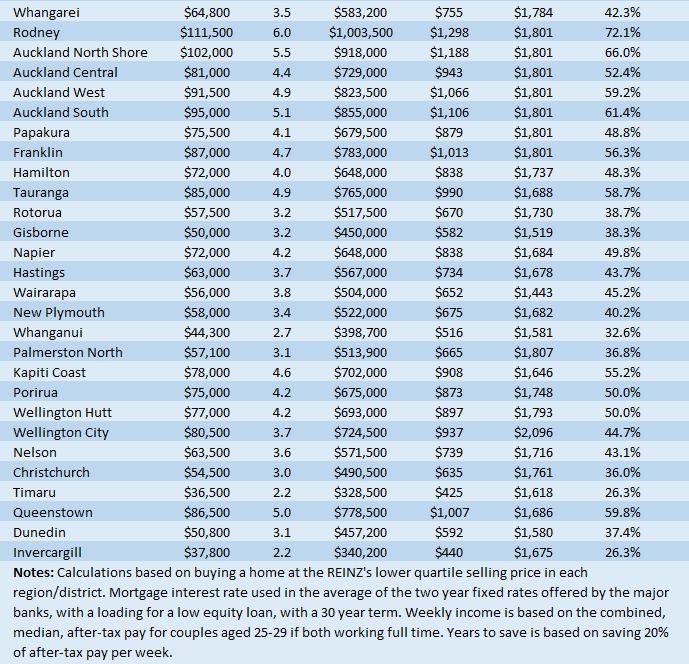

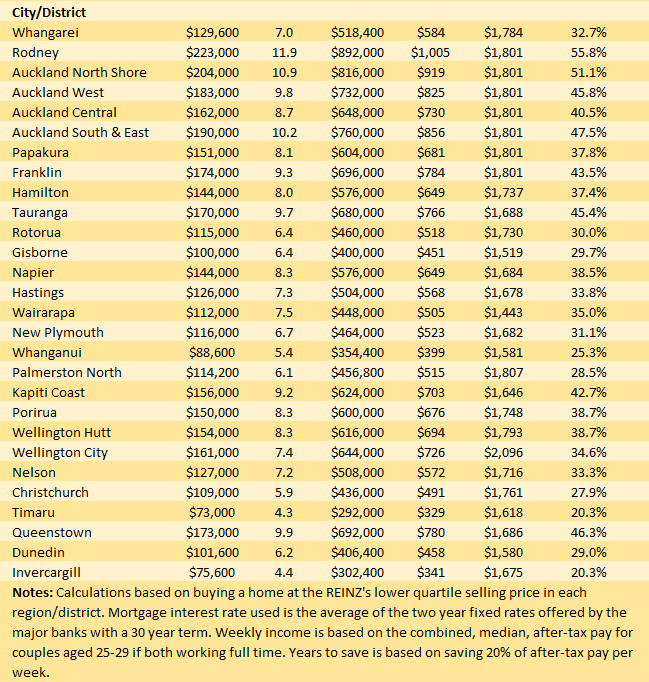

The tables below give the main affordability metrics for typical first home buyers with either 10% or 20% deposits in all regions and main urban districts throughout the country.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

166 Comments

Funny headline for the article. "Falling house prices". Still the average minimum in the country is 650k and its being justified as a fall.

This is a mockery of the poor or the ones on average salary.

The best hilarious part was decline of mortgage, 2 year rate from 4.21 to 4.19. Wow what a decrease, I can probably now save enough on that decrease in rate to afford one coffee a year.

Seriously, we need the prices to come down to sub 500k on an average property to make anything affordable.

But the leader of the current government wants the house prices to increase every month, so what can the poor expect.

I have spoken to many older - much older - folk who remember various of the post-war governments' great efforts to increase affordable access to home ownership. Home ownership was not magically more affordable in NZ's earlier history, and the post-war governments' put great effort into achieving much higher rates of home ownership.

Funnily, they didn't always seek to make it easier for young people to pay more. Not like recent years. Homes had to cost less.

We have warped morals today where we celebrate our wealth that is merely the saddling up of younger generations with larger and larger debts.

Interesting- had a look at article that showed House price to wages was 58% in the 80's when interest rates were 20%

The $20,000 decline in the national lower quartile price that has occurred since November would have reduced the amount required for a 10% deposit by just $2000.

This is right, Greg. $20,000 is a lot of money, especially for those looking to buy in the lower quartile, but it doesn't lower the bar much in terms of deposit required.

If you happened to buy in November, however, you've just watched $20,000 of your hard-earned money disappear in the space of 2 months.

The cost of borrowing money is going up all over the world. It’s going to be risk off for next few years as everyone tackles inflation and pays off debt,who in their right mind would risk buying a cheap house having a huge mortgage for next 30 years when everything will be on sale soon and that same house will be so much less and you will not lose your deposit and be in negative equity. A number of people on here have never seen a downturn so naive, when average earners over 50% of population cannot afford to buy a home the game is up the crash will come.

The crash likely should come, if economic fundamentals had much to do with it. But they didn't seem to have that much to do with the path to the bubble, so people are wary of betting against governments' and central banks' efforts to protect house and other asset prices.

Aspirational homebuyers should consider heading overseas and experiencing the world for a few years while the bubble here deflates. They can further their career and their horizons while strengthening their finances.

Buying here at just after the peak of stupidity is simply writing your own financial suicide note and throwing away the best years of your life.

Abandon your friends, abandon your family, all in the hopes that you find a better lifestyle elsewhere. The grass isn't always greener.

If your goal is to buy a home it is still possible. If your goal is to buy a home without making any sacrifices and just expecting it to be handed to you then moving overseas isn't going to help you.

Find new friends, find a new family... come on, let's get adventurous!

Never better said than by John Clarke https://www.youtube.com/watch?v=die5eWFp2Gc

Moving overseas is a sacrifice for some people. I don't know how many times I have heard people say 'just leave Auckland if you want to buy a house.' Moving overseas counts as leaving Auckland just as much as moving to Timaru does.

If your goal is to buy a home without making any sacrifices and just expecting it to be handed to you then moving overseas isn't going to help you

It's never been about avoiding sacrifice. The sacrifice has to be justifiable though, and it's a perfectly reasonable position to argue that it's not anymore, at least not in this country.

Leaving friends and family behind is a sacrifice too, but remember it wasn't too many generations ago that your ancestors and mine did just that, in order to find a better life here in New Zealand. The only difference is that keeping in touch over long distances is a lot easier now than it was back then.

I think hope will return as house prices sink 40% to 50% could be more if inflation and interest rates keep climbing. The Most average wage earners can afford would be 450k kjeldorian at this point hopefully you won’t need to go overseas.

You're dreaming. If inflation is persistently high then wage growth will also be high. NZD will drop to keep us internationally competitive.

It always makes me laugh how much specufestors sneer at the young but get so agitated at the thought of them leaving.

Abandon! Abandon! Fear! Uncertainty! Doubt! Auckland has the greenest grass in the world! You are just entitled and expect handouts! A rotbox here is the only goal in life!

An stint overseas can be tremendously enriching and provide valuable perspectives.

Hahahaha I AM one of the young. You think I stand in front of the mirror and sneer at myself?

You seem like the kind of chap that stands in front of a mirror and rehearses boomer talking points. Must be a jolly good laugh. Haw haw.

Nah i'm the boring kind of person who reads budgeting and financial literature. Better than crying about being a victim though.

Oh that's cool.

Most people have budgeting figured out by their first year as a student but there are a few slow learners around.

Have you got up to the chapter about minsky bubbles in your financial literature yet?

Good on anyone not wasting time sitting around crying. There is a whole world of opportunities and adventures out there.

I like reading differing opinions about it.

Can't be that many people who do get it right if they can't afford homes?

I didn't read the part in minsky bubbles where you claim things are too hard, give up and go overseas. Maybe you could provide a link?

Totally get having reasons to stay, but just to introduce the concept of sunk cost fallacy. Quitting something is a completely viable option (irrespective of your prior investment in this activity) and it shouldn't be considered a bad thing. Reevaluating investments (whether capital or time) periodically is important.

That is because during a bubble people’s psychology become so wrapped up in their own greed (and FOMO) that it isn’t until afterwards that they experience regret for not acting differently.

Yet here we have experience people suggesting people to take that action by acting differently and you’re actively abusing them for taking that position - probably because for your own personal benefit you want the bubble to keep expanding at your own benefit and to their detriment.

1. Give up and leave

2. There are still ways to get ahead.

Seems to be two competing philosophies here, option 2 gets massive negative response on here. I think it's because people can't reconcile the fact that it may be their own fault that they can't get ahead.

I actively vote against my best interests because I think it'll be better for NZ. But sure, just assume I'm a greedy boomer. That fits your narrative better.

Give up and leave

Your problem I think is that for some reason you think of going overseas as 'giving up.' It's not 'giving up' to make a move that would put you and your family in a better financial position. You can't have it both ways - simultaneously claiming that it's 'their own fault that they can't get ahead' and that doing something that will help them get ahead (moving overseas) is 'giving up.' It's not as though anyone has an obligation to stay in NZ and pay a fortune for a house, and if they don't they are somehow a bad person who isn't willing to work hard to get ahead.

Indeed. This person seems to be quite mentally confused.

I would have thought the converse would have been more true. Giving up would be staying where you are, just accepting your fate and making do. Working hard to achieve something, if that means upping sticks and moving elsewhere to pursue a dream, is certainly not giving up.

Lol - I haven’t suggested that you’re a greedy boomer - now you are claiming ‘the victim’ status, which you have attacked already as being a morally poor position to take.

Just ignore everyone here and continue to ‘get ahead’.

Your happiness isn’t dependent upon the health of society as a whole (sarc)

Who knew there were so many differing opinions on budgeting. All those people that can't afford a private jet... just didn't get budgeting right. Lawl, what fools!

An "expert" on budgeting would understand the concept of shopping around yeah? You know... you should avoid shopping at places with lousy products and high prices.

Shopping at the competitor's store with higher quality products and lower prices isn't giving up. It's what high IQ shoppers do. The crappy store eventually ups its game or goes out of business.

Minsky says there is a sale coming soon. Hope it's not a going out of business sale.

B L,

"Most people have budgeting figured out by their first year as a student but there are a few slow learners around" Really? Not in my experience..

Well keep at it linklater, you'll get there.

Thanks for these little pearls of wisdom. Perhaps you could twine some of your best into haiku and publish. Bestseller no doubt.

Abandon your friends,

Your family don't matter,

F*** off overseas.

Why are you even remotely concerned about other peoples social networks? You know nothing about other peoples circumstances.

I can't buy a house,

My spending is frivolous

moving won't help me.

Does it make you feel morally superior to take that position - is that your point - that people who are left renting, who are the business customers of property investors, are inferior human beings? And without these morally inferior people, property investors have no business model?

I got asked for Haiku's.

My life is hopeless,

Don't get bitter get better,

Offensive line deleted. Substituting asterisks for letters does not mitigate the offensiveness of your remark. Lively commentary is to be encouraged but keep it out of the gutter please. - Greg N.

‘My life is hopeless,

Don't get bitter get better,

(Copied line from comment above deleted. - Greg N).

If this is you being better I would hate to come across the bitter version.

I can't get ahead,

Why don't you try X or Y?

...No, I'm a victim.

What are you trying to get ahead of?

(Im fine by the way, I may appear to be a victim to you, but that is only because you appear to have decided to fill the role of a social bully so therefore anyone who isn’t as aggressive as you in chasing self interest is therefore a ‘victim’)

I have no intention of trying to get ahead - at least in terms of getting ahead of my fellow members of society. I work, contribute to society, and only need enough to get by comfortably. I have no need to get ahead of my fellow members of society by exploiting them or turning them into debt slaves via a debt ponzi - if that is what you mean by getting ahead?

I’d much prefer to be content and help other members of society find their happiness also - as opposed to everyone trying to ‘get ahead’ of one another as I can see how that is a zero sum game. It results in nasty and aggressive people who think their own self interest is more important than the stability of society of a whole - let alone the prosperity of the generations that will follow us.

Unfortunately some people have significant narcissistic and/or sociopathic personality traits. Usually they aren't as capable of thinking about the wellbeing of others. It helps when you read their posts to have this in mind.

I actively vote against my best interests and support others. I'm assuming you must be talking about the others on here talking about giving up and leaving.

Good for you. You sound like a really great person.

Not everything is about you.

I disagree with your opinion "give up and leave"

that's all.

By getting ahead I mean getting in a better, more stable situation than you are currently in. Not everything is a competition.

Kjeldorian, have you ever changed jobs? Moved to a different company, for example, or left a job and started working for yourself?

KJeldorian.. gosh you are an argumentative chap. Being disagreeable for the sake of being disagreeable shows a lack of emotional control. Just observing your name calling and dummy spitting. You all make good points , haven’t we had enough poo slinging for one day ?

You have got it all wrong. Getting ahead is getting ahead personally and doesn't involve trampling others in the process. Its about setting a realistic goal and going for it. Sure its much harder than setting some sort of personal fitness target because you have more control over that but its about not being one of the constant whiners on here that are going nowhere.

Try Y, like move abroad...?

So long as X or Y does not involve leaving the country, right? Could you perhaps give us a list of the things people are and are not allowed to try in order to get ahead according to you? I take it moving to Timaru is on the list, but moving to Tasmania is not? If you move to Timaru you're clearly the right kind of person willing to make the right kind of sacrifices, but if you move to Tasmania it's you're own fault you can't get ahead probably because of your frivolous spending and you are 'giving up.'

Different view-point,

but you still get a thumbs up.

Love a good Haiku.

Kjeldy mate, I think "whoosh" best sums up the reaction to much of your repartee on here...

But I'm enjoying it.

The whoosh of logic and truth going above everyones head.

Dude chill I'm on your side ( for the moment). I was referring to your wit going over some other heads...which on rereading my comment still seems perfectly clear.

Why do you need to buy a house? Why are Kiwis so obsessed with home ownership?

Because owning a home generally provides security of tenure, something that's not guaranteed when renting.

For first home buyers, with no family support, buying a first home is more than just a sacrifice now.

We have collectively robbed our current young people so that existing land owners can take huge and unsustainable capital gains.

If your 20 something, why not go overseas? Nz is an expensive place, isolated and limited in opportunities for young motivated professionals.

Most kids leave NZ for an oe at some point anyway.

Leave NZ, take a look, and in time see how much you miss NZ.

It need not be handed to young Kiwis any more than it was to older generations.

An equivalent level of handed to would be sufficient.

Exactly - the level of 'handed' to me that would involve houses at 3x household incomes and 20% interest would be great, thanks. Even if that 20% interest endured for the live of the loan, I'd still be better off than I am now, paying 3% on a house substantially below the median house price.

You'd also have the option of saving the equivalent of 3 years income with the help of 15% term deposit rates to buy the house outright, instead of saving 3 years income for just the house deposit with little help from 1 - 2% Term Deposit rates.

Funny how previous generations couldn't just save a little harder, rather than taking out 3 mortgages at 20% and then moaning about it 30 - 40 years later.

100% agree. Well said.

Exactly right. If I were young and skilled, I would not hesitate a second to do exactly what you are proposing.

...well an easier option would be to vote TOP (says the boomer who would be better off with status quo - but can't understand why our younger and asset less voters aren't voting TOP on masse)!

Quiet unbelievable..Stockholm syndrome perhaps?

Yup, but if these people had more opportunities they would have less excuses.

You don't know a thing about these people, and the 'excuses' are perfectly valid. Statistically (i.e. objectively) things are more difficult than they ought to be for most people, and heading overseas to greener pastures is a reasonable option for many.

Condescending and untrue.

Perhaps you know few young people. Try mixing with a few, the ones I meet are fine people.

It won't deflate.

We've been told that buying now is the worst thing you could have done for the last 15 years, where the reverse is true. If you don't buy you're screwed.

Lucky this is largely an opinion piece.

I see recency bias is strong in this one...

Can't fault people for trusting that further RBNZ and government welfare will be thrown at the market to try to keep prices inflated and inflating.

So the past is representative of the future?

I was in the US as the GFC unfolded and people made the same assumption while everyone was loading up on property debt.

That's very absolute.

For all you know the global economy will melt down in 1 months time.

Or the will start up QT 2.0 and we'll Have avg nz values at 2mil next year.

Risk and balance. Nothing is 100%

"...... while the bubble here deflates." [Brock Landers - see above.]

Good point, Brock. Things will "deflate" rather than burst - i.e. another soft-landing.

You're right on the money.

TTP

P.S. Enjoy living overseas. Hope it works out for you.

Indeed. As you say, the next few years are going to be very very flaccid.

It's a great opportunity to do something more interesting with our lives than losing time and money on the flipside of an asset bubble.

New Zealand ain't going anywhere.

Speaking of not going anywhere, serious question Brock, when are you off to Aussie ? The reason I ask is everyone will be having a laugh if your still here in 12 months time. Your on borrowed time this side of the ditch.

Good on you Brock go over get cashed up come back in two three years you will be able to buy most of what on offer in Auckland with your savings.

I already could. I'm just not in the habit of buying overpriced crap that's likely to plummet in value.

So you would like to buy a house that will increase in value so you can later realise a profit from your investment?

Hypocrisy much?

From the sounds of it Brock's buying a cheapie new build on land that's not worth much. Investment doesn't seem to be a priority there, he's got standards don't you know.

Cool story though Brockie, imagine if you bought yourself a house before you went on your O.E, instead of doing it the other way round. That would've seemed the wisest choice back then, and now.

I wonder if it's the paint fumes or just natural stupidity that brings out such dumb assumptions. But it's cute how obsessed you are.

That was not possible, nor would it have been the most optimal thing to do.

Buying a new house: check

It's a cheapie: check

It's not in an established area with high land costs: check

These are all things you've confirmed over time.

My dumbness has me travelling the world and generally being pretty content. Your intelligence has you being pretty cranky at a whole bunch of externalities to help you feel better for taking your time getting your act together.

Each to their own but people would be happier following the reverse of your advice, because the outcome stinks

Don't expect too much from somebody that managed to do two useless degrees before figuring out they are better suited to a basic trade. But surely getting a simple checklist right isn't too much to ask?

Tall poppy syndrome is not the behaviour of a content person. But at least you have an imagination. Keep making stuff up and you might get something right one day.

Hmm now your confusing minor amusement with "tall poppy syndrome". You'd need to be some sort of success first.

Just more of a success than you is enough. Let's be honest, the bar is set very low there.

I can't even see what logical thought process was followed to come up with that gem. It's quite impressive though. I'm not a property investor.

I don't want to buy cucumbers for $8 each either. It's not because I can't, it's because its lousy value for money.

Hi Carlos.

Thank you for your nonsensical grammar again. Build is currently pencilled in for completion in early 2023, so there is no hurry. I quite like the idea of bridging the gap with an extended global trip once the weather turns to crap here though. I hope this helps.

Nice story Brock, so the take from that is you will still be in NZ in 2025 especially after the sequel includes the house plan getting eaten by a Dingo and then the builder gets eaten by a Croc. Still I genuinely wish you the best over there, hope it changes your attitude.

It appears that your reading comprehension isn't much better than your spelling or grammar.

Which parts of "my attitude" do you hope are changed?

I attended a wedding on the weekend and spoke to a few of the guests - mostly mid 20s and university educated. Everyone I spoke to had plan to leave New Zealand, not as in an OE like normal, but more a case of leaving for greener pastures since Auckland has become unliveable for young people.

The bride and groom were off to Amsterdam in June, others were telling what their new salary was going to be in Brisbane and what house cost there, beaming at the prospect of being able to form a household.

It really saddens me to see how we have screwed our young people.

Eventually, NZ will be a country full of geriatrics, beneficiaries and gangsters deported from Australia.

Property investors' greed and self-centredness simply unraveling New Zealand society. But...they'll resort to hiding in gated subdivisions and grasping young folks' taxes as their pension before they looking beyond their own noses.

1st property. Now asking price 775k.

https://www.trademe.co.nz/a/property/residential/sale/listing/338987389…

2nd property. Sold November 908k.

https://www.trademe.co.nz/property/insights/address/Auckland/Panmure/Qu…

What makes these 2 identical townhouse price... so difference? They're almost next to each other.

17D Domain Rd vs 127N Queens Road?

No photos on the second townhouse, could be any number of reasons. Different layout, different finishings.

We've been to both. Identical layout and finish. about 20 metres apart. Maybe it's the road that justify the 133k differences.

One buyer was more foolish than the other?

One has two kitchens though going by the photos. https://homes.co.nz/address/auckland/panmure/127n-queens-road/zqoBQ?sea…

127C Queens Road, Panmure

Sold for $810,000 on 10 Feb 2022

Little paradise that is panmure, Who wouldn't want to pay close to 1m for this

If prices are going down then it isn't a property ladder, it's a property snake.

A snake is just nature's rope ladder, for the adventurous.

have you seen how well a snake can climb a ladder?

I always thought the “ladder” thing was kind of apt. What happens when everyone climbs up the same ladder? Especially when the bottom few rungs are busted off and it’s top heavy.

There is nothing wrong with climbing the ladder as long as you don't get to the top and find it is against the wrong wall.

As I read this its obvious in FHB wanting to buy a lower housing price house in Auckland just have not chance with 5 years to save for 10% deposit and weekly payments for mortgage of $1074 fixed for two years, what happens if rate go up 2% and have to re-fix or they go down to one income because of a baby or sickness they would not even be able to pay mortgage after 2 week as on one wage would no even be enough to pay weekly payment. As it stand they have $720 to survive off with inflation up cost of food would be $240 petrol $80 power/water/rates $120 insurance house/car $45 doctors dentist prescriptions $20 total weekly out goings $505 so $215 left between them so if rates do go up 2% they will go backwards also this is if they have no loans or credit cards I think everyone has a couple of these.I don’t think it is fair to say it is affordable because it obviously is not in Auckland and other areas.

Propaganda/False narrative of house price fall

Is that sarcasm? So hard to tell on this site sometimes.

At this point even the spruiker-iest agents are admitting there's a fall from late 2021. Small compared to the run-up earlier in 2021, sure, but definitely a change of direction.

If you are so edgy about one article base on facts you should probably review your property position to reflect your risk profile.

AJ123 .....let's do some research on the median Auckland house price from now (January 2022 $1,200,000 from the REINZ HPI index) till just before Christmas - so base the median Auckland house price on the HPI November 2022 figures ......I make a prediction that the November figure will be LOWER by 15% or $1,020,000

So if your comment was sarcasm, fair enough and I agree ....... otherwise see above.

In reality, it is far from affordability, the gain houses have made in last 2 years cannot be reverted and that is the ground reality.

Why I said it is a false narrative, is because this type of report will lead to loosening of LVR, reduction in interest rate & other tactics to give the property market a nudge. It is very true still housing in NZ is crazy and no one can deny it.

Total death due to covid in NZ 56, approved covid releif payment 69 billion, interest rate reduced to .25, LVR reduced & hence property price increase by 50% to 60%. Is 6% or 7% fall justified the run which property market had?

The answer is NO

AJ123 ....I read your post carefully and your line ...."the gain houses have made in last 2 years cannot be reverted and that is the ground reality."

I really need to question here the statement that gains cannot be reverted and that is the ground reality - can you please tell me what market in the world (sharemarkets, commercial property, bond markets, cryptocurrencies etc) are not subject to declines - whether 1% or 25% ?

Because if you know of such a market ? I will stop what I am doing now and put all my available resources into it !

NZ Housing market 100% secure guaranteed by NZ government.

11000 visas are approved in Jan every one will need home more to be approved by June.

This market will not let you fail until NZ govt gets bankrupt which is far from reality in the next 25 years. Eventually, it will gain momentum and in long term it will again double. Every govt labour or national will use all tactics to keep ticking it up, there will be no downfall.

We're all sweet then ...... let normal transmission resume ..... as long as AJ123 and his ilk are all OK with their property portfolios, with a "Government gaurantee", then there is nothing to be concerned about .....better get myself down to the good people at the local B&T branch and put all my business profits into that $1.2 million beautifully renovated ex state house, sun all day, outdoor flow, 3 bdm home in Mt Roskill and surrounds.......

Think it's time for a cup of tea ......... enjoy your day AJ123

Glimmer of hope. Really. I would say that most young would be first home buyers are so far underwater any such interpretation is just a cruel insult. I have just hung up from talking to my colleagues in the USA. They were saying that the average sort of house where they live in Illinois cost about US$130,000 (their houses are far more generous than ours) and I think that the average wage is somewhere north of US$ 70,000. (Whats more, if you are half way decent, you could just about be guaranteed a job for life) Why the hell would you stay here?

And we wonder why we are seeing spontaneous public anger, protests and near riots. Interesting to note that Canada also has very unaffordable housing prices, protests and riots. What we are seeing now is just the start. i predict public discord is going to get a whole lot worse.

Europe is the same with decent entry levels a 100.000.

NZ is just on an other level

In the wop-wops maybe. Pick a west coast city, though, and the prices are nearly as stupid as here. Incomes are better though, I'll give you that.

NZ on a worldwide comparison is the definition of the wop-wops.

The west coast of the states is the outlier, Many cities and states have median house price to income multiples in the 3 to 4x. Like we use to.

Not so bad as here. I have several friends living in different parts of California. They are flabbergasted at house prices here in NZ. One of them just bought a decent place in SF with a reasonable commute for a price nowhere near as bad as Auckland.

Bay area medians about $1m USD, approx $1.5m NZD. LA, Seattle, Vancouver (BC) pretty much the same.

Sure, if you want to live in Columbus, Ohio, it's a lot cheaper.

Midwest cities are much more congruent comparison for NZ cities than LA, Seattle, SF, etc.

Maybe. But to a point, people vote with their feet. If it were as clear cut as that, everyone would have sold up and moved to des moines en masses.

Funnily enough, their incomes are also in USD not NZD.

Also interesting that many of them have been able to buy better houses for the money than the equivalent Auckland equation (commute time and practicality, safety, type of house). Not to mention that if you do want to live in central SF apartments are better priced for the size and quality than Auckland. Not to mention that the Bay is a tech haven with some amazing salaries, having a wee bit more justification to be expensive beyond the entitlement and welfare driving NZ's problems (though of course SF is like Auckland in being infested by authoritarian NIMBYs).

It should be unsurprising they find the idea of a $1.5 million basic house in Milldale or Drury a little absurd.

If you're fighting the fight that everywhere else's prices are as absurd as NZ you're fighting a losing battle...

NZ is terrible and among the worst. No doubt about it. That doesn't mean one needs to be cherry picking and overstating to make the case.

Hence my point. The Western states aren't too bad so if it takes comparing the worst of the Bay with Auckland...that's a picked cherry indeed.

Pretty sure you brought up the bay!

Well, you did argue that basically any West coast city is priced as badly as here..while plainly they're not, in general. Despite the odd areas closer to the tech hubs that have the highest prices that might have to cherry pick to support the idea.

NZ is not comparable. There are many affordable cities in the United States, and those coastal cities are enormously more productive and richer than us.

Probably because a $130k house there has you living in an area that has you wearing a bullet proof vest while taking the dog for a walk ? Try Google.

"The typical home value of homes in Illinois is $249,145. This value is seasonally adjusted and only includes the middle price tier of homes. Illinois home values have gone up 14.0% over the past year."

You also cannot just simply just "Move there" either. The average wage there is $60K.

Also you cannot compare some tiny landlocked state in the middle of the USA with anywhere in New Zealand. Detroit is also a total shithole since it lost the Automotive industry.

With two people working that average wage boosts to $120k household income. There's your 2:1 price to income ratio right there. If one income well you've still got 4:1.

And here's the kicker: 2.1% interest rate fixed for 30 years. With 3% deposit depending on your credit rating.

Why am I in NZ again?

Yes, spot on. There are many places in the states that are far more affordable.

The main reason being is they have land policies that discourage land banking and make development land cheap and easy to develop. Because land is an obvious local input, they have full control.

BUT any country/city in the world has less control when material inputs come from other places where you cannot control policy. So this is why with some logistic and material supplies, even very affordable states have seen a larger than expected increase in prices. But a 15% increase on $300,000, is a lot more affordable than a 15% increase on a comparable house where its starting baseline is $800,000.

This is why it is stupid to try and control external inputs when the Govt. doesn't give a stuff about controlling internal inputs like the cost of land.

I hear house prices in Wellington are extraordinary and that the CBD is a bit of a dive lately with people living in tents hurling insults and human waste at people…

But I guess that justifies the insane price of housing there.

So Carlos have you lived and worked in the USA ? .....that is a very myopic "kiwi" view

It is really unfair that Brits can transfer their pension here and we cant move anywhere without losing ours. As I am nearing retirement age, we would be strongly considering leaving if we could get the pension. That would free up another house for someone

You get to take your kiwisaver with you. That is comparable to most foreign pension systems where a percentage of earnings are paid into an individual fund.

It would be cheaper for NZ to outsource its pensioners off to South East Asia and other cheap places too. Probably costs us a lot to keep them all here. We do it with wage slaves, why not with pensioners?

You need to read a bit of Alan Evans and Alain Bertuad to get some understanding as to why prices are as they are.

At one extreme you always have outliers, like Detriot (was) and Hong Kong still is. Any analysis, while making note of the reasons for this, leaves these out, looking at how things work 99.9% of the time everywhere else.

For example, you have two states, California and Texas which have many similarities, except Texas houses prices relative to income are half Californias, yet Texas has far more growth than California. The reason being is that California has always had restricted growth housing policies, and Texas doesn't.

Both states end up with about the same in population size etc. and all the positives and negatives that can be thrown their way about living the American Dream, except the Texans can do it with housing that is far more affordable.

California has had more people leaving than arriving for the first time in its history last year, and many of them going to Texas.

No actually it is rather a nice and prosperous little city. Sure it is miles from the sea in Illinois.

Chris-M ....just spent 10 years in the USA with a small property business, in Washington DC (MD) suburbs, only 10 miles from the Whitehouse, so totally agree , as most Kiwis just have absolutely no idea what you can get for USD 250K, in a good area. Also every American I know "freaks" out what is paid here in Auckland.

The very sad part about this is that all the PRO property commenters on this site, have so much at stake personally, so the last thing they want is for prices to "flatline", let alone decrease ! As their so called "business model" for getting ahead is capital growth, rather than rental income, as in NZ that just only "oils the machine" - while in the States, thats the big cherry on the cake.

Corruption in NZ seems to have been most evident in the capture of governance by land speculators. Rates, zoning, tax, demand-side subsidies...mysteriously all seem to have been co-opted to suit those who got in cheap off the backs of previous generations, now enriching themselves at the expense of the next.

Yes this has been my angle of conversation but alas the property junkies are not getting it. I often come at it from a social impact/lifestyle point of view because I am in a position to see first hand the damage being done to our communities and country. What we are seeing in Wellington is only the start, the division and inequality out there now is huge and only getting worse, it will tear our country apart because no one wants to do anything about it. But all I get from property junkies is "Yeah but property will never fail, guaranteed capital gains, you are stupid if you don't buy investment properties".

Stupid is destroying something good for the majority just so a minority can feel rich.

Bottom quartile prices in English Regions (in NZD) below. The huge difference in the entry price for housing is caused by our chronic shortage of social housing, and the eye watering Govt subsidy of landlords through accommodation supplement. The bottom of the market is always determined by the rents that can be paid / charged in that area. The system is broken.

- North East 197,000

- North West 260,000

- Yorkshire and The Humber 256,000

- East Midlands 320,000

- West Midlands 320,000

- East of England 473,000

- London 774,000

- South East 539,990

- South West 425,000

- Wales 258,000

Those lower quartile houses might have thatched roofs and 300 year old plumbing for all we know.

Yeah, ok... Or they might be relatively new, double-glazed, very well-insulated, 3-bedroom homes next to key employers etc.

https://www.rightmove.co.uk/properties/118644995#

Nah, they're not. I come from Yorkshire & Humber region. Though a lot of them are terraced houses, they are definitely over all good quality. Especially compared to NZ. Double glazing, central heating and good insulation are pretty standard. What I could call a basic standard is hit, at least.

My (probably lower quartile) house in the UK is brick with slate roof, very solidly built. Still has the original roof from the 1900s, give or take a couple of patches. Houses in the UK are generally much more solid than typical NZ houses - partly because they don't need to flex for earthquakes.

It's a nice two bed semi-detached house in a city bigger than Wellington, well located with a big garden. It is selling for the equivalent of $385,000.

edit: forgot to mention the double glazing, 30cm of loft insulation, wall insulation, central heating...this is all standard in the UK and wouldn't be worth mentioning.

Wait.

You've misspelt “be quick”, surely?

All this money just for shelter, crazy.

The market needs to come back a long way before we look anything like affordable. The Salvation Army were correct in calling it a catastrophe. As a property valuer, I see daily the effect this is having on families. A proper correction would be in the order of 40%, and even then on an international basis NZ is still not affordable. It wont happen though, the government will see to that

I think we might be approaching the point where government and central banks are actually losing control - both politically and around the monetary policy/inflation narratives. Look at the instability around the world both domestically and internationally, financially and politically.

I think anything is on the cards.

So true. I firmly believe this year will be tougher than the last two for NZ, and something will totally derail this government. They are so out of their depth

Commenting by exception here, and certainly not on covid - I think the thing that will be the final straw for the government is when Auckland Council consults with the community in April on the massive planning changes mandated by central government - there will be an uproar.

Many would rather hide in gated and guarded communities from the problems they are creating than settle for even slightly less wealth extracted from next generations of Kiwis.

By definition, NZ is one of the largest most isolated gated communities in the world, and like our advantage that gave us with the likes of Covid, we will squander that advantage.

It's more like a 60% fall to bring the prices down to sensible levels. At which point we lose a million people, just like Ireland. And they will be those that can move, just like Ireland (the young and productive). But I seriously doubt we would be able to replicate the Irish way out, by becoming a tax haven for large multi nationals...

"by becoming a tax haven for large multi nationals..."

Are we not already?

No

Drop company income tax significantly and raise an LVT on the unimproved value of land and we'd go a long way there.

Correct. If you break a property out into its component parts into what are value-added and non-value added inputs, this shows that the non-value-added bits add up to approx. 40%, or more.

That is given the right policies, the same land and house could be built for at least 40% less than its present value with no decrease in amenity.

This would bring us back to 4.5 to 5 x median house price to income multiple.

However, once a policy is enacted, we can't control that decent without any collateral damage any more than we could control the increase and the collateral damage it has done(to a different group of people).

But since there are many policy changes international that affect us in which we have no control regardless, then a Global crash may get us there.

What hope are we talking about for FHB.

When one say glimmer of hope, one is being highly optimistic as FHB, particularly in Auckland is dead unless, one streches beyond and that too to buy matchbox houses.

Am happy as being lucky, though did not voted for Labour but in trying to woo National voters, Jacinda Arden and her team in their enthusium went much beyond in supporting housing market as never seen before.

Labour party may or may not get national votes but are sure to lose heaps of their traditional voters.

Central bank and government will be quick to react to data that housing market is cooling as it does not suit their interest and may lose power unless they act quickly to boost the housing market.

Traditional Labour voters - i.e. working classes - would be better placed searching for an actual left-leaning party rather than choosing either tinge of Natbour. Otherwise they'll be forever stuck having their wealth transferred upwards by policy.

People will do anything to hold on to their “Aucklander badge”. Even if it means crappy house, time spend in traffic, no spare money taking kids for overseas trip and before they realise 20 years have gone past…

I just don't understand why the average working professional hasn't left NZ, especially now that covid has allowed for many to work remotely. For 30 years Labour and National have promised and delivered nothing. Affordabiity is now through the rough, quality of life is dropping and the country, especially for white guys is totally woke. Why do any of you believe most of these problems will be fixed after 30 years of both parties promising but never delivering. Ministes from both parties, especially National have multiple property investments and both sides use the excuse that they are protecting recent buyers and don't want to see their investment into their biggest asset drop. This tells you straight away that a major correction will never happen unless the market somehow crashes, in which case NZ will be a right off anyhow and you most likely won't get a mortgage. I follow the news in NZ and everything is worse than it's ever been, the country is actually a walking diaster looking for a cliff. Most of you are just not going to have any quality of life, you will become debt slaves to banks and the wealthy and many of you will suffer as both parties inact more regulations taking away more freedoms.

https://www.parliament.nz/media/8172/register-of-pecuniary-and-other-specified-interests-2021.pdf

In parliament, the National Party makes up the majority of property owners. 33 members either own or have investments in 117 properties. This is an average of 3.5 houses per member. Every National MP also owns at least one property.

Outstanding post! NZ has been low wage-high cost for ages. The trade off was you lived in a nice peaceful country with a good lifestyle.

Now you don't even get that! Labour are toast but National/Act will have to radically change their thinking in order to resolve the myriad issues facing NZ. More of the same will not work, but our whole political system revolves around short termism in order to get re-elected in 3 years.

I have done my OE and and even got educated overseas so I am not going down that road again but I am encouraging my children to, and that saddens me.

If National get in and Luxon does a John Key young people will be even more angry than they are now. The wealth transfers to asset owners simply have to stop if politicians want to maintain NZ society.

Luxon talks the productivity talk as Key did before him. As key did before him, he himself invests in ...residential property.

Young Kiwis need to look elsewhere than the Natbour twins.

"Unfortunately prices are already so high that the improvement in affordability was marginal."

If you cant save 200K in a lifetime, 195K is not much use

Rising interest rates offset falling prices.

Home buyers think in terms of mortgage payment amounts.

So no real change.

Dumb home buyers do. If someone pays a million dollars for a house, and house prices fall to the extent that that house is now only worth $800,000, they still have to pay a million dollars to the bank.

No I see what you're getting at. Home prices always go up, at least in the long run, so don't worry about the total cost. Just worry about being able to pay the installments.

Oh man I think we're in trouble. Or at least the banks are.

Watching the RBNZ live stream, what a clown show. These guys cannot give specific numbers on anything.

At the start of thew COVID era, house prices dipped, only to suddenly rise. And risen it has, by 25-30% in just a year. Our Government stepped in, to introduce tax and other incentives for new builds in March 2021. To little effect, as a year later, house prices increased by about 25%.

Inflation is a measure of the cost of living, and owning a house is an investment. Is this right?

Surely a resident has a right to food and to own their own shelter.

House prices have spiralled out of control. This beast cannot be easily tamed, even an increase in OCR and a projected 9 % decrease in house prices canot undo the huge increase over the past two years.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.