A new report produced by Gareth Morgan aims a fresh broadside at the 'privilege' afforded by the current tax system and proposes again radical overhaul to include a way of taxing capital and of taxing foreign entities.

Residential property would inevitably become the main focus.

The report, titled: "New Zealand Income Tax: Unfair and favours the rich", says several of our taxation structures are able to be exploited and that is exacerbating inequality across society as well as denying New Zealand the economic growth it could otherwise achieve.

"A growing problem is the tyranny or hegemony of the majority wherein a substantial tract of voters – the property-owning group – is able to extract benefit for no value provided to society. Such rent-seeking is the antithesis of an efficient, equitable society and warrants corrective measures," Morgan says.

The new paper is based on work initiated in the 2011 publication of the book, “The Big Kahuna”, by Morgan and Susan Guthrie and updates and refines one side of the tax and welfare reforms proposed in that work. It is part of a project that looks at the need for even wider taxation reform and considers options for reform of social welfare. The intention is to produce a sequel to The Big Kahuna, late in 2016.

Morgan says the new paper covers "just two" of the weaknesses in our taxation regime that are underwriting an unfair and economically inefficient economy.

"The costs of conferring privilege are real – not just financial – but more widely than that socially and politically. It is incumbent on a government to continually strive to maximise the performance of its taxation regime on the basis of neutrality, equity and efficiency.

"...The two topics covered in this discussion on tax are by no means an exhaustive canvas of what can be done to improve our taxation regime. There are issues around tax and charitable organisations and around tax and the Approved Issuer Levy available to those raising money from abroad, which also warrant examination. They, amongst, others will be the subject of future work."

'Glaring gaps'

But on the two topics covered in the new work, Morgan says they are two of the glaring gaps - "deliberate loopholes" - in New Zealand’s income tax regime.

"These loopholes have persisted for many decades and have contributed to a rising concentration of wealth, particularly but not exclusively, held in the form of property assets. These loopholes have distorted investment and income, and ultimately undermined the growth potential of the economy. Not surprisingly, these loopholes are of increasing public concern as well.

"The proposal here is reform of the income taxation regime. The reform I suggest is not incremental, it is fundamental. I propose that New Zealand moves from a tax regime that confers privilege and amplifies inequality, to one that supports equality of opportunity, freedom of choice, and higher living standards. Such a radical change will, of course, have to be introduced carefully as there will be important transition issues."

Morgan says the first income tax loophole addressed in the paper arises from how income is defined for tax purposes. The current definition of income used by IRD excludes from tax, some of the benefit received by owners of capital. Despite being recognised in the National Income Accounts as genuine income, some forms of income are not taxed. The second loophole that is addressed is one that extends to foreign-owned enterprises, "providing them with an easy avenue to dodge their tax obligations in New Zealand".

"Three of the desirable properties of a taxation system are that it be fair, neutral and economically efficient. The New Zealand income tax regime is none of these things," Morgan says.

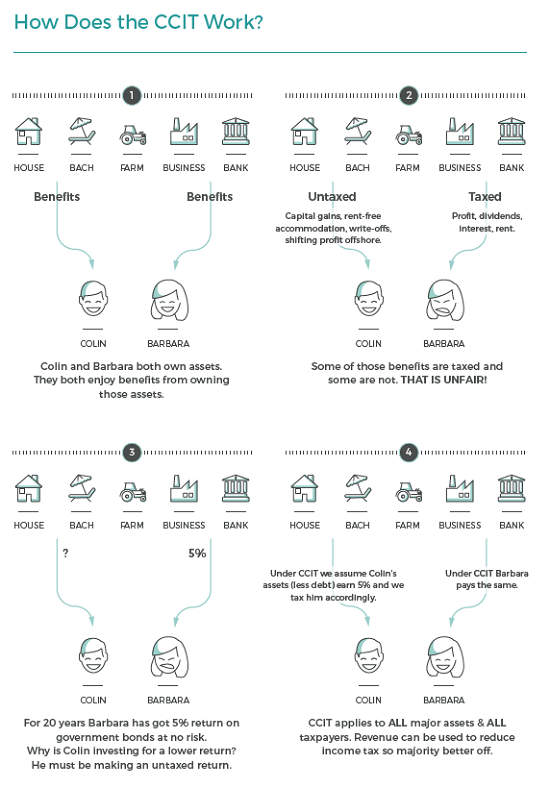

Turning to his proposal for a "Comprehensive Capital Income Tax" (CCIT), Morgan says Parliament’s "decision to turn a blind eye" to the very real economic benefits received by home-owners "instills a massive unfairness in our tax regime".

'Real income benefit'

"The effective income benefit that owner-occupiers enjoy from their ownership of housing is very real yet it’s untaxed. If you put $500k into a bank you are taxed on the benefit you receive (interest), but if you buy a house with it you are not (yet the accommodation services received are real). Both are benefits received, why should one be taxed and not the other? The answer, is that our tax system is largely a cash-based system, a significant problem which was recognised in 2001 in the McLeod Tax Review and raised again in 2010 by the Tax Working Group. The limited definition of ‘income’ that underpins the New Zealand tax system is a likely contributor to the rise in inequality witnessed in New Zealand."

Morgan says the effective average tax rate paid on salary and wages is 18%, that on other forms of income to households averages just 12%, while the effective tax rate paid on corporate incomes, "always hard to measure", appears to be around 16%. These average tax rates are based on government revenue data and income estimates from the National Income (or “GDP”) Accounts. "On the face of it these varying rates of income tax are unfair. However they are the reality and one of the two reasons our income tax system is overdue for reform."

Morgan says the proposed CCIT bears many similarities to the tax reforms tabled in the 2001 McLeod Tax Review.

"The essence of the idea is that income is received by people in more ways than just cash, and if a tax regime fails to acknowledge this, anomalies in the way the tax burden is shared are unavoidable."

Arguably the biggest hole in the income tax base is the absence of non-market income, or income that is produced from applying the capital stock in a way that generates a return for the owner, which the owner then consumes, Morgan says.

Disturbing the allocation of capital

"Nobody would suggest that these noncash or in-kind items – which are after all included in the recognised measure of national income - are not real. This single distortion has arguably been the source of the greatest disturbance in allocation of capital in capitalist economies over recent decades. In the property market, the tax wedge favours ownership over renting to a degree that would not exist if both forms of rental income were taxed. Further, this distortion has underpinned a demand for property ownership that is quite apart or separate to any demand for accommodation, resulting in a quite different allocation of capital than would otherwise be the case. The tax incentive has a lot to answer for."

Morgan says the proposition of the CCIT is that own-use of (non-financial) capital provides an assessable income depending on whether the owner lets the capital lie idle, underutilised or enjoys the full benefit of its services. But in all cases, that benefit should be taxed – at least to the extent that the income from it could be at least equal to the risk-free rate the economy is offering.

"Let’s illustrate by taking a car as an example – the owner can rent it out, use it in her business that produces a cash income, drive it for pleasure, or leave it idle in the garage. In only two of the four cases is the service the car produces assessable for income tax. Yet in all four cases the owner could reap a benefit.

"The concept of the CCIT is that in all four cases the car’s services are available as income for the owner and therefore assessable for income tax. For the two cases where there is no cash income, the question becomes how much assessable income should be deemed. We know what rate of return the owner could earn with no risk at all from the amount she’s invested in the car so the assessable income should be set at least at that rate. In a world of long term government bonds offering yields of 5% then, a 5% income on the car is a minimum that could be assessable. The value of the car is available from the statutory depreciation schedules, or market prices, while the owner can only be expected to declare an income that accords to the equity they own in the equipment. If there is debt registered against the vehicle that will already be reaping taxable income for the lender so no need to tax it twice. This approach is an alternative to the tax authority deeming that the 5% rate of return should apply to the full vehicle (depreciated) value but have the interest bill on any debt deducted.

A twofold approach

"The point of this approach to taxation of income from capital is twofold; to ensure that all effective income is taxed (this is the argument for a tax regime that is equitable); and to raise the utilisation of capital (this is the economic efficiency argument).

"In practical terms the tax assessment would require every economic entity to provide a schedule of assets and debt each year. Then for assessable income purposes, the CCIT is applied to the owner’s net equity in the asset. So if a 5% return is assumed and the relevant income tax rate (20% for instance) is applied to that deemed income, then each and every year then, the owning entity’s CCIT liability is 1% of the aggregate depreciated net (i.e. less debt) capital they own.

"If the entity already generates taxable income that is subject to income tax then that tax can be netted from the assessed CCIT – so the CCIT could be as low (but not less than) zero. This simply ensures that capital-owning business entities pay at least the tax they would by investing that capital at the risk-free rate."

Addressing the question of what asset value the CCIT cuts in at, Morgan says this is ultimately this is a political question "but a minimum asset schedule of $200,000 and a $10,000 per capital item lower threshold, may be a practical floor for individual personal owner/taxpayers".

"For multi-owner (Partnerships or Trust) assets the floor might be $200,000 per capital item. A property worth $5m say with 100 beneficial owners would attract CCIT on $4.8m, irrespective of individual owners’ proportional interest. For incorporated taxable entities there would be no need for the $200k exemption."

Expanding the income tax base

To illustrate this, Morgan says that a couple who jointly owned one $40,000 and one $8,000 car, and a boat worth $10,000, and had $350,000 equity in a house (say the house was worth $600,000 but they had a mortgage of $250,000), would be assessed as having $400,000 of net worth (the cheaper car would not be counted). Using a risk free rate of 5% and a tax rate of 20% CCIT of $4,000 would be payable.

"A CCIT applied at these rates in New Zealand would expand the income tax base by the order of at least 20%. In other words it could finance a drop in income tax rates across the board of the same – for example, the average tax rate on salary and wages of 18% could fall to something closer to 14%. And of course the politicians of the day would decide exactly who to favour most in that tax cut."

One obvious argument levelled against such a non-cash-based tax would be; how would those liable for the tax meet the payments?

Morgan has answers for that:

"On this, think about CCIT in an analogous way to property rates – but rather than being simply an annual impost on the owner of land and buildings, it is applied to the equity in all productive or non-financial capital which provides a return of some form (in cash or in services) to its owner. Owners of land and buildings have to arrange their overall portfolio so that they have sufficient cash to pay their rates each year. The CCIT requires exactly the same. What we would expect is for owners of currently non-taxed capital to have to rearrange their financial affairs in order to pay tax on the benefit they receive via ownership.

'We expect the price of property to be lower'

"By requiring owners of capital to take into account the cash flow implications of an annual impost under CCIT, we would expect the price of property for example to be lower than would otherwise prevail – the reason being that the after-tax return from ownership will be lowered. This will improve the alignment of house prices with the demand for accommodation, as opposed to the status quo where property prices reflect more the combined benefit anticipated from tax-free capital gain and the tax break afforded the benefit from accommodation received each year by owner-occupiers.

"The cash required to meet the annual CCIT impost can be expected to be available from owners who rearrange their portfolios to include more cash-earning assets. It may well be reasonable to allow owners in certain circumstances to defer their CCIT for a limited period (so long as use of money interest is charged) until they sort their cash flow. This type of circumstance could include a loss-making year for a business, or even a year where profit is made but cash flow is tight because of investment outlays say. Another circumstance might be a homeowner who is waiting for a liquidity event such as an asset sale in order to meet their tax obligations. But it’s an important principle to ensure in these cases there is no free ride for the owner so charging them use-of-money interest at market rates would be appropriate. It may be appropriate in some circumstances for the owner to grant the IRD a charge over the asset as well."

So, what happens to home owners who have invested on the expectation of tax-free capital gain?

"This is a question about transition from the current regime to the CCIT regime," Morgan says.

"A related question is by how much we might expect property prices to correct in a world without the tax loophole owners currently enjoy. It will be less than if that loophole were completely removed – the CCIT does not fully tax the accommodation benefit that owner-occupiers enjoy. To do that it would tax the market rental equivalent of the property, whereas under CCIT what is taxed is 5% of the property value. Rental yields would be above the risk-free rate in a world of tax-neutrality, reflecting the risk of the asset class.

How much prices drop by 'depends'

"Anyway, even a partial closure of the loophole (as CCIT brings about) can be expected to lower property prices. By how much depends on how much of the current demand is driven by what owners currently expect to make over time from tax-free capital gain. That depends on location or course and anticipated population growth and buyer pressure. The amount is indeterminate without making arbitrary assumptions around how speculators discount expected future wealth gains compared to current cash flow, or without knowing how much of the return currently is achieved already via taxable means. The greater that is, the less the reduction in capital value that can be expected."

Morgan says the introduction of a CCIT-based income tax regime would adversely affect the capital value of property for some, that fall conferring equivalent benefit to prospective property owners in the form of a reduced cost of entry to the market.

"It is then in essence a wealth transfer, the extent of the transfer will depend on the extent of the proportion of return (financial and other) that is already in taxable form. It is a current market reality that rental yields of higher valued properties are lower – which itself reflects the demand from higher income owner-occupiers for the tax-free benefits and ownership rights over the ‘luxury comforts’ conferred. On financial grounds alone one might expect then the capital impact of the CCIT to be greatest for these types of property – but it is not a given.

"Unambiguously, demand for housing will align more closely with accommodation needs – how much closer is indeterminate."

Overseas experience

Morgan says there are offshore examples of similar taxes to the one he is proposing.

"The list of countries that do deploy such taxes is extensive and includes Australia, the UK, France, Belgium, Canada, Luxembourg, South Korea, Iceland, Switzerland, Denmark, the Netherlands and Germany.

"Many of these countries procure revenue from these taxes to an extent that the total revenue is at least 2% of GDP. Our estimates of what the CCIT would procure is between 3% and 4% of GDP. Some countries struggle with defining the most appropriate deductible expenses. That reality makes the alternative of applying the CCIT only to the equity held in the asset (rather than the total asset value and allowing interest and other expenses deductible) more appealing. As well, the idea to apply the CCIT to the worldwide balance sheet of the taxpayer (rather than just the New Zealand assets) looks to be far more effective at preventing avoidance.

"The Netherlands is closest to a pure CCIT regime – it uses a combination of a wealth tax and an imputed rental tax. Assets are assumed to have a 4% return, which is taxed at 30%. There is a per asset minimum of c.$NZ40,000 but no overall net asset minimum (debt is not taken into account)."

Taxing foreign entities

Moving on to the taxation of foreign entities, Morgan says that in New Zealand foreign firms have a number of ways of avoiding the tax impost that they would face if they were New Zealand-owned.

"Some are due to regulatory weaknesses, others due to stratagems these firms employ to deliberately reduce taxable earnings.

"On the regulatory front there are weaknesses around the double taxation agreements that New Zealand is party to. In short they allow a foreign firm to avoid New Zealand income tax if it doesn’t have a “permanent establishment” here. For online businesses in particular this is a no-brainer. The remedy lies in modernising these tax treaties.

"Given the two common ways for foreign firms to shift taxable profits beyond the New Zealand tax jurisdiction – namely taking on debt-heavy balance sheets, or deploying transfer pricing on their inputs – there are two broad ways to proceed.

"The first is relatively simple but arguably overkill. It would see the IRD deeming a profit for the company as a pro rata share of the company’s worldwide profit apportioned by its New Zealand share of global sales. Clearly for taxation purposes the “company” would need to be defined as the general group of companies behind the product or service, rather than any special purpose New Zealand subsidiary set up specifically for distribution here. That does give rise to identification issues and difficulties around partly foreign-owned local operations.

"The second approach is to deal with the profit transferring behaviour of any foreign owned company operating in New Zealand. The remedies here comprise of two stratagems as follows;

1. Thin Capitalisation Leveraging up the balance sheet so that interest costs rise is an easy way to dodge tax – the interest is a deduction and it flows offshore to who-knows-where so the lender (a related party) can collect that money in a lower (sometimes zero) tax jurisdiction. New Zealand moved against this in 1996 by introducing thin capitalisation rules which in effect nowadays attempt to limit the amount of gearing to 60% of the balance sheet assets of the New Zealand-registered company. Of course this still affords plenty of scope for tax dodging via debt and seems little more than symbolic. A more robust way of setting the gearing ceiling would be to get data on industry average gearing for the firm’s peers and set the ceiling at that level for all firms whose interest payments flow beyond our tax jurisdiction. Our IRD would probably argue that would be too much hassle and that the 60% rule is 23 quick and more-or-less effective. We’d suggest it’s lazy and that the default should be no interest-bearing debt from abroad is allowed unless the taxpayer is able to prove their claim that the interest is a legitimate cost. They could do this only if the debt met particular criteria; for example to get tax relief the taxpayer would have to produce the data on international gearing norms for their sector and, secondly, provide evidence as to why their gearing internationally should be higher than international norms. With this sort of regime the onus of proof for deductibility lies with the taxpayer, not the IRD. If they can’t prove it they don’t get it.

2. Transfer Pricing The second tax dodge available for foreign companies is transfer pricing. Companies who play this game “purchase” an input from a related party that sits outside the New Zealand tax jurisdiction (often in a tax haven), effectively transferring their pre-tax profits to that party. Again the IRD does have a policy on this, it’s a policy that reflects our signing of international double tax treaties with other OECD countries. But the reality is it doesn’t work, we are sitting ducks. Multinationals can shift profits away from where the economic activity occurs to where the tax liability is minimised. Examples are abundant – Coca Cola, Facebook, Apple are just examples of multinationals operating in New Zealand whose practices have come under fire because their tax liabilities are significantly and consistently lower, year after year as a percentage of sales, than any comparable firms operating solely in New Zealand. Prima facie there is certainly a case to put the onus of proof of compliance on these firms. In order to shut down transfer pricing practices firms should pass three eligibility tests before being allowed to claim the costs of imported inputs (materials, royalties, interest, licence fees) as deductible expenses. Importantly with these tests, the onus of proof for deductibility would fall on the taxpayer, and not be up to the IRD to prove an expense didn’t qualify. If the corporate can’t provide the proof then the costs simply are not deductible for the purposes of stating New Zealand taxable profits. The first test for tax deductibility would be proving that the input being purchased from a non-New Zealand party is not from one that has a beneficial foreign shareholding of say 5% or more in common with the taxable company. ‘Beneficial’ covers direct and indirect (through third parties) shareholdings. The second, and additional hurdle would be requiring the tax payer to establish that the cost of the input is no higher than would occur in an arms length transaction between non-related parties. If the taxpayer cannot establish Test 2 because of lack of comparable industry data (such might be the case for a royalty for IP say) then the third test is for the taxpayer to establish that the royalty is no more than parties pay for the use of that IP in the IP owner’s country. And if the IP owner’s country is a tax haven then the taxpayer has to use as their benchmark the average of 3 white list countries to establish the absence of price ramping. Finally, as an alternative to the eligibility tests above, the multinational could instead establish its taxpayer bona fides by simply proving that its overall tax burden across all the white list countries it operates in, is no lower than industry averages. This alternate method demonstrates that the New Zealand tax impost is intended to be no higher (or lower) than the average of white list jurisdictions.

Foreign ownership of homes

On the question of foreign ownership of residential property and land, Morgan says with the exception of “sensitive land” New Zealand maintains an open borders approach to property investment by foreigners – no matter their origin.

"Such a strategy might make sense when it comes to commercial property - the origin of the investment doesn’t matter if the result is higher utilisation of capital and greater income and employment.

"The CCIT discussed earlier would ensure that the stock of idle capital would be limited, no matter who the owner."

However, Morgan says when it comes to residential property in New Zealand there now appears to be a shortage of affordable property for prospective first-time homeowners.

"In Auckland, in particular, the price of housing appears to significantly exceed what would be justified solely by the demand for accommodation.

'Incongruous'

"It seems incongruous then that we allow foreigners (i.e. people who don’t reside here) to hoard housing here for their own home country reasons (for example, if their own country has poor enforcement of property rights). It’s especially unfathomable that we would exempt from reciprocal restrictions residents of countries that forbid ownership of residential property by New Zealanders.

"We surely should at least restrict them to leasehold ownership only. With the deregulation of Chinese capital now underway we can expect capital flight from that country, much as we see from Russia year after year. The sheer magnitude of the inflows could rise to levels quite disruptive, not just in the Auckland market, but countrywide.

"The rationale from these investors is simple – it’s a bolthole in which to place savings beyond the reach of oppressive and unpredictable regimes in their home countries.

"To welcome foreign investment is the hallmark of an open capitalist society, but when those flows come from residents of countries that lock out foreign investment as well as constrain the rights of their own citizens, that investment should be significantly qualified – at least until the investor becomes a citizen of New Zealand or a similar “white list” country," Morgan says.

"The reason is not that we should not welcome foreign investment, but rather that the sheer magnitude of “bolt hole” capital flows can prove to swamp our small market with society wide consequences.

Flows come and go

"These flows come and go (remember the Japanese in the late 1980s, we thought they were going to annex Surfers Paradise at one stage?) and that instability is disruptive for our own residents. Annexation of significant swathes of our property from local investors seems a senseless denial of local citizens’ access to their own productive capital – inhibiting employment and income growth.

"In 2015 the UK followed the US, Switzerland, France and Spain by introducing a capital gains tax payable on sale by foreign owners of property. The rationale is that UK residents pay such a tax on their second and subsequent homes, and for foreigners this is an analogous situation. While a capital gains tax is nowhere near as efficient as a CCIT, the intention of these governments is clearly to limit the distortion of residential property markets caused by the activity of foreign buyers motivated by events in their home markets.

"In New Zealand under a CCIT regime foreign investment in property would produce taxable income – the property would need to provide tax equivalent to a return on investment of 5% or the return calibrated in the income tax return, whichever is the higher.

"The foreign investor would be subject to the normal provisions regarding tax deductibility of costs that are required of foreign investors. The impact of this approach is to welcome foreign investment in non-residential property on the same basis as a New Zealand investor would encounter investing in a business. The effective restriction on foreigners would be with regard to investment in residential property which would be restricted to those from “white list” countries."

68 Comments

Why don't we keep it simple and just tax anyone that has a cat. Those with two cats only get taxed at the higher rate of determined breed. Those with camouflage are taxed higher (tabby) as well as those known to be more aggressive to wildlife. (burmese)

"However, Morgan says when it comes to residential property in New Zealand there now appears to be a shortage of affordable property for prospective first-time homeowners."

Umm, well duh. Stop talking and start your own party Gareth I would tell him. He's got the money and the mouth. And a great deal of hindsight it would seem.

Fiirst homer buyer is Endangered species under National Government. Need to protect them from extinction.

Yes, 100% agree. But that was beginning to happen10 years ago IF anyone had been seriously watching.

National Government is not interested in fair and just laws and are not interested in taking any action so whatever anyone suggest is down the drain. National will be in mood to listen only next year being year of election but by that time would be too late.

We need leaders with vision in New Zealand and not businessmen to run the country that too dirty shrewed busibessmen.

Simple question, How come National party be Blind and Deaf to Housing Bubble which even school going childern knows.

You can wake a person who is sleeping but not someone who is pretending to sleep.

Mr David if your suggestions are not in line with vested interest of govt are not good even if they are good for future of the country.

With this government only thing that comes to mind is ARROGENT AND THICK SKIN otherwise why would they not act which is in the interest of yhe country.

1. Leaders with "vision" but no money sense can be very dangerous people. North Korea and Zimbabwe both have them and it isn't working very well.

2. It is very hard to get people to agree what is good for the country. Some people don't even believe good and bad exist.

3. All politicians are thick skinned, it has nothing to do with their party.

Leaders also have social responsibilities

I agree, but to ignore competence in favour of vision alone is unbalanced and dangerous is my point.

This is sensible policy, and needs be considered a whole lot less flippantly than the comments so far indicate. I am a net loser, but still see it as critical that the next generation are given the opportunity the last one has had, and sooner rather than later. Unless wealth comes into the tax system, there is no end to the rich getting richer as Thomas Pikketty demonstrates. That leaves increasing numbers in the cold - literally in some cases.

I'm surprised Gareth hasn't mentioned oxygen here, as he is clearly from the school that says everything can be taxed. I sacrificed a lot to own my own home, while many others had overseas trips (OE), flash cars and started families (at a time when I considered I couldn't afford to). So now he advocates that I pay an additional tax on that? As to my car - four benefits that could be taxed. I'm sorry Gareth it costs me to own my car, so I already pay for the benefit that vehicle ownership has. He makes little mention of GST and that as a portion of income, the lower and middle classes (which are sinking, ever quicker) GST takes up a disproportionate ratio.

Having had that gripe, there is a lot in here that I agree with, but I do wonder if that is just dressing on an underlying agenda to provide a program that extract evermore taxes from the bottom, thus keeping the establishment's boot on our throat.

Further to my comment, how much would he tax push bikes? He also makes no mention of the fact that trucking companies are subsidised by every other road user while Kiwi Rail has to pay it's own way. (Yes I know they received a big chunk in this latest budget, but National has served them notice that it stops in two years). There are so many flaws in his proposal that it is laughable at best.

It's not about more tax at all. It's about broadening the tax base and dropping the tax rates. Current situation is that I enjoy the benefit of major loopholes in the tax regime as an owner of assets, and my equivalent who owns bank deposits doesn't. That is a breach of any principle of fairness and as well is hugely economically inefficient. It means I invest not for the economic return but for the return that the tax regime makes the greatest.

There is substantial inequality in the payment of tax. There are many wealthy people paying a disproportionately low rate of tax given the benefit they obtain from our economy. I'm not sure why so many comments are arguing in support of tax breaks for the rich.

While I am a nobody in the investment world and obtain a number of tax breaks not available to most citizens by running a business that is merged with my lifestyle. While not loopholes those tax writes offs are a benefit to my gain in net worth. I'm sure that if I suggested that if I should have less tax write offs or more tax for myself someone would get upset about it.

I don't really understand why people want the country to go broke to make a minority of citizens richer.

I suggest that you're quite naive. Give a politician an opportunity to apply more tax so that he can drop it somewhere else invariably leads to just adding more tax. GST is a good example in point. What was the original planned amount, and paye reduction to, and what actually happened? I do agree that too many are avoiding tax through loopholes, but to suggest that I should pay more tax on my car when I already pay tax through fuel charges, road user charges, and registration really gets me fired up. Especially when those taxes are supposed to pay for roads, but actually are siphoned off in the general slush fund for other political agendas, as well as subsidising trucking companies.

And one would assume you purchased your car using tax paid income....then along comes Gareth wanting to tax you on it again.....

Owner occupation of a house may be seen as an 'economic benefit' but it can also be seen as a basic human right.

It is a severe misrepresentation to dress up the need for shelter as, "favouring the rich", "tax exploitation", "Tyranny or hegemony", "rent seeking" and "not equitable".

Having a place to live is a basic human right.

You owning that place is not a basic human right. However it does confer very real (untaxed) benefits to the owner vs people who are renting.

It is a severe misrepresentation to confuse having somewhere to live with owning your own house

Fair enough.

I would still suggest treating a place to live as nothing more than (or only or primarily) an economic asset just because it is owned is selling short the truth of matter.

Speculation should be stoped and that is government responsibilty specially when it is so rampant. I know for sure that overseas money is in play with this housing buble and govt is not interedted to do anything. Which is a shame.

It would be nice if, for a change, GM provided a step-by-step plan of how to get There from Here.

Step 1: get this past the Voters.....

Mostly agree with the report and ideas, at least it is moving towards a fairer and more sustainable future, the only one i would add is a 'tobin tax' on financial transactions. But if we contine to misallocate our tax dollars its all for nothing anyway.

Even for RBNZ proposal of income to loan measure, the government will take ages to approve to give time to speculators. Will not see it in near future. Defenitely no announcement by RBNZ on 9th june as per govt tactic to delay any measure to control housing buble. Watch iton 9th June.

you wont see loan to income this year

Hon BILL ENGLISH: That is hypothetical. The Reserve Bank has yet to investigate whether the tool is workable. Then it has got to decide that it wants to include it in the memorandum of understanding about macro-prudential tools. Then it has got to go out and consult everybody and work out how to apply it.

Grant Robertson: Are there any limits to a debt to income ratio that he will rule out now?

Hon BILL ENGLISH: No, because it is not my role in law to do that. In law, the respective roles are that if the Reserve Bank wants to introduce another macro-prudential tool, then it negotiates with the Government to include it in the memorandum of understanding. The design and application of the tool are, as they should be, the tasks of the independent statutory regulator. Much as the member might think it is appropriate, I do not think the New Zealand Minister of Finance should break the law.

Should try and control the speculation that is happening. In last 3 months have seen house price gone up by 25% which is crazy. Houses that were available for 800 have gone above million in 3 months.

People's homes are already taxed through rates. Anyone suggesting a further tax is frankly evil in my opinion. I would fight this at every step.

I understand your comment. But the problem is minimising/not paying tax is a national sport. The wealthy can afford health insurance, private schools, live in the right areas to get to "better schools"... Im not pointing fingers, Im not on the bones of my arse - But we are creating an under class that will likely never escape unless we change something.

People will say - Im not paying more tax it just gets wasted by the beuracrats anyway - I dont disagree they make some stupid decisions

BUT every NZ child deserves a fair go at a reasonable life, if this means paying more tax, Im for it.

that doesn't mean they can't have further taxes.

Stop being a nimby.

Great article

The last thing the government wants is prices to drop going into an election year.... this means expect absolutely nothing in the short term in regards to solving the speculators/investor demand issue...

They will come up with some.promises for the election and that's about it...

Crazy thing is back in 2007 DonKey thought that houses prices were at a crisis level (500k) yet in 2016 with prices close to 1m they are not.

DonKey has a typical banker mentality. They look for short term goals such as GDP even if the gdp growth is based purely on boosting the population with low skilled migrants and the gdp per capitia is in reverse

High housing prices also help GDP as people feel wealthier and buy cars and holidays on credit.

Donkey has no vision.... his only interest is short term targets and ensuring he gets voted in at the next election

In 8 years he has failed miserably in regards to housing. He should be ashamed of himself.

You are correct but imagine what the house price will be in 2 years time. Beyond average kiwi and unless you are downsizing or overseas buyerwill never be able to buy house in Auckland. Shame on government for only thinking about politics and not about the country.

Come on Evita just click save once and wait. Is that so hard?

Don't blame users for software defects. The site operators should just fix the trivial issue along with that filthy rag on the header.

Would it help if I put some naughty words here to draw attention to the issue?

It's already at that stage. Let's not forget NZ has the highest prices relative to incomes in the developed world.

"The effective income benefit that owner-occupiers enjoy from their ownership of housing is very real yet it’s untaxed. If you put $500k into a bank you are taxed on the benefit you receive (interest), but if you buy a house with it you are not (yet the accommodation services received are real). Both are benefits received, why should one be taxed and not the other?

Everytime I read this kind of logic... I cringe..

Gareths line of logic can be applied to anything we spend our money on.... anything that we derive a"benefit" from...... eg... spending money on a holiday..???

To claim that something has a "tax free" benefit , simply because that money COULD, alternatively, have been invested ,earning interest , .... is an inane argument..completely lacking in common sense..

I tend to like the idea of a Land tax.... along the Henry George lines.

I tend to favour minimal PAYE tax.... ( would productivity rise..?? )

The depreciated value of an asset provides an income every year - that's what assets are. It is totally different to spending on consumption such as a trip. The GDP accounts recognise the imputed rent of owner occupied housing as income. Yet it is untaxed. That is the anomaly. That you "like" a land tax which is merely a subset of a tax on the imputed income from capital, tells me you don't understand the difference between current and capital concepts. Therein lies your challenge.

The GDP accounts recognise the imputed rent of owner occupied housing as income.

Might this not simply reveal an imperfection in the construct of this thing we call GDP?

Thankfully, the only person who actually gives a toss what Gawweth Morgan thinks is Gawweth Morgan.

IKR? LOL.

The guy is a fool, trying to control everything like a typical bitter socialist. Someone should ask, ‘why should we listen to you? What makes you so right all the time’. Soviet economics, bring on the statue of Gareth the redeemer!

Hardly a fool. He has been clever enough to amass a huge fortune; did it by making a positive contribution to the economy and without having to resort to the negative, exploitative and tax loop hole dependent activities he is addressing.

Morgan is a natural target for the clobber anyone who has a go set but there are many people like me who view him as an insightful contributor to the NZ narrative. I am struggling however with his concept of taxing all capital on a theoretical returns basis. The unfair FIF notional return based tax has elements of his thinking and it increases risk for Kiwis by discouraging diversification. Similar distortions would occur under the Gareth plan. Tax deductible investment entities would proliferate, every home become an Airbnb. Maybe Gareths plan is to set up trade me valuation services Ltd to support the gigantic asset valuation industry that’d be needed to support his scheme.But I share his incredulity about the bizarre policy that allows foreigners free access to NZ housing stock.

GM made his money by partly bank rolling his son's project that resulted in Trademe. When it was sold he netted $50 mil. So not his idea, or business acumen. He is though an economist, and when I hear a wealthy economist talking how we can tax everything, I start having nightmares around George Orwell's 1984 theme.

Do you really believe that his son's upbringing, guidance and advice played no part in Trade Me's success. The really clever people in this world are the ones who are able to influence others to be successful.

Gareth also did pretty well on his own behalf through his investment company and econometric research company. Hardly a free loading slug riding on the back of his son.

Your ignorance is astounding. Apart from the fact that Trade Me provided less than a quarter of my wealth, you clearly have no idea as to how that particular business came about. Try to focus on the subject matter here rather than sink into the swill of personal uninformed invective

what conservative rubbish - a Capital Tax is hardly socialist - it's just anathema to brain addled asset owners who believe they are sumwun speshal and deserve speshal tweetment

Nationalizing all land and leasing it back to you - now that would be Socialist.

People who are in property market, do not have to worry about anything as the government is not going to do anything to stop the party as it is not in their interest and they do care a damn about the country. Making First Home Buyer an Endangered Species in Auckland. Feel sorry for the young generation that it is their luck that they had and have government like national party.

Interesting but I'm not entirely convinced. Should we really be taxing the family home?

How would it work for businesses or farms (note the distinction). Should they be taxed on the capital employed. What if the business has little capital tied up like, say a software company, makes large profits, should they go lightly taxed on the basis of a low capital structure. What if later the company matures to be worth hundreds of millions of dollars. Under this regime the capital gain would not be untaxed.

There is a profit that accrues to borrowers for investment in property or anything else. That is the inflation of the debt. This gain goes untaxed and is one of the large tax loopholes that underpins property and other passive investment. This advantage is enjoyed at the expense of the savers who have to unfairly pay tax on the inflation portion of the interest that they receive. I suggest that the the tax on interest paid and received needs to be adjusted to allow for inflation.

The whole issue of taxation and wealth redistribution urgently needs to be addressed in a comprehensive, long term basis. This is one interesting contribution to the debate but a lot more work is required.

Gareth is such a clever chap and yet he comes up with rubbish like this? Sad really.

I believe we could tax cat ownership though, as mentioned above. The rate could be based on the number of native birds killed per annum, minus the number of rats and mice. A suitable weighting by species of native bird based on rarity would be required, as would a similar rating for rats as against mice. Some consideration would have to be given to the number and species of introduced birds killed and what weightings are appropriate, if any. Whether the killed birds were also eaten could be a mitigating or aggravating factor in some instances as presumably some cat food would be available for human consumption in third world countries as a displacement effect.

Similarly, a system of determining the credit for killing the neighbours cat would be needed, which could be based on the tax rate applying to the dead cat. By extension dog owners could receive a credit for each cat killed, although a system of oversight would need to be put in place to determine if the cat was fair game, such as being on the dog owners' property at the time of the killing. This would have the additional benefit of helping to address the unfair discrimination that dog owners currently experience.

Such a tax system would not be without cost, as all cat owners would need to submit a live feed from their cats at all times and there would need to be a National Cat Monitoring Office suitably staffed and equipped. The employment benefits are obvious, and would, I believe, result in a fair and equitable redistribution of the exogenous costs of cat ownership.

Dear cat lovers, please, please, please, do not think I am a cat hater. I merely make this suggestion as a simple parody of the Morgan Method.

I feel you have overlooked the clear economic benefits received from a cat sitting on your lap.

There is the 'feel good' factor, similar to that obtained through entertainment. And obviously the cat is warm, so there is an obvious heating benefit there. If we set up a committee to examine the issues, I feel sure we could come up with more evil, hidden tax exploitations from cat ownership.

Ah, yes, the imputed food benefit of all those dead mice and birds on the doormat in the morning, for instance.

How much tax did Gareth pay on the gains he made from selling his stakes in TM & GMI ?

He would probably the first to agree with you on that point. In fact I think that I have heard him say so him self.

Nothing to stop him making a voluntary payment if he feels that strongly about it......

Zero - the same tax I've paid on all the property I've sold.

Oddly enough I own a home (that I occupy), two businesses and starting a third business. The latest business is even an investment structured to be sold for capital gain within two years. And the oddity is, I really have no problem with the idea or practice of capital gains tax on investment vehicles but feel it's wrong for the house. I don't even think of the house in investment terms. It's just where I live. It is interesting isn't it.

What about the imputed benefit in kind to Gareth of his good name? You can't make this stuff up. The imputed benefit of having a wealthy son, the list goes on. It's not fair, he should be taxed.

[Deal with the issue; the tax-free status of property gains. Personal insults not acceptable. Ed]

I can sympathize with the intent that GM has, and there is certainly a case for better asset allocation.

But needing to value assets (which is really essential to the whole concept) has a lotta fish-hooks.

- How often, and by persons with what qualification?

- How are 'floors', 'threshholds' on asset values to be applied and how are these assessed in the first place?

- How is the deemed rate of return to be set - by whom, how often, by what criteria?

- Are the valuation and judgement costs themselves tax-deductible and for what classes of asset-holders?

- Are existing asset taxes (e.g. rates on capital value of properties by TLA's) able to be offset against the deemed-income tax take, and if not, why not?

Imagine a pensioner, on NS, with a $500,000 house. There's real 'income' in the traditional sense, plus a deemed income on say $300K of the (assuming the $200K threshhold). So immediately GM's proposal comes with a requirement to calculate multiple tax types and thus slices, in a single return. And this equates to a tremendous complication in the tax regime - something NZ has managed to avoid so far.

In fact, the only thing I'd keep outta the whole thing is the property angle, which at least has the virtue of being currently available via TLA valuation rolls. Couple the valuation roll number to some IRD numbers and there's the tax base. KISS.

But there's still that little matter of getting this into the political arena and getting it voted through.

I wouldn't bet the farm (capital value $????) on seeing it in my lifetime, absent a Revolution.

Gareth Morgan - as I read your treatise I wonder if you could explain the rationale behind the following

NZ used to have and at some time has eliminated

1. Surtax on very large incomes

2. Aggregation of spouses incomes for determining tax rates

3. Death duties

4. Gift duties

5. Muldoon's clawback of mortgage interest on sale of rental property

It would be helpful to understand your proposals if we understood the reasoning of what once was but has been abolished, and why - we need to understand the reasoning

I am assuming that the Big Kahuna still includes a payment to all individuals which is then offset by income tax? I still think it is a beautiful idea that would actually work well. If you are a retiree with a modest house the Kahuna payment with likely more than offset the CCIT meanwhile if you are a retiree with a carefully tax minimized income who draws down of a vast amount of capital assets overtime your going to be hit heavily - as you should be.

I have a household income of well over 200k with no children and own my own home in the central suburbs but I still think it is a good idea. I worked my way from nothing but I don't believe generations of my family to come should be able to rest on their laurels and enjoy all the capital I build up tax free. Equality must eventually be achieved for a fair society, based on what everyone puts in, not how much assets they inherit.

Unfortunately no tax system is perfect or universally fair to all participants. That unfairness (real or perceived) is seen in the passion expressed in the comments above. Rage comes easily to the man who thinks he's paying more tax, or might be asked to pay more tax, than his wealthier neighbour.

I suspect for a tax system to be compatible with social harmony, it has to be reasonably fair and simple and transparent enough to be understood by a frighteningly average punter. I'm not sure the CCIT idea meets the simple and transparent criteria. And I suspect the smart and well-resourced minds who spend their days creating tax avoidance schemes would shoot it full of holes for their wealthy clients.

That said, as a country we definitely need to discuss our tax system more, and celebrity gossip less. A better tax system is out there, and CCIT might be part of it, but cheap shots from all sides won’t help us figure that out.

This sounds like it would be too complex and just lead to even more tax dodges as people shuffle equity and debt positions (not to mention trusts) to minimise the "deemed income" from their assets. Far simpler to have a straightforward land tax. Of course it is a bit tough for the poor person with 80% mortgage who has to pay more land tax on top of that, but perhaps that will moderate property prices.

I get sick and tired of claims that property investors are not being taxed clightly and that is the reason for the falling home ownership percentage. Then people point to other countries as an example. What is not stated is that some of those countries counted as a good example actually give home owners a tax credit off the principle home owners mortgage payments. Obviously I have a vested interest in wanting to stay in business. Well the current Government has increased taxes on us investors. Even Nick Smith is now quoting the extra Billion dollars per year they have been taking off us recently. This tax has to come from somewhere. Property investors do not print their own money. The market is creaking and groaning as it adjusts to this increase tax. Why is everyone surprised when some people are less well off. I suggest to you investors are extracting money from where ever they can find it to pay the extra taxes.

Australia run a CGT for property and it didn't stop their market to going berserk.

One mistake in your post though ..

This tax has to come from somewhere.

S/be

This tax has to come from somewhere else.

Tax on overseas non resident buyer is need of the time. Government wants solution and can say with surety if introduced, the market may or may not crash but the ever rising house price will stop and is needed as this house bubble is not only bad for first time buyer but also for eceonomy. As this bubble is fuelled by overseas buyer. Wait for the next data but condition is, it should be done properly that is citizen and resident should be seperated with overseas buyer n also also students and people on short term work visa as everyone knows that prooert is bought through students funded by family from overseas to avoid hiving tgeir local ird number.

Tax on overseas non resident buyer is need of the time. Government wants solution and can say with surety if introduced, the market may or may not crash but the ever rising house price will stop and is needed as this house bubble is not only bad for first time buyer but also for eceonomy. As this bubble is fuelled by overseas buyer. Wait for the next data but condition is, it should be done properly that is citizen and resident should be seperated with overseas buyer n also also students and people on short term work visa as everyone knows that prooert is bought through students funded by family from overseas to avoid hiving tgeir local ird number.

Far too complicated and inefficient, I don't think Kiwis want to live in a tax web like that. If house prices are of particular concern the main thing Key and Co need to do is prevent foreigners grabbing our choice freehold housing. If doing so breaks some FTA clause that isn't the end of the world and can surely be tidied up in arrears.

I suspect people will think yes I have accumulated my capital and paid tax along the way, and now I'm going to be taxed again for my prudence. Gareth makes no distinction between historic capital amassed by tax-free speculation versus hard tax-paid graft yet proposes to tax both alike. That is hardly fair and is the fatal flaw in his scheme. It's just not swallowable. Top marks for trying though, good to see some new thoughts coming through.

Ha, trade me 25% of his wealth? How about adding to that the majority of his funds under management to help him sell his investment business for millions, I’d say it is the majority. His son made the money while Gareth holds onto socialist ideals which nobody is interested in now. The world has moved on but Gareth the redeemer has not.

Home ownership rates will decline under GM's taxation policy.

The trouble with all tax legislation is that there is always a group who will undertake the compliance required or set up the correct structure etc.....and then there are always the people who find all this legislated compliance to much to deal with.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.