By David Hargreaves

If you've thought in the past 10 years that your housing costs have been rising faster than your income - then you are probably right.

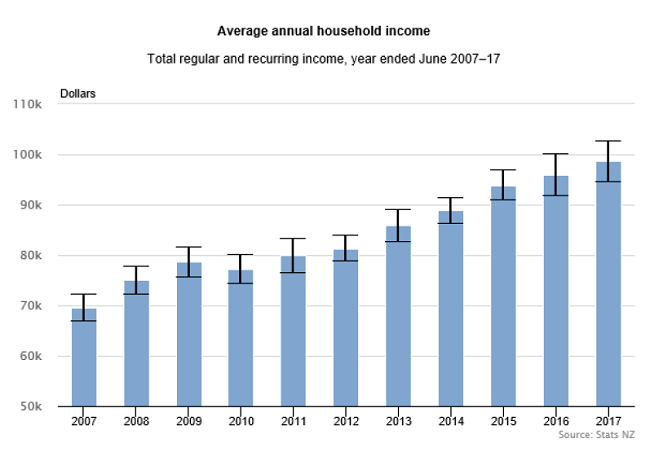

Statistics New Zealand's new household income and housing costs figures for the year to June show that in the past 10 years housing cost rises did indeed outstrip increases in household income.

In fact in that period household income rose 42% while annual housing costs increased by some 50.5%. Both increases have been more than twice the rate of inflation over the same period.

Since 2007, average annual household income is up nearly $30,000 to reach $98,621 (before tax) in 2017.

But over the same 10 years, average annual housing costs increased from $10,658 to $16,037. Inflation, as measured by the consumers price index, increased 20.2%.

But the news is slightly better when looked at over just the past year - which of course has seen house price increases moderate.

In the year ended June 2017, average weekly housing costs were $318.50, almost unchanged from 2016. Lower mortgage interest rates helped to largely dampen any increases in housing costs.

Average mortgage interest payments were significantly lower for the June 2017 year (down 11.6% to $250.80 a week), falling from $283.70 a week for the year ended June 2016.

Of course, more recently, mortgage interest rates have started to edge up again as the banks respond to funding pressures through declining rates of deposit uptake.

Stats NZ said renters were almost three times as likely as home owners to spend 40% or more of their household income on housing costs.

For the June 2017 year, about one in five (20.8%) renting households spent 40% or more of their household income on rent and other housing costs.

In contrast, fewer than one in 10 (7.8%) of people who owned, or partly owned, their own home spent 40% or more of their household income on housing costs.

Key facts

In the 10 years to June 2017:

► average annual household income (from all regular sources) increased 42%, to reach $98,621 for the year ended June 2017

► average weekly housing costs increased 52%, to reach $318.50 for the year ended June 2017.

For the year ended June 2017:

► average annual personal income was $51,945, up 7.7% from 2016

► average annual personal income for females increased at a much higher rate (9.2%) than for males (6.7%), when compared with 2016

► for every $100 of household income, New Zealand households spent an average of $16.40 on housing costs

► about 1 in 8 (12.5%) households spent 40% or more of their total household income on housing costs

► 65% of respondents reported their income was enough or more than enough to meet their everyday needs, while 10% stated they didn’t have enough to get by

► 82% of respondents said they were satisfied or very satisfied with their life in general.

47 Comments

David, could you please answer this question - the Reserve Bank and Government et al harp on and on about inflation and keeping it within a certain band, but as a layman in the world of Macro Economics, why are not rents and mortgage repayments taken into account in these figures ? Thank you CH

It is a vexed issue. The simplistic answer is that property is regarded as an "asset" so payments, certainly mortgage payments, are an "investment" and fall outside the gamut of inflation. They have this argument/discussion around the world as to whether there's a better way of capturing housing costs in inflation. Thanks for the question and I may have an opine on this subject at some stage.

It is a vexed issue. The simplistic answer is that property is regarded as an "asset" so payments, certainly mortgage payments, are an "investment" and fall outside the gamut of inflation. They have this argument/discussion around the world as to whether there's a better way of capturing housing costs in inflation. Thanks for the question and I may have an opine on this subject at some stage.

Thanks for pointing that out David, The CPI as a construct is woefully outdated, but also shows the resistance our institutions and ideologues have towards addressing the fundamental issues with bubble economics; how the CPI impacts on individuals and / or h'holds instead of a broader aggregate; and the acceptance of measurements that make policy formulation more difficult.

What we don't know is what really goes on behind the scenes. Central bankers and politicians probably have an inkling that the housing costs component of the CPI doesn't reflect the reality for many segments of the population. I have suggested that it's probably better that they use a range of different measures for price levels, depending on their objectives. But whichever way you want to frame it, trying to remove increases in the sticker prices of the most expensive cost in most peoples' lifetimes is not going to be representative of reality.

It might be an investment for the bank but is it really an investment for the borrower, especially the owner occupier?

A simple calculation:

Assume a $500k house 100% financed at 4.5% over 30 years and 2% inflation pa. At the end of 30 years the house price has almost doubled but the interest paid will be more than the gain. Add rates, insurance, maintenance etc over the 30 years and where's the return on that investment? There might be a $900k lump sum in the hand but where does that go if all other houses have doubled as well?

@meh You have failed to account for the rent you would have paid by not owning. But the point is that if you buy land (build costs are modeled) then that is an asset and its gains or losses are your problem.

@David Hargreaves the CPI does include rents and the cost of building...

Read what he wrote - He never said they didn't.

@nymad

Crazy horse said: David, could you please answer this question - the Reserve Bank and Government et al harp on and on about inflation and keeping it within a certain band, but as a layman in the world of Macro Economics, why are not rents and mortgage repayments taken into account in these figures ? Thank you CH

David said:

It is a vexed issue. The simplistic answer is that property is regarded as an "asset" so payments, certainly mortgage payments, are an "investment" and fall outside the gamut of inflation. They have this argument/discussion around the world as to whether there's a better way of capturing housing costs in inflation. Thanks for the question and I may have an opine on this subject at some stage.

So i pointed out to David that in fact housing is costed in the sense of rent and building.

Semantics, then.

The simplistic answer is that property is regarded as an "asset" so payments, certainly mortgage payments, are an "investment" and fall outside the gamut of inflation.

Emphasis on "certainly mortgage payments".

In order to help Crazy Horse understand CPI David should clarify for him that rent and build costs are in CPI. There is a myth building that rent is not included for example. Mortgage payments thus are partially included both via rent as a proxy and more notably via build costs.

Thanks for the contributions. Can I suggest reading this link for the nitty gritty. It explains it all better than I could in a brief comment. As I say, I may do a column on this subject at some point.

@Crazy Horse Rent and building costs are in the CPI:

Actual rentals for housing: 2002 - 5.54, 2006 - 6.87 2008 - 7.85

Home ownership: 2002 - 8.47, 2006 - 4.66, 2008 - 5.51

Purchase of new housing: 2002 - 8.47, 2006 - 4.66, 2008 - 5.51

I am surprised that average household incomes rose as much as 42% since 2007 ............ that did not happen in our household , our increase in gross income from employment has been more like 25%, although we are way above the average .

I guess we are all different , so averages often dont tell the full story .

What I have seen is asset prices explode in the past 10 years , but oddly enough the dividend yields on those assets has been roughly static and interest income on savings and cash has fallen .

Our Household has one more person (returned from O/S) 'increasing' our income. It would be interesting to see how the Size of Households 2007, compares with today, especially as the Flood of Kiwis heading to Aussie in 2007 has completely reversed. How many are now back with family as a result?

What Landlords don't seem to realize is that the more you increase your rents the less affordable it is for people to live in an area. This impacts on business since they have higher running costs due to having to support higher wages for employees can remain in expensive rental areas.

Eventually the legitimate business close and you're quite literally left with no one to pay your exorbitant rents.

Is called cummuting, as by your logic then nobody could live in London or New York

Huh, you think London and NY are low wage economies?

NY and London have high wage economies, CJ's logic suggests that is the requirement for having high rents. I'd agree with CJ.

Yes you are correct Unaha-closp. :) The more we drive up rents (And property prices) the harder it is for industries to compete in a global economy. Something has to unravel at some stage and that's why prices need to drop to affordable levels, otherwise we'll be faced with a recession that we can't recover from.

Yes I have already stated the idiocy of National pushing for a low wage economy while allowing house prices only suitable for a high wage economy. And the Greens get called stupid!

CJ099 so right

Right now Amazon is sorting through 100 Nth American cities proposals for Amazons 2nd Head Office outside Seattle. One of the top criteria is Affordable Housing

The facts are obvious even in NZ witness Queenstown where there’s no cheap housing for the workers

Workers have to find accommodation outside etc

High rents do not translate to being good for business To attract talent salary packages must be increased

A friend of mine is wanted by a large insurance co yet won’t come to NY unless he gets a substantial salary increase for obvious reason he will need to rent a very expensive apartment in the city

Do you think advertising execs in London get paid much, what about bar staff at the local inner city pub in NYC?

Which Keywest are you ? The real Keywest Fl ?

I tip average bar staff 15% more if I get extras

Got to go downstairs to the home theatre

Bye

Wow, CJ... just wow, and you will no doubt have the masses agreeing with you

@CJ099 Nonsense. Increased rents leads to increased profits, leads to increased spending which replaces the lost spending. A small portion is siphoned offshore which sucks but the bulk of your argument is based on bunk economics. It also implies, correctly, some amount of increased wealth disparity which also sucks and frankly thats the main problem, not some nonsense theory about rents draining business lol.

"Increased rents leads to increased profits"

Paying higher costs does not increase profits, in my experience.

The flood of Kiwis heading to Aussie has not reversed it has reduced. The Herald headlines were also completely wrong yesterday

Not by my calculations, a ponsonby villa bought in 2007 would have cost in money at that time more than it costs to service that same one now, we had 10% interest rates in 2007, now we have 4.5%, much cheaper now than in 2007 to own a house, work it off 900k 2007 and 1.7m today

How many years of rent payments did it take to save the deposit, too?

True, but that's too smart for most to understand

True, but that's too smart for most to understand

The cost of servicing debt is cheaper? So what? It's a furphy and complete nonsense.

People aren’t crying out due to the servicing costs of a mortgage, they are crying out because it’s nigh on impossible for them to save for a 6 figure deposit whilst renting.

We might need to stop measuring on house price to income ratios and start looking at deposit to income ratios.

keywest then you would have been really well off in 2005 and 2009. Interest rates were low then

Whats your point? To say it costs more to service a household more now is not true. It was a lot harder in 2007 / 2008 when interest rates were through the roof. 8.5% was the norm and we got paid 45% less per the article above.

The big picture though is that Interest rates have had to decrease & STAY DOWN to keep things in some sort of (temporary) working order. This is what a shrinking net energy pie does...

Our whole financial system is based on future promises and compensation in the form of interest/dividends/ capital gains for the delay in cashing in a promise ...this is the way the carrot works, to pull finance forward. So if interest returns are having to be manipulated lower to keep the system working its a terrible sign re the future's ability to pay

"average annual personal income was $51,945, up 7.7% from 2016"

That is absolutely huge, yet most complain that wages are not growing because of high immigration

"Average"

In our neoliberal world the elites are gaining super massive increases while the workers are getting next to nothing, thus averages tell us nothing.

It's the result of a survey. How many elites do you think were included? Maybe the 1% the Left prattle on about?

It would only take one housing specuvestor to completely screw the survey. And if they were surveying persons at home they would have an excellent chance of getting one. You lot don't appear to be out there working much.

So this report is a Survey? A set of questions asked of a 'random' set of participants?

http://www.stats.govt.nz/survey-participants.aspx

Tell me how many people understate their income in a survey! It's human nature to 'make yourself look/feel' good by being generous.....

That would explain why 82% of respondents said they were satisfied or very satisfied with their life in general

@nymad

Crazy horse said: David, could you please answer this question - the Reserve Bank and Government et al harp on and on about inflation and keeping it within a certain band, but as a layman in the world of Macro Economics, why are not rents and mortgage repayments taken into account in these figures ? Thank you CH

David said:

It is a vexed issue. The simplistic answer is that property is regarded as an "asset" so payments, certainly mortgage payments, are an "investment" and fall outside the gamut of inflation. They have this argument/discussion around the world as to whether there's a better way of capturing housing costs in inflation. Thanks for the question and I may have an opine on this subject at some stage.

So i pointed out to David that in fact housing is costed in the sense of rent and building.

Have to love stats, I would have liked to see wage growth, hours worked, number of people working in household and last but not least accomodation benefit. I arrived here 10'years ago land owners who haven't borrowed to heavily are doing well. Everyday workers who rent are working longer for less. but then so are people with multiple mortgages.

The article quotes averages, not medians. The median household income has risen from $57,198 in 2007 to $76,483 in 2017, a 34% rise. If the average has risen 42%, that is a sign of rising inequality. Inflation was 21% over the period so real median household incomes have risen 1% per year.

Now, I wonder why they put averages in the press release when the original report also includes medians?

Big woop, in actual dollar terms, income gains have far outstripped housing costs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.